Prepaid rent is a common accounting concept that arises when a business pays for rent in advance, typically for a period extending beyond the current accounting period. In cash basis accounting, the focus is on recording transactions when cash is exchanged, rather than when the expense is incurred. As a result, prepaid rent presents an interesting question in cash basis accounting: whether it should be recorded as an expense when paid or deferred to the period in which the rent is actually utilized. This distinction is crucial for accurately reflecting a company's financial position and ensuring compliance with accounting principles, making it essential to understand how prepaid rent is treated under the cash basis method.

| Characteristics | Values |

|---|---|

| Recognition Timing | Recorded as an expense when cash is paid, not when the rent is used. |

| Accounting Method | Cash basis accounting, not accrual basis. |

| Expense Treatment | Treated as an immediate expense in the period of payment. |

| Asset Recognition | Not recognized as an asset (prepaid rent) on the balance sheet. |

| Tax Implications | Expense is deductible in the year of payment for tax purposes. |

| Simplicity | Simplifies record-keeping by avoiding accruals and adjustments. |

| Common Use | Typically used by small businesses or individuals, not corporations. |

| Financial Statement Impact | Does not reflect the timing of actual rent usage in financial reports. |

| Compliance | Generally not accepted under GAAP or IFRS for external reporting. |

| Cash Flow Impact | Directly reduces cash balance at the time of payment. |

Explore related products

What You'll Learn

- Prepaid Rent Definition: Understanding prepaid rent as advance payment for future rental periods in accounting

- Cash Basis Overview: Cash basis records transactions when cash exchanges hands, not when incurred

- Recording Prepaid Rent: Prepaid rent is not recorded until payment is made in cash basis

- Expense Recognition: Expenses are recognized when paid, not when services are received in cash basis

- Impact on Financials: Prepaid rent does not affect income statement until cash is disbursed

![]()

Prepaid Rent Definition: Understanding prepaid rent as advance payment for future rental periods in accounting

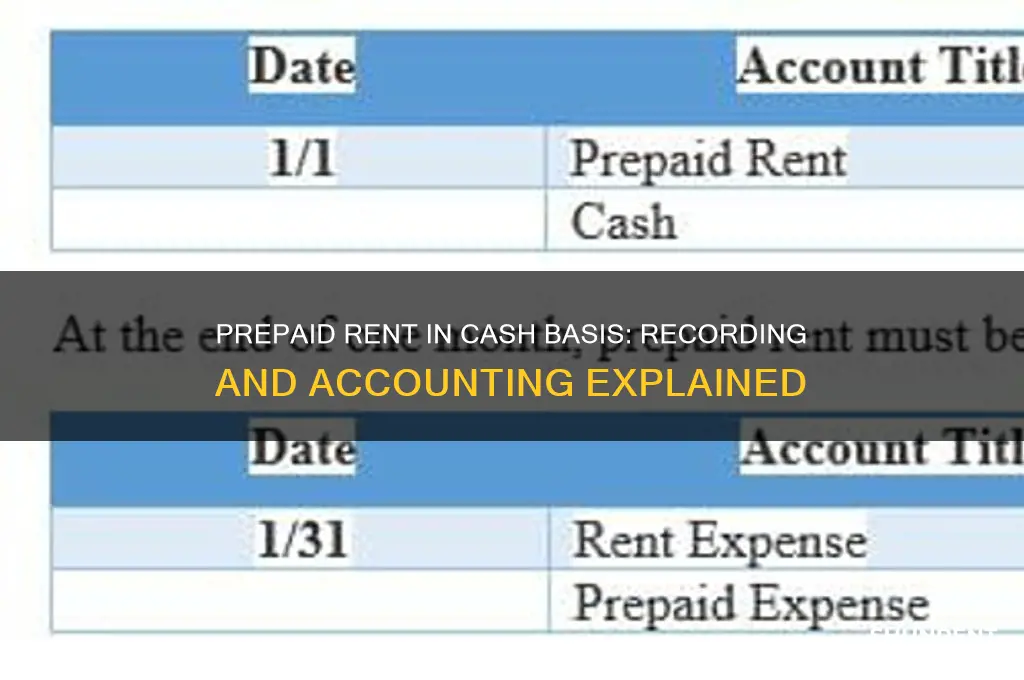

Prepaid rent represents a unique accounting challenge, particularly when considering the cash basis method. By definition, prepaid rent is an advance payment made by a tenant for the use of a property in future periods. This concept is straightforward in theory but becomes complex when determining how and when to record it, especially under cash basis accounting. Unlike accrual accounting, which matches expenses to the period in which they are incurred, cash basis accounting recognizes transactions only when cash changes hands. This fundamental difference raises the question: is prepaid rent recorded in cash basis accounting?

To address this, consider the mechanics of cash basis accounting. Under this method, expenses are recorded when paid, and revenues are recorded when received. Prepaid rent, however, involves paying for a future benefit. For example, if a tenant pays $12,000 in January for a year’s rent, the entire $12,000 is an immediate cash outflow. In cash basis accounting, this payment would be recorded as a rent expense in January, despite the fact that the benefit of occupancy extends over 12 months. This approach contrasts sharply with accrual accounting, where the $12,000 would be allocated evenly over the year as a prepaid asset, with monthly rent expense of $1,000.

The implications of recording prepaid rent in cash basis accounting are significant, particularly for small businesses or individuals using this method. By expensing the entire prepaid amount upfront, the business’s financial statements may inaccurately reflect its financial health. For instance, January’s expenses would appear disproportionately high, while subsequent months would show no rent expense, distorting profitability trends. This lack of matching between expenses and revenues can mislead stakeholders and complicate financial planning.

Despite these drawbacks, cash basis accounting remains popular due to its simplicity. For prepaid rent, the key is to recognize its limitations. If using this method, businesses should supplement their financial statements with notes or schedules that clarify the timing and allocation of prepaid expenses. For example, a small business might maintain an internal spreadsheet tracking prepaid rent, even if it isn’t formally recorded as an asset on the books. This ensures transparency and provides a more accurate picture of cash flow and obligations.

In conclusion, prepaid rent is recorded in cash basis accounting as an immediate expense when paid, regardless of the period it covers. While this simplifies record-keeping, it sacrifices the matching principle, potentially skewing financial insights. Businesses relying on cash basis accounting should be aware of this limitation and adopt supplementary practices to monitor prepaid expenses effectively. Understanding this nuance is crucial for accurate financial management and reporting.

Should Landlords Rent to Section 8 Tenants?

You may want to see also

Explore related products

![]()

Cash Basis Overview: Cash basis records transactions when cash exchanges hands, not when incurred

Prepaid rent presents a unique challenge in cash basis accounting, which fundamentally records transactions only when cash changes hands. This method contrasts sharply with accrual accounting, which recognizes revenue and expenses when they are earned or incurred, regardless of cash flow. In the case of prepaid rent, a business pays for future rent periods upfront, creating a disconnect between the cash outflow and the actual use of the rented space.

Consider a small business owner who pays $6,000 in January for six months of rent. Under cash basis accounting, the entire $6,000 is recorded as an expense in January, the month the payment is made. This treatment simplifies record-keeping but distorts the financial picture by overstating January’s expenses and understating those of subsequent months. Accrual accounting, on the other hand, would spread the $6,000 evenly across the six months, providing a more accurate representation of monthly expenses.

The simplicity of cash basis accounting makes it appealing for small businesses or sole proprietorships with straightforward finances. However, its treatment of prepaid expenses like rent can lead to misleading financial statements, particularly for businesses with significant prepaid obligations. For instance, a company with multiple prepaid expenses might appear unprofitable in the month of payment, despite healthy ongoing operations.

To mitigate this distortion, businesses using cash basis accounting should maintain detailed records of prepaid expenses. Tracking when prepaid amounts are actually "used up" can provide a clearer understanding of cash flow and financial health. For example, annotating January’s $6,000 rent payment as covering January through June can help in interpreting monthly financial statements.

Ultimately, while cash basis accounting offers simplicity, its treatment of prepaid rent highlights a trade-off between ease of use and financial accuracy. Businesses must weigh these factors carefully, considering their size, complexity, and reporting needs. For those with substantial prepaid expenses, transitioning to accrual accounting or supplementing cash basis records with additional tracking may be necessary to ensure a more accurate financial narrative.

Who Played Arnold Jackson on Different Strokes? The Actor Revealed

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

![]()

Recording Prepaid Rent: Prepaid rent is not recorded until payment is made in cash basis

In cash basis accounting, the timing of transactions is paramount. Prepaid rent, a common expense for businesses, presents a unique challenge in this context. Unlike accrual accounting, where expenses are recognized when incurred, cash basis accounting only records transactions when cash changes hands. This fundamental difference means that prepaid rent, despite being a future obligation, remains unrecorded until the actual payment is made.

Understanding this principle is crucial for accurate financial reporting under the cash basis method.

Consider a scenario where a business signs a one-year lease agreement in January, paying the entire year's rent upfront. In accrual accounting, the rent expense would be spread evenly across the twelve months. However, in cash basis accounting, the entire rent payment is recorded as an expense in January, the month of payment. This approach simplifies record-keeping but can distort the financial picture, especially for businesses with significant prepaid expenses.

For instance, a company with substantial prepaid rent might appear less profitable in the month of payment compared to subsequent months, even if its operational performance remains consistent.

This treatment of prepaid rent highlights a key limitation of cash basis accounting. While it offers simplicity and ease of use, it sacrifices the matching principle, a cornerstone of accrual accounting. The matching principle dictates that expenses should be recognized in the same period as the revenues they help generate. Cash basis accounting, by recording prepaid rent only upon payment, fails to align expenses with the periods they relate to, potentially leading to misleading financial statements.

This limitation underscores the importance of choosing the appropriate accounting method based on a business's size, complexity, and reporting needs.

Despite its drawbacks, cash basis accounting remains a viable option for small businesses and sole proprietorships with straightforward financial transactions. Its simplicity and focus on cash flow can provide valuable insights into a business's liquidity and short-term financial health. However, for businesses with significant prepaid expenses or those seeking a more comprehensive view of their financial performance, accrual accounting may be a more suitable choice. Ultimately, the decision between cash basis and accrual accounting depends on a careful assessment of a business's specific circumstances and reporting requirements.

Anderson Inc's $4,000 Rent Expense Payment: Timing and Impact

You may want to see also

Explore related products

![]()

Expense Recognition: Expenses are recognized when paid, not when services are received in cash basis

In cash basis accounting, the timing of expense recognition is straightforward: expenses are recorded when payment is made, not when the service is rendered or received. This principle sharply contrasts with accrual accounting, where expenses are matched to the period in which they are incurred, regardless of when payment occurs. For businesses using cash basis, this means that prepaid expenses, such as rent, are not recorded as expenses until the cash actually leaves the business. For example, if a company pays $12,000 in January for a year’s worth of rent, the entire $12,000 is expensed in January, not spread over the 12 months during which the rented space is used.

This approach simplifies financial tracking but can distort short-term profitability. Consider a small business owner who prepays $6,000 for six months of office rent. Under cash basis, the business’s expenses spike in the month of payment, making it appear less profitable than it truly is during that period. Conversely, the following months show lower expenses, potentially overstating profitability. This volatility highlights the trade-off between simplicity and accuracy in cash basis accounting. For businesses with significant prepaid expenses, this method may not provide a clear picture of financial health, especially for stakeholders analyzing month-to-month performance.

To mitigate these distortions, businesses using cash basis accounting should maintain detailed records of prepaid expenses. For instance, tracking prepaid rent in a separate ledger allows owners to monitor when payments were made and when the corresponding services are consumed. This practice, while not altering the financial statements, provides internal visibility into cash flow and expense distribution. Additionally, businesses can use budgeting tools to forecast cash outflows for prepaid expenses, ensuring liquidity is not compromised by lump-sum payments. For example, setting aside $1,000 monthly for a $12,000 annual rent payment can smooth cash flow and reduce the impact of large, one-time expenses.

Despite its limitations, cash basis accounting remains a practical choice for small businesses with straightforward operations and minimal prepaid expenses. However, as a business grows or begins dealing with larger prepaid amounts, transitioning to accrual accounting may become necessary to align expense recognition with service consumption. For instance, a business expanding into multiple rental properties would benefit from accrual accounting to accurately reflect monthly rent expenses across properties. Ultimately, the decision to record prepaid rent in cash basis hinges on the business’s size, complexity, and reporting needs, with simplicity often taking precedence in the early stages of operation.

Is Monthly Pet Rent Legal? Understanding Tenant Rights and Fees

You may want to see also

![]()

Impact on Financials: Prepaid rent does not affect income statement until cash is disbursed

Prepaid rent, a common accounting concept, behaves uniquely under the cash basis method. Unlike accrual accounting, which recognizes expenses when incurred, cash basis accounting only records transactions when cash changes hands. This fundamental difference has a direct impact on the income statement.

Imagine a small business owner who pays $12,000 in rent upfront for the entire year. Under accrual accounting, this would be recorded as a $1,000 monthly rent expense, impacting the income statement each month. However, under cash basis accounting, the entire $12,000 would be recorded as an expense only when the payment is made, regardless of the period it covers.

This delay in expense recognition can significantly distort the financial picture presented by the income statement. For instance, the month the rent is paid would show a substantial expense, potentially making the business appear less profitable than it actually is during that period. Conversely, the months following the payment would show lower expenses, artificially inflating profitability. This lack of matching expenses with the periods they relate to undermines the principle of accrual accounting, which aims to provide a more accurate representation of a company's financial performance over time.

Consequently, businesses using cash basis accounting need to be mindful of this limitation when analyzing their income statements. It's crucial to consider the timing of prepaid expenses and their impact on the reported profitability in any given period.

While cash basis accounting offers simplicity, its treatment of prepaid expenses like rent can lead to misleading financial snapshots. Understanding this nuance is essential for accurate interpretation and informed decision-making.

Renting a U-Haul: What's the Deal With G?

You may want to see also

Frequently asked questions

No, prepaid rent is not recorded on the cash basis of accounting. Cash basis accounting recognizes transactions only when cash is exchanged, whereas prepaid rent involves a payment for future rent, which is not yet incurred.

In cash basis accounting, prepaid rent is treated as an expense in the period it is paid, regardless of when the rent is actually used or incurred.

Cash basis accounting does not recognize prepaid expenses as assets because it focuses solely on cash flows. Prepaid rent is expensed immediately when paid, rather than being deferred to future periods.

No, prepaid rent cannot be deferred in cash basis accounting. It must be recorded as an expense in the period the payment is made, even if the rent covers future periods.

The alternative is accrual basis accounting, where prepaid rent is recorded as an asset when paid and then expensed over the period the rent is used, aligning expenses with the periods they benefit.