Prepaid rent is a common accounting concept that often raises questions regarding its classification as either revenue or expense. Essentially, prepaid rent refers to the payment made in advance for the use of a property or space over a specified period. From an accounting perspective, it is typically treated as an asset rather than revenue or expense initially, as it represents a future economic benefit. However, as the rental period progresses, the prepaid rent is gradually recognized as an expense through amortization, reflecting the consumption of the asset over time. Understanding the proper classification and treatment of prepaid rent is crucial for accurate financial reporting and analysis.

| Characteristics | Values |

|---|---|

| Classification | Prepaid rent is classified as an asset, not a revenue or expense. |

| Nature | It represents advance payment for future rent, recorded on the balance sheet. |

| Recognition | Initially recorded as a debit to Prepaid Rent (asset) and a credit to Cash (asset). |

| Expense Recognition | Gradually recognized as a rent expense over the rental period via amortization. |

| Revenue Impact | No direct impact on revenue; it is unrelated to income generation. |

| Accounting Standard | Follows accrual accounting principles (e.g., GAAP, IFRS). |

| Financial Statement Location | Reported as a current asset on the balance sheet until expensed. |

| Tax Treatment | Generally not deductible until the rental period is realized. |

| Example | Paying $12,000 for a year's rent in advance; $1,000 is expensed monthly. |

| Purpose | Ensures matching principle by aligning expenses with the period benefited. |

Explore related products

What You'll Learn

- Prepaid Rent Definition: Understanding prepaid rent and its accounting treatment in financial statements

- Classification as Asset: Why prepaid rent is classified as an asset, not revenue or expense

- Expense Recognition: How prepaid rent is recognized as an expense over time

- Impact on Financial Statements: Effects of prepaid rent on the balance sheet and income statement

- Accounting Treatment: Journal entries for prepaid rent and amortization process

![]()

Prepaid Rent Definition: Understanding prepaid rent and its accounting treatment in financial statements

Prepaid rent is a concept that often puzzles those new to accounting, primarily because it doesn’t neatly fit into the categories of revenue or expense at first glance. In essence, prepaid rent occurs when a business pays for the use of a property in advance, typically for a period extending beyond the current accounting cycle. This payment is not immediately recognized as an expense but is instead recorded as an asset on the balance sheet. The rationale is straightforward: the business has paid for a future benefit, and until that benefit is realized, the payment retains its value as an asset.

To understand its accounting treatment, consider the following steps. First, when the rent is prepaid, it is recorded as a debit to the prepaid rent account (an asset) and a credit to cash. This reflects the exchange of cash for a future service. Second, as the rental period progresses, the prepaid rent is gradually expensed. For example, if a company prepays $12,000 for a year’s rent, $1,000 is recognized as rent expense each month, with a corresponding reduction in the prepaid rent asset. This method aligns with the matching principle, ensuring expenses are recognized in the period they benefit.

A common misconception is that prepaid rent could be classified as revenue, but this is incorrect. Revenue is earned through the sale of goods or services, whereas prepaid rent is a cost paid in advance. Its nature is purely an expense over time, not a source of income. For instance, a retail store prepaying rent for its storefront does not generate revenue from this transaction; it merely secures the right to use the property.

The treatment of prepaid rent also varies slightly between cash and accrual accounting. In cash accounting, the expense is recognized when the payment is made, which can distort financial statements if large prepayments are involved. Accrual accounting, however, spreads the expense over the rental period, providing a more accurate representation of financial health. For businesses, this distinction is critical, as it impacts profitability metrics and tax obligations.

In conclusion, prepaid rent is neither revenue nor an immediate expense but an asset that transforms into an expense over time. Its accounting treatment requires careful tracking and periodic adjustments to reflect its consumption. By understanding this, businesses can maintain accurate financial records and make informed decisions. Practical tips include using accounting software to automate expense recognition and regularly reviewing prepaid accounts to ensure compliance with accounting standards.

Recharge and Re-Engage: Smoothly Transitioning Back to Work Post-Vacation

You may want to see also

Explore related products

![]()

Classification as Asset: Why prepaid rent is classified as an asset, not revenue or expense

Prepaid rent is not immediately recognized as an expense because it represents a payment for a future benefit. When a business pays rent in advance, it gains the right to use a property over a specified period, typically a month or more. This future usage is a resource controlled by the entity, aligning with the definition of an asset under accounting principles. Unlike an expense, which reflects a cost incurred for past benefits, prepaid rent signifies a cost paid upfront for benefits yet to be received. This distinction is critical for accurate financial reporting, ensuring that expenses are matched with the periods in which the related benefits are consumed.

To illustrate, consider a small business that pays $12,000 in January for a year’s worth of rent. Recording this entire amount as an expense in January would distort the financial statements, as the business has not yet utilized the full year’s occupancy. Instead, the $12,000 is initially recorded as a prepaid rent asset. Each month, $1,000 is recognized as rent expense, reflecting the portion of the prepaid rent consumed. This method adheres to the accrual accounting principle, which emphasizes matching expenses with the periods in which the related revenues are earned. By classifying prepaid rent as an asset, businesses maintain a more accurate representation of their financial position and performance.

Classifying prepaid rent as an asset also ensures compliance with accounting standards, such as the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). These frameworks require assets to be recognized when an entity controls a resource expected to generate future economic benefits. Prepaid rent meets this criterion, as it provides the business with the right to use a property in the future. In contrast, revenue and expenses are recognized based on different criteria—revenue when earned and expenses when incurred. Prepaid rent does not fit these definitions, further reinforcing its classification as an asset.

A practical tip for businesses is to maintain a prepaid rent schedule to track the amount paid in advance and the portion expensed each period. This schedule helps ensure consistency in financial reporting and simplifies the year-end closing process. For example, if a company prepays $6,000 for six months of rent, the schedule would show $1,000 expensed monthly, with the prepaid rent asset balance decreasing accordingly. This approach not only enhances accuracy but also provides transparency for stakeholders reviewing the financial statements.

In summary, prepaid rent is classified as an asset because it represents a payment for future benefits, aligns with accounting principles, and ensures accurate financial reporting. By distinguishing it from revenue and expenses, businesses can maintain a clear and truthful depiction of their financial health. This classification is not merely a technicality but a fundamental aspect of sound accounting practice, enabling stakeholders to make informed decisions based on reliable financial data.

Easy Steps to Return Clothes to Rent the Runway

You may want to see also

Explore related products

![]()

Expense Recognition: How prepaid rent is recognized as an expense over time

Prepaid rent is not an expense when paid; it’s an asset. This distinction is critical in accounting because it reflects the principle of matching expenses with the period in which they are incurred. When a business prepays rent, it records the payment as a debit to prepaid rent (an asset account) and a credit to cash. The expense recognition process begins only when the rented space is actually used. This is where the concept of amortization comes into play, transforming the prepaid asset into a recognized expense over time.

The recognition of prepaid rent as an expense follows a systematic approach. For example, if a company pays $12,000 for a year’s rent in advance, it doesn’t record a $12,000 expense immediately. Instead, it allocates $1,000 per month as rent expense, assuming a 12-month lease. This is done by debiting rent expense and crediting prepaid rent each month. The journal entry ensures that the financial statements accurately reflect the cost of using the rented space during the reporting period, aligning with the accrual accounting principle.

A key consideration in expense recognition is the consistency of the allocation method. Straight-line amortization is the most common approach, where the prepaid rent is evenly distributed over the lease term. However, if the rental agreement includes escalating payments or varying usage patterns, the allocation may need to be adjusted accordingly. For instance, if a retail business expects higher usage during peak seasons, it might allocate more expense to those months. This requires careful judgment and adherence to accounting standards like GAAP or IFRS.

Practical tips for managing prepaid rent include maintaining a detailed schedule of prepaid expenses to track remaining balances and ensure accurate monthly entries. Automation tools can streamline this process, reducing the risk of errors. Additionally, businesses should review lease agreements for any clauses that might affect expense recognition, such as rent holidays or variable payments. Proper documentation and periodic reconciliation of prepaid accounts are essential to avoid misstatements in financial reporting.

In conclusion, prepaid rent transitions from an asset to an expense through a structured recognition process. By systematically allocating the prepaid amount over the lease term, businesses ensure that their financial statements reflect the true cost of using rented space in the appropriate period. This approach not only complies with accounting principles but also provides a clearer picture of financial performance and resource utilization.

WIC Application Requirements: Mail, Rent, or Bills Needed?

You may want to see also

Explore related products

$24.99 $24.99

![]()

Impact on Financial Statements: Effects of prepaid rent on the balance sheet and income statement

Prepaid rent is not a revenue or an expense in the traditional sense but rather an asset that reflects a company’s advance payment for future rental obligations. This distinction is critical for understanding its impact on financial statements. When a business pays rent upfront for a period that extends beyond the current accounting cycle, it records the payment as a prepaid expense on the balance sheet. This entry increases the company’s current assets, reflecting its right to use the rented space in the future. For example, if a company pays $12,000 for a year’s rent in January, $10,000 is recorded as prepaid rent (an asset), and $2,000 is recognized as rent expense for the month.

The balance sheet is the first financial statement affected by prepaid rent. Initially, the asset account "Prepaid Rent" increases, while the cash account decreases, maintaining the accounting equation’s balance. Over time, as the rented period progresses, the prepaid rent is gradually expensed to the income statement. This process, known as amortization, ensures that expenses are matched with the revenue they help generate, adhering to the matching principle of accounting. For instance, if $1,000 of prepaid rent is expensed monthly, the asset account decreases by $1,000, and the rent expense account increases by the same amount each month.

On the income statement, prepaid rent affects the reported expenses and, consequently, net income. By spreading the prepaid rent expense over the rental period, the company avoids distorting its financial performance in any single period. This approach provides a more accurate representation of the company’s profitability. For example, if a company prepaid $6,000 for six months of rent, expensing $1,000 monthly ensures that each month’s income statement reflects only the portion of rent attributable to that period.

A comparative analysis highlights the importance of proper prepaid rent treatment. If a company were to expense the entire prepaid rent in the month of payment, it would overstate expenses and understate net income in that period, while understating expenses in subsequent periods. This misalignment could mislead stakeholders about the company’s financial health. Conversely, correctly amortizing prepaid rent ensures consistency and reliability in financial reporting, which is essential for decision-making by investors, creditors, and management.

In practical terms, businesses should establish clear policies for recording and amortizing prepaid rent. For instance, using accounting software to automate the amortization process can reduce errors and save time. Additionally, regular reviews of prepaid rent balances ensure accuracy and compliance with accounting standards. By understanding and correctly managing prepaid rent, companies can maintain transparent financial statements that accurately reflect their economic reality.

How Rent Influences Food Stamp Eligibility in Virginia

You may want to see also

Explore related products

![]()

Accounting Treatment: Journal entries for prepaid rent and amortization process

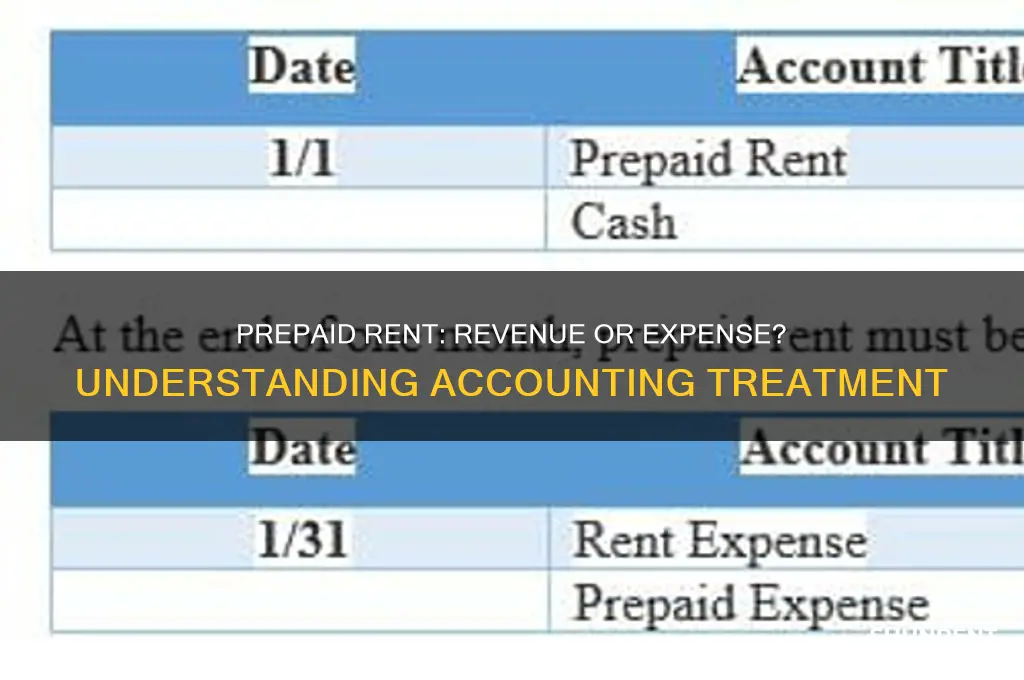

Prepaid rent is fundamentally an expense, not a revenue, because it represents a payment made in advance for the future use of a rented asset. This classification aligns with the matching principle in accounting, which ensures expenses are recognized in the period they are incurred, not when they are paid. For instance, if a company pays $12,000 annually for rent in January, only $1,000 is expensed each month, reflecting the cost of using the space during that period.

The accounting treatment for prepaid rent begins with a journal entry to record the initial payment. When rent is prepaid, the entry debits the Prepaid Rent account (an asset) and credits the Cash account. For example, if a company prepays $6,000 for six months of rent, the entry would be:

Debit: Prepaid Rent – $6,000

Credit: Cash – $6,000

This entry acknowledges the asset created by the prepayment, which will be used over time.

The amortization process systematically converts the prepaid rent asset into an expense as the rental period progresses. Each month, a portion of the prepaid rent is expensed to align with the matching principle. Using the previous example, the monthly amortization entry would be:

Debit: Rent Expense – $1,000

Credit: Prepaid Rent – $1,000

This reduces the prepaid rent asset while recognizing the expense in the appropriate period.

A critical caution in this process is ensuring consistency in the amortization schedule. Irregular or incorrect entries can distort financial statements, misrepresenting the company’s financial health. For example, expensing the entire prepaid amount in one period would overstate expenses and understate assets, violating accounting standards.

In conclusion, the accounting treatment for prepaid rent involves recognizing it as an asset initially and systematically expensing it through amortization. This approach ensures expenses are matched with the periods they benefit, maintaining accuracy and compliance in financial reporting. Practical tips include using accounting software to automate amortization schedules and regularly reviewing entries for errors.

Renting an English-Speaking GPS in Italy: Your Ultimate Travel Guide

You may want to see also

Frequently asked questions

Prepaid rent is considered an asset, not a revenue or an expense, as it represents advance payment for future rent obligations.

Prepaid rent is not classified as an expense because the benefit of the payment has not yet been fully consumed; it is recorded as an asset until the rent period is used.

Prepaid rent is initially recorded as a current asset on the balance sheet and then expensed over time as the rent period is utilized.

No, prepaid rent does not impact the income statement as revenue; it is only expensed when the rented period is consumed, reducing the asset and increasing expenses.