Prepaid rent is a crucial concept in accounting and financial reporting, representing payments made in advance for the use of property or space over a future period. On a balance sheet, prepaid rent is classified as a current asset, reflecting the portion of the payment that has not yet been utilized or expired. This classification is based on the principle that prepaid expenses should be recognized as assets until the related benefit is consumed. As the rental period progresses, the prepaid rent is gradually expensed, reducing the asset balance and recognizing the expense on the income statement. Understanding the treatment of prepaid rent on the balance sheet is essential for accurately portraying a company’s financial position and ensuring compliance with accounting standards.

| Characteristics | Values |

|---|---|

| Classification | Current Asset (if the prepaid period is within one year or operating cycle) |

| Balance Sheet Location | Listed under "Current Assets" or "Other Current Assets" |

| Nature | Represents rent paid in advance for future use |

| Recognition | Recorded as an asset when payment is made |

| Amortization | Expensed over the rental period as rent expense |

| Adjusting Entry | Requires periodic adjusting entries to recognize rent expense |

| Impact on Financial Statements | Reduces cash at payment, increases assets, and later reduces assets/increases expenses |

| Reporting Standard | Follows accrual accounting principles (GAAP/IFRS) |

| Example | If $12,000 is paid for 6 months of rent, $2,000 is expensed monthly |

| Purpose | Matches expenses with the period in which the benefit is received |

Explore related products

What You'll Learn

![]()

Prepaid Rent Definition

Prepaid rent represents a unique accounting concept where a tenant pays for future occupancy in advance. This transaction creates an asset on the tenant’s balance sheet, reflecting the right to use the property over a specified period. For instance, if a business pays $12,000 for a year’s rent upfront, it records $12,000 as a prepaid rent asset. Each month, $1,000 is expensed, reducing the asset balance while aligning expenses with the period benefited. This method adheres to the matching principle, a cornerstone of accrual accounting.

Consider the mechanics of prepaid rent in practice. Suppose a retail store prepays $6,000 for six months of rent. Initially, the journal entry debits Prepaid Rent (an asset) and credits Cash (an asset) for $6,000. Over the next six months, the store records a monthly adjusting entry: debit Rent Expense (an expense) and credit Prepaid Rent (an asset) for $1,000. This systematic approach ensures the balance sheet accurately reflects the remaining prepaid amount, while the income statement captures rent expense incrementally.

A comparative analysis highlights why prepaid rent is classified as a current asset. Unlike long-term assets, prepaid rent is typically consumed within a year. For example, a three-month prepaid lease falls under current assets, whereas a multi-year prepaid agreement might require separation into current and non-current portions. This distinction is critical for financial statement users, such as investors or creditors, who assess liquidity and short-term obligations.

Persuasively, treating prepaid rent as an asset rather than an expense upfront offers strategic advantages. It prevents distortion of financial performance by avoiding a large, one-time expense. Instead, it spreads the cost over the rental period, providing a clearer picture of profitability. For small businesses, this practice can improve cash flow management by deferring expenses and maintaining a healthier balance sheet. However, transparency is key—notes to financial statements should disclose the prepaid rent amount and its amortization schedule.

In conclusion, prepaid rent is more than an accounting entry; it’s a tool for financial accuracy and strategic planning. By understanding its definition, mechanics, and classification, businesses can optimize their balance sheets and align expenses with operational benefits. Whether prepaying rent for tactical reasons or contractual obligations, proper treatment ensures compliance with accounting standards and enhances financial clarity.

Renting a Gym Space: A Guide for Private Fitness Trainers

You may want to see also

Explore related products

$18.15 $24.95

![]()

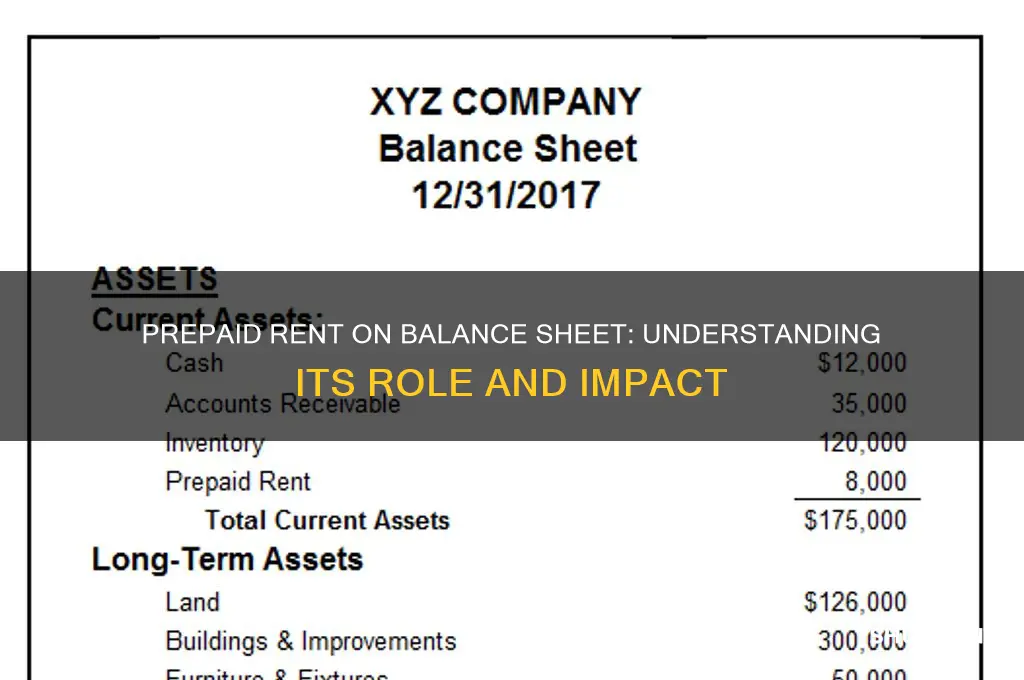

Balance Sheet Classification

Prepaid rent is a unique asset that challenges traditional balance sheet classification. It represents a payment made in advance for future use of a property, blurring the lines between current and non-current assets. To accurately classify prepaid rent, one must consider the time horizon of its benefit realization. Generally, if the prepaid rent covers a period of 12 months or less, it is classified as a current asset on the balance sheet. This is because the benefit will be fully realized within the operating cycle of the business. For instance, a company paying $12,000 annually for office space in January would record $1,000 monthly as rent expense, with the remaining $11,000 initially classified as prepaid rent under current assets.

The classification of prepaid rent as a current asset aligns with the principle of matching expenses to the periods in which they are incurred. By doing so, financial statements more accurately reflect the company’s short-term liquidity and operational efficiency. However, if the prepaid rent extends beyond 12 months, the portion exceeding this period should be classified as a non-current asset. For example, if a company prepays $24,000 for a two-year lease, $12,000 would be recorded as a current asset, and the remaining $12,000 as a non-current asset. This bifurcation ensures that the balance sheet provides a clear picture of both short-term and long-term financial commitments.

A common mistake in classifying prepaid rent is treating it as an expense rather than an asset. This error can distort financial ratios, such as the current ratio or working capital, which rely on accurate asset classification. To avoid this, businesses should establish clear accounting policies that define the threshold for current versus non-current classification. For instance, a policy might stipulate that any prepaid expense with a benefit period of six months or less is automatically classified as current, while longer periods require prorated classification.

From a comparative perspective, prepaid rent differs from other prepaid expenses, such as insurance or supplies, in its direct link to a specific asset—the leased property. This distinction underscores the importance of context in balance sheet classification. While prepaid insurance might be uniformly classified as a current asset due to its short-term nature, prepaid rent requires a more nuanced approach. Auditors and analysts should scrutinize the lease agreement to determine the appropriate classification, ensuring compliance with accounting standards like ASC 842 or IFRS 16.

In conclusion, the classification of prepaid rent on a balance sheet hinges on the timing of its benefit realization. By adhering to the 12-month rule and maintaining clear accounting policies, businesses can ensure their financial statements accurately reflect their financial position. This precision not only enhances transparency but also aids stakeholders in making informed decisions. Whether classified as current or non-current, prepaid rent serves as a reminder of the critical role that judgment and context play in financial reporting.

Renting Out a Townhouse: Challenges, Benefits, and Essential Tips

You may want to see also

Explore related products

![]()

Journal Entry Process

Prepaid rent is indeed recorded on a balance sheet as a current asset, reflecting payments made in advance for future rental periods. This accounting treatment aligns with the principle of matching expenses to the periods in which they are incurred. However, the process begins with a precise journal entry, which serves as the foundation for accurate financial reporting. Understanding this journal entry process is crucial for maintaining the integrity of the balance sheet and ensuring compliance with accounting standards.

The journal entry for prepaid rent involves a debit to the prepaid rent account and a credit to the cash account. For example, if a company pays $12,000 for six months of rent in advance, the entry would debit Prepaid Rent for $12,000 and credit Cash for $12,000. This entry recognizes the outflow of cash and the creation of an asset that will be consumed over time. The prepaid rent account is classified as a current asset because it represents a benefit that will be realized within one year or the operating cycle, whichever is longer.

As the rental period progresses, the prepaid rent must be adjusted to reflect the portion of rent that has been consumed. This is done through a monthly journal entry that debits Rent Expense and credits Prepaid Rent. For instance, if the monthly rent is $2,000, the entry would debit Rent Expense for $2,000 and credit Prepaid Rent for $2,000. This process ensures that the expense is recognized in the period it pertains to, adhering to the accrual basis of accounting. Over time, the prepaid rent account is reduced until it reaches zero, at which point all prepaid rent has been fully expensed.

A critical aspect of the journal entry process is consistency and accuracy. Errors in recording prepaid rent can distort financial statements, leading to misrepresentations of a company’s liquidity and expenses. For example, failing to adjust prepaid rent monthly could result in an overstatement of assets and an understatement of expenses. To avoid such pitfalls, companies should establish internal controls, such as regular reviews of prepaid accounts and reconciliation with lease agreements. Additionally, leveraging accounting software can automate these entries, reducing the risk of human error.

In conclusion, the journal entry process for prepaid rent is a straightforward yet essential component of financial accounting. It begins with the initial recognition of the prepaid asset and continues with periodic adjustments to allocate the expense appropriately. By mastering this process, businesses can ensure their balance sheets accurately reflect their financial position and maintain compliance with accounting principles. Attention to detail and adherence to best practices are key to achieving this goal.

Discover Top Design Studios for Rent: Your Ultimate Search Guide

You may want to see also

Explore related products

![]()

Amortization Treatment

Prepaid rent represents a unique accounting challenge, as it embodies both an asset and an expense. Initially recorded as a current asset on the balance sheet, it reflects the portion of rent paid in advance for future periods. However, as time progresses, this asset must be systematically recognized as an expense to align with the matching principle. This is where amortization treatment comes into play, serving as the mechanism to transition prepaid rent from the balance sheet to the income statement.

Amortization, in this context, involves allocating the prepaid rent expense over the period it benefits. For example, if a company pays $12,000 for a year’s rent in advance, $1,000 would be recognized as rent expense each month. This process ensures that financial statements accurately reflect the economic reality of the business, matching expenses with the revenues they help generate. The journal entry typically involves debiting rent expense and crediting the prepaid rent asset account, reducing the latter each period until it is fully expensed.

The treatment of prepaid rent through amortization is not arbitrary; it adheres to accounting standards such as GAAP and IFRS, which require expenses to be recognized in the period they are incurred. This consistency is critical for comparability across financial statements, enabling stakeholders to assess a company’s financial health accurately. For instance, a company with significant prepaid rent might appear asset-rich initially, but amortization reveals the true cash outflow over time, providing a clearer picture of liquidity and operational efficiency.

Practical implementation of amortization requires careful tracking and documentation. Companies often use accounting software to automate this process, ensuring accuracy and compliance. For small businesses or manual systems, a simple spreadsheet can suffice, with monthly adjustments to reflect the amortization schedule. It’s crucial to review these entries periodically to avoid errors, as misallocation can distort financial ratios like operating margins or return on assets.

In conclusion, amortization treatment of prepaid rent is a fundamental accounting practice that bridges the gap between upfront payments and periodic expenses. By systematically reducing the prepaid rent asset and recognizing the corresponding expense, businesses maintain transparency and adherence to accounting principles. Whether automated or manual, this process demands precision and consistency, ultimately contributing to the reliability of financial reporting.

Rent-A-Center Closing Time in Taunton, Massachusetts: Your Guide

You may want to see also

Explore related products

![]()

Financial Statement Impact

Prepaid rent is a unique asset that reflects a company’s advance payment for future rental obligations. On the balance sheet, it is classified as a current asset if the prepaid period is within one year or the operating cycle, whichever is longer. This classification is critical because it directly impacts liquidity ratios, such as the current ratio, by increasing the total current assets. For instance, if a company prepays $12,000 for a year’s rent, this amount appears on the balance sheet under current assets until it is fully expensed over the rental period.

The financial statement impact of prepaid rent extends beyond the balance sheet to the income statement. As the prepaid rent is consumed over time, it is gradually expensed as rent expense. This process is typically handled through monthly adjusting entries, ensuring that expenses match the period in which they are incurred. For example, if $1,000 of the prepaid rent is expensed monthly, the income statement will reflect this amount as a rent expense each month, while the prepaid rent asset on the balance sheet decreases by the same amount.

Another key impact is on cash flow statements. When prepaid rent is initially recorded, it reduces cash but does not immediately affect net income. This transaction is reported in the operating activities section of the cash flow statement as a use of cash. However, as the prepaid rent is expensed, it does not affect cash again but reduces the prepaid asset balance. This distinction highlights the importance of understanding how prepaid rent influences both cash flow and income statement dynamics.

For financial analysts and stakeholders, prepaid rent provides insights into a company’s cash management practices and short-term financial health. A significant prepaid rent balance may indicate proactive management of future expenses or, conversely, a lack of immediate liquidity if other current assets are insufficient. For example, a startup with $50,000 in prepaid rent and only $10,000 in cash might face liquidity challenges despite having a substantial current asset.

In conclusion, prepaid rent’s financial statement impact is multifaceted, affecting asset classification, expense recognition, and cash flow reporting. Proper accounting for prepaid rent ensures compliance with accrual accounting principles and provides a clearer picture of a company’s financial position. Companies should regularly review and adjust prepaid rent balances to maintain accuracy and transparency in their financial statements.

Top Minneapolis Spots for Renting Cross-Country Skis This Winter

You may want to see also

Frequently asked questions

Yes, prepaid rent is classified as a current asset on the balance sheet because it represents a payment made in advance for future rent expenses.

Prepaid rent is recorded as a debit to the prepaid rent account (an asset) and a credit to cash or the payment method used, reflecting the advance payment.

No, prepaid rent is typically listed as a current asset because it is expected to be consumed within one year or the operating cycle, whichever is longer.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)