When considering whether renting out your apartment is included in rental income expenses, it’s essential to understand the tax implications and financial responsibilities involved. Rental income is generally taxable and must be reported to the IRS, but certain expenses directly related to maintaining and managing the property, such as repairs, maintenance, property management fees, and mortgage interest, can be deducted to reduce your taxable income. However, personal use of the property or mixed-use scenarios may complicate deductions, as the IRS has specific rules for allocating expenses between rental and personal use. Consulting a tax professional or referring to IRS guidelines can help clarify how to accurately report rental income and eligible expenses, ensuring compliance and maximizing potential deductions.

| Characteristics | Values |

|---|---|

| Definition of Rental Income | Income earned from renting out property, including apartments. |

| Tax Treatment | Rental income is generally taxable and must be reported on tax returns. |

| Expenses Deductibility | Expenses directly related to renting the apartment are deductible. |

| Deductible Expenses Examples | Mortgage interest, property taxes, maintenance, repairs, utilities, etc. |

| Depreciation | A portion of the property's value can be deducted annually as depreciation. |

| Personal Use Limitations | If the apartment is used personally for >14 days/year, deductions are limited. |

| IRS Guidelines | Follow IRS Publication 527 for detailed rules on rental income and expenses. |

| Reporting Requirements | Report rental income on Schedule E (Form 1040) in the U.S. |

| Net Rental Income Calculation | Total rental income minus allowable expenses equals net rental income. |

| State-Specific Rules | Some states may have additional or different rules regarding rental income. |

| Record-Keeping | Maintain detailed records of income, expenses, and property-related documents. |

Explore related products

What You'll Learn

- Reporting Rental Income: Understand IRS rules for declaring rental income on tax returns accurately

- Deductible Expenses: Identify allowable costs like maintenance, repairs, and property management fees

- Depreciation Benefits: Learn how to claim depreciation on the apartment’s value over time

- Personal Use Rules: Determine tax implications if you use the apartment for personal stays

- Tax Credits Available: Explore potential credits for energy efficiency or low-income housing programs

![]()

Reporting Rental Income: Understand IRS rules for declaring rental income on tax returns accurately

When it comes to reporting rental income on your tax returns, understanding the IRS rules is crucial to ensure accuracy and compliance. The Internal Revenue Service (IRS) considers rental income as any payment you receive for the occupancy or use of your property, including residential spaces like apartments. If you're renting out your apartment, the rent you collect is generally taxable and must be reported on your federal tax return. This includes not only the monthly rent but also any additional fees or payments received, such as advance rent or security deposits (if they are not returned to the tenant).

The IRS requires taxpayers to report all rental income in the year it is received, regardless of whether it’s in cash, property, or services. For instance, if a tenant performs services like maintenance or repairs in lieu of rent, the fair market value of those services is considered taxable rental income. It’s important to keep detailed records of all transactions, including lease agreements, rent payments, and any other income-related documents. This documentation will be essential when filing your taxes and can help substantiate your income in case of an audit.

Expenses related to renting your apartment can be deducted from your rental income, reducing your taxable liability. The IRS allows deductions for ordinary and necessary expenses incurred in the management, conservation, and maintenance of your rental property. Common deductible expenses include property taxes, mortgage interest, insurance, repairs, maintenance, depreciation, and utilities (if paid by the landlord). However, it’s important to note that personal use of the property can complicate these deductions. If you use the apartment for personal purposes for more than 14 days or 10% of the total rental days (whichever is greater), special rules apply, and your deductions may be limited.

Reporting rental income and expenses is typically done on Schedule E (Form 1040). This form is used to report income and expenses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests. On Schedule E, you’ll list your total rental income and then subtract your deductible expenses to determine your net rental income or loss. If you have multiple rental properties, you’ll need to report each one separately. Additionally, if your rental activity is considered a business (e.g., you’re a real estate professional), you may also need to file Schedule C (Form 1040) to report income and expenses.

Lastly, it’s essential to be aware of state and local tax requirements, as they may differ from federal rules. Some states have their own forms and guidelines for reporting rental income, and certain localities may impose additional taxes. Consulting a tax professional or using tax software can help ensure that you’re meeting all applicable requirements and maximizing your deductions. By understanding and adhering to IRS rules, you can accurately report your rental income and avoid potential penalties or audits.

Renter's Insurance Deductible: What's the Annual Reset?

You may want to see also

Explore related products

![]()

Deductible Expenses: Identify allowable costs like maintenance, repairs, and property management fees

When renting out your apartment, it’s essential to understand which expenses are deductible to maximize your tax benefits. Deductible expenses are costs directly related to maintaining and managing the rental property, ensuring it remains habitable and generates income. These expenses reduce your taxable rental income, ultimately lowering your tax liability. The Internal Revenue Service (IRS) allows deductions for specific costs, provided they are ordinary, necessary, and directly tied to the rental activity. Identifying these allowable costs is the first step in accurately reporting your rental income and expenses.

Maintenance and Repairs are among the most common deductible expenses for rental property owners. Maintenance includes routine tasks like painting, cleaning, or replacing worn-out parts to keep the property in good condition. Repairs, on the other hand, address specific issues such as fixing a leaky roof, repairing broken appliances, or replacing damaged flooring. Both maintenance and repairs are fully deductible in the year they are incurred, as long as they are not considered improvements, which add value to the property or prolong its life. For example, fixing a broken window is a repair, while installing energy-efficient windows is an improvement and may need to be depreciated over time.

Property Management Fees are another allowable expense if you hire a property manager to handle tasks like tenant screening, rent collection, or property maintenance. These fees are fully deductible because they are directly related to managing the rental property. Similarly, advertising costs to attract tenants, such as online listings or newspaper ads, are also deductible. Additionally, insurance premiums for landlord or fire insurance policies that protect the rental property are eligible expenses. These costs are necessary to safeguard your investment and ensure the property remains rentable.

Utilities and Other Operational Costs may be deductible if you pay for them as part of the rental agreement. For instance, if you cover water, electricity, or internet services for your tenants, these expenses can be written off. However, if tenants pay their own utilities, these costs are not deductible. Property Taxes are another significant deductible expense, as they are directly tied to the ownership and operation of the rental property. These taxes are typically assessed by local governments and are fully deductible in the year they are paid.

Lastly, depreciation is a unique deductible expense that accounts for the wear and tear of the property over time. Unlike the other expenses mentioned, depreciation is a non-cash deduction that allows you to recover the cost of the building (not the land) over a specified period, typically 27.5 years for residential properties. This deduction is crucial because it acknowledges the property’s decreasing value due to age, use, and obsolescence. By including depreciation, you can further reduce your taxable rental income, even in years when other expenses are low. Understanding and properly documenting these deductible expenses ensures compliance with tax laws and optimizes your financial returns from renting your apartment.

Renting a Van for a Week: Tips, Costs, and Best Practices

You may want to see also

Explore related products

![]()

Depreciation Benefits: Learn how to claim depreciation on the apartment’s value over time

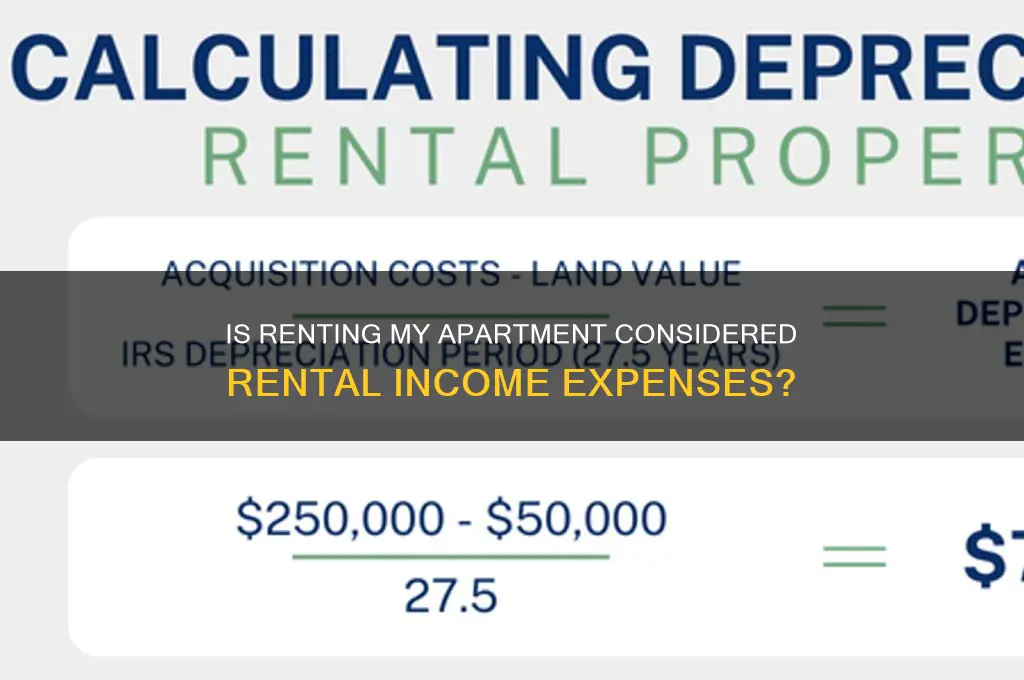

When renting out your apartment, understanding how to claim depreciation on its value over time can significantly reduce your taxable rental income. Depreciation is a tax deduction that allows you to recover the cost of the property’s wear and tear, obsolescence, and deterioration. It’s important to note that depreciation applies only to the building and its structural components, not the land, as land does not depreciate. To claim depreciation, you must first determine the property’s basis, which is typically its purchase price plus any settlement fees or closing costs. The IRS allows residential rental properties to be depreciated over 27.5 years using the straight-line depreciation method. This means you can deduct a portion of the building’s value each year, reducing your taxable rental income accordingly.

To begin claiming depreciation, you’ll need to separate the value of the land from the value of the building. This can be done through a property appraisal or by using the assessed values from your local tax authority. Once you have the building’s value, divide it by 27.5 to determine your annual depreciation deduction. For example, if the building is valued at $200,000, your annual depreciation expense would be $7,272 ($200,000 / 27.5). This amount is then deducted from your rental income, lowering the taxable amount. Keep in mind that depreciation is a paper loss, meaning it doesn’t involve a cash outlay but still reduces your tax liability.

It’s crucial to maintain accurate records when claiming depreciation. Document the property’s purchase price, any improvements made (which may be depreciated separately over 15 years), and the allocation of land versus building value. If you sell the property, the accumulated depreciation will be subject to depreciation recapture, taxed at a maximum rate of 25%. Proper record-keeping ensures compliance with IRS rules and helps maximize your tax benefits. Additionally, consider consulting a tax professional or using tax software to accurately calculate and report depreciation.

Another aspect to consider is the potential for bonus depreciation or Section 179 expensing, though these typically apply to personal property or improvements rather than the building itself. For instance, if you install new appliances or make significant upgrades, you may be able to deduct a portion of these costs immediately. However, the building’s structural components must still be depreciated over 27.5 years. Understanding these distinctions ensures you take full advantage of all available deductions.

Finally, if you’re new to rental property ownership, familiarize yourself with IRS Publication 527, *Residential Rental Property*, which provides detailed guidance on depreciation and other rental expenses. Claiming depreciation correctly not only reduces your current tax burden but also improves your property’s after-tax cash flow. By staying informed and organized, you can make the most of depreciation benefits while maintaining compliance with tax laws.

Is Alvarado, TX Safe for Motel Rentals? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Personal Use Rules: Determine tax implications if you use the apartment for personal stays

When determining the tax implications of using your rental apartment for personal stays, it's essential to understand the Personal Use Rules outlined by tax authorities, such as the IRS in the United States. These rules dictate how to allocate expenses and income when a property is used both for rental purposes and personal enjoyment. If you use the apartment for personal stays, it can impact the deductibility of rental expenses and the reporting of rental income. Generally, the more days you use the property for personal purposes, the more restrictions you'll face on claiming deductions.

The IRS defines personal use as any stay by the owner, their family, or friends, even if no rent is charged. If your personal use exceeds the greater of 14 days or 10% of the total days the property is rented at fair market value, the property is considered a vacation home for tax purposes. In this case, you must allocate expenses between rental and personal use. Rental income is reported in full, but deductions for rental expenses are limited to the amount of rental income received. For example, if you rent the apartment for $10,000 annually and use it personally for 30 days, your deductions cannot exceed $10,000, even if your actual expenses are higher.

To allocate expenses, calculate the ratio of rental days to total days of use. For instance, if the apartment is rented for 180 days and used personally for 45 days, 80% of expenses (180 / 225) can be deducted as rental expenses. The remaining 20% is considered personal and is not deductible. Expenses such as mortgage interest and property taxes may still be deductible on your personal taxes, but only if they exceed the standard deduction or are itemized. It's crucial to maintain detailed records of rental and personal use days, as well as all expenses, to accurately apply these rules.

If your personal use does not exceed the 14-day or 10% threshold, the property is treated as a rental property for tax purposes. In this scenario, you can generally deduct all legitimate rental expenses, such as maintenance, repairs, and depreciation, regardless of rental income. However, you must still report all rental income received. For example, if you rent the apartment for 120 days and use it personally for 10 days, you can deduct all eligible expenses as long as they are reasonable and necessary for the rental activity.

In summary, the Personal Use Rules require careful tracking of how you use your rental apartment. Exceeding the personal use limits triggers restrictions on expense deductions, while staying within the limits allows for more flexibility. To navigate these rules effectively, consult tax guidelines or a professional to ensure compliance and optimize your tax position. Proper planning and record-keeping are key to managing the tax implications of using your rental property for personal stays.

Renting the Perfect Space for Your Commercial Photo Shoots

You may want to see also

Explore related products

![]()

Tax Credits Available: Explore potential credits for energy efficiency or low-income housing programs

When renting out your apartment, it’s essential to understand that rental income is generally taxable, but you can offset this income with eligible expenses. Beyond deductions, exploring tax credits related to energy efficiency or low-income housing programs can further reduce your tax liability. These credits are not just deductions but direct reductions of the tax you owe, making them highly valuable. For instance, if you invest in energy-efficient upgrades like solar panels, insulation, or energy-efficient windows, you may qualify for the Nonbusiness Energy Property Credit or the Residential Clean Energy Credit, depending on the improvements. These credits can significantly lower your tax burden while making your rental property more attractive to tenants.

For landlords involved in low-income housing, the Low-Income Housing Tax Credit (LIHTC) is a powerful incentive. This federal program encourages the development and rehabilitation of affordable rental properties by offering credits to property owners who agree to rent units to low-income tenants at reduced rates. To qualify, your property must meet specific criteria, such as rent and income limits for tenants, and you must commit to maintaining affordability for a set period, typically 15 to 30 years. Working with a tax professional or housing agency can help ensure compliance and maximize this credit.

Another avenue to explore is the Energy Efficient Home Credit, which applies to builders and developers but can also benefit landlords who construct or substantially renovate rental units. This credit rewards energy-efficient construction that meets specific standards set by the IRS. While it may not directly apply to minor upgrades in existing properties, it’s worth considering if you’re planning significant renovations or new construction. Combining this credit with other energy-related incentives can amplify your tax savings.

Additionally, state-specific programs often complement federal credits. Many states offer their own energy efficiency or low-income housing credits, which can be claimed in addition to federal benefits. For example, California’s Multifamily Affordable Housing Solar Roofs Program provides incentives for installing solar panels on affordable housing units. Researching local programs through your state’s housing or energy department can uncover additional opportunities to reduce your tax liability.

Finally, documenting all eligible expenses and improvements is critical to claiming these credits. Keep detailed records of purchases, installation costs, and certifications proving compliance with energy efficiency or affordability standards. Working with a tax professional can ensure you’re taking full advantage of available credits while avoiding potential pitfalls. By strategically leveraging these programs, you can not only reduce your tax burden but also enhance the value and sustainability of your rental property.

Should You Rent Beach Chairs in Maui?

You may want to see also

Frequently asked questions

Yes, the rent you receive from your apartment is considered rental income and must be reported on your tax return.

Yes, you can deduct eligible expenses such as mortgage interest, property taxes, maintenance, and depreciation from your rental income to calculate your taxable profit.

No, only the portion of your apartment that is rented out is eligible for rental income and expense calculations. Personal use portions are not included.

Yes, if you pay utilities for the rented portion of your apartment, they can be deducted as rental expenses, provided they are directly related to the rental activity.

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)