The income to rent ratio is a crucial financial metric used to assess the affordability of housing for individuals or households. It is calculated by dividing the tenant's monthly pre-tax income by their monthly rent payment, providing a clear picture of how much of their earnings are allocated to housing costs. This ratio is essential for both renters and landlords, as it helps determine whether the rent is sustainable for the tenant and reduces the risk of payment defaults. A commonly recommended guideline is that the income to rent ratio should be at least 3:1, meaning a person should earn at least three times the amount of their monthly rent to ensure financial stability and the ability to cover other living expenses comfortably. Understanding this ratio is vital for making informed decisions in the rental market and maintaining a balanced budget.

| Characteristics | Values |

|---|---|

| Definition | Income to rent ratio is a metric used to assess affordability of rent relative to income. It is calculated by dividing monthly rent by monthly gross income. |

| Ideal Ratio | Generally, a ratio of 30% or less is considered affordable, meaning no more than 30% of gross income should go toward rent. |

| Formula | Income to Rent Ratio = (Monthly Rent) / (Monthly Gross Income) × 100 |

| Purpose | Helps renters and landlords determine if rent is sustainable based on income. Also used by lenders to evaluate financial stability. |

| Industry Standard | A ratio above 30% may indicate financial strain, while below 30% suggests manageable housing costs. |

| Variability | Ratios can vary by location, income level, and personal financial circumstances. |

| Latest Data (Example) | As of 2023, the average U.S. renter spends ~27% of income on rent, though this varies by city (e.g., NYC: 40%, Houston: 25%). |

| Importance | Ensures renters avoid being "cost-burdened" and helps landlords assess tenant reliability. |

| Limitations | Does not account for other expenses (e.g., utilities, debt) or savings goals. |

| Regional Differences | Urban areas often have higher ratios due to higher rent costs compared to income. |

Explore related products

What You'll Learn

- Definition: Income to rent ratio measures affordability by comparing monthly income to rent costs

- Ideal Ratio: A 30% or lower ratio is generally considered financially manageable

- Calculation: Divide monthly rent by pre-tax income, then multiply by 100 for percentage

- Importance: Helps renters avoid financial strain and plan budgets effectively

- Variations: Ratios may differ based on location, lifestyle, and financial goals

![]()

Definition: Income to rent ratio measures affordability by comparing monthly income to rent costs

The income to rent ratio is a straightforward yet powerful tool for assessing housing affordability. It operates on a simple principle: divide your monthly pre-tax income by your monthly rent. The resulting figure, expressed as a percentage or ratio, reveals how much of your earnings are allocated to housing. For instance, if your monthly income is $5,000 and your rent is $1,500, your income to rent ratio is 30% (1,500 / 5,000). This calculation provides a clear snapshot of financial feasibility, helping both renters and landlords gauge sustainability.

A widely accepted rule of thumb is that a healthy income to rent ratio falls below 30%. Exceeding this threshold may indicate financial strain, as a larger portion of income is devoted to housing, leaving less for other essentials like food, transportation, and savings. For example, a ratio of 40% means nearly half of your income goes toward rent, which could limit your ability to handle unexpected expenses or save for the future. This benchmark is particularly useful for renters evaluating their budget or landlords assessing tenant risk.

However, the 30% rule isn’t one-size-fits-all. Factors like location, income level, and personal financial goals can influence what’s considered affordable. In high-cost urban areas like New York or San Francisco, ratios above 30% are common due to skyrocketing rents. Conversely, in more affordable regions, a lower ratio might be achievable. Renters should also consider their broader financial picture, including debt obligations and savings targets, when interpreting their ratio.

To calculate your income to rent ratio accurately, ensure you’re using your gross monthly income (before taxes) and your total monthly rent, including any additional fees like utilities or parking. If your income varies, such as with freelance work, average your earnings over the past six months for a more reliable figure. For landlords, verifying a tenant’s income and calculating this ratio can help predict payment reliability. Tools like pay stubs, tax returns, or bank statements can aid in this process.

Ultimately, the income to rent ratio is more than just a number—it’s a diagnostic tool for financial health. Whether you’re a renter aiming to stay within budget or a landlord screening tenants, understanding this metric empowers better decision-making. By keeping your ratio in check, you can ensure housing remains affordable without compromising other financial priorities. Use it as a starting point, but always tailor your approach to your unique circumstances for the most accurate assessment.

Is Splitting Rent with a Couple Fair? Pros, Cons, and Considerations

You may want to see also

Explore related products

![]()

Ideal Ratio: A 30% or lower ratio is generally considered financially manageable

A 30% income-to-rent ratio isn't just a financial rule of thumb—it's a benchmark for stability. This threshold, widely adopted by lenders and financial advisors, ensures that housing costs don’t overwhelm your budget. When rent consumes more than 30% of your income, essential expenses like groceries, healthcare, and savings often suffer. For instance, a household earning $4,000 monthly should aim to spend no more than $1,200 on rent to maintain this balance. Exceeding this ratio can lead to financial strain, making it harder to recover from unexpected expenses or build wealth over time.

Achieving a 30% or lower ratio requires strategic planning. Start by calculating your gross monthly income and multiplying it by 0.3 to determine your rent limit. If your income fluctuates, use a conservative average to avoid overcommitting. For example, a freelancer earning $5,000 one month and $3,000 the next should base their rent on the lower figure to ensure affordability during lean periods. Additionally, consider shared housing or less expensive neighborhoods to align with this ideal ratio. Tools like budgeting apps can help track income and expenses, making it easier to stay within this financial guardrail.

Critics argue that a 30% ratio is outdated, particularly in high-cost urban areas where housing consumes a larger share of income. However, this benchmark remains a practical starting point for financial health. Even in expensive cities, striving for this ratio encourages prioritization of needs over wants. For instance, a young professional in New York City might opt for a smaller apartment or a longer commute to keep rent manageable. While flexibility is necessary in certain markets, the 30% rule serves as a critical reminder to avoid overextending financially.

Ultimately, maintaining a 30% or lower income-to-rent ratio is about long-term financial resilience. It’s not just about affording rent today but ensuring you can save for emergencies, invest in your future, and enjoy life without constant financial stress. For families, this ratio is especially crucial, as it provides a buffer for childcare, education, and other expenses. By adhering to this guideline, you create a foundation for financial security, allowing you to navigate life’s uncertainties with greater confidence and peace of mind.

Renting Cinematography Gear: A Step-by-Step Guide for Filmmakers

You may want to see also

Explore related products

![]()

Calculation: Divide monthly rent by pre-tax income, then multiply by 100 for percentage

The income to rent ratio is a critical metric for assessing housing affordability, and its calculation is straightforward yet powerful. To determine this ratio, divide your monthly rent by your pre-tax income, then multiply the result by 100 to express it as a percentage. For example, if your monthly rent is $1,200 and your pre-tax income is $4,000, the calculation would be: ($1,200 ÷ $4,000) × 100 = 30%. This means 30% of your income goes toward rent, a figure often used as a benchmark for financial stability.

This calculation serves as a reality check for renters and landlords alike. Financial advisors typically recommend that your income to rent ratio should not exceed 30%, as this leaves room in your budget for other essential expenses like utilities, groceries, and savings. If the ratio surpasses this threshold, it may indicate financial strain. For instance, a ratio of 40% or higher suggests that a significant portion of your income is allocated to housing, potentially limiting your ability to manage unexpected costs or save for the future.

While the 30% rule is widely accepted, it’s not one-size-fits-all. Factors like location, lifestyle, and financial goals can influence what’s considered affordable. In high-cost urban areas like New York or San Francisco, ratios above 30% are common due to skyrocketing rents. Conversely, in more affordable regions, a lower ratio might be achievable and advisable. It’s essential to tailor this metric to your personal circumstances rather than adhering strictly to a generic guideline.

To use this calculation effectively, start by gathering accurate data. Ensure your pre-tax income includes all regular earnings, such as salary, bonuses, and side hustles. For renters, this exercise can help decide whether a particular property is within budget. For landlords, it can assist in setting rent prices that are both competitive and fair, reducing the risk of tenant turnover due to financial hardship. Regularly reviewing your income to rent ratio can also highlight when it’s time to adjust spending, increase income, or seek more affordable housing.

Finally, while the income to rent ratio is a valuable tool, it shouldn’t be viewed in isolation. Pair it with other financial metrics, such as debt-to-income ratio or savings rate, for a comprehensive view of your financial health. For example, someone with a high income and low debt might comfortably manage a 35% ratio, while someone with significant debt may struggle even at 25%. By understanding and applying this calculation thoughtfully, you can make informed decisions that align with your long-term financial goals.

Idina's Return to Rent on Broadway in 2008

You may want to see also

Explore related products

$16.99 $28.5

![]()

Importance: Helps renters avoid financial strain and plan budgets effectively

Rent should not exceed 30% of your gross monthly income, a rule of thumb that serves as a financial guardrail for renters. This income-to-rent ratio is a critical metric because it directly impacts your ability to manage other expenses and save for the future. When rent consumes a larger portion of your income, it leaves less room for essentials like groceries, utilities, transportation, and healthcare. By adhering to this ratio, renters can avoid the cycle of living paycheck to paycheck and build a more stable financial foundation.

Consider a renter earning $4,000 per month. Following the 30% rule, their rent should not surpass $1,200. If they choose an apartment costing $1,500, they’ll allocate 37.5% of their income to rent, leaving only $2,500 for all other expenses. This imbalance increases the risk of financial strain, especially during unexpected emergencies like car repairs or medical bills. Conversely, staying within the recommended ratio ensures a buffer for such situations and allows for discretionary spending or savings.

Planning a budget becomes significantly more manageable when the income-to-rent ratio is optimized. For instance, a renter with a $3,500 monthly income and $1,050 rent (30%) can allocate $800 to utilities, groceries, and transportation, $500 to savings, and still have $1,150 for leisure or debt repayment. This structured approach not only reduces stress but also fosters financial discipline. Renters who prioritize this ratio are better equipped to track spending, identify areas for cutbacks, and work toward long-term goals like homeownership.

However, adhering to the 30% rule isn’t always feasible, especially in high-cost urban areas where rent prices soar. In such cases, renters must make informed trade-offs. For example, a renter in San Francisco might spend 45% of their income on rent but compensate by reducing dining out or subscription services. The key is to remain mindful of the ratio’s purpose: to prevent rent from becoming a financial burden. Tools like budgeting apps or spreadsheets can help renters adjust other expenses to maintain balance, ensuring that overspending in one area doesn’t derail their financial health.

Ultimately, the income-to-rent ratio is more than a financial guideline—it’s a tool for empowerment. By understanding and applying this ratio, renters gain control over their finances, reduce the risk of strain, and create a sustainable budget. Whether you’re a first-time renter or a seasoned tenant, this metric serves as a compass, guiding you toward financial stability and peace of mind.

Renting Dragon Ball Super Hero: A Step-by-Step Guide for Fans

You may want to see also

Explore related products

![]()

Variations: Ratios may differ based on location, lifestyle, and financial goals

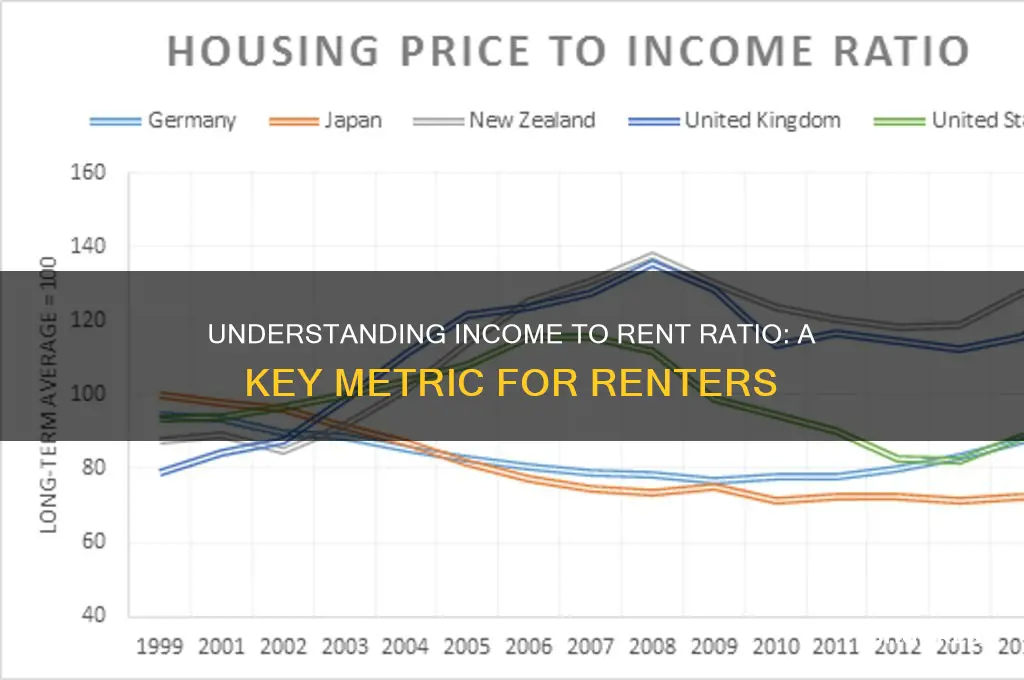

The income-to-rent ratio, often recommended as 30% or less, isn’t a one-size-fits-all rule. In high-cost cities like San Francisco or New York, renters frequently exceed this threshold, spending 40–50% of their income on housing due to limited options. Conversely, in rural areas or smaller towns, ratios as low as 20–25% are common, reflecting lower rents and cost of living. Location dictates not just affordability but also the feasibility of adhering to conventional financial guidelines.

Lifestyle choices further skew this ratio. A young professional prioritizing proximity to urban amenities might allocate 45% of their income to rent for a studio in a trendy neighborhood. Meanwhile, a remote worker in a suburban area could cap their housing expenses at 25% to prioritize savings or travel. The trade-off between convenience, comfort, and financial flexibility varies widely, making the "ideal" ratio deeply personal.

Financial goals also reshape this metric. Someone aggressively saving for a down payment on a home might aim for a 20% rent-to-income ratio, freeing up funds for investments. Conversely, a renter focused on debt repayment or building an emergency fund might accept a higher ratio temporarily. The ratio isn’t static—it evolves with priorities, whether that’s wealth accumulation, debt elimination, or lifestyle enhancement.

Practical adjustments can help align rent spending with individual circumstances. For instance, in expensive markets, consider roommates to reduce the effective rent-to-income ratio. In cheaper areas, negotiate lease terms or opt for longer contracts to lock in lower rates. Tools like budgeting apps can track spending and ensure housing costs don’t derail broader financial objectives. Ultimately, the ratio is a starting point, not a rigid rule—tailor it to your reality.

Who Pays HOA Fees: Landlord or Tenant? Key Responsibilities Explained

You may want to see also

Frequently asked questions

The income to rent ratio is a financial metric that compares a tenant’s monthly income to their monthly rent payment. It helps landlords assess affordability and ensures tenants can comfortably cover rent without financial strain.

The ratio is calculated by dividing the tenant’s monthly pre-tax income by their monthly rent. For example, if a tenant earns $4,000 per month and pays $1,200 in rent, the ratio is 3.33 ($4,000 ÷ $1,200).

A commonly recommended income to rent ratio is 3:1 or higher, meaning a tenant’s monthly income should be at least three times their monthly rent. This ensures they can afford rent while covering other expenses.

The ratio helps landlords evaluate a tenant’s ability to pay rent consistently. A higher ratio indicates lower risk of default, while a lower ratio may suggest potential financial instability. It’s a key factor in tenant screening.