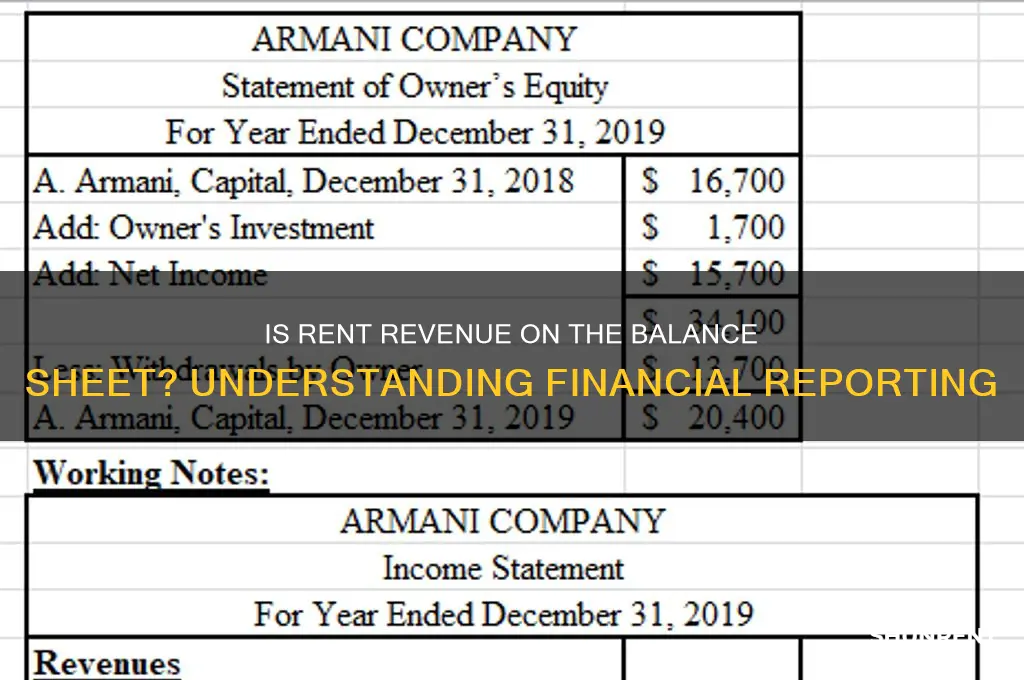

The question of whether rent revenue appears on the balance sheet is a common one in accounting, and the answer lies in understanding the fundamental differences between the income statement and the balance sheet. Rent revenue, being an income item, is typically recorded on the income statement, which summarizes a company's revenues and expenses over a specific period. The balance sheet, on the other hand, provides a snapshot of a company's financial position at a given point in time, listing its assets, liabilities, and equity. While rent revenue itself is not directly reported on the balance sheet, any unearned rent revenue or prepaid rent may be reflected as a liability or asset, respectively, depending on the specific circumstances and accounting principles applied.

| Characteristics | Values |

|---|---|

| Is rent revenue on the balance sheet? | No |

| Where is rent revenue recorded? | Income Statement (Profit and Loss Statement) |

| Why isn't rent revenue on the balance sheet? | The balance sheet shows a snapshot of a company's assets, liabilities, and equity at a specific point in time. Rent revenue is an income item that flows through the income statement, reflecting revenue earned over a period. |

| How is rent revenue classified on the income statement? | Operating Revenue (if it's a core part of the business, e.g., for a real estate company) or Non-Operating Revenue (if it's incidental, e.g., renting out a small portion of office space) |

| Is rent receivable on the balance sheet? | Yes, if rent is owed but not yet received, it is recorded as a current asset (Accounts Receivable or Rent Receivable) on the balance sheet. |

| How is prepaid rent treated? | Prepaid rent is recorded as a current asset on the balance sheet until the rental period is consumed, at which point it is expensed on the income statement. |

| Accounting standard reference | Under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), rent revenue is recognized on the income statement when earned, not on the balance sheet. |

Explore related products

What You'll Learn

- Rent Revenue Definition: Understanding rent revenue as income from leasing property, not on balance sheets

- Balance Sheet Basics: Balance sheets show assets, liabilities, equity, excluding revenue like rent

- Income Statement Role: Rent revenue appears on income statements, not balance sheets

- Accrual vs. Cash Basis: Accrual accounting records rent revenue when earned, not received

- Prepaid Rent Treatment: Prepaid rent is an asset on the balance sheet, not revenue

![]()

Rent Revenue Definition: Understanding rent revenue as income from leasing property, not on balance sheets

Rent revenue is a critical component of income for property owners and real estate investors, yet its treatment in financial statements often leads to confusion. By definition, rent revenue refers to the income generated from leasing property to tenants. This income is typically recognized on a periodic basis, such as monthly or annually, depending on the lease agreement. However, a common misconception is that rent revenue appears on the balance sheet. In reality, it is recorded on the income statement, as it represents earnings over a specific period rather than an asset or liability.

To understand why rent revenue is not on the balance sheet, consider the purpose of each financial statement. The balance sheet provides a snapshot of a company’s assets, liabilities, and equity at a specific point in time. Rent revenue, being an income item, does not fit into these categories. Instead, it is reported on the income statement, which tracks revenues and expenses over a defined period, such as a quarter or fiscal year. For example, if a landlord collects $12,000 in rent for a year, this amount would be listed under revenue on the income statement, not as an asset on the balance sheet.

A practical example can clarify this distinction. Imagine a commercial property owner who leases office space to a business for $5,000 per month. Each month, the $5,000 is recorded as rent revenue on the income statement, contributing to the owner’s total earnings. However, the balance sheet would only reflect the value of the property itself as an asset, not the ongoing rent payments. The rent revenue is transient income, not a permanent financial position, which is why it belongs on the income statement.

From a financial management perspective, this distinction is crucial for accurate reporting and analysis. Misclassifying rent revenue as an asset on the balance sheet could distort a company’s financial health, making it appear more asset-rich than it actually is. Conversely, properly recording rent revenue on the income statement provides a clear picture of cash flow and profitability. For instance, investors analyzing a real estate company’s performance would focus on the income statement to assess how much revenue is generated from rentals, rather than examining the balance sheet.

In conclusion, rent revenue is a straightforward concept—income from leasing property—but its placement in financial statements requires careful attention. By understanding that rent revenue belongs on the income statement, not the balance sheet, property owners and investors can maintain accurate financial records and make informed decisions. This clarity ensures that the transient nature of rent income is properly reflected, distinguishing it from the long-term assets and liabilities that define a company’s financial position.

When Amazon Charges for Rented Books: A Complete Guide

You may want to see also

Explore related products

![]()

Balance Sheet Basics: Balance sheets show assets, liabilities, equity, excluding revenue like rent

A balance sheet is a financial snapshot, capturing a company's financial position at a specific moment. It's divided into three main sections: assets, liabilities, and equity. These sections provide a clear picture of what a company owns, owes, and the residual value for its owners. Notably, revenue items like rent are not directly included on the balance sheet. Instead, they flow through the income statement, impacting the equity section indirectly over time.

To understand why rent revenue isn't on the balance sheet, consider the nature of this financial statement. The balance sheet is structured around the accounting equation: Assets = Liabilities + Equity. Revenue, including rent, affects equity by increasing retained earnings, but it doesn't appear as a separate line item. For instance, if a company collects $10,000 in rent, this amount would be recorded as revenue on the income statement, eventually contributing to net income, which then adjusts retained earnings in the equity section.

Let’s break this down with a practical example. Imagine a small real estate company that owns an office building. The building itself is an asset, recorded at its historical cost or fair market value. If the company leases the building and collects $50,000 in rent monthly, this revenue is recognized on the income statement. However, the balance sheet will only reflect the building’s value as an asset and any liabilities or equity changes resulting from the rent collection, such as increased cash (an asset) or reduced accounts receivable.

A common misconception is that revenue directly appears on the balance sheet. This confusion often arises because revenue impacts equity, but it’s not listed separately. For example, if a company generates $100,000 in rent revenue over a quarter, this amount would increase net income on the income statement, which then flows into retained earnings on the balance sheet. The balance sheet, however, will show the effect of this revenue indirectly through changes in cash, accounts receivable, or retained earnings, not as a standalone item.

To ensure clarity, always distinguish between the income statement and the balance sheet. The income statement tracks revenue and expenses over a period, while the balance sheet provides a static view of assets, liabilities, and equity at a specific point. For businesses dealing with significant rental income, it’s crucial to accurately record rent revenue on the income statement and understand how it indirectly influences the balance sheet. This distinction is fundamental for financial analysis and decision-making, ensuring a clear and accurate representation of a company’s financial health.

Food Truck Rental Costs: What to Expect for Your Business

You may want to see also

Explore related products

![]()

Income Statement Role: Rent revenue appears on income statements, not balance sheets

Rent revenue is a critical component of a company's financial performance, but its placement in financial statements is often misunderstood. Unlike assets or liabilities, rent revenue does not appear on the balance sheet. Instead, it is exclusively recorded on the income statement, where it reflects the company's earnings over a specific period. This distinction is fundamental for accurately interpreting financial health and operational efficiency.

To understand why rent revenue belongs on the income statement, consider its nature as an operating activity. The income statement tracks revenues and expenses over a period, such as a quarter or fiscal year, to determine net income or loss. Rent revenue, whether from leasing property or equipment, is a recurring income stream directly tied to business operations. For instance, a real estate company’s rent revenue from tenants is reported here, alongside other operational revenues like sales or service fees. This placement ensures that stakeholders can assess how effectively the company generates income from its core activities.

Contrastingly, the balance sheet provides a snapshot of a company’s financial position at a single point in time, listing assets, liabilities, and equity. Rent revenue does not qualify for inclusion here because it is not a resource owned or controlled by the company. Instead, it is a flow of income that impacts profitability, not a static element of financial structure. For example, while a building owned by a company appears as an asset on the balance sheet, the rent collected from leasing that building is reported on the income statement as revenue.

A practical tip for financial analysis is to examine the income statement’s revenue section to gauge the stability and growth of rent income. If rent revenue constitutes a significant portion of total revenue, it highlights the company’s reliance on leasing activities. Conversely, a decline in rent revenue may signal challenges such as tenant turnover or market downturns. By focusing on this line item, investors and managers can make informed decisions about operational strategies and risk management.

In summary, rent revenue’s placement on the income statement, not the balance sheet, underscores its role as a dynamic indicator of operational performance. This distinction is crucial for accurate financial analysis and strategic planning. By understanding this categorization, stakeholders can better evaluate a company’s ability to generate sustainable income from its leasing activities.

Can You Rent a Chain? Exploring Unconventional Rental Options

You may want to see also

Explore related products

![]()

Accrual vs. Cash Basis: Accrual accounting records rent revenue when earned, not received

Rent revenue is a critical component of financial reporting, but its treatment differs significantly between accrual and cash basis accounting. Under accrual accounting, rent revenue is recognized when it is earned, regardless of when the payment is received. This means that if a tenant signs a lease agreement on January 1 for a year-long rental period, the full year’s rent is recorded as revenue in January, even if the payment is made in monthly installments. This approach aligns revenue with the period in which it is actually earned, providing a more accurate picture of financial performance. For instance, a commercial landlord leasing office space would record the entire year’s rent as revenue upfront, reflecting the economic substance of the agreement rather than the timing of cash flows.

In contrast, cash basis accounting records rent revenue only when the payment is received. Using the same example, if the tenant pays rent monthly, the landlord would recognize revenue in 12 separate installments throughout the year. This method is simpler and may be suitable for small businesses or individuals, but it fails to match revenue with the period in which it is earned. For larger entities or those with complex lease agreements, this mismatch can distort financial statements, making it harder to assess true profitability or financial health. For example, a real estate investment trust (REIT) relying on cash basis accounting might show fluctuating revenue due to payment timing, even if its leasing activity remains consistent.

The choice between accrual and cash basis accounting has practical implications for balance sheet presentation. Under accrual accounting, rent revenue is recorded as earned, and if payment is not yet received, it is offset by an accounts receivable entry on the balance sheet. This ensures that both revenue and the corresponding asset are reflected, maintaining the balance sheet equation. Conversely, cash basis accounting does not record revenue until payment is received, meaning there is no accounts receivable entry. As a result, the balance sheet may underrepresent the company’s financial position, particularly if significant rent payments are due but not yet collected.

For businesses, understanding these differences is crucial for compliance and decision-making. Accrual accounting is generally required under GAAP (Generally Accepted Accounting Principles) for publicly traded companies and many private entities, as it provides a more accurate representation of financial performance. However, smaller businesses may opt for cash basis accounting due to its simplicity. A practical tip for transitioning from cash to accrual basis is to review all lease agreements and create a schedule of earned but unreceived rent, ensuring proper recognition and balance sheet accuracy. This step is particularly important during audits or when seeking financing, as lenders and investors often scrutinize revenue recognition practices.

In conclusion, the treatment of rent revenue under accrual versus cash basis accounting highlights a fundamental difference in financial reporting philosophy. Accrual accounting prioritizes the matching principle, recognizing revenue when earned, while cash basis focuses on the timing of cash flows. For businesses managing rental properties or lease agreements, choosing the right method impacts not only income statements but also balance sheet accuracy. By understanding these nuances, companies can ensure compliance, improve financial transparency, and make more informed strategic decisions.

The Tragic Death of Rent Director Jonathan Larson Explored

You may want to see also

Explore related products

![]()

Prepaid Rent Treatment: Prepaid rent is an asset on the balance sheet, not revenue

Prepaid rent, a common transaction in business operations, often sparks confusion regarding its classification on the balance sheet. Unlike rent revenue, which is recognized in the income statement, prepaid rent is not a revenue item. Instead, it represents an advance payment for future rental periods, making it a current asset on the balance sheet. This distinction is crucial for accurate financial reporting and understanding a company’s liquidity position. For instance, if a company pays $12,000 for a year’s rent in advance, this amount is recorded as prepaid rent, not as revenue, and is gradually expensed over the rental period.

To properly account for prepaid rent, follow these steps: first, record the full payment as a debit to the prepaid rent account (an asset) and a credit to cash. Second, as each rental period passes, recognize the portion of rent used by debiting rent expense and crediting prepaid rent. For example, if a $12,000 annual payment is made in January for 12 months, $1,000 is expensed monthly. This method ensures the asset is reduced over time, reflecting the consumption of the prepaid benefit.

A comparative analysis highlights the difference between prepaid rent and rent revenue. While rent revenue is earned by landlords and recorded when due, prepaid rent is an outlay by tenants for future use. This contrasts with revenue recognition principles, which require income to be matched with the period it is earned. Prepaid rent, however, aligns with the matching principle by deferring the expense to the periods benefiting from the rental agreement. This treatment avoids distorting financial statements by misclassifying assets as income.

Practical tips for managing prepaid rent include maintaining detailed schedules to track expiration dates and amounts, ensuring timely adjustments. For businesses with multiple leases, consider using accounting software to automate expense recognition. Additionally, review prepaid rent balances quarterly to verify accuracy and alignment with lease agreements. Misclassification of prepaid rent as revenue can mislead stakeholders about a company’s financial health, emphasizing the need for precision in accounting practices.

In conclusion, prepaid rent’s treatment as an asset, not revenue, is a fundamental accounting principle. By understanding this distinction and applying proper recording methods, businesses can maintain transparent and accurate financial statements. This clarity not only aids in compliance with accounting standards but also provides a true picture of a company’s short-term resources and obligations.

Elderly Scooter Rentals: Convenient Mobility Solutions for Seniors Nearby

You may want to see also

Frequently asked questions

No, rent revenue is not reported on the balance sheet. It is recorded on the income statement as part of the company's operating income.

Rent revenue is recorded on the income statement under the revenue or sales section, as it represents income generated from rental activities.

Rent revenue is not on the balance sheet because it is a revenue item, which reflects income over a period. The balance sheet shows assets, liabilities, and equity at a specific point in time.

Rent revenue indirectly affects the balance sheet by increasing retained earnings (if profitable) or cash balances when received, which are reflected in the asset section of the balance sheet.