The question of whether rent paid in advance is considered an expense is a common one in accounting and financial management. When rent is paid in advance, it typically covers a period that has not yet been utilized, such as paying for the next month’s rent at the end of the current month. From an accounting perspective, this prepayment is not immediately recognized as an expense but rather as a prepaid asset or deferred expense on the balance sheet. The expense is then recognized over the period the rent covers, usually through amortization, ensuring that the expense aligns with the period in which the benefit is received. This approach adheres to the matching principle, which requires expenses to be matched with the revenues they help generate. Thus, while rent paid in advance is a cash outflow, it is not fully expensed until the period it pertains to, making it a prepaid expense rather than an immediate one.

| Characteristics | Values |

|---|---|

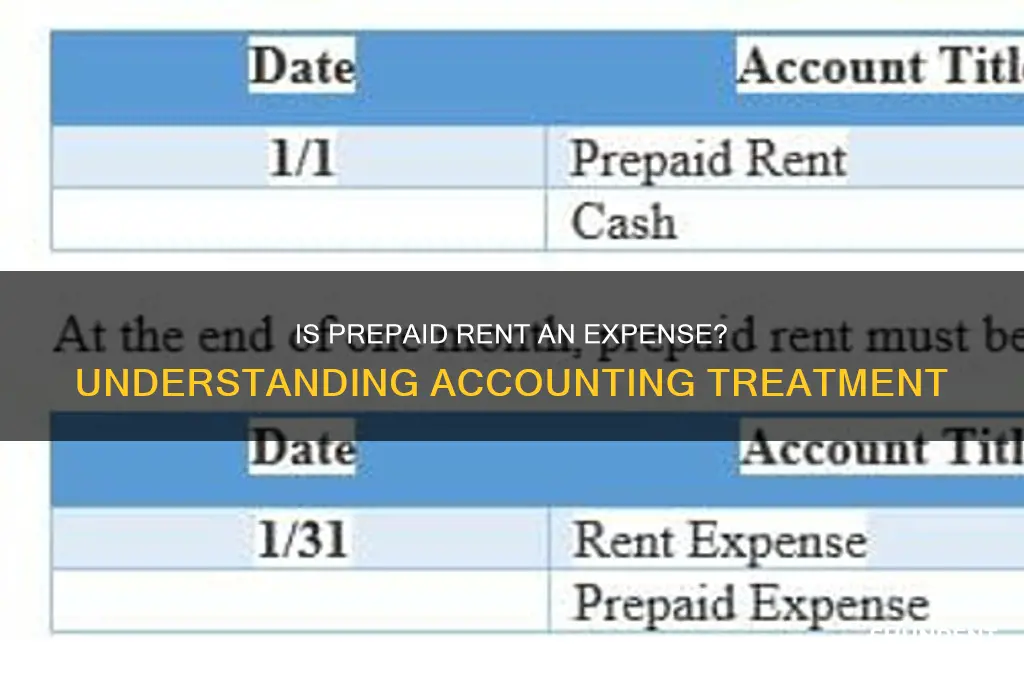

| Accounting Treatment | Prepaid rent is considered an asset (prepaid expense) until the rental period is consumed, then it becomes an expense. |

| Recognition | Recorded as an asset on the balance sheet initially, then expensed over the rental period. |

| Expense Timing | Expensed in the period the rent benefits are received, not when paid. |

| Journal Entry (Initial Payment) | Debit: Prepaid Rent (Asset), Credit: Cash |

| Journal Entry (Monthly Expense) | Debit: Rent Expense, Credit: Prepaid Rent |

| Tax Treatment | Generally not deductible in the year paid unless it covers a period within the same tax year. |

| Reporting | Reported as a current asset on the balance sheet until expensed. |

| Example | Paying $12,000 for a year’s rent in advance: $1,000 is expensed monthly as rent expense. |

| GAAP/IFRS Compliance | Complies with accrual accounting principles under both GAAP and IFRS. |

| Impact on Financial Statements | Reduces cash initially, increases assets, and later increases expenses and reduces assets. |

Explore related products

What You'll Learn

- Prepaid Rent Definition: Understanding what constitutes prepaid rent and its accounting treatment

- Expense Recognition Principle: How prepaid rent aligns with accrual accounting methods

- Balance Sheet vs. Income Statement: Classifying prepaid rent as an asset or expense

- Amortization of Prepaid Rent: Spreading the cost over the rental period

- Tax Implications: How prepaid rent affects taxable income and deductions

![]()

Prepaid Rent Definition: Understanding what constitutes prepaid rent and its accounting treatment

Prepaid rent occurs when a tenant pays for occupancy rights in advance of the period to which the payment applies. For instance, if a business pays $12,000 in January for a year’s lease, only $1,000 is considered rent expense for that month. The remaining $11,000 is classified as a prepaid asset on the balance sheet, reflecting the future economic benefit yet to be consumed. This distinction is critical in accounting to ensure expenses are matched to the periods in which they are incurred, adhering to the matching principle.

The accounting treatment of prepaid rent involves two key steps. First, record the initial payment as a debit to the prepaid rent asset account and a credit to cash. For example, if a company prepays $6,000 for six months of rent, the journal entry would be: Debit Prepaid Rent $6,000, Credit Cash $6,000. Second, as each rental period elapses, adjust the accounts to recognize the expense. Using the same example, each month would see a $1,000 debit to Rent Expense and a $1,000 credit to Prepaid Rent, gradually reducing the asset balance until it is fully expensed.

A common misconception is that prepaid rent is immediately expensed upon payment. This approach violates generally accepted accounting principles (GAAP) and distorts financial statements. By capitalizing prepaid rent as an asset, businesses accurately reflect their financial position and performance. For instance, a startup with significant prepaid rent shows stronger liquidity than if the entire amount were expensed upfront. This treatment also aligns with tax regulations, which often require prepaid expenses to be amortized over the benefit period.

Small businesses and freelancers should pay particular attention to prepaid rent, as it directly impacts cash flow and tax liabilities. For example, a freelancer prepaying $3,000 for a year’s office space should allocate $250 monthly as rent expense. This not only ensures compliance with accounting standards but also provides a clearer picture of monthly profitability. Tools like QuickBooks or Excel templates can automate these adjustments, reducing the risk of errors.

In conclusion, prepaid rent is neither an immediate expense nor a permanent asset but a temporary balance sheet item. Its proper accounting treatment—initial capitalization followed by systematic amortization—ensures financial statements accurately reflect a company’s economic reality. Whether managing a multinational corporation or a solo venture, understanding and applying these principles is essential for financial transparency and decision-making.

RV Rentals in Houston: Where to Rent Trailers?

You may want to see also

Explore related products

![]()

Expense Recognition Principle: How prepaid rent aligns with accrual accounting methods

Prepaid rent challenges traditional expense recognition because it represents a cash outflow that doesn’t immediately correspond to the period in which it’s paid. Under the Expense Recognition Principle, expenses must be matched with the revenues they help generate, regardless of when cash changes hands. For instance, if a business pays $12,000 annually for rent in January, recognizing the entire amount as an expense in that month distorts financial statements. Instead, accrual accounting spreads this cost over 12 months, aligning it with the benefits received. This method ensures that each reporting period reflects its true financial performance, avoiding artificial spikes or dips in profitability.

To implement this principle, accountants use a systematic approach. First, record the prepaid rent as an asset on the balance sheet, not as an expense. For example, a $12,000 annual rent payment would be logged as a prepaid expense. Next, allocate the cost monthly by debiting rent expense and crediting the prepaid rent account for $1,000 each month. This process, known as amortization, ensures the expense is recognized as the rented space is used. By year-end, the prepaid rent asset account is depleted, and the expense is fully recognized, maintaining accuracy in financial reporting.

A common misconception is that prepaid rent is an expense at the time of payment. However, this contradicts the matching principle, a cornerstone of accrual accounting. Consider a retail store paying rent quarterly in advance. If the $15,000 payment is expensed immediately, the quarter’s income statement would overstate expenses, underreporting profit. By deferring recognition, the business reflects only the $5,000 portion applicable to that period, providing a clearer picture of its financial health. This approach is particularly critical for long-term leases, where significant upfront payments could otherwise skew results.

For small businesses or startups, managing prepaid rent can be daunting, but tools like accounting software simplify the process. Programs like QuickBooks or Xero automate amortization schedules, reducing manual errors. For instance, a company paying $24,000 annually for office space can set up a recurring journal entry to allocate $2,000 monthly. Additionally, maintaining a separate ledger for prepaid expenses helps track remaining balances. Regularly reviewing these entries ensures compliance with accounting standards and supports informed decision-making.

In conclusion, prepaid rent aligns with accrual accounting by deferring expense recognition until the benefit is consumed. This method upholds the Expense Recognition Principle, ensuring financial statements accurately reflect a company’s operations. By treating prepaid rent as an asset initially and systematically expensing it over time, businesses avoid distortions in profitability. Whether managing a small enterprise or a large corporation, adhering to this practice fosters transparency and reliability in financial reporting.

Calculating Rent Paid in Advance: A Step-by-Step Guide for Tenants

You may want to see also

Explore related products

![]()

Balance Sheet vs. Income Statement: Classifying prepaid rent as an asset or expense

Prepaid rent presents a classification conundrum in financial reporting. While it represents money spent, its treatment differs between the balance sheet and income statement due to the timing of its benefit.

Understanding this distinction is crucial for accurate financial representation.

The Balance Sheet Perspective: An Asset in Waiting

From the balance sheet's vantage point, prepaid rent is undeniably an asset. It represents a future economic benefit – the right to occupy a property for a period already paid for. This aligns with the definition of an asset as a resource controlled by an entity, expected to generate future economic benefits. Think of it as a store of value, akin to inventory or cash, waiting to be utilized.

For instance, if a company pays $12,000 in January for a year's rent, the balance sheet would reflect $12,000 as a prepaid rent asset. As each month passes, $1,000 would be expensed, reducing the prepaid rent asset and recognizing the rent expense for that period.

The Income Statement's View: Expense Recognition Over Time

The income statement, focused on a specific period's performance, takes a different approach. Here, prepaid rent is not expensed in full at the time of payment. Instead, it's recognized as an expense gradually, matching the period in which the benefit is received. This adheres to the matching principle, a cornerstone of accrual accounting, which dictates that expenses should be matched with the revenues they help generate.

Practical Implications and Best Practices

Misclassification of prepaid rent can distort financial statements. Overstating expenses on the income statement paints an inaccurate picture of profitability, while underrepresenting assets on the balance sheet can mislead stakeholders about the company's financial health.

To ensure accuracy:

- Maintain Clear Records: Track prepaid rent payments and their corresponding periods meticulously.

- Consistent Application: Apply the same classification method consistently across reporting periods.

- Disclosure: Disclose the amount of prepaid rent in the notes to the financial statements for transparency.

Prepaid rent, though a single transaction, demands careful consideration in financial reporting. Its classification as an asset on the balance sheet and its gradual expensing on the income statement reflect the nuanced nature of accounting principles. By understanding this distinction and adhering to best practices, businesses can ensure their financial statements accurately portray their financial position and performance.

Renting Your 5th Wheel: A Step-by-Step Guide to Success

You may want to see also

![]()

Amortization of Prepaid Rent: Spreading the cost over the rental period

Prepaid rent presents a unique accounting challenge: it’s money spent now for a benefit received later. Simply expensing the full amount upfront distorts financial statements, overstating current expenses and understating future obligations. This is where amortization steps in as a critical tool for accuracy.

Think of it as slicing a pie: instead of devouring the whole thing at once, you enjoy a piece each month. Amortization spreads the prepaid rent expense evenly across the rental period, reflecting the true cost of occupancy over time.

The Mechanics of Amortization

The process is straightforward. Divide the total prepaid rent by the number of months covered by the payment. This yields the monthly amortization expense. For instance, if a company prepays $12,000 for a year's rent, the monthly amortization expense would be $1,000 ($12,000 / 12 months). This amount is then recorded as a rent expense each month, with a corresponding reduction in the prepaid rent asset account.

Example: A startup pays $6,000 in January for six months of office rent. Instead of expensing $6,000 in January, they amortize $1,000 each month for six months, accurately reflecting their monthly occupancy cost.

Why Amortization Matters

Amortization isn't just about compliance with accounting principles; it's about financial transparency and informed decision-making. By spreading the cost, businesses gain a clearer picture of their monthly expenses, enabling better budgeting and forecasting. It also prevents artificial spikes in expenses during the prepaid period, providing a more accurate representation of financial health.

Caution: While amortization is generally straightforward, complexities can arise with variable rent structures or lease agreements with escalating payments. In such cases, consult an accountant to ensure proper treatment.

Beyond the Numbers: Strategic Implications

Amortization of prepaid rent isn't merely a technical accounting adjustment; it has strategic implications. By smoothing out expenses, businesses can better assess their cash flow needs and make informed decisions about investments and growth. It also allows for more accurate comparisons of financial performance across periods, providing a clearer picture of operational efficiency.

In essence, amortization of prepaid rent is a vital tool for transforming a lump-sum payment into a series of manageable, meaningful expenses. It ensures financial statements accurately reflect the reality of a business's occupancy costs, enabling better decision-making and a clearer understanding of financial health.

Understanding Rent-to-Own Trailer Agreements: A Comprehensive Guide for Buyers

You may want to see also

![]()

Tax Implications: How prepaid rent affects taxable income and deductions

Prepaid rent, a common practice in leasing agreements, presents a unique challenge for taxpayers. The tax treatment of such payments hinges on the concept of matching expenses to the period they benefit. While paying rent in advance may offer convenience or contractual advantages, its impact on taxable income and deductions requires careful consideration to ensure compliance and optimize financial outcomes.

Understanding the Tax Principle

The Internal Revenue Service (IRS) adheres to the matching principle, which dictates that expenses should be recognized in the same period as the revenue they generate. This principle aims to provide a more accurate representation of a business's financial performance. When rent is paid in advance, the entire payment cannot be deducted in the year of payment. Instead, it must be allocated over the period to which it applies.

Allocation Methods: A Practical Approach

Taxpayers have two primary methods to allocate prepaid rent: the straight-line method and the deferral method. The straight-line method spreads the rent expense evenly over the lease term, providing a consistent deduction each year. For instance, if a business pays $12,000 in advance for a year's rent, it would deduct $1,000 per month. The deferral method, on the other hand, recognizes the entire payment as an asset initially, then expenses it as rent is consumed. This method can be more complex but may offer advantages in certain scenarios, such as when rent payments vary significantly.

Tax Planning Strategies: Maximizing Benefits

Strategic tax planning can help businesses optimize the tax implications of prepaid rent. For instance, a company expecting higher profits in the current year might benefit from prepaying rent to reduce taxable income. Conversely, if a business anticipates lower profits in the following year, deferring the deduction could be advantageous. Additionally, understanding the tax treatment of prepaid rent is crucial for accurate financial forecasting and budgeting.

Compliance and Documentation: Avoiding Pitfalls

Proper documentation is essential to support the chosen allocation method and ensure compliance with IRS regulations. Taxpayers should maintain detailed records of lease agreements, payment schedules, and calculations used to determine the rent expense for each period. Inaccurate reporting or failure to allocate prepaid rent correctly can lead to audits, penalties, and interest charges. Consulting with a tax professional can provide valuable guidance in navigating these complexities and ensuring adherence to tax laws.

In summary, prepaid rent's tax implications require a nuanced understanding of accounting principles and tax regulations. By employing appropriate allocation methods, strategic tax planning, and maintaining meticulous records, taxpayers can effectively manage the impact of prepaid rent on their taxable income and deductions, ultimately contributing to a more accurate financial picture and informed decision-making.

Oregon City Wheelchair Rentals: Your Comprehensive Accessibility Guide

You may want to see also

Frequently asked questions

Yes, rent paid in advance is considered an expense, but it is recorded as a prepaid expense on the balance sheet until the rental period is used up, at which point it is expensed on the income statement.

Rent paid in advance is initially recorded as an asset (prepaid rent) on the balance sheet. As the rental period progresses, it is gradually expensed to the income statement through amortization.

Paying rent in advance does not immediately reduce taxable income. The expense is recognized over the rental period, so the tax benefit is spread out accordingly.

Rent paid in advance cannot be fully deducted in the year it is paid. Instead, it is deducted over the period it covers, following the matching principle in accounting.