Prepaid rent is a common accounting concept that often raises questions regarding its classification. The debate centers on whether it should be categorized as a temporary account or a permanent one. Temporary accounts, also known as nominal accounts, are typically used to record transactions for a specific period and are closed at the end of an accounting cycle, transferring their balances to permanent accounts. In contrast, permanent accounts, or real accounts, maintain ongoing balances and are not closed. Prepaid rent represents advance payments made for future rental periods, and its treatment as a temporary or permanent account depends on the accounting principles and practices followed by a business, making it a nuanced topic in financial reporting.

| Characteristics | Values |

|---|---|

| Account Type | Asset |

| Classification | Current Asset (if short-term) |

| Duration | Temporary (for the period it covers) |

| Recognition | Recorded as an asset initially |

| Expense Timing | Expensed over the period benefited |

| Adjustment | Adjusted monthly through amortization |

| Balance Sheet | Reported under current assets |

| Income Statement | Impact reflected as rent expense |

| Purpose | Represents advance payment for future rent |

| Reversal | Reduced as rent is consumed |

| Tax Treatment | Matches expense with revenue recognition |

Explore related products

What You'll Learn

- Prepaid Rent Definition: Understanding prepaid rent as an advance payment for future rental periods

- Temporary vs. Permanent: Distinguishing temporary accounts from permanent ones based on reporting periods

- Accounting Treatment: How prepaid rent is recorded and adjusted in financial statements

- Balance Sheet Classification: Identifying prepaid rent as a current asset on the balance sheet

- Year-End Adjustments: The role of adjusting entries in reflecting prepaid rent accurately

![]()

Prepaid Rent Definition: Understanding prepaid rent as an advance payment for future rental periods

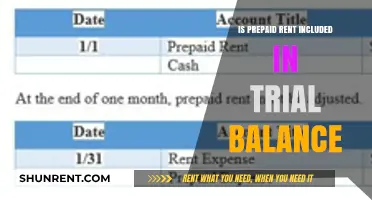

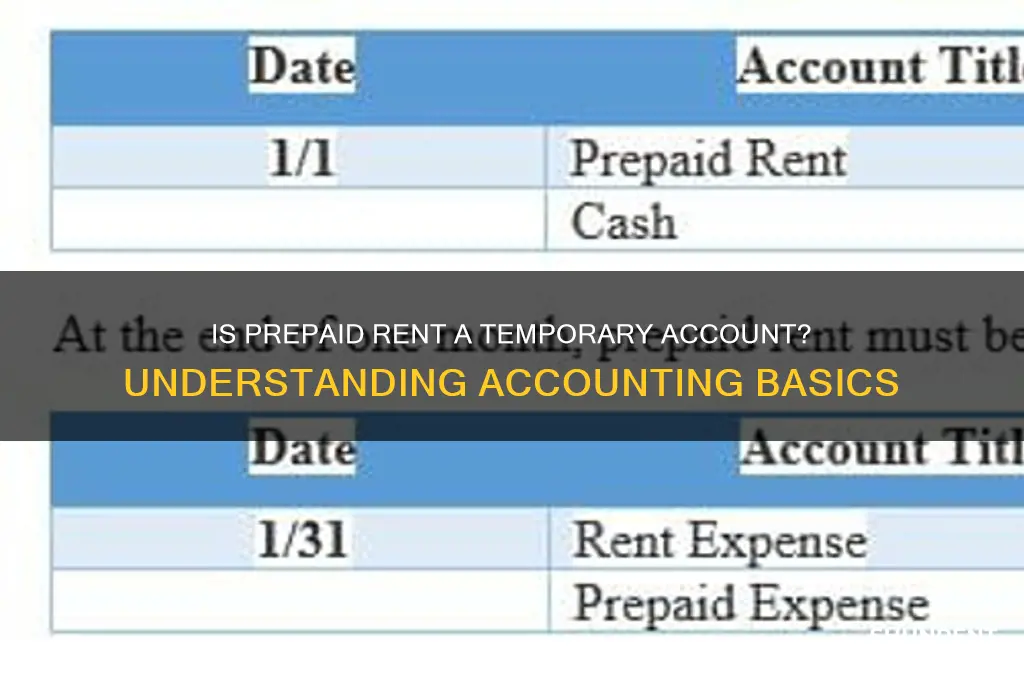

Prepaid rent is an accounting concept that represents a tenant’s advance payment for future rental periods. Unlike regular rent payments, which cover the current period, prepaid rent is recorded as an asset on the balance sheet because it reflects a future benefit the tenant has already paid for. For example, if a business pays $12,000 in January for a year’s rent, only $1,000 is expensed each month as rent, while the remaining balance is held as a prepaid asset. This treatment ensures that expenses are matched to the periods in which they are incurred, aligning with the accrual accounting principle.

The classification of prepaid rent as a temporary account is a point of contention. Temporary accounts, such as revenue and expense accounts, are closed at the end of an accounting period to reset their balances to zero. However, prepaid rent is typically classified as a current asset, not a temporary account, because it retains its balance until the prepaid period expires. For instance, if a company prepays $6,000 for six months of rent, the asset account is reduced by $1,000 each month as the expense is recognized, but the account itself remains active until the prepaid period ends.

To understand why prepaid rent is not considered temporary, consider its purpose and behavior. Temporary accounts are designed to capture transactions for a specific period and are reset periodically. In contrast, prepaid rent is a balance sheet item that reflects a resource expected to provide future economic benefits. It is adjusted monthly through amortization, not closed out entirely. For example, a prepaid rent account for $12,000 will decrease by $1,000 each month as rent expense is recognized, but the account remains until the full prepaid amount is expensed.

Practical implications of this classification are significant for businesses. Treating prepaid rent as a temporary account would lead to incorrect financial reporting, as it would imply the account is closed at year-end, erasing the remaining prepaid balance. Instead, businesses should maintain the prepaid rent account as a current asset, adjusting it monthly to reflect the portion of rent consumed. For instance, a small business that prepays $3,000 for three months of rent should record a $1,000 rent expense each month, reducing the prepaid rent asset accordingly.

In conclusion, prepaid rent is an advance payment for future rental periods, recorded as a current asset on the balance sheet. While it is adjusted monthly to recognize rent expenses, it is not considered a temporary account because it does not reset to zero at the end of an accounting period. Understanding this distinction is crucial for accurate financial reporting and compliance with accounting principles. By properly managing prepaid rent, businesses can ensure their financial statements reflect the true economic reality of their operations.

Is Renting a Modem from Comcast Necessary?

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![]()

Temporary vs. Permanent: Distinguishing temporary accounts from permanent ones based on reporting periods

Prepaid rent, a common accounting entry, often sparks confusion regarding its classification as a temporary or permanent account. To clarify, let's delve into the distinction between these account types based on reporting periods. Temporary accounts, such as revenue, expense, and dividend accounts, are reset to zero at the end of each accounting period, typically a fiscal year. This reset ensures that the next period's financial statements reflect only current activity, providing a clear picture of the company's recent performance. In contrast, permanent accounts, including assets, liabilities, and equity, carry forward their balances from one period to the next, offering a cumulative view of the company's financial position.

Consider the nature of prepaid rent: it represents an advance payment for a future benefit, typically rent for a specified period. From an accounting perspective, prepaid rent is initially recorded as an asset, reflecting the company's right to use the rented property in the future. As the rental period progresses, the asset is gradually expensed, reducing its balance. This process highlights a key characteristic of temporary accounts: their balances fluctuate with periodic activity. However, prepaid rent itself is not a temporary account; rather, it is a permanent account (asset) that is periodically adjusted through a temporary account (rent expense).

To illustrate, suppose a company pays $12,000 in January for a year's rent. The initial journal entry would debit Prepaid Rent (asset) and credit Cash for $12,000. Each month, $1,000 would be expensed by debiting Rent Expense (temporary account) and crediting Prepaid Rent (permanent account). By year-end, Prepaid Rent would be zero, but the account itself remains on the balance sheet, ready to record future prepayments. This example underscores the importance of understanding the interplay between temporary and permanent accounts in financial reporting.

A practical tip for distinguishing between these accounts is to examine their purpose and behavior over time. Temporary accounts are transactional, reflecting periodic activity that is closed out to retained earnings. Permanent accounts, on the other hand, are positional, providing a continuous record of the company's resources, obligations, and ownership. For instance, while rent expense is closed to retained earnings at year-end, prepaid rent continues to track future rental benefits. This distinction is crucial for accurate financial statement preparation and analysis.

In conclusion, prepaid rent is not considered a temporary account but rather a permanent asset account that interacts with temporary accounts during the reporting period. By recognizing the role of reporting periods in classifying accounts, accountants can ensure that financial statements accurately represent both current performance and long-term financial health. This nuanced understanding is essential for maintaining the integrity of financial reporting and informing strategic decision-making.

Renting Police Officers for Film: A Guide to Authentic On-Screen Policing

You may want to see also

Explore related products

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

![]()

Accounting Treatment: How prepaid rent is recorded and adjusted in financial statements

Prepaid rent is not considered a temporary account but rather an asset account, specifically a current asset. This classification stems from its nature as a payment made in advance for future benefits. When a business pays rent upfront, it records the transaction by debiting Prepaid Rent (an asset) and crediting Cash (an asset), reflecting the exchange of one asset for another. This initial entry ensures the balance sheet accurately represents the company’s resources. However, the accounting treatment doesn’t end there; adjustments are necessary to align expenses with the period in which they are incurred, adhering to the matching principle.

The adjustment process for prepaid rent involves recognizing the portion of the prepaid amount that pertains to the current accounting period as an expense. For example, if a company pays $12,000 for a year’s rent in January, $1,000 of that amount should be expensed each month. At the end of each month, an adjusting entry is made: debit Rent Expense (an expense account) and credit Prepaid Rent (the asset account). This reduces the prepaid rent balance while increasing rent expense, ensuring the income statement reflects the correct amount of rent incurred during the period. Over time, the prepaid rent account is depleted as the expense is recognized.

A critical aspect of this accounting treatment is its impact on financial statements. On the balance sheet, prepaid rent initially appears as a current asset, signaling liquidity and future benefits. As adjustments are made, the asset account decreases, while the corresponding expense reduces net income on the income statement. This dynamic interplay ensures both statements remain accurate and compliant with accounting standards. For instance, if no adjustments were made, the income statement would underreport expenses, and the balance sheet would overstate assets, distorting financial health.

Practical tips for handling prepaid rent include maintaining a schedule of prepaid expenses to track expiration dates and amounts. This schedule simplifies the adjustment process and reduces the risk of errors. Additionally, businesses should review prepaid accounts regularly to ensure timely recognition of expenses. For small businesses or those new to accounting, leveraging accounting software can automate these adjustments, minimizing manual effort and enhancing accuracy. Understanding and correctly applying these principles not only ensures compliance but also provides a clearer picture of a company’s financial position and performance.

Renting Chairs at Myrtle Beach: A Simple Guide for Visitors

You may want to see also

Explore related products

![]()

Balance Sheet Classification: Identifying prepaid rent as a current asset on the balance sheet

Prepaid rent is a unique accounting entry that often sparks debate among finance professionals. While it represents an advance payment for future occupancy, its classification on the balance sheet is not as straightforward as one might assume. The key question is whether prepaid rent should be categorized as a current asset, and the answer lies in understanding the nature of this account and its role in financial reporting.

In the realm of accounting, assets are typically classified as either current or non-current, depending on their liquidity and expected conversion into cash within a year. Current assets, such as cash, accounts receivable, and inventory, are vital for assessing a company's short-term financial health and liquidity. Here's where prepaid rent enters the picture: when a business pays rent in advance, it essentially purchases a future benefit, which is the right to occupy a property for a specified period. This advance payment is recorded as a prepaid expense, but its classification as a current asset is not always obvious.

To determine if prepaid rent qualifies as a current asset, consider the following scenario: a company pays $12,000 for a year's rent in advance, starting January 1. Each month, $1,000 is recognized as rent expense, and the prepaid rent account is reduced accordingly. By the end of the first quarter, $3,000 has been expensed, leaving $9,000 in the prepaid rent account. At this point, the remaining prepaid rent is indeed a current asset because it represents a resource that will be consumed within the next 12 months. This classification is crucial for investors and creditors who rely on the balance sheet to evaluate a company's liquidity and short-term financial obligations.

However, a word of caution is necessary. The classification of prepaid rent as a current asset is not universal and may vary depending on the accounting framework and specific circumstances. For instance, under the International Financial Reporting Standards (IFRS), prepaid expenses are generally classified as non-current assets if they are not expected to be realized within 12 months. In contrast, the Generally Accepted Accounting Principles (GAAP) in the United States typically treat prepaid rent as a current asset, regardless of the payment term, as long as it is expected to be consumed within the operating cycle. This discrepancy highlights the importance of understanding the applicable accounting standards and their impact on financial statement presentation.

In practice, businesses should carefully assess the term of their rental agreements and the pattern of rent consumption. For example, if a company pays two years' rent in advance, it might be more appropriate to classify a portion of the prepaid rent as a non-current asset, reflecting the long-term nature of the commitment. This approach ensures that financial statements provide a true and fair view of the company's financial position, enabling stakeholders to make informed decisions. By meticulously analyzing prepaid rent and its classification, businesses can maintain accurate financial records and comply with accounting standards, ultimately fostering transparency and trust in their financial reporting.

Renting a Chipper Shredder in Indianapolis: A Quick Guide

You may want to see also

![]()

Year-End Adjustments: The role of adjusting entries in reflecting prepaid rent accurately

Prepaid rent is not considered a temporary account; rather, it is classified as an asset on the balance sheet. This distinction is crucial because it reflects a resource that provides future economic benefits. However, its accurate representation hinges on year-end adjustments, which ensure that financial statements align with the matching principle—expenses are recognized in the period they are incurred, not when they are paid. Without these adjustments, prepaid rent would distort both the income statement and balance sheet, overstating assets and understating expenses in the current period.

Adjusting entries for prepaid rent serve a dual purpose: they reclassify the portion of prepaid rent that has been consumed during the accounting period as an expense, while reducing the prepaid rent asset account accordingly. For example, if a company pays $12,000 in January for a year’s rent, $1,000 should be recognized as rent expense each month. At year-end, an adjusting entry would debit Rent Expense for $12,000 and credit Prepaid Rent for $12,000, leaving the Prepaid Rent account with a zero balance if the entire amount has been expensed. This process ensures that the financial statements reflect the true financial position and operational performance of the business.

The timing of these adjustments is critical. Year-end adjustments must be made before closing the books to avoid misstatements in the next accounting period. For instance, failing to adjust prepaid rent would result in the next year’s rent expense being overstated, as the prepaid amount would be expensed again. This oversight could mislead stakeholders, from investors to tax authorities, who rely on accurate financial reporting. Thus, meticulous attention to adjusting entries is not just a procedural step but a safeguard against financial misrepresentation.

Practical implementation of prepaid rent adjustments involves a systematic approach. First, identify the total prepaid rent and determine the portion applicable to the current period. Second, calculate the adjusting entry by debiting Rent Expense and crediting Prepaid Rent for that amount. Third, ensure consistency by reviewing prior periods’ adjustments to avoid errors. Tools like accounting software can automate this process, reducing the risk of manual miscalculations. For small businesses, a simple spreadsheet can suffice, but accuracy remains paramount.

In conclusion, while prepaid rent is not a temporary account, its accurate reflection in financial statements depends on precise year-end adjustments. These entries bridge the gap between cash payments and expense recognition, upholding the integrity of financial reporting. By understanding and executing these adjustments, businesses can ensure compliance with accounting principles and provide stakeholders with a clear, truthful picture of their financial health.

Discovering Tulsa's Average Rent: A Comprehensive Guide for Renters

You may want to see also

Frequently asked questions

No, prepaid rent is not considered a temporary account. It is classified as a current asset on the balance sheet because it represents rent paid in advance for a future period.

Prepaid rent is not a temporary account because it does not reset to zero at the end of an accounting period. Instead, it is adjusted over time as the rent expense is recognized.

Prepaid rent is classified as a current asset account, as it represents a payment made in advance for a benefit that will be received within one year or the operating cycle, whichever is longer.

Prepaid rent differs from temporary accounts because it is a balance sheet account that carries a balance forward, whereas temporary accounts (e.g., revenue, expenses) are closed to retained earnings at the end of an accounting period and reset to zero.