When determining whether rent payments should be reported on a 1099-MISC or 1099-NEC form, it’s essential to understand the distinctions between these tax documents. The 1099-NEC (Nonemployee Compensation) is specifically used to report payments made to independent contractors or freelancers for services rendered, while the 1099-MISC is used for miscellaneous income, such as rents, royalties, or prizes. For landlords or property owners, rent payments received from tenants are typically reported on a 1099-MISC under Box 1 (Rent), as they fall under the category of rental income rather than compensation for services. However, if the rent includes payments for services (e.g., property management or maintenance), those amounts might need to be separated and reported differently. Understanding these distinctions ensures compliance with IRS regulations and accurate tax reporting.

| Characteristics | Values |

|---|---|

| Form Type | Rent payments are typically reported on Form 1099-NEC, not Form 1099-MISC. |

| IRS Guidelines | Since 2020, the IRS reintroduced Form 1099-NEC specifically for nonemployee compensation, which includes rent if paid to an independent contractor or business. |

| Applicability | If rent is paid to an individual or business for property used in a trade or business, it should be reported on Form 1099-NEC if the total payments exceed $600 in a calendar year. |

| Exceptions | Rent paid to real estate agents or property managers may be reported on Form 1099-MISC under "Other Income" (Box 3) if not related to nonemployee compensation. |

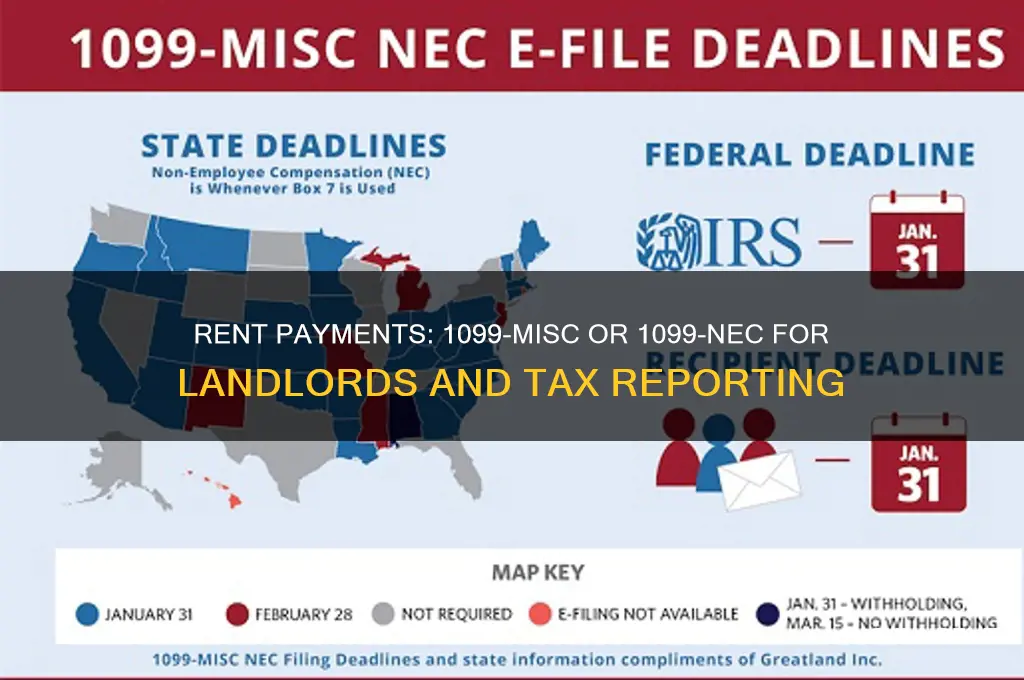

| Filing Deadline | Form 1099-NEC must be filed with the IRS and provided to the recipient by January 31st of the following year. |

| Penalties | Failure to file correctly or on time can result in penalties ranging from $50 to $590 per form, depending on the delay and the filer's size. |

| State Requirements | Some states may have additional reporting requirements for rent payments, so check local regulations. |

| Recipient Type | Only payments to businesses or independent contractors require reporting; payments to individuals for personal use are not reportable. |

| Documentation | Landlords or payers should maintain records of rent payments and recipient information for at least four years. |

Explore related products

What You'll Learn

- Rent Classification: Determining if rent payments qualify as 1099-MISC or 1099-NEC

- IRS Guidelines: Understanding IRS rules for reporting rent income on tax forms

- Landlord Reporting: When landlords must issue 1099 forms to tenants or vendors

- Property Types: Differentiating residential, commercial, and other property rent reporting

- Payment Thresholds: Minimum payment amounts triggering 1099-MISC or 1099-NEC requirements

![]()

Rent Classification: Determining if rent payments qualify as 1099-MISC or 1099-NEC

Rent payments to individuals or unincorporated entities often trigger reporting requirements, but determining whether they belong on a 1099-MISC or 1099-NEC hinges on the nature of the arrangement. The IRS reintroduced the 1099-NEC in 2020 specifically for nonemployee compensation, such as payments to independent contractors. Rent, however, typically falls under the 1099-MISC category if it meets certain criteria. For instance, if you pay $600 or more in rent to a landlord who is an individual or partnership, you must report this on a 1099-MISC, using Box 1 for rent income. This distinction is crucial because misclassifying rent payments can lead to penalties or confusion for both the payer and the recipient.

To accurately classify rent payments, consider the relationship between the payer and the recipient. If the rent is paid to a property management company or a corporation, no 1099 reporting is required, as these entities are exempt. However, if the recipient is an individual or partnership, the payment must be reported on a 1099-MISC. For example, a small business renting office space from a retired couple would need to issue a 1099-MISC if the annual rent exceeds $600. Conversely, if the same business hires an independent contractor for repairs and pays them over $600, that payment would go on a 1099-NEC, not a 1099-MISC.

A common pitfall is assuming all payments to individuals require a 1099-NEC. This misconception stems from the form’s name, which includes "nonemployee compensation." However, rent is explicitly excluded from this category and must be reported on a 1099-MISC. To avoid errors, payers should carefully review IRS instructions, particularly Publication 1220, which outlines specific reporting requirements. For instance, if a tenant pays rent directly to a property owner, the owner must report this income on their tax return, but the tenant is not responsible for issuing a 1099 unless they are a business entity.

Practical tips can streamline the classification process. First, maintain clear records of all rental agreements and payments, noting the recipient’s legal structure (individual, partnership, or corporation). Second, use accounting software that supports 1099 reporting to automate tracking and form generation. Third, consult a tax professional if the arrangement involves complex scenarios, such as rent paid in exchange for services. For example, if a landlord reduces rent in return for the tenant’s maintenance work, the fair market value of the services might need to be reported as nonemployee compensation on a 1099-NEC, while the rent itself remains on a 1099-MISC.

In conclusion, classifying rent payments as 1099-MISC or 1099-NEC requires a clear understanding of IRS guidelines and the specifics of the rental arrangement. By focusing on the recipient’s entity type and the nature of the payment, payers can ensure compliance and avoid unnecessary complications. Remember, rent paid to individuals or partnerships generally belongs on a 1099-MISC, while nonemployee compensation for services goes on a 1099-NEC. Staying informed and organized is key to navigating this often-confusing aspect of tax reporting.

Maximizing Tax Returns: Understanding Rent Deductions and Benefits

You may want to see also

Explore related products

![]()

IRS Guidelines: Understanding IRS rules for reporting rent income on tax forms

Rent income, a staple for many property owners, falls under specific IRS guidelines that dictate how it should be reported. The IRS classifies rental income as business income, not passive income, which means it must be reported on Schedule E of Form 1040. This distinction is crucial because it determines the type of tax form used for reporting and the associated tax implications. For instance, if you’re a landlord receiving rent from tenants, this income is subject to ordinary income tax rates, not the potentially lower capital gains rates. Understanding this classification is the first step in navigating the IRS rules for reporting rent income accurately.

One common question arises when dealing with payments to service providers related to rental properties: *Is rent reported on a 1099-MISC or 1099-NEC?* The answer lies in the nature of the payment. Rent itself is not reported on either form, as it is income to the landlord, not a payment to a contractor or vendor. However, if you pay an independent contractor, such as a property manager or repairperson, more than $600 in a tax year, you must issue a 1099-NEC (Nonemployee Compensation). The 1099-MISC is used for other types of payments, like rent paid to an individual or company for leasing equipment, but not for typical rental income reporting. This distinction prevents confusion and ensures compliance with IRS regulations.

To illustrate, consider a landlord who hires a plumber to fix a rental property’s leaky pipes. If the plumber is paid $800 for the job, the landlord must file a 1099-NEC for that payment. Conversely, the monthly rent collected from tenants is reported on Schedule E, not on any 1099 form. This example highlights the importance of understanding the purpose of each form and applying it correctly. Misreporting can lead to penalties, audits, or delays in tax processing, making it essential to differentiate between income reporting and contractor payments.

Practical tips for landlords include maintaining detailed records of all rental income and expenses, as well as payments to contractors. Use accounting software or spreadsheets to track these transactions, ensuring accuracy and ease of reporting. Additionally, stay updated on IRS guidelines, as tax laws can change annually. For instance, the 1099-NEC was reintroduced in 2020 to replace the 1099-MISC for nonemployee compensation, a change that caught many taxpayers off guard. By staying informed and organized, landlords can streamline their tax reporting process and avoid common pitfalls.

In conclusion, while rent income is not reported on a 1099-MISC or 1099-NEC, understanding the IRS rules surrounding these forms is vital for landlords. Properly classifying income and payments ensures compliance and minimizes the risk of errors. By focusing on Schedule E for rental income and using the 1099-NEC for contractor payments, property owners can navigate tax season with confidence and precision.

Renting a Townhouse: What You Need to Know

You may want to see also

Explore related products

![]()

Landlord Reporting: When landlords must issue 1099 forms to tenants or vendors

Landlords often assume their tax responsibilities end with property-related deductions, but a lesser-known obligation involves issuing 1099 forms to certain tenants or vendors. This requirement hinges on whether payments qualify as reportable income under IRS rules. For instance, if a landlord pays a tenant $600 or more in a tax year for services (e.g., property management or maintenance), a 1099-NEC must be filed. Rent payments, however, are not reportable income for tenants and do not trigger this requirement.

The distinction between 1099-MISC and 1099-NEC is critical. Since 2020, the IRS reintroduced the 1099-NEC specifically for nonemployee compensation, while the 1099-MISC is reserved for other income types, such as rent paid to a business entity exceeding $600. Landlords must carefully categorize payments to avoid penalties. For example, paying a vendor $700 for repairs requires a 1099-NEC, but rent paid to a tenant for occupancy does not, unless it includes service fees.

Missteps in landlord reporting can lead to costly consequences. Failure to issue a required 1099 form may result in penalties ranging from $50 to $580 per form, depending on the delay. To avoid errors, landlords should maintain detailed records of all payments, including recipient names, addresses, and tax IDs. Utilizing accounting software or consulting a tax professional can streamline this process, ensuring compliance without unnecessary stress.

A practical tip for landlords is to proactively collect W-9 forms from vendors and service-providing tenants at the start of any business relationship. This document captures essential tax information, simplifying year-end reporting. Additionally, landlords should review IRS guidelines annually, as rules can change. By staying informed and organized, landlords can fulfill their reporting duties efficiently, focusing on property management rather than tax complications.

Essential Requirements for Renting a Pontoon Boat: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Property Types: Differentiating residential, commercial, and other property rent reporting

Rent reporting for tax purposes hinges on property type, with residential, commercial, and other categories triggering distinct 1099 requirements. Residential rentals, encompassing single-family homes, apartments, and condos leased for dwelling purposes, generally fall outside 1099 reporting obligations. The IRS considers these payments personal rather than business expenses, exempting landlords from issuing 1099-MISC or 1099-NEC forms to tenants. However, landlords themselves must report rental income on Schedule E of Form 1040, ensuring compliance with tax laws.

Commercial properties, including office spaces, retail stores, and warehouses, operate under different rules. Rent paid for business use typically qualifies as a deductible business expense for tenants. Landlords receiving $600 or more in annual rent from a commercial tenant must issue a 1099-NEC (Nonemployee Compensation) form. This requirement stems from the IRS’s classification of commercial rent as a service payment rather than a property payment, aligning it with the 1099-NEC’s purpose. Failure to file this form can result in penalties, emphasizing the need for meticulous record-keeping.

Other property types, such as mixed-use buildings or specialized rentals like storage units, introduce complexities. For mixed-use properties, where a single building serves both residential and commercial purposes, landlords must allocate rent payments proportionally. The commercial portion, if exceeding $600, necessitates a 1099-NEC, while the residential portion remains exempt. Storage unit rentals, often considered personal, typically do not require 1099 reporting unless tied to a business activity, such as storing inventory for resale.

Practical tips for landlords include maintaining clear lease agreements that specify property use, tracking payments meticulously, and consulting tax professionals for ambiguous cases. Tenants, particularly business owners, should verify whether their rent payments require 1099 reporting to avoid discrepancies in tax filings. Understanding these distinctions ensures compliance, minimizes audit risks, and fosters transparency in landlord-tenant relationships.

In summary, property type dictates rent reporting obligations, with residential rentals generally exempt and commercial rentals triggering 1099-NEC requirements. Mixed-use and specialized properties demand careful allocation and assessment. By adhering to these guidelines, both landlords and tenants can navigate tax season with confidence and accuracy.

Renting Mobile Hotspots in Tokyo: A Quick and Easy Guide

You may want to see also

Explore related products

![]()

Payment Thresholds: Minimum payment amounts triggering 1099-MISC or 1099-NEC requirements

Understanding payment thresholds is crucial for determining whether rent payments require a 1099-MISC or 1099-NEC. The IRS sets clear minimums: $600 in a tax year triggers reporting. This applies to payments for services, not property rentals, which typically fall under 1099-MISC for rent to individuals. However, if rent includes additional services (e.g., maintenance or utilities), the threshold still applies, but the form choice depends on the nature of the payment.

Consider a landlord paying a property manager $700 annually for rent collection and maintenance. This exceeds the $600 threshold, requiring a 1099-NEC for the service component. Conversely, if the same landlord pays a tenant $500 for property repairs, no reporting is needed unless the total reaches $600. Tracking these amounts is essential to avoid penalties for underreporting.

For businesses, the threshold remains $600, but corporations are generally exempt from receiving 1099s. For example, renting office space from a corporate landlord typically doesn’t require a 1099, even if payments exceed $600. However, payments to individuals or sole proprietors for rent or services always require scrutiny against the threshold.

Practical tips include maintaining detailed records of all payments and categorizing them accurately. Use accounting software to track totals and flag amounts nearing $600. If unsure whether a payment qualifies, consult IRS guidelines or a tax professional. Remember, the threshold applies per payee, so aggregate all payments to a single recipient annually.

In summary, the $600 threshold is a hard rule, but its application depends on the payment’s nature. Rent payments to individuals typically fall under 1099-MISC unless services are involved, which shifts to 1099-NEC. Staying vigilant about these distinctions ensures compliance and avoids costly IRS penalties.

Did Rent Live Air on Fox TV? Exploring the Broadcast

You may want to see also

Frequently asked questions

Rent payments to individuals or unincorporated businesses are typically reported on a 1099-MISC, specifically in Box 1 for rent income.

A 1099-NEC is used for reporting non-employee compensation, such as payments to independent contractors. Rent is generally not considered non-employee compensation, so a 1099-NEC is not used for rent payments.

No, rent payments made to corporations are generally exempt from 1099 reporting unless the corporation is in the legal or medical field.

Rent payments totaling $600 or more during the tax year must be reported on a 1099-MISC.

If the property management company is an unincorporated business or individual, and the rent paid totals $600 or more, you should report it on a 1099-MISC. However, if the company is incorporated, it is typically exempt from 1099 reporting.