A good rent-to-income ratio is a critical financial metric used to determine how much of a tenant’s income should ideally be allocated to rent, ensuring affordability and financial stability. Generally, experts recommend that rent should not exceed 30% of a person’s gross monthly income, a guideline established by the U.S. Department of Housing and Urban Development (HUD). This ratio helps renters avoid financial strain by leaving enough income for other essential expenses like utilities, groceries, and savings. For landlords and property managers, understanding this ratio is equally important, as it aids in assessing a tenant’s ability to pay rent consistently. However, individual circumstances, such as high debt or fluctuating income, may necessitate adjusting this ratio to better suit personal financial realities.

| Characteristics | Values |

|---|---|

| Ideal Rent-to-Income Ratio | 30% or less of gross monthly income |

| Acceptable Range | 25% - 30% of gross monthly income |

| Maximum Recommended | 30% of gross monthly income (beyond this may strain finances) |

| Common Rule of Thumb | "Spend no more than 1/3 of your income on rent" |

| Affordability Benchmark | If rent exceeds 30%, it’s considered a cost burden by HUD (U.S. Department of Housing and Urban Development) |

| Gross Income Calculation | Total monthly income before taxes and deductions |

| Net Income Consideration | Some advise using net income, but gross income is more commonly used for this ratio |

| Regional Variations | Ratios may vary by city or country due to cost of living differences |

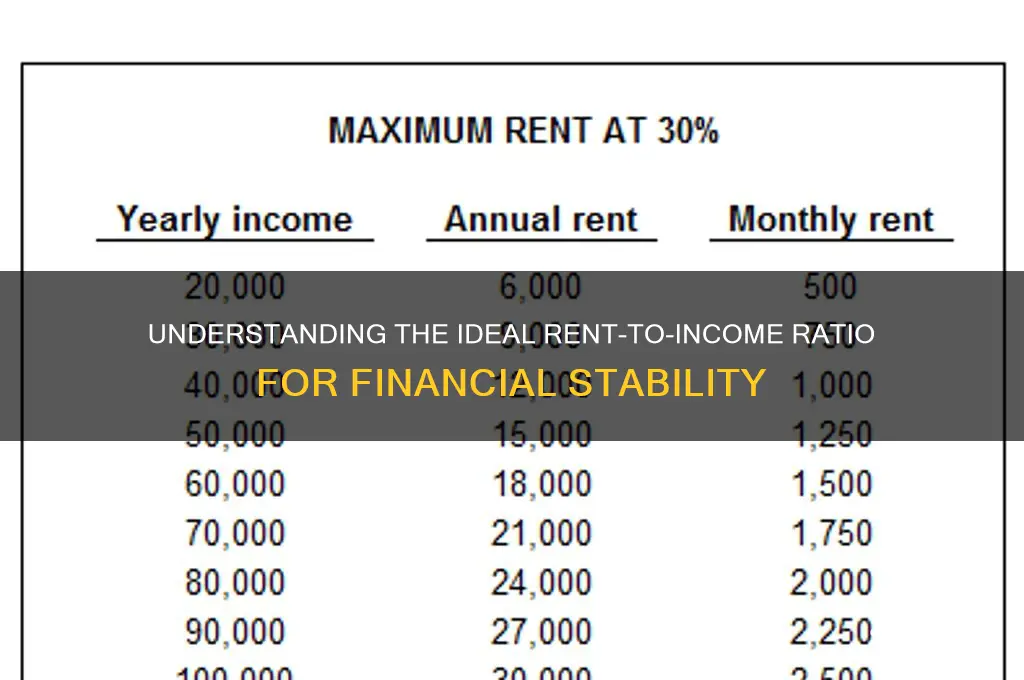

| Example Calculation | Monthly income of $5,000 → Ideal rent ≤ $1,500 (30% of $5,000) |

| Importance | Ensures financial stability and ability to cover other expenses |

Explore related products

What You'll Learn

- Ideal Ratio Range: 30% or less of gross income is widely recommended for affordability

- Local Market Variations: Ratios may shift based on city or region housing costs

- Budgeting Considerations: Includes utilities, groceries, and savings after rent payment

- Landlord Requirements: Many landlords demand 3x rent in monthly income

- Adjusting for Debt: High debt-to-income ratios may necessitate lower rent spending

![]()

Ideal Ratio Range: 30% or less of gross income is widely recommended for affordability

A widely accepted benchmark in personal finance suggests that rent should consume 30% or less of your gross monthly income. This rule of thumb, often referred to as the 30% rule, originated from federal housing programs in the 1960s and has since become a standard measure of housing affordability. For example, if your monthly gross income is $5,000, your rent should ideally not exceed $1,500. This guideline helps individuals avoid financial strain by ensuring that a significant portion of their income remains available for other essential expenses, savings, and discretionary spending.

However, the 30% rule isn’t one-size-fits-all. Its practicality varies based on factors like location, income level, and lifestyle. In high-cost-of-living cities like New York or San Francisco, adhering to this ratio can be nearly impossible for many residents. For instance, a household earning $60,000 annually (roughly $5,000 monthly) might struggle to find rent under $1,500 in these markets, where average rents often surpass $2,500. In such cases, experts suggest adjusting the ratio to a more realistic 40–50% of income, but only if accompanied by strict budgeting in other areas.

To apply this rule effectively, start by calculating your gross monthly income and multiplying it by 0.3. Compare the result to your current or prospective rent. If the rent exceeds this threshold, consider negotiating with landlords, seeking roommates, or exploring less expensive neighborhoods. For instance, a single professional earning $4,000 monthly should aim for rent around $1,200 or less. If their desired apartment costs $1,600, they might propose a rent concession or look for a place with lower utilities included.

Critics argue that the 30% rule oversimplifies financial planning, ignoring individual circumstances like debt, childcare costs, or medical expenses. For low-income households, even 30% may be unsustainable. A family earning $2,500 monthly, for example, would be limited to $750 in rent, which could be unattainable in many areas. In such scenarios, seeking subsidized housing or government assistance programs may be necessary. Conversely, high-income earners might comfortably allocate more than 30% to rent if their savings and investments are robust.

Ultimately, the 30% rule serves as a starting point, not a rigid mandate. Its value lies in encouraging renters to prioritize financial stability by aligning housing costs with income. By staying within this range, individuals can build savings, manage debt, and avoid the stress of living paycheck to paycheck. For those unable to meet the 30% threshold, the key is to compensate by reducing expenses in other areas or increasing income through side hustles or career advancement.

Renting a Pavilion in Cook Forest: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Local Market Variations: Ratios may shift based on city or region housing costs

Rent-to-income ratios aren’t one-size-fits-all. A 30% threshold, often cited as ideal, crumbles under the weight of local market realities. In San Francisco, where median rents hover near $4,000, even dual-income households earning well above the national average might struggle to meet this benchmark. Conversely, in Tulsa, Oklahoma, where median rents sit around $900, a 30% ratio leaves ample room for savings and discretionary spending. This disparity underscores a critical truth: geographic location dictates what constitutes a "good" ratio far more than blanket financial advice.

Consider the mechanics of supply and demand. Coastal cities with booming tech industries and limited housing stock see rents skyrocket, forcing residents to allocate larger portions of their income to shelter. In contrast, Rust Belt cities with shrinking populations and surplus housing stock offer affordability that allows for lower ratios. For instance, a Cleveland resident earning $50,000 annually might comfortably spend 25% on rent ($1,042 monthly), while a Seattleite earning the same would need to stretch to 40% ($1,667 monthly) just to secure a modest apartment. These examples illustrate how local economies distort traditional financial guidelines.

To navigate these variations, renters must adopt a hyper-local lens. Start by researching the median rent in your target neighborhood, not just the city average, as prices can fluctuate dramatically within a few miles. Next, compare this figure to your gross monthly income, aiming for a ratio that aligns with local norms rather than national standards. For instance, in New York City, a 40% ratio might be considered manageable, while in Austin, Texas, anything above 30% could signal financial strain. Tools like Zillow’s rent index or local housing authority reports can provide granular data to inform your calculations.

However, relying solely on ratios can be misleading. Factor in additional costs unique to your region, such as parking fees in dense urban centers or higher utility bills in areas with extreme weather. For example, a Los Angeles renter might save on heating costs but face steep parking expenses, while a Minneapolis tenant might incur higher winter heating bills. Adjust your budget accordingly, ensuring your ratio accounts for these regional nuances.

Ultimately, a "good" rent-to-income ratio is one that sustains your financial health within the context of your local market. It’s not about hitting a magic number but about balancing housing costs with other expenses, savings goals, and lifestyle priorities. In high-cost cities, this might mean accepting a higher ratio temporarily while pursuing career growth or exploring shared housing options. In more affordable regions, it could mean leveraging a lower ratio to accelerate debt repayment or investment goals. The key is adaptability—tailoring your approach to the economic pulse of your specific location.

Kindly Requesting Rent: A Guide to Polite and Effective Communication

You may want to see also

Explore related products

![]()

Budgeting Considerations: Includes utilities, groceries, and savings after rent payment

A commonly recommended rent-to-income ratio is 30% or less, meaning no more than 30% of your gross monthly income should go toward rent. However, this is just the starting point. Once rent is paid, the remaining budget must stretch to cover utilities, groceries, savings, and other essentials. Failing to account for these post-rent expenses can lead to financial strain, even if your rent falls within the "ideal" ratio.

Consider utilities first. On average, utilities (electricity, water, gas, internet, and trash) can consume 5–10% of your monthly income. For a household earning $4,000 monthly, this translates to $200–$400. Groceries are another significant expense, typically ranging from 10–15% of income, or $400–$600 for the same household. Together, these two categories can easily total $600–$1,000, leaving less room for savings or discretionary spending if not planned carefully.

Savings should not be an afterthought. Financial experts recommend setting aside at least 20% of your income for savings and debt repayment. For our $4,000-earning household, this means $800 should ideally go toward emergency funds, retirement, or paying down debt. If rent consumes 30% ($1,200) and utilities and groceries take another $600–$1,000, the remaining $1,000–$1,200 must cover transportation, insurance, entertainment, and savings. This tight margin highlights why a 30% rent-to-income ratio, while advisable, requires meticulous budgeting to avoid overspending.

To manage these expenses effectively, prioritize tracking your spending in each category. Use budgeting apps or spreadsheets to monitor utilities and groceries, aiming to stay within the 5–10% and 10–15% ranges, respectively. Automate savings by setting up direct deposits into a separate account, ensuring the 20% goal is met before discretionary spending. Finally, consider reducing costs where possible—switching to energy-efficient appliances, meal planning to cut grocery bills, or negotiating lower utility rates can free up additional funds for savings or unexpected expenses.

In conclusion, a good rent-to-income ratio is only the beginning of financial stability. Post-rent budgeting demands a detailed approach to utilities, groceries, and savings, ensuring these essential expenses don’t derail your financial goals. By allocating specific percentages to each category and adopting cost-saving strategies, you can maintain a balanced budget even with a seemingly "ideal" rent burden.

Fridge Scratches: What Renters Need to Know

You may want to see also

Explore related products

$35.71 $49.99

![]()

Landlord Requirements: Many landlords demand 3x rent in monthly income

A common rule of thumb in the rental market is the 3x rent-to-income ratio, a benchmark many landlords use to assess a tenant's ability to pay. This means that a tenant's monthly income should be at least three times the rent amount. For instance, if a landlord is advertising a $1,500 apartment, they would typically seek tenants earning a minimum of $4,500 per month. This requirement is a quick and widely accepted method for landlords to mitigate the risk of rental defaults.

The Logic Behind the 3x Rule

Landlords adopt the 3x rent-to-income ratio to ensure tenants can comfortably afford rent while covering other living expenses. It’s a buffer against financial strain, as it assumes that only one-third of a tenant’s income goes toward housing. This leaves room for utilities, groceries, transportation, and unexpected costs. For example, a tenant earning $4,500 monthly and paying $1,500 in rent has $3,000 remaining for other necessities, reducing the likelihood of missed payments.

Practical Tips for Tenants

If your income doesn’t meet the 3x threshold, there are strategies to improve your chances of approval. First, consider a co-signer with a stable income who can guarantee the lease. Alternatively, offer to pay a larger security deposit or multiple months’ rent upfront to demonstrate financial commitment. Some landlords may also accept proof of additional income sources, such as investments or side hustles, to supplement your primary earnings.

Cautions for Landlords

While the 3x rule is a useful starting point, it’s not foolproof. Relying solely on this ratio can exclude qualified tenants with non-traditional income streams or high savings. For instance, a retiree with substantial savings but a modest monthly pension might not meet the 3x requirement despite being a low-risk tenant. Landlords should consider a holistic approach, evaluating credit scores, rental history, and overall financial stability alongside income ratios.

The 3x rent-to-income ratio serves as a practical tool for landlords to gauge tenant affordability, but it shouldn’t be the sole criterion. Tenants can enhance their applications through co-signers or upfront payments, while landlords benefit from a more nuanced evaluation process. Balancing this rule with other financial indicators ensures a fair and effective rental agreement for both parties.

Renting a Bugatti: Where to Find This Luxury Supercar

You may want to see also

![]()

Adjusting for Debt: High debt-to-income ratios may necessitate lower rent spending

High debt-to-income ratios can significantly impact your ability to manage rent payments comfortably. A commonly recommended rent-to-income ratio is 30% or less, but this assumes a relatively low debt burden. For individuals with substantial debt obligations—student loans, car payments, credit card balances—this threshold may need adjustment. Financial experts suggest that if your debt-to-income ratio exceeds 36%, your rent should ideally fall below 25% of your income to maintain financial stability. This ensures that your combined debt and housing expenses don’t overwhelm your budget.

Consider a practical example: a young professional earning $50,000 annually with monthly student loan payments of $500 and a car loan of $300. Their total monthly debt payments amount to $800, or 19.2% of their gross monthly income ($4,166). If they adhere to the 30% rent-to-income rule, they’d allocate $1,250 to rent. However, this leaves only $2,116 for other essentials like groceries, utilities, and savings. To avoid financial strain, reducing rent to 20% of income ($833) would provide a more sustainable balance, freeing up $417 for other expenses or debt repayment.

Adjusting rent based on debt isn’t just about immediate affordability—it’s a long-term strategy. High rent payments coupled with significant debt can hinder progress toward financial goals, such as building an emergency fund or saving for a home. For instance, someone with a 40% debt-to-income ratio might aim for a rent-to-income ratio of 20–22%, allowing them to allocate more resources toward debt reduction. Over time, as debt decreases, they can reassess and potentially increase their housing budget without compromising financial health.

To implement this adjustment, start by calculating your debt-to-income ratio (monthly debt payments divided by gross monthly income). If it exceeds 36%, consider reducing your target rent-to-income ratio to 25% or less. Use budgeting tools to model different scenarios, ensuring that rent, debt, and other expenses align with your income. Additionally, prioritize high-interest debt repayment to lower your overall financial burden, which can indirectly improve your ability to manage rent. By tailoring your rent spending to your debt obligations, you create a more resilient financial foundation.

Where Rent Expenses Belong on Your Balance Sheet: A Guide

You may want to see also

Frequently asked questions

A good rent-to-income ratio is generally considered to be 30% or less of your gross monthly income. This means that your monthly rent should not exceed 30% of what you earn before taxes.

The 30% rule helps ensure that you have enough income left over for other essential expenses like utilities, groceries, transportation, and savings. It promotes financial stability and reduces the risk of being "house poor."

While having no debt may provide more flexibility, it’s still risky to exceed the 30% threshold. Unexpected expenses or financial changes could strain your budget. It’s best to stick to the 30% rule or slightly above only if you have a robust emergency fund and stable income.

If your rent exceeds 30% of your income, consider finding a more affordable place, increasing your income through a raise or side job, or sharing living expenses with a roommate. Prioritize reducing housing costs to avoid financial stress.