Rent is typically categorized as an operating expense in accounting, falling under the broader category of selling, general, and administrative expenses (SG&A). For businesses, rent payments are considered a necessary cost of doing business, particularly for leased properties such as office space, retail locations, or equipment. In financial statements, rent is recorded as an expense on the income statement, reducing the company’s net income, and is also reflected in the cash flow statement as an outflow from operating activities. Proper classification of rent ensures accurate financial reporting and helps stakeholders understand the company’s cost structure and operational efficiency.

| Characteristics | Values |

|---|---|

| Accounting Category | Expense |

| Type of Expense | Operating Expense (for businesses) or Personal Expense (for individuals) |

| Financial Statement | Income Statement (for businesses) or Personal Budget (for individuals) |

| Timing | Recorded when incurred (accrual basis) or when paid (cash basis) |

| Tax Treatment | Tax-deductible for businesses; not deductible for personal rent (in most cases) |

| Account Classification | Rent Expense (for businesses) or Housing Expense (for individuals) |

| Frequency | Typically monthly or annually |

| Impact on Cash Flow | Reduces cash balance when paid |

| Matching Principle | Matches the expense to the period in which the benefit is received |

| Common Ledger Account | Rent Expense (for businesses) |

| Example | Monthly office rent for a business or apartment rent for an individual |

Explore related products

What You'll Learn

- Expense Classification: Rent is categorized as an operating expense in the income statement

- Prepaid Rent: Recorded as a current asset until the rental period is utilized

- Lease Accounting: Classified under ASC 842 or IFRS 16 for long-term leases

- Cash Flow Treatment: Rent payments are reported under operating activities in cash flow statements

- Tax Deductibility: Rent is generally tax-deductible as a business expense

![]()

Expense Classification: Rent is categorized as an operating expense in the income statement

Rent, a ubiquitous cost for businesses and individuals alike, is classified as an operating expense in the income statement. This categorization is not arbitrary; it stems from the fundamental nature of rent as a necessary, ongoing cost directly tied to the core operations of a business. Unlike capital expenditures, which involve the acquisition of long-term assets, rent represents a periodic payment for the use of property or equipment essential to day-to-day activities. For instance, a retail store’s rent for its storefront is directly linked to its ability to operate and generate revenue, making it an operational rather than a capital expense.

From an accounting perspective, classifying rent as an operating expense serves multiple purposes. Firstly, it provides a clear picture of a company’s operational efficiency by grouping rent with other day-to-day costs like utilities, wages, and supplies. This allows stakeholders to assess how well a business manages its core expenses relative to its revenue. Secondly, it adheres to accounting principles such as GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), ensuring consistency and comparability across financial statements. For example, a manufacturing company’s rent for its factory would be reported alongside other production-related expenses, offering transparency into its cost structure.

One practical takeaway for business owners is the importance of accurately tracking and allocating rent expenses. Misclassification can distort financial ratios like operating profit margin, misleading investors and internal decision-makers. For instance, if a tech startup mistakenly categorizes office rent as a capital expense, it could artificially inflate its profitability in the short term, only to face corrections later. To avoid this, businesses should maintain clear expense policies and leverage accounting software that automates proper categorization based on predefined rules.

Comparatively, rent contrasts with expenses like depreciation, which is also an operating expense but relates to the wear and tear of owned assets. While both are operational in nature, rent is an external payment, whereas depreciation is an internal allocation of cost. This distinction highlights the importance of understanding the source and purpose of each expense. For a small business owner, recognizing this difference can inform decisions about leasing versus purchasing property, balancing cash flow needs with long-term asset ownership.

In conclusion, rent’s classification as an operating expense is a cornerstone of accurate financial reporting. It reflects the expense’s direct role in sustaining business operations and aligns with established accounting standards. By properly categorizing rent, businesses ensure their financial statements provide a true and fair view of their operational health, enabling informed decision-making and stakeholder trust. Whether for a multinational corporation or a local café, this classification is a critical detail with far-reaching implications.

Is Rent Money a Liability? Understanding Your Financial Obligations

You may want to see also

Explore related products

![]()

Prepaid Rent: Recorded as a current asset until the rental period is utilized

Rent, in accounting, is typically categorized as an expense when it is incurred and paid. However, when rent is paid in advance, it takes on a different classification: prepaid rent. This concept is crucial for accurate financial reporting and understanding a company’s short-term financial health. Prepaid rent is recorded as a current asset on the balance sheet, reflecting the portion of rent that has been paid but not yet used. This treatment ensures that the expense is recognized in the period it benefits, aligning with the matching principle in accounting.

Consider a scenario where a business pays $12,000 annually for office space in January, covering the entire year. Instead of expensing the full $12,000 immediately, the company records $1,000 as a rent expense each month and maintains the remaining balance as prepaid rent. At the end of January, the balance sheet would show $11,000 under prepaid rent (a current asset) and $1,000 as rent expense on the income statement. This method provides a clearer picture of the company’s financial position by deferring the expense recognition to the periods in which the rental benefit is actually received.

Recording prepaid rent as a current asset is particularly important for liquidity analysis. Current assets are expected to be used or converted into cash within one year, and prepaid rent falls into this category because it represents a future economic benefit. For instance, if a company has $20,000 in prepaid rent for the next six months, this amount is considered part of its working capital, signaling its ability to meet short-term obligations. However, it’s essential to distinguish prepaid rent from long-term assets, as its usefulness is limited to the rental period covered.

A practical tip for businesses is to regularly review prepaid rent accounts to ensure accuracy. For example, if a lease ends early or terms change, the prepaid balance must be adjusted accordingly. Failure to do so can lead to overstatement of assets and misrepresentation of financial health. Additionally, companies should reconcile prepaid rent accounts monthly, comparing them to lease agreements and payment schedules to avoid errors. This diligence ensures compliance with accounting standards and provides stakeholders with reliable financial information.

In summary, prepaid rent serves as a bridge between expense recognition and asset utilization, embodying the principles of accrual accounting. By recording it as a current asset, businesses maintain transparency and accuracy in their financial statements. This approach not only adheres to accounting standards but also aids in effective financial planning and analysis. Understanding and managing prepaid rent correctly is thus a critical skill for accountants and business leaders alike.

Recording Rent Concessions in Commercial Leases: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

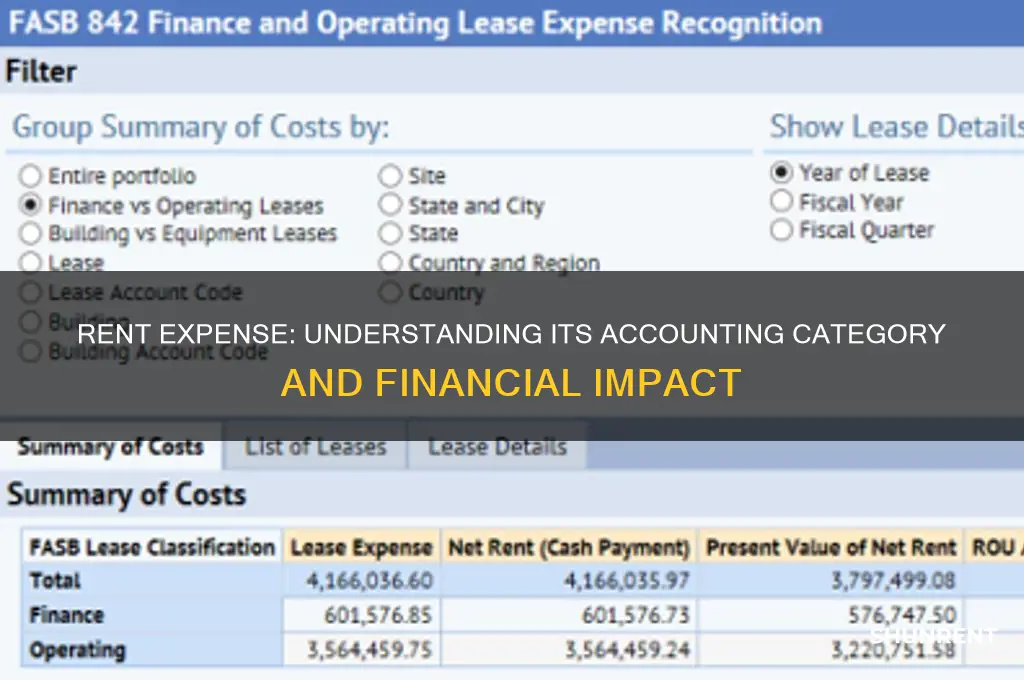

Lease Accounting: Classified under ASC 842 or IFRS 16 for long-term leases

Rent, a ubiquitous expense for businesses and individuals alike, is not merely a straightforward payment in the world of accounting. Its classification can significantly impact financial statements, particularly when dealing with long-term leases. This is where the intricacies of lease accounting come into play, specifically under the guidelines of ASC 842 (Accounting Standards Codification 842) and IFRS 16 (International Financial Reporting Standards 16).

Understanding the Shift in Lease Accounting

The introduction of ASC 842 and IFRS 16 marked a significant change in how leases are accounted for, moving away from the traditional operating and capital lease distinction. These standards mandate that lessees recognize most leases on their balance sheets, providing a more comprehensive view of an entity's financial obligations. This shift is particularly crucial for long-term leases, which were often treated as operating leases and kept off the balance sheet under previous standards.

Classifying Leases: A Practical Approach

Under ASC 842 and IFRS 16, the classification of leases is straightforward. All leases, except for short-term leases (12 months or less) and low-value assets, must be recognized on the balance sheet. This means that long-term leases, such as those for office spaces, retail stores, or equipment, will result in the recognition of a right-of-use asset and a corresponding lease liability. The right-of-use asset represents the lessee's right to use the leased asset, while the lease liability reflects the obligation to make lease payments.

Impact on Financial Statements

The implications of this classification are far-reaching. By bringing long-term leases onto the balance sheet, companies provide a more accurate representation of their financial health. Investors and creditors gain a clearer understanding of an entity's long-term obligations, which can influence lending decisions and investment strategies. For instance, a company with significant lease commitments may appear more leveraged, potentially affecting its credit rating and borrowing costs.

Navigating the Transition: A Step-by-Step Guide

- Identify Leases: Review all contracts to identify arrangements that meet the definition of a lease under ASC 842 or IFRS 16.

- Classify Leases: Determine whether each lease is short-term or low-value, as these may be exempt from balance sheet recognition.

- Calculate Lease Liability: Measure the present value of future lease payments to establish the lease liability.

- Recognize Right-of-Use Asset: Record the right-of-use asset, initially measured at the amount of the lease liability, adjusted for initial direct costs, lease incentives, and any prepaid lease payments.

- Ongoing Accounting: Subsequently, account for lease payments by allocating the payment between the reduction of the lease liability and interest expense. Also, recognize depreciation expense for the right-of-use asset.

Cautions and Considerations

While the new standards enhance transparency, they also introduce complexity. Companies must carefully assess the impact of lease classification on their financial ratios and covenants. Additionally, the transition may require significant effort, particularly for entities with numerous leases. It is essential to plan the transition process meticulously, ensuring compliance with the specific requirements of ASC 842 or IFRS 16, depending on the applicable jurisdiction.

In conclusion, the classification of rent under ASC 842 or IFRS 16 for long-term leases is a critical aspect of modern accounting. By understanding and applying these standards, businesses can provide a more accurate and transparent view of their financial position, ultimately fostering greater trust and confidence among stakeholders.

How to Efficiently Separate Rocks from Dirt?

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61gNC08X3PL._AC_UY218_.jpg)

![]()

Cash Flow Treatment: Rent payments are reported under operating activities in cash flow statements

Rent payments, a ubiquitous expense for businesses and individuals alike, are classified under operating activities in the cash flow statement. This categorization stems from the fundamental nature of rent as a core operational expense. Unlike investments or financing activities, rent is directly tied to the day-to-day functioning of a business, such as occupying office space, retail locations, or manufacturing facilities.

Consider a retail store: the rent for its storefront is essential for conducting sales, storing inventory, and providing a customer experience. Without this space, the business’s primary operations would cease. Thus, rent is not merely a cost but a critical enabler of revenue generation. This operational necessity justifies its inclusion under operating activities, aligning with accounting standards like the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP).

From a cash flow perspective, reporting rent under operating activities provides a clear picture of a company’s ability to generate cash from its core business functions. It distinguishes these payments from financing activities (e.g., loan repayments) or investing activities (e.g., purchasing equipment). For instance, a tech startup leasing office space would report these payments in the operating section of its cash flow statement, allowing stakeholders to assess how efficiently the company manages its primary operational expenses relative to its revenue.

However, nuances exist. Prepaid rent or lease deposits may blur the lines, as these involve upfront cash outflows not directly tied to current operations. In such cases, the treatment depends on the accounting method used (e.g., straight-line rent expense recognition). Practitioners must ensure consistency and transparency in reporting to avoid misleading interpretations.

In practice, businesses should meticulously track rent payments and reconcile them with lease agreements to ensure accurate cash flow reporting. Tools like accounting software can automate this process, reducing errors and saving time. For investors and analysts, understanding this classification is crucial for evaluating a company’s operational efficiency and liquidity. Rent, though a routine expense, carries significant weight in financial storytelling—its proper treatment in cash flow statements is non-negotiable.

Where to Rent Snorkel Gear in Cancun: A Quick Guide

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![Rent: Filmed Live on Broadway [Blu-ray]](https://m.media-amazon.com/images/I/51SDxJNQfVL._AC_UY218_.jpg)

![Rent (Blu-ray) Starring Rosario Dawson, Taye Diggs, Jesse L. Martin, Idina Menzel [Spanish Artwork]](https://m.media-amazon.com/images/I/81wUIoGBEcL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

![]()

Tax Deductibility: Rent is generally tax-deductible as a business expense

Rent, a significant expense for many businesses, often qualifies as a tax-deductible item, providing a crucial financial benefit. This deduction falls under the category of ordinary and necessary business expenses in accounting, as outlined by tax authorities like the IRS in the United States. To qualify, the rent must be directly related to the operation of the business, such as leasing office space, retail locations, or manufacturing facilities. For instance, a small business owner renting a storefront can deduct the monthly rent payments from their taxable income, reducing their overall tax liability. This classification ensures that businesses can offset the cost of maintaining a physical presence, which is essential for operations.

However, not all rent expenses are treated equally. Leasehold improvements, which are modifications made to a rented property to suit business needs, may be depreciated over time rather than deducted in full immediately. For example, if a company installs custom shelving in a rented warehouse, the cost of the shelving would be capitalized and depreciated over its useful life. Understanding these nuances is critical for accurate tax reporting and maximizing deductions. Additionally, home-based businesses must allocate rent expenses between personal and business use, deducting only the portion attributable to business activities.

From a strategic perspective, businesses should carefully document their rent expenses to ensure compliance with tax regulations. This includes maintaining lease agreements, payment receipts, and records of business usage for rented spaces. For example, a freelancer using a spare room as a home office could deduct a portion of their rent based on the square footage dedicated to business activities. Proper documentation not only supports tax deductions but also protects against audits. Businesses should also consult tax professionals to navigate complexities, such as differentiating between rent and other property-related expenses like utilities or maintenance, which may have different deductibility rules.

Comparatively, rent deductions differ across jurisdictions, with some countries offering more favorable tax treatments than others. In Canada, for instance, rent expenses are fully deductible if they are reasonable and directly tied to earning business income. In contrast, some European countries may impose limits on deductibility based on the type of property or the business’s legal structure. International businesses must therefore stay informed about local tax laws to optimize their deductions. For example, a multinational corporation with offices in multiple countries would need to tailor its accounting practices to align with each region’s regulations, ensuring compliance while maximizing tax benefits.

In practical terms, businesses can enhance their tax savings by structuring rent agreements thoughtfully. For instance, negotiating a lease with a lower base rent and higher variable costs (e.g., percentage rent based on sales) could provide greater flexibility in managing cash flow. Similarly, short-term leases may offer more favorable tax treatment in certain scenarios, as they align with the business’s immediate needs. By proactively managing rent agreements and staying informed about tax laws, businesses can turn a fixed expense into a strategic financial tool, reducing their tax burden while maintaining operational efficiency.

Maximizing Farm Rental Income: Machinery Deduction Strategies for Landowners

You may want to see also

Frequently asked questions

Rent typically falls under the operating expenses category in accounting, as it is a regular, ongoing cost associated with running a business.

Rent is considered an expense, not an asset, because it represents a cost incurred for the use of a property or asset, rather than ownership.

Rent is recorded on the income statement as part of the operating expenses, reducing the net income for the period.

Yes, if rent is paid in advance, it is initially recorded as a prepaid expense (an asset) and then expensed over the rental period through amortization.