Renting for life has become an increasingly popular option as housing prices soar and financial priorities shift, prompting many to question whether it’s a smarter choice than buying a home. Advocates argue that renting offers flexibility, lower upfront costs, and freedom from maintenance responsibilities, making it ideal for those who value mobility or prefer not to tie up capital in property. However, critics point out that renting long-term can lead to a lack of equity, rising rental costs, and limited control over living spaces, potentially leaving individuals financially vulnerable in retirement. Whether renting for life is a good idea depends on individual circumstances, such as income stability, lifestyle preferences, and long-term financial goals, making it a decision that requires careful consideration of both immediate benefits and future implications.

Explore related products

What You'll Learn

![]()

Financial Flexibility vs. Long-Term Costs

Renting offers unparalleled financial flexibility, a benefit that cannot be overstated in an unpredictable economy. When you rent, you’re not tied to a 30-year mortgage or the hidden costs of homeownership, such as property taxes, maintenance, and repairs. For instance, a renter can relocate for a job opportunity without the burden of selling a home, potentially saving thousands in closing costs and real estate fees. This agility is particularly valuable for young professionals or those in dynamic industries. A study by the Urban Institute found that renters are more likely to move for career advancement, highlighting how renting can align with long-term financial growth through increased earning potential.

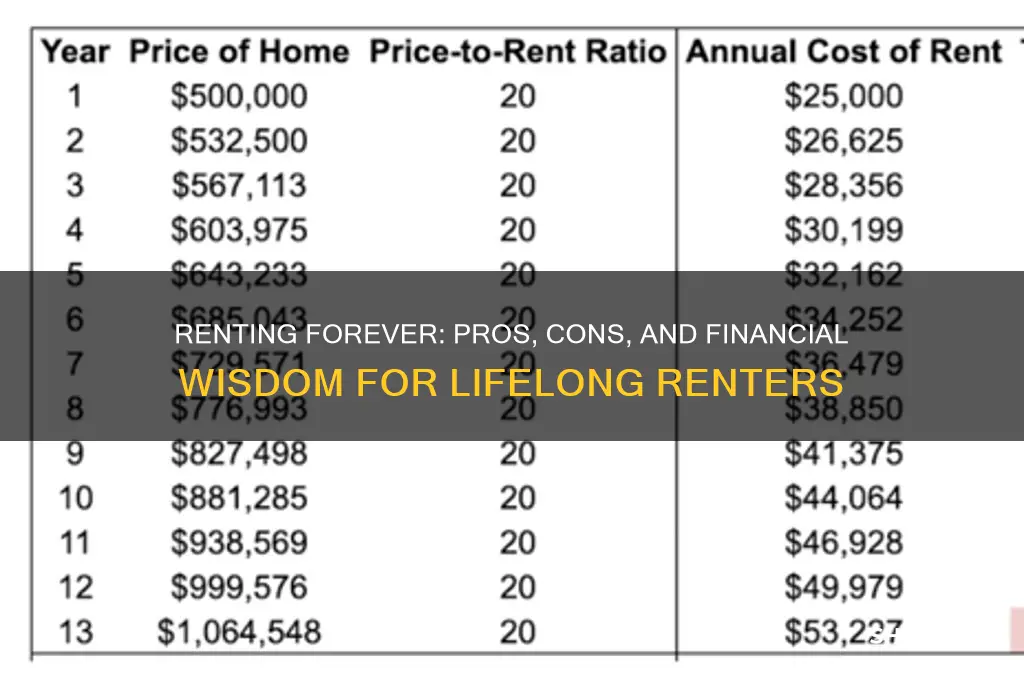

However, this flexibility comes with a trade-off: long-term costs. Rent prices are subject to market fluctuations, and while homeowners build equity over time, renters pay into an asset they’ll never own. Consider this: if you rent a $1,500 apartment for 30 years, you’ll spend $540,000 without any return on investment. In contrast, a homeowner with a $300,000 mortgage at 4% interest would pay approximately $516,000 over 30 years but retain an asset that could appreciate in value. To mitigate this, renters should prioritize saving and investing the difference between rent and mortgage payments—ideally in a diversified portfolio or retirement account—to ensure they’re not falling behind in wealth accumulation.

A practical strategy for renters is to adopt a "rent-to-invest" mindset. Allocate 20-30% of what you save on homeownership costs (e.g., maintenance, property taxes) into a high-yield savings account or index fund. For example, if renting saves you $300 monthly compared to owning, invest $90-$180 of that into an S&P 500 index fund, which historically yields an average annual return of 7-10%. Over 30 years, this could grow to $150,000-$250,000, partially offsetting the lack of home equity. Additionally, renters should negotiate lease terms, such as rent stabilization or long-term contracts, to lock in rates and reduce exposure to market volatility.

Ultimately, the decision between renting and buying hinges on your financial priorities and risk tolerance. Renting provides immediate flexibility and lower upfront costs, making it ideal for those who value mobility or prefer not to manage property. However, it requires disciplined saving and investing to avoid long-term financial disadvantages. Homeownership, while less flexible, offers equity-building and potential tax benefits. For those unsure, consider a hybrid approach: rent while saving aggressively for a down payment, ensuring you’re financially prepared to buy when the time is right. The key is to align your housing choice with your broader financial goals, not just short-term convenience.

Top Florida Locations to Rent a Dodge Truck Easily

You may want to see also

Explore related products

![]()

Lack of Equity and Asset Building

One of the most significant drawbacks of renting for life is the absence of equity accumulation. When you rent, your monthly payments contribute to the landlord’s wealth, not your own. Over time, this can result in a substantial financial gap. For instance, a $1,500 monthly rent payment over 30 years totals $540,000, money that could have been invested in a mortgage to build home equity. Unlike homeowners, renters miss out on the forced savings mechanism of paying down a loan, which gradually increases their net worth.

Consider the long-term implications of this financial structure. Homeownership allows individuals to leverage equity for major expenses, such as education or business ventures, through loans or lines of credit. Renters, however, must rely on personal savings or high-interest debt for such needs. For example, a homeowner with $100,000 in equity can access funds at a lower interest rate compared to a renter using credit cards or personal loans. This disparity highlights how renting limits financial flexibility and asset growth.

To mitigate the lack of equity, renters must adopt disciplined saving and investing strategies. Allocate a portion of your income—ideally 15–20%—to tax-advantaged retirement accounts and diversified investment portfolios. For instance, contributing $500 monthly to an index fund with a 7% annual return could grow to over $1 million in 40 years. Additionally, consider investing in real estate through REITs (Real Estate Investment Trusts) to gain exposure to property markets without owning a home.

However, renting isn’t inherently detrimental to wealth-building if approached strategically. Evaluate your lifestyle and financial goals. If you prioritize mobility, lower maintenance costs, or live in an area with high property taxes, renting may free up resources for other investments. For example, a renter in San Francisco could save $30,000 annually by renting instead of buying, funds that could be redirected to stocks, bonds, or entrepreneurship. The key is to ensure that the money saved from renting is actively invested, not spent on non-essential expenses.

Ultimately, the decision to rent for life requires a clear understanding of opportunity costs. While renters avoid the risks of property depreciation or market downturns, they also forgo the potential for significant asset appreciation. For those committed to renting, treating rent payments as a baseline expense and systematically investing the difference between renting and owning costs is crucial. By doing so, renters can still build wealth, though the path may differ from traditional homeownership.

Rent HD or SD for iPad: Which Option is Right for You?

You may want to see also

Explore related products

![]()

Mobility and Lifestyle Benefits

Renting for life offers unparalleled mobility, a benefit that aligns with the increasingly transient nature of modern careers and personal aspirations. For professionals in tech, consulting, or entertainment, job opportunities often arise in different cities or even countries. Renting eliminates the burden of selling a home, allowing individuals to relocate swiftly without financial or logistical delays. Consider the case of a software engineer who receives a job offer in Silicon Valley after years in Austin. A renter can simply terminate their lease (typically with 30 to 60 days’ notice) and move, whereas a homeowner would face months of listing, negotiating, and closing—potentially missing the opportunity altogether.

This mobility extends beyond career shifts to lifestyle preferences. Renting enables individuals to live in diverse environments without long-term commitments. A young couple might rent a downtown apartment for urban convenience, then transition to a suburban rental with more space as their family grows. Retirees could spend winters in a warm-climate rental and summers in a cooler region, tailoring their living situation to seasonal preferences. This flexibility is particularly appealing in an era where experiences often take precedence over permanence.

However, mobility comes with trade-offs. Frequent moves can disrupt social networks and community ties, which are essential for mental health and well-being. Renters must also navigate varying rental markets, where costs and availability fluctuate. For instance, a move from a low-cost city like Indianapolis to a high-cost city like San Francisco could double monthly rent, requiring careful financial planning. To mitigate this, renters should allocate 30–40% of their income to housing and maintain an emergency fund equivalent to 3–6 months’ rent.

Despite these challenges, renting fosters a lifestyle of adaptability and exploration. It suits those who prioritize variety over stability, whether for career growth, personal discovery, or simply the joy of new environments. For example, a freelance photographer might rent in different cities to immerse themselves in local cultures, enhancing their work and life experiences. This approach requires intentionality—renters must balance the freedom to move with the need for consistency in other areas, such as relationships or financial goals.

Ultimately, the mobility and lifestyle benefits of renting for life are most valuable for individuals whose priorities align with flexibility and change. It’s not a one-size-fits-all solution but a strategic choice for those who view life as a series of chapters rather than a single, static narrative. By embracing renting, they gain the freedom to write those chapters wherever and however they choose.

Counting Christmas Mentions in Rent: A Festive Phrase Analysis

You may want to see also

Explore related products

![The Art of Being Human: The Humanities as a Technique for Living [RENTAL EDITION]](https://m.media-amazon.com/images/I/419LnNiWDSS._AC_UY218_.jpg)

![]()

Maintenance-Free Living Advantages

One of the most compelling arguments for renting for life is the promise of maintenance-free living. Homeownership often comes with a laundry list of responsibilities: fixing leaky roofs, mowing lawns, replacing aging appliances, and addressing unexpected repairs. Renting shifts these burdens to landlords or property managers, freeing tenants from both the financial and time-consuming demands of upkeep. For instance, a 2022 study by the National Association of Home Builders found that homeowners spend an average of $4,000 annually on maintenance and repairs, a cost renters avoid entirely. This financial predictability is particularly appealing for retirees, young professionals, or anyone seeking to simplify their lifestyle.

Consider the practical implications of this arrangement. Renters can allocate the time and money saved on maintenance to other priorities, such as travel, hobbies, or investments. For example, instead of spending weekends fixing a broken furnace, a renter might take a weekend trip or enroll in a skill-building course. This shift in focus from property upkeep to personal enrichment can significantly enhance quality of life. Additionally, renters often benefit from amenities like on-site maintenance teams, which can resolve issues within hours, compared to the days or weeks homeowners might wait for a contractor.

However, it’s essential to weigh the trade-offs. While maintenance-free living is a significant advantage, renters sacrifice control over their living space. Landlords may be slow to address non-urgent issues or restrict modifications, such as painting walls or installing custom fixtures. To maximize the benefits of this lifestyle, renters should prioritize properties with responsive management and clear maintenance policies. Reading reviews, asking about average response times, and understanding lease terms can help ensure a smooth experience.

For those considering renting for life, the maintenance-free aspect is a powerful incentive, but it’s not one-size-fits-all. Families with long-term plans might find the lack of customization limiting, while individuals or couples seeking flexibility may thrive. A useful tip is to create a "maintenance budget" for your current living situation and compare it to the cost of renting. If the difference is substantial, renting could offer not just convenience but also financial freedom. Ultimately, maintenance-free living is about reclaiming time and resources—a trade many find well worth making.

Is Renting a Condo Off Craigslist Safe? Tips and Warnings

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![]()

Renting in Rising Housing Markets

In rising housing markets, the decision to rent indefinitely becomes a strategic choice rather than a default option. As home prices climb, the traditional advice to "buy now or regret later" loses its universality. Renting allows flexibility, a critical advantage when markets are volatile. For instance, in cities like Austin or Phoenix, where home values surged over 30% in the past two years, renters avoided being locked into mortgages at peak prices. This section explores how renting can be a savvy move in such environments, balancing financial prudence with lifestyle adaptability.

Consider the math: In markets where home prices rise 10–15% annually, the pressure to buy intensifies. However, renting offers a hedge against overpaying. For example, if a $500,000 home appreciates to $575,000 in a year, the $75,000 difference could fund years of rent in many areas. Additionally, renters avoid hidden costs like property taxes, maintenance, and HOA fees, which can add 2–4% to annual homeownership expenses. A comparative analysis shows that in high-growth markets, renting often preserves capital better than buying, especially for those unwilling to commit long-term.

To maximize renting in rising markets, adopt a proactive approach. First, negotiate lease terms that cap rent increases, ideally below market appreciation rates. Second, invest the difference between rent and potential mortgage payments into diversified assets like index funds or real estate ETFs, which historically yield 7–10% annually. Third, stay mobile; renters can relocate to emerging neighborhoods before they gentrify, locking in lower rents. For instance, renters in Brooklyn’s Bushwick in the early 2010s paid half the rent of newcomers a decade later.

However, renting in rising markets isn’t without risks. Rent control laws are rare in the U.S., leaving tenants vulnerable to sudden hikes. To mitigate this, prioritize areas with stable rental markets or landlords offering multi-year leases. Additionally, track local zoning changes and development plans, as these can signal future rent spikes. For example, a new tech hub announcement in a neighborhood often precedes 20–30% rent increases within two years. Staying informed allows renters to pivot before costs escalate.

Ultimately, renting in rising housing markets is a tactical decision suited for specific profiles: young professionals, remote workers, or those prioritizing liquidity over equity. It’s not about avoiding homeownership but timing it strategically. By treating rent as a tool rather than a burden, individuals can navigate volatile markets while building wealth elsewhere. The takeaway? In a landscape where home prices outpace incomes, renting isn’t just a fallback—it’s a financial lever.

Renting Your RV: A Step-by-Step Guide to Maximize Profits

You may want to see also

Frequently asked questions

Renting can be a good idea if you value flexibility and mobility, as it allows you to move without the commitment of selling a property. However, it lacks the long-term financial benefits of homeownership, such as equity building.

Renting may be financially smarter if you live in an area with high property prices, unpredictable housing markets, or if you prefer not to deal with maintenance costs. However, over time, renting can mean missing out on potential property appreciation and tax benefits associated with homeownership.

Renting can be a good idea for retirees or those on a fixed income because it eliminates the unpredictability of property taxes, maintenance, and repairs. It also provides flexibility to downsize or relocate as needs change, though it’s important to ensure rental costs remain manageable within your budget.

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)