When considering rental income for tax purposes, it’s essential to understand whether renting itself is included in rental income expenses. Generally, rental income refers to the revenue earned from leasing property, while rental expenses encompass costs directly associated with maintaining and managing the rental property, such as repairs, maintenance, property management fees, and insurance. Renting, as an activity, is not an expense but rather the source of the income. However, the costs incurred to facilitate renting, such as advertising for tenants or legal fees for lease agreements, can be deducted as rental expenses. Therefore, while renting itself is not an expense, the associated costs of managing and maintaining the rental property are deductible against rental income, reducing taxable profit.

| Characteristics | Values |

|---|---|

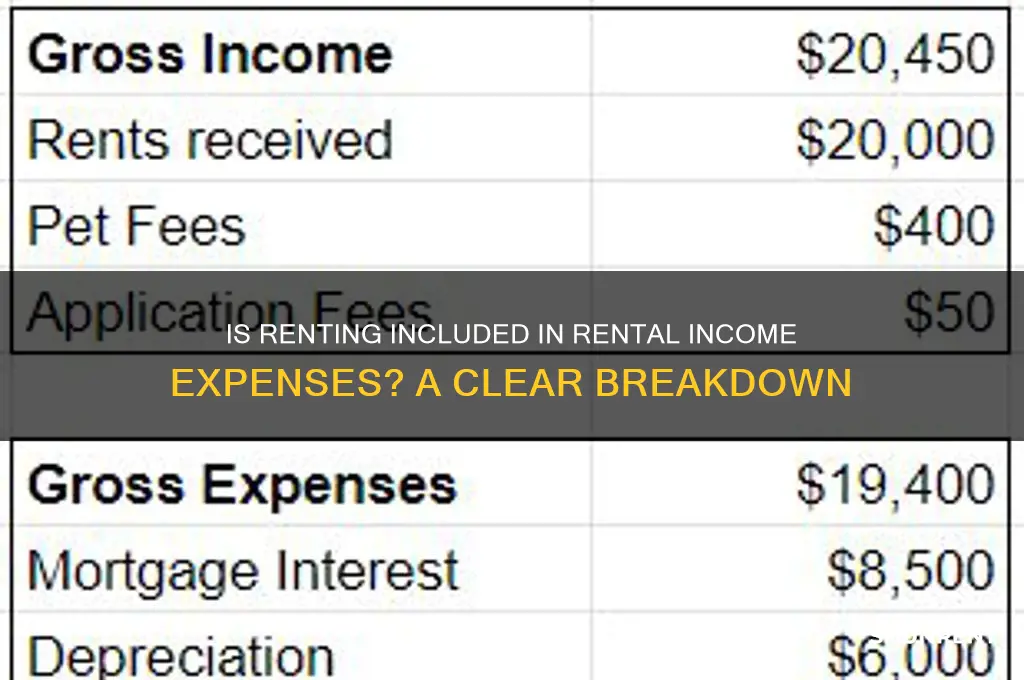

| Is Rent Included in Rental Income Expenses? | No, rent received is considered income, not an expense. |

| What is Rental Income? | Money received from tenants for occupying a property. |

| What are Rental Expenses? | Costs incurred to maintain and manage the rental property, deductible from rental income for tax purposes. |

| Examples of Rental Expenses | Mortgage interest, property taxes, insurance, repairs, maintenance, property management fees, depreciation, advertising, legal fees, utilities (if paid by landlord) |

| Tax Treatment | Rental income is taxable, while eligible rental expenses reduce taxable rental income. |

| IRS Publication | Refer to IRS Publication 527, Residential Rental Property, for detailed guidance on rental income and expenses. |

Explore related products

What You'll Learn

- Rent Payments: Are monthly rent payments considered part of rental income expenses

- Property Taxes: Do property taxes paid by landlords count as rental expenses

- Maintenance Costs: Is routine maintenance included in rental income expenses

- Insurance Premiums: Are landlord insurance premiums deductible as rental expenses

- Utilities Coverage: Do utilities paid by landlords qualify as rental income expenses

![]()

Rent Payments: Are monthly rent payments considered part of rental income expenses?

Monthly rent payments are a cornerstone of the landlord-tenant relationship, but their classification in financial terms can be nuanced. From a tenant’s perspective, rent is an expense—a cost of securing housing. For landlords, however, rent payments are income, representing the revenue generated from leasing property. This fundamental distinction is critical for understanding how rent fits into the broader category of rental income expenses. While rent itself is not an expense for the landlord, the costs associated with maintaining the rental property (e.g., repairs, property taxes, mortgage interest) are deductible expenses against that rental income.

Consider the tax implications for landlords. The IRS allows deductions for expenses directly tied to earning rental income, such as property management fees, insurance, and depreciation. However, the rent payment itself is not deductible because it is the income being taxed. For example, if a landlord collects $1,200 in monthly rent and spends $300 on maintenance, the $300 is an expense, but the $1,200 rent is the gross income against which those expenses are offset. This separation ensures landlords report their net rental income accurately, avoiding overstated deductions or underreported earnings.

Tenants often mistakenly assume their rent payments are tax-deductible, but this is generally not the case. The IRS allows deductions for rent only in specific scenarios, such as renting a portion of a home for business use or qualifying for certain housing assistance programs. For instance, self-employed individuals working from a home office may deduct a portion of their rent proportional to the space used for business. Otherwise, rent remains a personal expense, not a deductible item on individual tax returns.

A comparative analysis highlights the asymmetry between landlords and tenants. While landlords treat rent as income and associated costs as expenses, tenants view rent as a liability with limited opportunities for financial relief. This disparity underscores the importance of understanding tax laws and property management principles. For landlords, meticulous record-keeping of expenses is essential to maximize deductions and minimize tax liability. Tenants, meanwhile, should explore state or local rent assistance programs or housing credits to offset their rental costs.

In practical terms, landlords can optimize their financial position by categorizing expenses correctly. For example, a landlord with a $15,000 annual rental income and $5,000 in deductible expenses (repairs, insurance, etc.) would report $10,000 in taxable rental income. Tenants, on the other hand, should focus on budgeting strategies, such as negotiating lease terms or seeking rent-controlled units, to manage their housing costs effectively. Both parties benefit from clarity on how rent payments and related expenses are treated, ensuring compliance and financial efficiency.

Crafting the Perfect Email: Tips for Renters Contacting Homeowners

You may want to see also

Explore related products

![]()

Property Taxes: Do property taxes paid by landlords count as rental expenses?

Landlords often face a maze of financial considerations, and one question that frequently arises is whether property taxes can be deducted as rental expenses. The answer is a clear yes—property taxes paid by landlords on rental properties are generally deductible. This deduction is a significant benefit, as it reduces the taxable rental income, thereby lowering the overall tax liability. However, the specifics can vary depending on local tax laws and how the property is used, so it’s essential to understand the rules to maximize this advantage.

To claim property taxes as a rental expense, the property must be used for rental purposes. For example, if a landlord owns a duplex and lives in one unit while renting out the other, only the portion of property taxes attributable to the rental unit is deductible. This allocation is typically based on the percentage of the property used for rental activities. For instance, if 50% of the property is rented, 50% of the property taxes can be claimed as a rental expense. Accurate record-keeping is crucial to substantiate these deductions during tax filings.

Another critical aspect is timing. Property taxes are deductible in the year they are paid, not the year they are assessed. For instance, if a landlord pays 2023 property taxes in January 2024, the deduction would be claimed on the 2024 tax return. This rule ensures compliance with the IRS’s cash basis accounting method, which is commonly used by individual landlords. Landlords using the accrual method may have different rules, but most opt for the simpler cash basis approach.

While property taxes are deductible, it’s important to distinguish them from other non-deductible expenses. For example, fines or penalties related to late property tax payments are not deductible. Additionally, if a landlord improves the property—such as adding a new roof—the cost is capitalized and depreciated over time rather than deducted as an immediate expense. Understanding these distinctions ensures landlords accurately report their rental income and expenses.

Practical tips for landlords include maintaining detailed records of property tax payments, including receipts and assessment notices. Using accounting software or spreadsheets can streamline this process. Consulting a tax professional is also advisable, especially for landlords with multiple properties or complex rental scenarios. By leveraging property tax deductions effectively, landlords can optimize their financial outcomes and ensure compliance with tax regulations.

Personal vs. Company Rent Collection: Pros, Cons, and Best Practices

You may want to see also

Explore related products

![]()

Maintenance Costs: Is routine maintenance included in rental income expenses?

Routine maintenance is a critical aspect of property management, yet its classification as a deductible rental income expense often confuses landlords. The IRS allows deductions for expenses that are "ordinary and necessary" for managing rental property. Routine maintenance, such as fixing leaky faucets, repainting walls, or replacing worn-out locks, falls squarely into this category. These tasks preserve the property’s condition and habitability, making them essential for generating rental income. However, distinguishing between routine maintenance and capital improvements is key. While the former is deductible in the year incurred, the latter must be depreciated over time. For instance, repairing a roof leak is maintenance, but replacing the entire roof is an improvement.

To maximize deductions, landlords should maintain detailed records of all maintenance activities. Receipts, invoices, and a log of repairs are indispensable. For example, if a landlord spends $500 on plumbing repairs in a year, this amount can be fully deducted from rental income. Additionally, preventive maintenance, like annual HVAC inspections or gutter cleaning, also qualifies. These proactive measures not only reduce long-term costs but also demonstrate a landlord’s commitment to property upkeep, which can be beneficial during tax audits.

A comparative analysis reveals that while routine maintenance is universally deductible, the treatment of maintenance costs varies internationally. In the UK, for instance, landlords can deduct "wear and tear" allowances, though this has been replaced by a system allowing deductions for actual costs incurred. In contrast, Canadian landlords can claim expenses for repairs but not for improvements, similar to the U.S. system. Understanding these nuances is crucial for landlords operating across borders or seeking to benchmark their practices against global standards.

Persuasively, landlords should view routine maintenance not merely as an expense but as an investment in their rental property’s longevity and value. Neglecting maintenance can lead to larger, costlier repairs and tenant dissatisfaction, potentially reducing rental income. For example, ignoring a small roof leak can result in water damage costing thousands to repair. By prioritizing routine maintenance, landlords ensure their properties remain attractive to tenants, thereby stabilizing rental income and minimizing vacancies.

In conclusion, routine maintenance is unequivocally included in rental income expenses, provided it is ordinary and necessary. Landlords should adopt a proactive approach, maintain meticulous records, and stay informed about tax regulations to optimize their deductions. By doing so, they not only comply with legal requirements but also safeguard their investment and enhance their property’s appeal.

Finding the Perfect Commercial Office Space for Rent in Ohio

You may want to see also

Explore related products

$10.9

![]()

Insurance Premiums: Are landlord insurance premiums deductible as rental expenses?

Landlord insurance premiums are a critical expense for property owners, but their deductibility as rental expenses often raises questions. The Internal Revenue Service (IRS) allows landlords to deduct insurance premiums if they are ordinary and necessary for managing or maintaining rental property. This includes policies covering fire, theft, liability, and other risks specific to the rental business. However, personal insurance unrelated to the rental activity, such as homeowner’s insurance for a primary residence, is not deductible as a rental expense. Understanding this distinction is essential for accurate tax reporting and maximizing deductions.

To qualify for a deduction, the insurance policy must directly relate to the rental property. For example, landlord insurance covering rental income loss due to tenant damage or vacancy is deductible. Similarly, liability insurance protecting against tenant lawsuits is eligible. However, if a policy includes coverage for personal belongings or non-rental property, only the portion attributable to the rental activity can be deducted. Landlords should carefully review their policies and allocate premiums accordingly to ensure compliance with IRS guidelines.

A practical tip for landlords is to maintain detailed records of insurance payments and policies. Documentation should clearly link each premium to the rental property, including policy descriptions, payment receipts, and any correspondence with insurers. This not only simplifies tax preparation but also provides evidence in case of an audit. Additionally, consulting a tax professional can help landlords navigate the complexities of deducting insurance premiums, especially when policies cover multiple properties or include mixed-use elements.

Comparatively, while landlord insurance premiums are deductible, other insurance-related costs may not qualify. For instance, premiums for health, life, or disability insurance are generally not deductible as rental expenses. Similarly, insurance for personal vehicles, even if used for property management, falls outside the scope of rental deductions. Landlords should focus on policies directly tied to the rental property’s operation and maintenance to avoid disallowed deductions.

In conclusion, landlord insurance premiums are deductible as rental expenses when they are directly related to the management and protection of rental property. By understanding IRS rules, maintaining thorough records, and seeking professional advice, landlords can confidently claim these deductions while avoiding common pitfalls. This approach not only optimizes tax benefits but also ensures compliance with federal regulations, contributing to a more efficient and profitable rental business.

Renting a Canoe at Lake Louise: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Utilities Coverage: Do utilities paid by landlords qualify as rental income expenses?

Landlords often cover utility expenses as part of their rental agreements, but the tax implications of this practice are frequently misunderstood. When a landlord pays for utilities like electricity, water, or gas, these costs can be deducted as rental income expenses on their tax returns. The Internal Revenue Service (IRS) allows such deductions because they are considered ordinary and necessary expenses for maintaining the rental property. However, the specifics depend on how the utilities are structured in the lease agreement and whether they are directly tied to the property’s operation.

For instance, if a landlord includes utilities in the rent and pays them directly, these payments are deductible as part of the property’s operating expenses. This is because the utilities are essential for the property’s habitability and the landlord’s ability to generate rental income. Conversely, if utilities are separately metered and paid by the tenant, they do not qualify as a landlord’s expense. Documentation is key here—landlords should maintain records of utility payments and ensure they are clearly linked to the rental property to substantiate their deductions during tax filings.

A comparative analysis reveals that landlords who bundle utilities into rent often benefit from simplified expense tracking and tax deductions. However, this approach may reduce the overall rental income reported, which could impact loan eligibility or property valuation. On the other hand, landlords who require tenants to pay utilities directly may report higher rental income but lose the ability to deduct those specific expenses. The choice depends on the landlord’s financial strategy and the local rental market dynamics.

To maximize tax benefits, landlords should consider the following steps: first, review lease agreements to ensure utility coverage is clearly defined. Second, separate utility expenses from personal ones to avoid complications during audits. Third, consult a tax professional to confirm eligibility for deductions based on the property’s location and tax laws. For example, some states may have specific regulations regarding utility deductions for multi-unit properties.

In conclusion, utilities paid by landlords qualify as rental income expenses when they are directly associated with the rental property and properly documented. This not only reduces taxable rental income but also reflects the true cost of maintaining the property. By understanding these nuances, landlords can optimize their tax strategies and ensure compliance with IRS regulations. Practical tips include using property management software to track utility payments and staying informed about annual tax law changes that may affect deductions.

Key Considerations for Renting the Perfect Acupuncture Office Space

You may want to see also

Frequently asked questions

No, the rent you pay for your personal residence is not considered a rental income expense. Rental income expenses are costs directly related to managing and maintaining rental properties you own, not your personal living expenses.

Yes, property management fees are typically included in rental income expenses, as they are costs incurred for managing and maintaining your rental property, which can be deducted from your rental income.

Yes, repairs and maintenance costs directly related to your rental property are considered rental income expenses and can be deducted to reduce your taxable rental income.