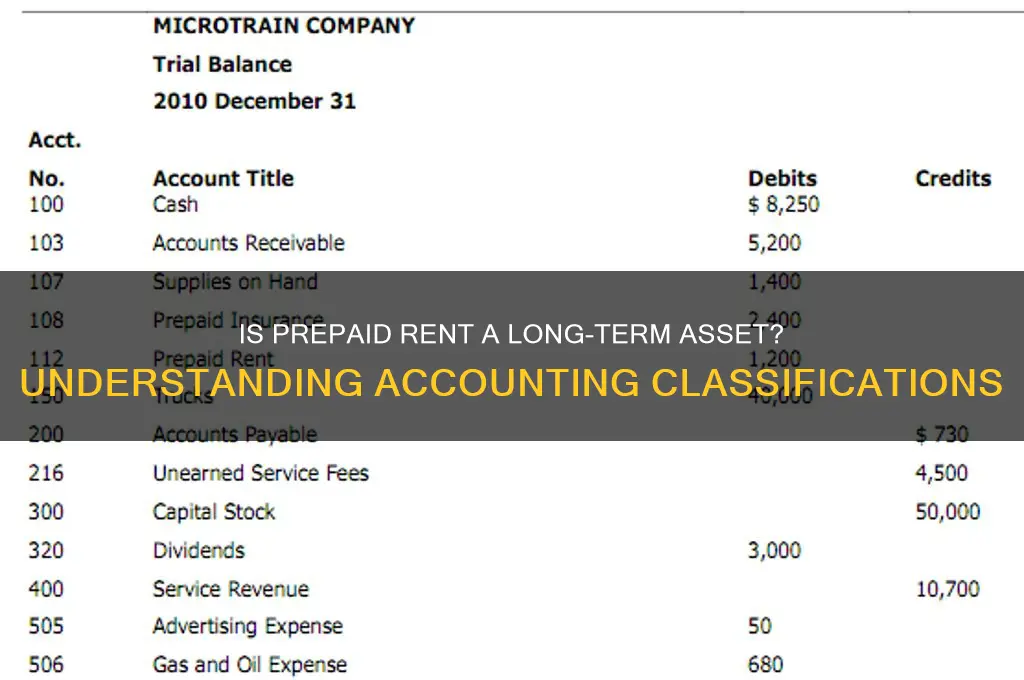

Prepaid rent is a common accounting concept that refers to rent payments made in advance for a specific period, typically beyond the current accounting period. While it represents a future economic benefit, the classification of prepaid rent as a long-term asset is a subject of debate. According to generally accepted accounting principles (GAAP), prepaid rent is generally considered a current asset because it is expected to be consumed or used up within one year or the operating cycle, whichever is longer. However, in certain cases, if the prepaid rent covers a period extending beyond one year, it may be classified as a long-term asset, subject to specific accounting treatments and disclosures. Understanding the nature and classification of prepaid rent is crucial for accurate financial reporting and analysis, as it impacts a company's balance sheet, income statement, and overall financial health.

| Characteristics | Values |

|---|---|

| Classification | Current Asset (not a long-term asset) |

| Definition | Payment made in advance for rent covering a future period, typically within one year |

| Accounting Treatment | Recorded as an asset on the balance sheet until the rent period is consumed |

| Recognition | Recognized when payment is made, not when rent is due |

| Amortization | Expensed over the rental period (e.g., monthly) as rent expense |

| Reporting | Listed under current assets in the balance sheet |

| Time Horizon | Typically covers a period of less than one year |

| Liquidity | Considered liquid as it will be used within a short period |

| Examples | Paying 6 months of rent in advance for office space |

| Tax Treatment | Generally not deductible until the rent period is consumed |

| Impact on Financial Statements | Reduces cash initially, then gradually reduces prepaid rent and increases rent expense over time |

Explore related products

$9.99 $9.99

What You'll Learn

- Prepaid Rent Definition: Understanding prepaid rent as an advance payment for future occupancy

- Asset Classification: Determining if prepaid rent qualifies as a long-term asset

- Current vs. Long-Term: Differentiating between current and long-term asset categorization

- Accounting Treatment: How prepaid rent is recorded and reported in financial statements

- Time Threshold: The role of the one-year time frame in asset classification

![]()

Prepaid Rent Definition: Understanding prepaid rent as an advance payment for future occupancy

Prepaid rent is a concept that often puzzles those unfamiliar with accounting principles, yet it’s a straightforward transaction in practice. At its core, prepaid rent is an advance payment made by a tenant to a landlord for the use of a property in the future. This payment is recorded on the tenant’s balance sheet as an asset because it represents a right to future occupancy, not an immediate expense. For instance, if a business pays $12,000 upfront for a year’s rent, only $1,000 is expensed each month, while the remaining balance is treated as a prepaid asset. This method aligns with the matching principle in accounting, ensuring expenses are recognized when the benefit is received.

To understand why prepaid rent is classified as an asset, consider its nature and timing. Unlike a typical expense, prepaid rent provides a future benefit—the right to occupy a space over a specified period. This characteristic distinguishes it from immediate costs like utilities or supplies. For example, a retail store paying six months’ rent in advance gains the asset of future occupancy, which is gradually expensed as each month passes. This treatment ensures financial statements accurately reflect the business’s obligations and resources, providing a clearer picture of its financial health.

One common misconception is that prepaid rent is always a long-term asset. While it can be, its classification depends on the payment’s duration and the reporting period. If the prepaid rent covers a period beyond the next 12 months, it is typically categorized as a long-term asset. However, if it spans only a few months, it remains a current asset. For instance, a company prepaying rent for 18 months would split the amount: the portion covering the next 12 months is current, while the remaining six months is long-term. This distinction is crucial for accurate financial reporting and analysis.

Practical management of prepaid rent requires meticulous record-keeping and periodic adjustments. Businesses should maintain a prepaid rent schedule to track the unexpired portion of the payment and ensure it’s amortized correctly. For example, a quarterly review can help identify discrepancies and align the asset’s value with the actual benefit received. Additionally, using accounting software can automate this process, reducing the risk of errors. By treating prepaid rent with precision, companies can maintain compliance with accounting standards and make informed financial decisions.

In conclusion, prepaid rent serves as a bridge between present payment and future occupancy, embodying the principles of accrual accounting. Its classification as an asset—whether current or long-term—hinges on the duration of the benefit it provides. By understanding and managing prepaid rent effectively, businesses can ensure their financial statements accurately reflect their commitments and resources. This clarity not only aids internal decision-making but also fosters trust among stakeholders, reinforcing the importance of this seemingly simple accounting concept.

Where to Rent Lockers for Bus Travel: A Comprehensive Guide

You may want to see also

Explore related products

$51.58 $55

![]()

Asset Classification: Determining if prepaid rent qualifies as a long-term asset

Prepaid rent, by definition, represents advance payments for future occupancy. Its classification as a long-term asset hinges on the duration of the rental period and accounting principles. While it involves a future benefit, its treatment differs from traditional long-term assets like property or equipment. Understanding this distinction is crucial for accurate financial reporting and analysis.

Analyzing the Criteria

Accounting standards, such as GAAP and IFRS, classify assets based on their expected useful life and liquidity. Long-term assets are typically those with a useful life exceeding one year, while current assets are expected to be consumed or converted to cash within a year. Prepaid rent, though extending beyond the current period, often falls short of meeting the one-year threshold for long-term classification. For instance, a six-month prepaid lease would be considered a current asset, despite its future benefit.

The Role of Materiality

Materiality plays a significant role in asset classification. Even if a prepaid rent agreement spans multiple years, its value relative to the company's overall assets may be immaterial. In such cases, treating it as a current asset simplifies financial reporting without materially misrepresenting the company's financial position. However, for substantial prepaid rent agreements, a more nuanced approach is warranted.

Practical Considerations

In practice, companies often adopt a pragmatic approach. If a prepaid rent agreement covers a period exceeding one year and is material, it may be classified as a long-term asset, with the portion applicable to the current year recognized as a current asset. This hybrid approach ensures compliance with accounting standards while providing a more accurate representation of the company's financial obligations.

Ultimately, determining whether prepaid rent qualifies as a long-term asset requires a contextual analysis. Factors such as the rental period, materiality, and accounting framework must be considered. While prepaid rent typically falls under current assets, exceptions exist for significant, long-term agreements. By carefully evaluating these factors, businesses can ensure accurate financial reporting and informed decision-making.

Choosing the Right Wet Tile Saw Rental for Your Project

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![]()

Current vs. Long-Term: Differentiating between current and long-term asset categorization

Prepaid rent often sparks confusion in asset categorization. While it represents a future benefit, its classification as current or long-term hinges on a critical factor: the operating cycle of the business. This distinction is more than semantic; it directly impacts financial statements and investor perception.

Misclassification can distort liquidity ratios, misleading stakeholders about a company's short-term financial health.

Understanding the Operating Cycle:

The operating cycle, the time it takes to convert inventory into cash, serves as the dividing line. Assets expected to be converted to cash or used up within one operating cycle or one year (whichever is longer) are classified as current. Think of prepaid rent for a retail store's monthly lease. If the operating cycle is three months, rent prepaid for the next month falls within the current cycle and is therefore a current asset.

Conversely, rent prepaid for a year-long lease on a warehouse, exceeding the typical operating cycle, would be classified as a long-term asset.

Practical Considerations:

Imagine a tech startup with a 6-month operating cycle. They prepay six months of rent for their office space. Despite the payment covering a period longer than a year, it falls within their operating cycle, making it a current asset. This example highlights the importance of understanding the specific context of each business.

Additionally, companies should disclose their operating cycle length in financial statements to ensure transparency and accurate interpretation.

Beyond the Basics:

While the operating cycle is the primary determinant, exceptions exist. Certain prepaid expenses, like insurance premiums spanning multiple years, may be classified as long-term assets even if they partially fall within the operating cycle. This is because they provide benefits over an extended period, aligning with the definition of long-term assets.

Takeaway:

Distinguishing between current and long-term assets is crucial for accurate financial reporting. Prepaid rent, a seemingly straightforward concept, requires careful consideration of the operating cycle and the specific circumstances of the business. By understanding these nuances, businesses can ensure their financial statements accurately reflect their financial position and performance.

Crafting a 5-Star Renter Review: Tips for Honest and Helpful Feedback

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![]()

Accounting Treatment: How prepaid rent is recorded and reported in financial statements

Prepaid rent represents a unique accounting challenge, as it straddles the line between an asset and an expense. When a business pays rent in advance, it initially records the transaction as an asset on the balance sheet, reflecting the future economic benefit of using the rented space. However, as time passes and the rent period is consumed, the asset is gradually reclassified as an expense on the income statement. This dual nature requires precise accounting treatment to ensure financial statements accurately represent the company’s financial position and performance.

Recording prepaid rent begins with a journal entry that debits the prepaid rent account (an asset) and credits cash or the payment method used. For example, if a company pays $12,000 for six months of rent in advance, the entry would be: *Debit Prepaid Rent $12,000, Credit Cash $12,000*. This entry acknowledges the upfront payment as an asset, as the company has not yet utilized the full benefit of the rent. As each month passes, the company must recognize the portion of rent consumed, typically through a monthly adjusting entry. For instance, $2,000 would be debited to Rent Expense and credited to Prepaid Rent each month, reducing the asset balance while expensing the used portion.

The reporting of prepaid rent in financial statements varies depending on the time horizon of the prepayment. If the prepaid rent covers a period of one year or less, it is classified as a current asset on the balance sheet, aligning with the short-term nature of the benefit. However, if the prepayment extends beyond one year, the portion applicable to the period beyond one year is often separated and reported as a long-term asset. This distinction is crucial for stakeholders, as it affects liquidity ratios and the perception of the company’s short-term financial health. For example, a $24,000 prepayment for two years of rent would be split: $12,000 under current assets and $12,000 under long-term assets.

A common pitfall in accounting for prepaid rent is inconsistent application of the matching principle, which requires expenses to be recognized in the period they are incurred. Companies must ensure that the amortization of prepaid rent aligns with the actual usage of the rented space. For instance, if a company pays rent quarterly but records it monthly, the financial statements may misrepresent both expenses and assets. To avoid this, businesses should establish clear policies for recognizing prepaid rent, such as using a straight-line method or aligning with lease terms. Auditors often scrutinize these entries, so accuracy and consistency are paramount.

In conclusion, the accounting treatment of prepaid rent hinges on proper classification, timely recognition, and adherence to accounting principles. By recording prepaid rent as an asset initially and systematically expensing it over time, companies ensure their financial statements reflect both the preservation of resources and the consumption of benefits. Whether classified as a current or long-term asset, prepaid rent provides insight into a company’s financial commitments and resource management. Mastering this treatment not only enhances financial accuracy but also builds trust with investors and stakeholders.

Understanding Arizona Rental Tax Rates: A Comprehensive Guide for Landlords

You may want to see also

Explore related products

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

![]()

Time Threshold: The role of the one-year time frame in asset classification

The one-year time frame is a critical dividing line in accounting, separating current assets from long-term assets. This threshold is rooted in the liquidity principle: assets expected to be converted to cash or used up within one year or one operating cycle (whichever is longer) are classified as current. Prepaid rent, a common example, often falls into a gray area. If a company prepays rent for a 12-month lease, it is typically classified as a current asset because the benefit is consumed within the one-year window. However, if the prepaid rent extends beyond one year, it may be split, with the portion expiring within the year classified as current and the remainder as long-term.

Consider a scenario where a retail business prepays $24,000 for a two-year lease. Under the one-year rule, $12,000 (the first year’s rent) would be recorded as a current asset, while the remaining $12,000 would be classified as a long-term asset. This bifurcation ensures that financial statements accurately reflect the timing of resource consumption. The rule is not arbitrary; it aligns with the need for stakeholders to assess short-term liquidity and long-term financial health. For instance, a lender evaluating a company’s ability to meet immediate obligations would focus on current assets, while an investor might scrutinize long-term assets for growth potential.

Critics argue that the one-year threshold can sometimes oversimplify asset classification, particularly in industries with unique operating cycles. For example, a construction company with a multi-year project might prepay rent for an office space for three years. While the one-year rule would split the prepaid rent, the entire amount is directly tied to the project’s lifecycle. In such cases, strict adherence to the rule may not fully capture the asset’s operational relevance. However, the one-year threshold remains a practical standard, balancing simplicity with utility for most businesses.

To navigate this threshold effectively, businesses should adopt a proactive approach. First, analyze lease agreements to determine the exact duration of prepaid rent. Second, align asset classification with the company’s operating cycle, especially if it exceeds one year. Third, disclose any deviations from the one-year rule in financial notes to maintain transparency. For instance, if a company classifies a 15-month prepaid rent entirely as current, it should explain the rationale, such as the rent being consumed within the operating cycle. This ensures compliance with accounting standards while providing clarity to users of financial statements.

In conclusion, the one-year time frame is more than a technicality—it is a cornerstone of asset classification that influences financial reporting and decision-making. While it may not fit every scenario perfectly, its widespread application ensures consistency and comparability across industries. Understanding and applying this threshold correctly is essential for accurately portraying a company’s financial position, whether prepaid rent is involved or other assets straddling the one-year line.

Renting a Bus Station Locker: A Step-by-Step Guide

You may want to see also

Frequently asked questions

No, prepaid rent is typically classified as a current asset because it represents rent paid in advance for a period of one year or less.

Prepaid rent is recorded as a current asset because the benefit is consumed within the operating cycle (usually one year), regardless of the lease term.

Rarely. It may be classified as long-term only if the prepaid period extends beyond one year and the company’s operating cycle is longer than 12 months.

Prepaid rent is reported under current assets as it represents a short-term benefit that will be used within the next year.