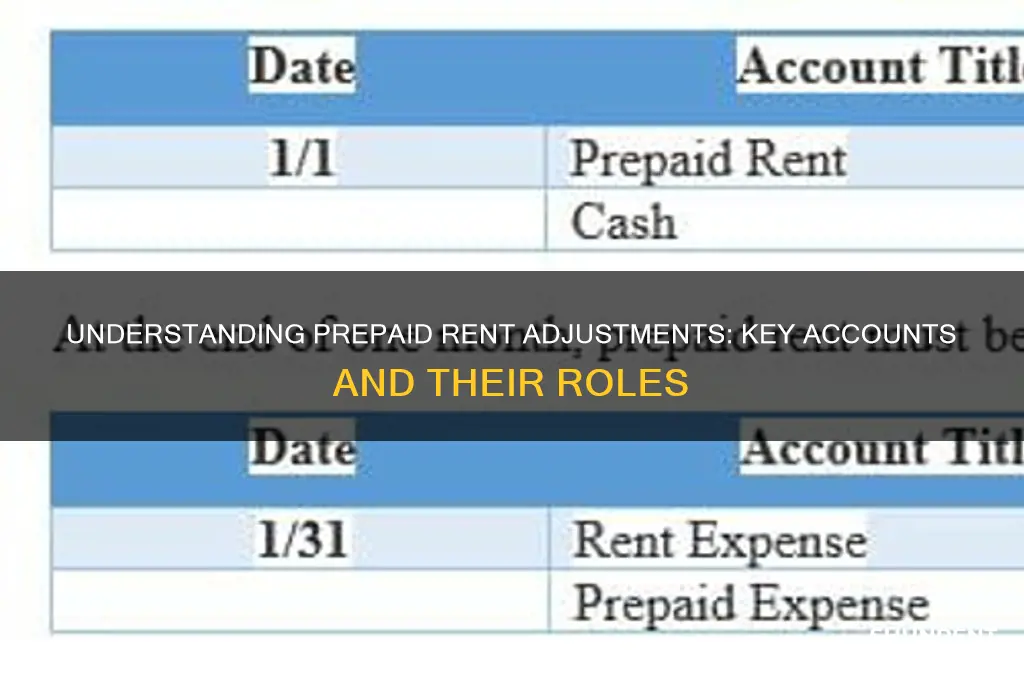

Prepaid rent adjustments are essential in accounting to accurately reflect the portion of rent paid in advance that pertains to future accounting periods. Typically, these adjustments involve two primary accounts: the Prepaid Rent account, which is an asset account, and the Rent Expense account, which is an expense account. When rent is paid in advance, it is initially recorded as a debit to Prepaid Rent and a credit to Cash. As the rental period progresses, the portion of prepaid rent that applies to the current period is recognized as an expense by debiting Rent Expense and crediting Prepaid Rent. This process ensures that expenses are matched to the appropriate accounting period, adhering to the accrual accounting principle and providing a more accurate representation of a company’s financial position.

| Characteristics | Values |

|---|---|

| Account Type | Asset Account |

| Account Name | Prepaid Rent or Prepaid Expenses |

| Nature | Current Asset |

| Purpose | To record rent payments made in advance for future periods |

| Adjustment Entry | Debit Prepaid Rent, Credit Cash (at payment) |

| Amortization Entry | Debit Rent Expense, Credit Prepaid Rent (monthly/periodic) |

| Reporting | Balance Sheet (under Current Assets) |

| Tax Treatment | Expensed over the rental period, not fully deductible in the payment year |

| Common Use | Businesses with long-term lease agreements |

| Contra Account | None (Prepaid Rent is a standalone account) |

| Reversing Entry | Optional, to simplify subsequent period adjustments |

| Financial Impact | Reduces Cash initially, then increases Rent Expense over time |

| Audit Focus | Proper allocation of expenses to the correct periods |

Explore related products

$9.99

What You'll Learn

![]()

Journal Entry for Prepaid Rent

Prepaid rent represents a unique accounting challenge, requiring careful journal entries to reflect the timing of expenses accurately. When a business pays rent in advance, it must recognize the expense over the period it benefits from the rental, not all at once. This necessitates a journal entry that initially records the prepaid rent as an asset and then systematically allocates it to expense as time passes.

Here’s a step-by-step breakdown of the journal entry process:

Initial Payment: When rent is paid in advance, debit the "Prepaid Rent" account (an asset) and credit the "Cash" account. For example, if a company pays $12,000 for six months of rent, the entry would be:

- Debit: Prepaid Rent $12,000

- Credit: Cash $12,000

Monthly Adjustment: Each month, a portion of the prepaid rent is recognized as an expense. Debit the "Rent Expense" account (an expense) and credit the "Prepaid Rent" account. For the above example, the monthly entry would be:

- Debit: Rent Expense $2,000

- Credit: Prepaid Rent $2,000

This method ensures the expense is matched to the period it benefits, aligning with the accrual accounting principle.

While the process seems straightforward, errors can occur if the timing or amount of the adjustment is miscalculated. For instance, failing to adjust prepaid rent monthly could distort financial statements, overstating assets and understating expenses. To avoid this, businesses should establish a consistent schedule for adjustments, ideally tied to their accounting period. Additionally, reconciling the prepaid rent account regularly can help identify discrepancies early.

The journal entry for prepaid rent adjustment serves as a critical tool for maintaining accurate financial records. By properly recording the initial payment and subsequent adjustments, businesses ensure compliance with accounting standards and provide a clear picture of their financial health. This practice not only enhances transparency but also aids in better decision-making by reflecting true expenses over time. For small businesses or those new to accounting, leveraging accounting software can automate these entries, reducing the risk of errors and saving time.

Tarrytown, NY: Can You Rent Apartments on Martling Ave?

You may want to see also

Explore related products

![]()

Adjusting Entry at Year-End

At year-end, businesses must ensure their financial statements accurately reflect expenses incurred, even if cash transactions occurred in a different period. Prepaid rent, a common example, requires an adjusting entry to allocate the expense to the correct accounting period. This entry debits Rent Expense, recognizing the portion of rent consumed during the year, and credits Prepaid Rent, reducing the asset account by the same amount. For instance, if a company pays $12,000 annually for rent in December but only $1,000 pertains to that month, the adjusting entry would debit Rent Expense for $1,000 and credit Prepaid Rent for $1,000, ensuring the expense is matched to the period it benefits.

The process begins by determining the prepaid rent balance and calculating the portion applicable to the current year. This involves reviewing the lease agreement and rent payment schedule. For example, if a $6,000 biannual payment was made in July for six months, $3,000 would be expensed by year-end. The adjusting entry would debit Rent Expense for $3,000 and credit Prepaid Rent for $3,000. Failure to make this adjustment would overstate assets and understate expenses, distorting financial performance.

A critical caution is avoiding confusion between prepaid rent and accrued rent. Prepaid rent is an asset recorded when rent is paid in advance, while accrued rent is a liability recorded when rent is owed but unpaid. Adjusting entries for prepaid rent focus on expense recognition, whereas accrued rent entries involve recording unpaid obligations. Misclassifying these accounts can lead to material misstatements in financial statements. Always verify the timing of payments and lease terms to ensure accuracy.

In practice, automating this process through accounting software can reduce errors. Most systems allow for recurring adjusting entries based on predefined schedules. For small businesses, a manual checklist can serve as a reminder to review prepaid rent balances at year-end. Additionally, reconciling prepaid rent accounts monthly helps identify discrepancies early. By adhering to these practices, businesses maintain compliance with accrual accounting principles and provide stakeholders with reliable financial information.

Renting a Condo Remotely: A Step-by-Step Guide for Out-of-Towners

You may want to see also

Explore related products

![]()

Impact on Financial Statements

Prepaid rent adjustments directly influence the accuracy of a company’s financial statements by ensuring expenses are recognized in the correct accounting period. When rent is paid in advance, it initially hits the balance sheet as a prepaid asset, not an expense. Over time, as the rental period elapses, this prepaid asset is gradually expensed, reducing its balance while increasing the rent expense on the income statement. This process, known as amortization, aligns with the matching principle, which requires expenses to be recognized when they contribute to revenue generation. Without proper adjustment, financial statements would overstate assets and understate expenses in the short term, distorting profitability and liquidity metrics.

Consider a company that pays $12,000 annually for rent in January but operates on a monthly basis. Initially, the entire $12,000 is recorded as a prepaid asset. Each month, $1,000 is moved from the prepaid rent account to the rent expense account. This adjustment ensures the income statement reflects $1,000 of rent expense monthly, accurately representing the cost of using the rented space. Simultaneously, the prepaid rent account on the balance sheet decreases by $1,000 each month, reflecting the consumption of the prepaid resource. This systematic approach maintains the integrity of both the income statement and the balance sheet.

The impact of prepaid rent adjustments extends beyond the income statement and balance sheet to influence key financial ratios. For instance, the current ratio, which measures liquidity, includes prepaid rent as part of current assets. If prepaid rent is not adjusted properly, the current ratio may appear artificially inflated, misleading stakeholders about the company’s short-term financial health. Similarly, the operating expense ratio, which compares operating expenses to revenue, could be understated if prepaid rent is not expensed correctly. Accurate adjustments are therefore critical for reliable financial analysis and decision-making.

To ensure proper handling of prepaid rent adjustments, companies should implement robust accounting procedures. First, clearly document the terms of lease agreements, including payment schedules and rental periods. Second, establish a consistent amortization schedule to systematically allocate prepaid rent over time. Third, reconcile prepaid rent accounts regularly to identify and correct discrepancies. For example, if a company pays $6,000 for six months of rent in advance, it should verify that $1,000 is expensed each month. Automation tools can streamline this process, reducing the risk of errors. By adhering to these practices, businesses can maintain accurate financial statements that reflect their true financial position and performance.

Finally, the treatment of prepaid rent adjustments can vary depending on accounting standards, such as GAAP or IFRS, and industry-specific practices. For instance, under GAAP, prepaid rent is typically classified as a current asset if it will be fully expensed within one year. In contrast, IFRS may allow for different classifications based on the lease term. Companies operating internationally or in specialized industries must stay informed about applicable standards to ensure compliance. Additionally, auditors often scrutinize prepaid rent accounts for accuracy, making proper adjustments a critical component of financial reporting. By understanding these nuances, businesses can avoid misstatements and enhance the credibility of their financial statements.

Renting by Gender: Navigating Sex-Based Housing Options and Considerations

You may want to see also

Explore related products

![]()

Prepaid Rent Amortization Schedule

Prepaid rent often requires adjustment to align with the matching principle in accounting, ensuring expenses are recognized in the period they benefit. A Prepaid Rent Amortization Schedule is a systematic tool used to allocate the cost of prepaid rent over the rental period, typically month by month. This schedule is essential for businesses that pay rent in advance, as it prevents the entire payment from being expensed in a single period, distorting financial statements. For example, if a company pays $12,000 annually in January for rent, the amortization schedule would allocate $1,000 to each month, ensuring the expense is evenly distributed.

Creating a Prepaid Rent Amortization Schedule involves several steps. First, identify the total prepaid amount and the rental period. Next, divide the total prepaid rent by the number of months covered. For instance, a $6,000 six-month prepaid rent would result in a monthly expense of $1,000. Record this amount in the rent expense account each month, while reducing the prepaid rent asset account by the same amount. This process ensures the balance sheet and income statement accurately reflect the company’s financial position and performance over time.

One common mistake in prepaid rent adjustment is failing to update the amortization schedule when lease terms change. For example, if a lease is extended or terminated early, the schedule must be revised to reflect the new rental period. Additionally, businesses should avoid manually calculating adjustments, as this increases the risk of errors. Instead, use accounting software or spreadsheets to automate the process, ensuring accuracy and consistency. Regularly reviewing the schedule also helps identify discrepancies early, preventing cumulative errors.

From a comparative perspective, prepaid rent amortization differs from other prepaid expenses, such as insurance or supplies, due to its recurring and predictable nature. While insurance premiums might cover a fixed term, rent payments often follow a monthly or annual cycle, making them easier to amortize. However, the principle remains the same: match the expense to the period it benefits. For instance, a company paying $10,000 for a year of insurance would amortize $833.33 monthly, similar to rent but with a different underlying structure.

In conclusion, a Prepaid Rent Amortization Schedule is a critical tool for accurate financial reporting, ensuring prepaid rent is expensed systematically over the rental period. By following a structured approach, avoiding common pitfalls, and leveraging technology, businesses can maintain compliance with accounting standards while providing a clear financial picture. Whether managing a small business or a large corporation, mastering this process is essential for effective financial management.

Ultimate Guide to Renting an RV for Cross-Country Adventures

You may want to see also

Explore related products

![]()

Difference Between Prepaid and Accrued Rent

Prepaid and accrued rent are two distinct accounting concepts that reflect different timing of cash flows and expense recognition. Prepaid rent occurs when a tenant pays rent in advance for a future period, while accrued rent arises when rent is owed but not yet paid for a period that has already passed. Understanding the difference is crucial for accurate financial reporting and proper account adjustments.

Analyzing the Accounts Involved

Prepaid rent is recorded as a current asset on the balance sheet because it represents a payment made for future benefits. For example, if a company pays $12,000 in January for six months of rent, $10,000 would be recorded as prepaid rent, and $2,000 would be expensed in January. Each subsequent month, $2,000 is moved from the prepaid rent account to the rent expense account, reflecting the consumption of the prepaid benefit. In contrast, accrued rent is recorded as a current liability on the balance sheet and an expense on the income statement. If a tenant occupies a property in December but pays in January, the landlord records the rent as accrued rent payable in December, ensuring the expense is matched to the period it was incurred.

Practical Application and Adjustment

Adjusting entries are essential for both prepaid and accrued rent to align financial statements with the accrual accounting principle. For prepaid rent, the adjustment involves debiting rent expense and crediting prepaid rent each month to reflect the portion of rent consumed. For accrued rent, the adjustment involves debiting rent expense and crediting accrued rent payable to recognize the obligation. For instance, if a tenant owes $3,000 in rent for December but pays in January, the landlord would debit rent expense and credit accrued rent payable in December, ensuring the expense is recognized in the correct period.

Impact on Financial Statements

The treatment of prepaid and accrued rent directly affects the income statement and balance sheet. Prepaid rent reduces cash outflow in the period of payment but increases assets, while accrued rent increases expenses and liabilities in the period the rent is incurred. For example, a company with $5,000 in prepaid rent and $2,000 in accrued rent would show $5,000 as an asset and $2,000 as a liability, respectively. Properly managing these accounts ensures that financial statements accurately reflect the company’s financial position and performance.

Key Takeaway for Accountants

Distinguishing between prepaid and accrued rent is vital for maintaining accurate financial records. Prepaid rent is an asset that requires periodic adjustments to recognize expenses, while accrued rent is a liability that ensures expenses are matched to the period they are incurred. By understanding these differences, accountants can ensure compliance with accounting standards and provide stakeholders with a clear and accurate financial picture. Regular reviews of these accounts, especially at month-end or year-end, are essential to avoid misstatements and maintain transparency.

Discover Affordable NYC Rentals: Smart Tips for Cheap Rent in New York

You may want to see also

Frequently asked questions

A prepaid rent adjustment is an accounting entry made to recognize the portion of prepaid rent that applies to the current accounting period, ensuring that expenses are matched with the revenues they help generate.

The accounts typically used are the Prepaid Rent (asset) account and the Rent Expense (expense) account. The adjustment reduces the prepaid rent asset and increases the rent expense.

The journal entry debits Rent Expense (to recognize the expense) and credits Prepaid Rent (to reduce the asset) for the amount of rent applicable to the current period.

Prepaid rent adjustments should be made at the end of each accounting period (e.g., monthly, quarterly) to allocate the prepaid rent expense accurately over the rental period.

The purpose is to comply with the matching principle in accounting, ensuring that expenses are recognized in the same period as the revenues they help generate, providing a more accurate financial picture.