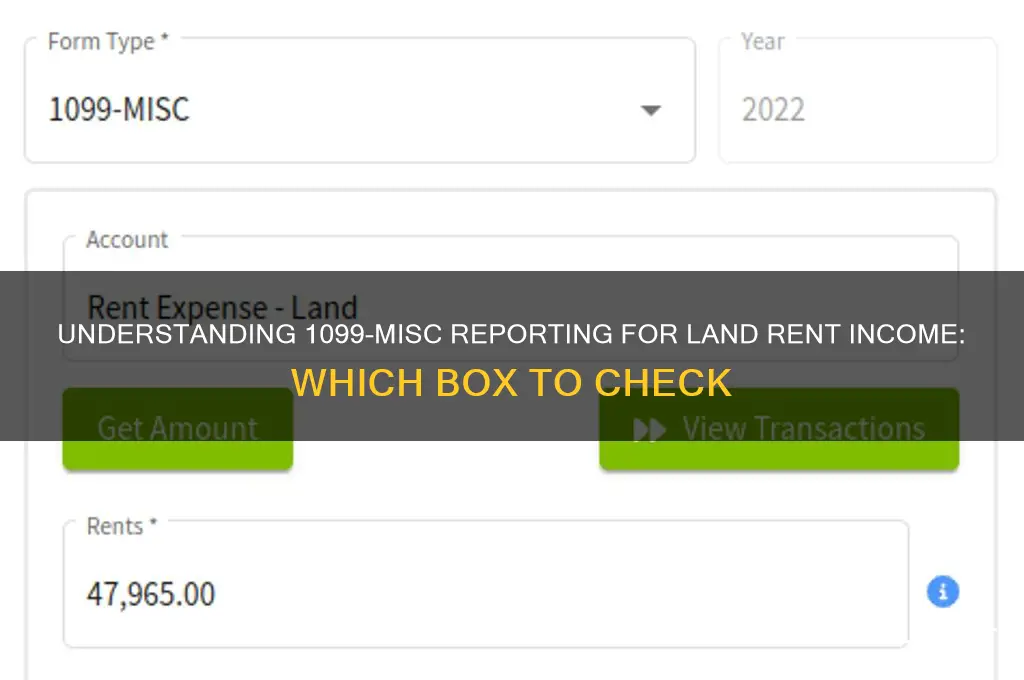

When filing a 1099-MISC form for land rent, it’s crucial to understand which box to check to ensure accurate reporting. For land rent payments, Box 1 (Rents) is typically used, as it specifically pertains to rental income, including payments made for the use of land or property. This box is designated for reporting income derived from real estate rentals, making it the appropriate choice for landowners or property managers who receive payments for leasing land. Properly identifying the correct box ensures compliance with IRS regulations and helps avoid potential penalties or audits related to misclassification of income.

| Characteristics | Values |

|---|---|

| Form Type | 1099-MISC |

| Box Number | Box 1 (Rents) |

| Purpose | Reporting income from land rent to the IRS |

| Threshold for Reporting | $600 or more paid to a single recipient in a tax year |

| Recipient Type | Individuals, partnerships, or LLCs (not corporations) |

| Filing Deadline | January 31 (to recipient) and February 28 (paper filing to IRS) or March 31 (e-filing) |

| Tax Implications for Recipient | Income is taxable and must be reported on Schedule E of Form 1040 |

| Tax Implications for Payer | May need to withhold taxes if backup withholding applies |

| Additional Requirements | Recipient’s TIN (Taxpayer Identification Number) must be collected via Form W-9 |

| Common Mistakes | Reporting in the wrong box (e.g., Box 7 for non-employee compensation) |

| Related Forms | Form 1096 (Transmittal of Information Returns) |

Explore related products

What You'll Learn

- Box 1: Rent Income - Report land rent payments made to landlords or property owners

- Box 2: Royalties - Not applicable for land rent; used for resource royalties

- Box 3: Other Income - Catch-all for payments not fitting other categories, rarely used for rent

- Box 4: Federal Income Tax Withheld - Report backup withholding if applicable to rent payments

- Box 7: Nonemployee Compensation - Not used for land rent; for independent contractor payments

![]()

Box 1: Rent Income - Report land rent payments made to landlords or property owners

Landowners and tenants alike often find themselves navigating the complexities of tax reporting, particularly when it comes to land rent payments. Box 1 of the 1099-MISC form is specifically designated for reporting rent income, a critical aspect for both parties involved in land leasing agreements. This box is not just a mere formality; it serves as a vital tool for the IRS to track rental income, ensuring compliance with tax laws and helping to prevent underreporting.

From an analytical perspective, the inclusion of land rent in Box 1 highlights the IRS's recognition of the diverse nature of rental income. Unlike traditional property rentals, land leasing can encompass various scenarios, such as agricultural land, commercial plots, or even vacant lots. Each of these arrangements may have unique financial implications, but they all converge in Box 1, underscoring the importance of accurate reporting. For instance, a farmer leasing land for crop cultivation must report the rent paid, just as a business leasing land for a parking lot would. This standardization simplifies the process for taxpayers while providing the IRS with a comprehensive view of rental income across different sectors.

For those tasked with filing, understanding what constitutes reportable rent income is crucial. The IRS defines this as any payment made for the use of land, regardless of the purpose. This includes not only fixed rent but also any additional payments tied to the land's use, such as percentage rent based on crop yields or sales. It’s essential to differentiate these payments from other types of income, such as service fees or property improvements, which may fall under different reporting categories. For example, if a tenant pays for both land rent and irrigation services, only the rent portion should be reported in Box 1.

A practical tip for landlords and tenants is to maintain detailed records of all transactions related to land leasing. This includes lease agreements, payment receipts, and any correspondence regarding rent adjustments. Clear documentation not only facilitates accurate reporting but also serves as a safeguard in case of an audit. For instance, if a tenant claims a deduction for rent expenses, the landlord’s corresponding report in Box 1 should align with these records to avoid discrepancies.

In conclusion, Box 1 of the 1099-MISC form plays a pivotal role in the tax reporting process for land rent payments. Its focus on rent income ensures that both landlords and tenants fulfill their tax obligations while providing the IRS with a clear picture of rental activities. By understanding the specifics of what to report and maintaining thorough records, taxpayers can navigate this aspect of tax compliance with confidence and precision.

Legally Renting Your Stationary Travel Trailer: A Comprehensive Guide

You may want to see also

Explore related products

![Landlords' Duties and Tenants' Rights: in Texas [Second Edition]](https://m.media-amazon.com/images/I/71dNNcNXjwL._AC_UY218_.jpg)

![]()

Box 2: Royalties - Not applicable for land rent; used for resource royalties

Landowners often wonder which box to check on a 1099-MISC form when reporting income from land rent. Box 2, labeled "Royalties," is a common point of confusion. While it might seem related to land use, this box is specifically designated for resource royalties, such as payments for oil, gas, or mineral extraction. Land rent, however, falls under a different category entirely, making Box 2 inapplicable for this type of income.

To clarify, resource royalties refer to payments made for the right to extract or use natural resources from a property. For instance, if a mining company pays a landowner for the rights to extract coal from their land, that payment would be reported in Box 2. The IRS defines royalties as income from the use of property, but this definition is narrowly applied to natural resources. Land rent, which is compensation for the use of land itself (e.g., farming, leasing for events, or parking), does not qualify as a royalty under tax law.

A practical example illustrates the distinction: Imagine a farmer renting 50 acres of land for $5,000 annually. This payment is land rent, not a royalty, and should not be reported in Box 2. Conversely, if the same landowner receives $2,000 for allowing a gas company to drill on their property, that $2,000 would be reported in Box 2 as a royalty. The key difference lies in the nature of the payment—whether it’s for the land’s use or for the extraction of resources.

When preparing a 1099-MISC for land rent, avoid the mistake of checking Box 2. Instead, report the income in Box 1 ("Rents"), which is specifically designated for payments related to the use of real estate. Misclassifying land rent as royalties can lead to confusion for the recipient and potential scrutiny from the IRS. Always double-check the form instructions or consult a tax professional to ensure accuracy, especially when dealing with multiple income streams from the same property.

In summary, while Box 2 on the 1099-MISC form serves an important purpose for reporting resource royalties, it has no place in land rent transactions. Understanding this distinction not only ensures compliance with IRS regulations but also simplifies the tax reporting process for both payers and recipients. Keep the categories clear: Box 2 for resource royalties, Box 1 for land rent.

Exploring the Minimum Age Requirements for Renting with Turo

You may want to see also

Explore related products

![]()

Box 3: Other Income - Catch-all for payments not fitting other categories, rarely used for rent

Landowners often grapple with which box to check on a 1099-MISC form when reporting rental income, particularly for land rent. While Box 1 (Rents) seems like the obvious choice, some filers mistakenly turn to Box 3 (Other Income) as a catch-all for payments that don’t neatly fit elsewhere. This box is rarely appropriate for rent, yet its misuse persists due to confusion or a lack of clarity in IRS guidelines. Understanding when—and more importantly, when not—to use Box 3 is critical to avoid errors that could trigger audits or penalties.

Box 3 is designed as a residual category for income that doesn’t fall under the other nine boxes on the 1099-MISC form. Examples include prizes, awards, or payments not covered by specific categories like rents, royalties, or nonemployee compensation. For instance, if a landowner receives payment for granting temporary access to their land for a film shoot, this might qualify as "Other Income" if it’s not a traditional rental arrangement. However, standard land rent—whether for agricultural, residential, or commercial use—clearly belongs in Box 1, not Box 3. Misclassifying rent here could lead to confusion for the recipient and potential scrutiny from the IRS.

The temptation to use Box 3 often arises from its broad label, but this approach undermines the form’s purpose. Each box serves a distinct function, ensuring the IRS can accurately categorize income for tax purposes. For example, income reported in Box 1 is subject to specific tax treatments, such as potential deductions for property expenses, which wouldn’t apply to "Other Income." By misusing Box 3, filers risk depriving recipients of these benefits or exposing them to unnecessary tax liabilities. Always verify the nature of the payment against IRS definitions before defaulting to this catch-all category.

Practical tip: If you’re unsure whether a payment qualifies as rent or falls into another category, consult IRS Publication 527 (Residential Rental Property) or seek guidance from a tax professional. For land rent, the key criterion is whether the payment is for the use of the property. If so, Box 1 is the correct choice. Reserve Box 3 for truly unique or non-standard income scenarios, ensuring compliance and clarity for both the payer and recipient.

Renting a Scooter at Disney World: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Box 4: Federal Income Tax Withheld - Report backup withholding if applicable to rent payments

Backup withholding is a critical yet often overlooked aspect of reporting land rent payments on a 1099-MISC form. Box 4, labeled "Federal Income Tax Withheld," is specifically designated for reporting backup withholding, which applies when the payee has failed to provide a correct taxpayer identification number (TIN) or has been notified by the IRS to withhold tax at a flat rate. This mechanism ensures compliance with tax regulations and prevents underreporting of income. For landlords or property managers, understanding when and how to use Box 4 is essential to avoid penalties and maintain accurate financial records.

To determine if backup withholding applies, start by verifying the payee’s TIN. If the TIN is missing, incorrect, or the payee has been notified by the IRS to be subject to backup withholding, you are required to withhold 24% of the payment and report this amount in Box 4. This rate is consistent across all applicable transactions and is not subject to adjustment based on the payee’s income level or tax bracket. Failure to comply with backup withholding rules can result in fines, making it imperative to stay informed and diligent in your reporting.

Practical implementation involves a few key steps. First, ensure you have a completed Form W-9 from the payee, which provides their TIN and certifies its accuracy. If discrepancies arise, promptly request clarification or an updated form. Second, monitor IRS notifications regarding backup withholding requirements for specific payees. Third, integrate backup withholding calculations into your payment process, ensuring the 24% is deducted before issuing the payment. Finally, accurately report the withheld amount in Box 4 of the 1099-MISC form and provide a copy to both the payee and the IRS by the annual filing deadline, typically January 31st.

A common misconception is that backup withholding only applies to large transactions or high-income individuals. In reality, it is triggered by TIN-related issues or IRS notifications, regardless of the payment amount. For example, if a landowner rents a small plot for $500 annually and fails to provide a valid TIN, the payer must withhold $120 (24% of $500) and report it in Box 4. This underscores the importance of meticulous record-keeping and proactive communication with payees to avoid unintended withholding scenarios.

In conclusion, Box 4 of the 1099-MISC form serves as a safeguard against tax evasion and ensures compliance with federal regulations. By understanding the triggers for backup withholding, implementing systematic checks, and adhering to reporting deadlines, landlords and property managers can navigate this requirement effectively. While it may seem complex, treating Box 4 as a routine part of financial management minimizes risks and fosters transparency in land rent transactions.

Surviving San Francisco: Strategies for Affording Sky-High Rents

You may want to see also

Explore related products

![]()

Box 7: Nonemployee Compensation - Not used for land rent; for independent contractor payments

Landowners often grapple with which box to check on a 1099-MISC form when reporting rental income, particularly for land rent. Box 7, labeled "Nonemployee Compensation," is a common point of confusion. Despite its name, this box is not for reporting land rent payments. Instead, it is exclusively reserved for payments made to independent contractors for services rendered. Understanding this distinction is crucial to avoid misreporting and potential IRS penalties.

From a practical standpoint, Box 7 is used when a payer hires an individual or business to perform a service and that entity is not an employee. For example, if a farmer hires a freelance agronomist to consult on crop rotation, the payment would be reported in Box 7. However, if the same farmer pays a landowner for the use of their field, that payment is considered rent, not nonemployee compensation. Rent payments belong in Box 1 (Rents) of the 1099-MISC form, not Box 7. This clear separation ensures compliance with IRS regulations and prevents confusion during tax season.

A common mistake occurs when payers assume that any payment to a non-employee falls under Box 7. This misconception often stems from the term "nonemployee compensation," which sounds broadly applicable. However, the IRS defines this category narrowly: it applies only to payments for services, not for the use of property. For instance, if a construction company pays a landowner for the right to store equipment on their land, that is rent, not compensation for services. Misclassifying such payments in Box 7 can lead to audits or fines, as the IRS scrutinizes this box for potential underreporting of contractor income.

To avoid errors, follow these steps: first, determine whether the payment is for a service or for the use of property. If it’s the latter, use Box 1. Second, ensure the recipient’s taxpayer identification number (TIN) is accurate, as incorrect TINs can trigger IRS notices. Finally, double-check the payment threshold—Box 7 requires reporting only if payments exceed $600 in a tax year, while Box 1 has no minimum threshold. By adhering to these guidelines, payers can accurately report land rent and contractor payments without conflating the two.

In summary, while Box 7 on the 1099-MISC form is essential for reporting independent contractor payments, it has no place in land rent transactions. Rent payments belong in Box 1, a distinction that simplifies tax reporting and reduces the risk of IRS scrutiny. By understanding this difference and following the outlined steps, landowners and businesses can ensure compliance and avoid costly mistakes.

Transform Your Rento Game: Mastering the 2D to 3D Transition

You may want to see also

Frequently asked questions

For land rent payments, check Box 1 (Rents) on the 1099-MISC form.

Yes, land rent is generally considered taxable income for the recipient and must be reported on their tax return.

No, a 1099-MISC is only required if the total payments for land rent exceed $600 in a calendar year.

No, land rent payments should be reported on a 1099-MISC (Box 1), not a 1099-NEC, which is used for non-employee compensation.