Prepaid rent is a crucial concept in accounting and financial reporting, representing the amount of rent paid in advance for a future period. It appears on a company's balance sheet as a current asset, reflecting the portion of rent that has been paid but not yet utilized or expired. The amount that appears for prepaid rent on the balance sheet is typically calculated by determining the value of rent that pertains to the period beyond the reporting date, ensuring accurate representation of the company's financial position and adherence to accounting principles such as the matching principle. This entry helps in providing a clear picture of the company's short-term assets and its commitment to future rental obligations.

| Characteristics | Values |

|---|---|

| Definition | Prepaid rent is an amount paid in advance for the use of a property or space before the rental period begins. |

| Balance Sheet Classification | Current asset (if the prepaid period is within one year or the operating cycle, whichever is longer). |

| Journal Entry | Debit: Prepaid Rent (Asset), Credit: Cash (Asset) or Bank (Asset). |

| Expense Recognition | Recognized as rent expense over the period the rent covers, typically using the straight-line method. |

| Adjusting Entry | At the end of the accounting period, an adjusting entry is made to recognize the portion of prepaid rent that has been used: Debit: Rent Expense, Credit: Prepaid Rent. |

| Financial Statement Impact | Reduces cash/bank balance initially and is gradually expensed, affecting the income statement over time. |

| Tax Treatment | Generally not deductible in the year of payment but is expensed over the rental period for tax purposes. |

| Example | If $12,000 is paid for a year's rent in advance, $1,000 is recognized as rent expense each month. |

| Reporting | Appears on the balance sheet under current assets until fully expensed. |

| Relevance | Important for accurate financial reporting and matching expenses with the periods they benefit. |

Explore related products

What You'll Learn

![]()

Initial Prepaid Rent Calculation

Prepaid rent is a common accounting concept that reflects the advance payment of rent for a future period. When calculating the initial prepaid rent amount, the focus is on determining the portion of rent that applies to a period beyond the current accounting cycle. This calculation is crucial for accurately representing financial obligations and ensuring compliance with accounting standards like GAAP or IFRS. For instance, if a business pays $12,000 annually for rent in December but the payment covers the upcoming year, only $1,000 (1/12 of the total) would be recognized as an expense in December, with the remaining $11,000 recorded as a prepaid asset.

To perform an initial prepaid rent calculation, start by identifying the total rent payment and the period it covers. Divide the total payment by the number of periods (usually months) to determine the monthly rent. Next, allocate the appropriate portion to the current period as an expense and the remainder as a prepaid asset. For example, a $6,000 payment for six months of rent would result in $1,000 expensed monthly, with the unexpired portion tracked on the balance sheet. This method ensures expenses are matched to the correct accounting period, aligning with the accrual accounting principle.

A practical tip for businesses is to maintain detailed lease agreements and payment schedules to simplify prepaid rent calculations. Errors in this area can distort financial statements, leading to misrepresentations of liquidity and profitability. For instance, overstating prepaid rent could inflate assets, while understating it might underreport liabilities. Small businesses, in particular, should use accounting software or spreadsheets to automate these calculations, reducing the risk of manual errors. Regularly reconciling prepaid rent accounts with lease terms can also prevent discrepancies.

Comparatively, prepaid rent differs from other prepaid expenses like insurance or utilities in its recurring nature and typically larger amounts. While prepaid insurance might cover a fixed term (e.g., one year), rent often involves longer-term commitments, such as multi-year leases. This distinction highlights the need for precise calculations to avoid over or under-allocation. For example, a three-year lease paid annually requires careful monthly allocation to reflect the correct expense and asset balances each period.

In conclusion, the initial prepaid rent calculation is a critical task that demands accuracy and attention to detail. By understanding the lease terms, applying proper allocation methods, and leveraging tools for consistency, businesses can ensure their financial statements accurately reflect their rental obligations. This not only supports compliance but also provides stakeholders with a clear picture of the company’s financial health.

Is Office Rent a Supply or Equipment? Understanding Business Expenses

You may want to see also

Explore related products

![]()

Monthly Rent Adjustment Process

Prepaid rent often appears as a current asset on a balance sheet, reflecting the portion of rent paid in advance that applies to future periods. This accounting treatment ensures financial statements accurately represent a company’s obligations and resources. However, when rent adjustments occur, the process becomes more complex, requiring careful recalibration of prepaid rent balances. The Monthly Rent Adjustment Process is a critical mechanism for aligning prepaid rent with actual occupancy costs, ensuring both landlords and tenants maintain accurate financial records.

The first step in the Monthly Rent Adjustment Process involves identifying the basis for the adjustment. Common triggers include changes in lease terms, fluctuations in utility costs, or revisions to shared expense allocations. For instance, if a tenant’s rent includes a variable component tied to property taxes, an increase in tax assessments would necessitate an upward adjustment. Conversely, a decrease in shared maintenance costs might result in a credit to the tenant. These adjustments must be documented in writing to ensure transparency and compliance with lease agreements.

Once the adjustment basis is established, the next step is calculating the revised rent amount. This calculation typically involves prorating the adjustment over the remaining lease term or applying it immediately, depending on the lease’s stipulations. For example, if a $120 annual increase is applied mid-year, the monthly adjustment would be $10, with the remaining $60 distributed across the subsequent months. Precision in this step is crucial, as errors can lead to disputes or financial discrepancies.

After calculating the adjustment, the prepaid rent balance must be updated accordingly. If the adjustment increases the rent, the prepaid balance is reduced to reflect the higher monthly obligation. Conversely, a decrease in rent would increase the prepaid balance. This step often requires journal entries in accounting software, such as debiting rent expense and crediting prepaid rent for an increase. Regular reconciliation ensures the prepaid rent account remains accurate and aligns with the adjusted rent schedule.

Finally, communication is key to a successful Monthly Rent Adjustment Process. Tenants should receive detailed statements explaining the adjustment, including the rationale, calculation method, and impact on their prepaid balance. Landlords, meanwhile, must ensure their accounting systems reflect the changes accurately. For businesses, this process may involve coordinating with finance teams to update budgets and forecasts. By maintaining clarity and accuracy, both parties can avoid misunderstandings and ensure financial integrity.

In practice, the Monthly Rent Adjustment Process demands attention to detail, adherence to lease terms, and proactive communication. Whether triggered by external factors or contractual provisions, adjustments must be handled methodically to preserve the accuracy of prepaid rent accounts. For tenants and landlords alike, mastering this process is essential for maintaining financial transparency and fulfilling lease obligations effectively.

Renting Made Easy: A Guide to Redbox On Demand Streaming

You may want to see also

Explore related products

![]()

Prepaid Rent Expense Recognition

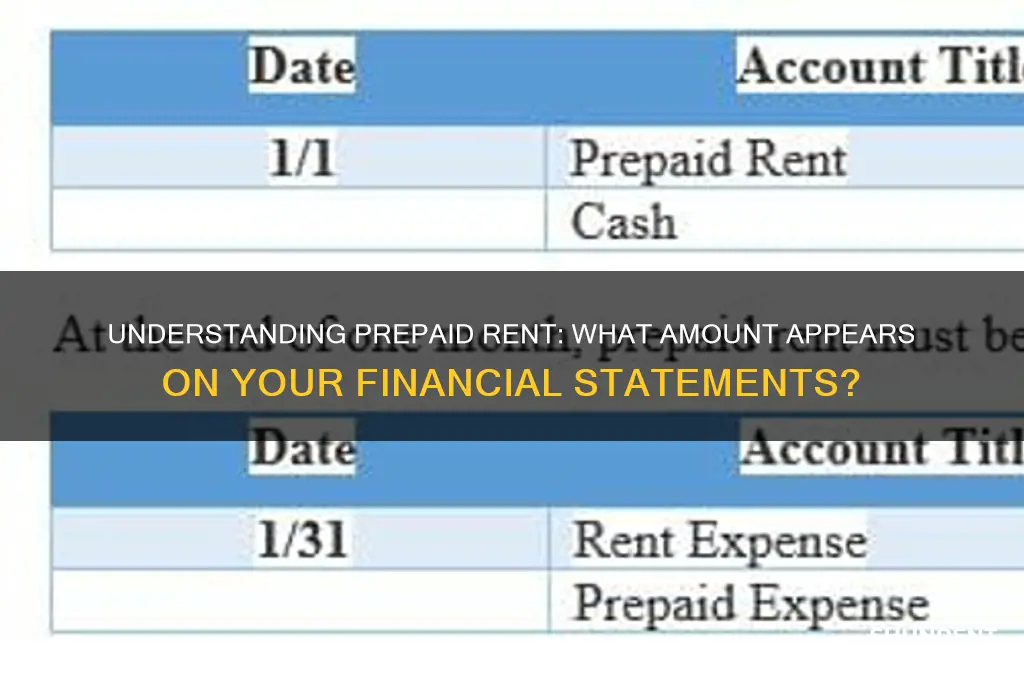

Prepaid rent represents a unique accounting challenge, as it involves paying for a future benefit upfront. When a business prepays rent, the entire amount is not immediately recognized as an expense. Instead, it is recorded as an asset on the balance sheet, reflecting the value of the future rental period. This initial entry ensures that the financial statements accurately represent the company’s resources and obligations. For example, if a company pays $12,000 for a year’s rent in January, the journal entry would debit Prepaid Rent (an asset) and credit Cash for $12,000. At this stage, no expense is recognized.

The recognition of prepaid rent expense occurs systematically over the rental period, aligning with the matching principle of accounting. This principle dictates that expenses should be matched with the revenues they help generate. To achieve this, the prepaid rent asset is gradually expensed each month. Using the previous example, the company would recognize $1,000 of rent expense monthly ($12,000 / 12 months). This is typically done through an adjusting entry, debiting Rent Expense and crediting Prepaid Rent for the monthly amount. By the end of the year, the Prepaid Rent account would be fully expensed, and the asset would be reduced to zero.

A common misconception is that prepaid rent is an expense at the time of payment. However, this approach would distort financial statements by overstating expenses in the prepaid period and understating them in subsequent periods. Proper recognition ensures consistency and accuracy in financial reporting. For instance, a quarterly report would reflect only the rent expense for that quarter, not the entire prepaid amount. This method provides a clearer picture of the company’s financial health and operational efficiency.

Practical implementation requires careful tracking and documentation. Businesses should maintain a schedule of prepaid expenses, detailing the initial payment, the rental period, and the monthly expense recognition. This ensures compliance with accounting standards and facilitates audits. For example, a small business prepaying $6,000 for six months of rent should create a schedule showing $1,000 expensed monthly. Additionally, accounting software often automates this process, reducing the risk of errors and saving time.

In conclusion, prepaid rent expense recognition is a critical aspect of financial accounting that balances asset management with expense reporting. By understanding and applying the principles outlined above, businesses can maintain accurate financial records and make informed decisions. Whether through manual tracking or automated systems, the key is consistency and adherence to accounting standards. This approach not only ensures compliance but also enhances the reliability of financial statements for stakeholders.

Washington State Rent Due Dates and Late Fees Explained

You may want to see also

Explore related products

![]()

Balance Sheet Reporting Method

Prepaid rent is a current asset that represents the amount of rent paid in advance for a future period. When reporting prepaid rent on a balance sheet, the focus is on accurately reflecting the portion of the payment that pertains to the current accounting period versus future periods. The balance sheet reporting method for prepaid rent involves allocating the prepaid amount between the current and future periods, ensuring that the financial statements provide a true and fair view of the company’s financial position.

Step-by-Step Reporting Process

To report prepaid rent on the balance sheet, follow these steps:

- Identify the Prepaid Amount: Determine the total rent paid in advance. For example, if a company pays $12,000 for six months of rent upfront, this is the prepaid amount.

- Allocate to Current Period: Calculate the portion of the prepaid rent that applies to the current accounting period. If one month has elapsed, $2,000 ($12,000 / 6 months) is expensed, and the remaining $10,000 is considered prepaid.

- Record Journal Entries: Debit "Prepaid Rent" (an asset account) for $12,000 and credit "Cash" for $12,000 initially. At the end of the first month, debit "Rent Expense" for $2,000 and credit "Prepaid Rent" for $2,000.

- Balance Sheet Presentation: Show the remaining prepaid amount ($10,000 in this case) under current assets on the balance sheet.

Cautions in Reporting

Misreporting prepaid rent can distort financial statements. Common errors include expensing the entire prepaid amount immediately or failing to adjust for the current period’s usage. For instance, if a company pays $24,000 for a year’s rent in January but expenses it all in the first month, it overstates expenses and understates assets. Additionally, ensure consistency in accounting treatment across periods to comply with GAAP or IFRS standards.

Practical Example and Takeaway

Consider a startup that pays $6,000 for three months of office rent in advance. At the end of the first month, $2,000 is expensed, leaving $4,000 as prepaid rent on the balance sheet. This method ensures the expense matches the period it benefits, aligning with the matching principle. The takeaway is clear: prepaid rent should be reported as a current asset, with only the unused portion appearing on the balance sheet, providing a transparent view of liquidity and financial health.

Comparative Analysis

Unlike accrued expenses, which are liabilities, prepaid rent is an asset because it represents a future benefit. For example, if a company accrues $1,000 in utilities, it records a liability until paid. In contrast, prepaid rent of $1,000 is an asset until the rent period is used. This distinction highlights the importance of classifying prepaid rent correctly on the balance sheet to avoid misrepresenting obligations and resources. By adhering to the balance sheet reporting method, companies ensure prepaid rent is accurately reflected, supporting informed decision-making by stakeholders.

Renting a Cabana at Hurricane Harbor: Your Ultimate Relaxation Guide

You may want to see also

Explore related products

![]()

Prepaid Rent Amortization Schedule

Prepaid rent represents an advance payment for future occupancy, a common practice in commercial leases to secure favorable terms or simplify cash flow management. However, accounting principles require this asset to be recognized systematically over the rental period, not all at once. This is where the prepaid rent amortization schedule becomes essential. It’s a structured plan that allocates the prepaid amount across the lease term, ensuring compliance with accrual accounting standards and providing a clear financial snapshot.

Constructing an amortization schedule involves dividing the total prepaid rent by the number of periods it covers. For instance, if a business prepays $12,000 for a year’s rent, the schedule would allocate $1,000 per month to the rent expense account. This method aligns expenses with the period in which the benefit is consumed, a cornerstone of the matching principle. The schedule typically includes columns for the period, beginning balance, amortization amount, and ending balance, offering transparency and predictability in financial reporting.

One critical aspect of the amortization schedule is its adaptability to lease terms. For example, if a lease includes a free rent period or escalating payments, the schedule must reflect these nuances. Advanced software tools or spreadsheet templates can automate this process, reducing errors and saving time. However, manual calculations remain viable for simpler leases, provided the formula is applied consistently. The key is to ensure the schedule accurately mirrors the lease agreement’s structure.

From a strategic perspective, the prepaid rent amortization schedule serves as a financial planning tool. It helps businesses forecast cash flow, manage tax liabilities, and assess the true cost of occupancy. For instance, a company with multiple prepaid leases can aggregate schedules to identify peak expense months or optimize tax deductions. Additionally, auditors and stakeholders often scrutinize these schedules for accuracy, making them a critical component of financial integrity.

In conclusion, the prepaid rent amortization schedule is more than a compliance tool—it’s a dynamic instrument for financial clarity and strategic decision-making. By breaking down prepaid rent into manageable, periodic expenses, it bridges the gap between upfront payments and ongoing benefits. Whether managed manually or through software, its precision and adaptability make it indispensable for businesses navigating complex lease agreements.

Should You Use Cash App for Rent Payments? Pros and Cons

You may want to see also

Frequently asked questions

The amount that appears for prepaid rent on the balance sheet is the portion of rent paid in advance that has not yet been used or expired.

The prepaid rent amount is determined by calculating the total rent paid in advance and subtracting the portion that has been consumed or pertains to the current accounting period.

Yes, the prepaid rent amount decreases over time as the prepaid period expires and is recognized as an expense in the income statement.

The prepaid rent amount appears under the "Current Assets" section of the balance sheet, as it represents a short-term asset that will be used within one year.

Once the rental period begins, the prepaid rent amount is gradually expensed to the income statement as rent expense, reducing the prepaid balance on the balance sheet.