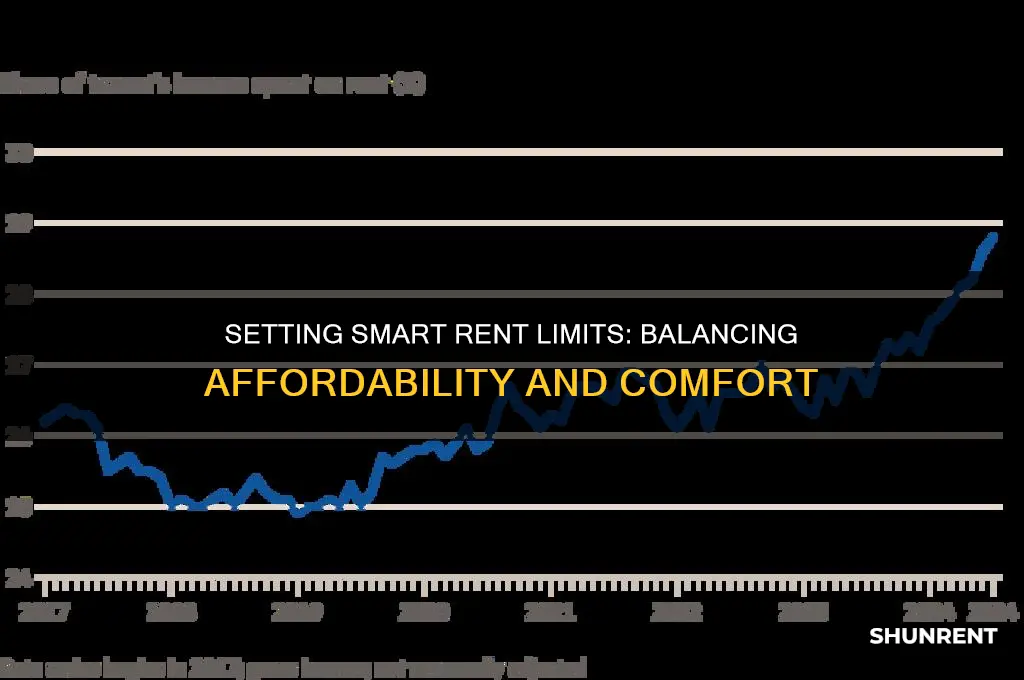

Setting a good limit on rent is a critical financial decision that balances affordability with lifestyle needs. A widely accepted rule of thumb is the 30% rule, which suggests that rent should not exceed 30% of your gross monthly income. This guideline helps ensure that you have enough funds left for other essential expenses, savings, and discretionary spending. However, this percentage may need adjustment based on individual circumstances, such as high cost-of-living areas, debt obligations, or personal financial goals. It’s also important to consider additional housing costs like utilities, maintenance, and transportation, which can significantly impact overall affordability. By carefully evaluating your income, expenses, and long-term financial objectives, you can determine a rent limit that supports both your current lifestyle and future stability.

| Characteristics | Values |

|---|---|

| 30% Rule | A widely accepted guideline suggesting that rent should not exceed 30% of your gross monthly income. |

| 50/30/20 Rule | Allocates 50% of income to needs (including rent), 30% to wants, and 20% to savings/debt repayment. Rent should ideally fit within the 50% needs category. |

| Local Cost of Living | Adjust rent limit based on regional or city-specific living costs (e.g., higher in NYC vs. rural areas). |

| Income Stability | Factor in job security and income consistency to ensure rent remains affordable during fluctuations. |

| Debt and Financial Obligations | Account for student loans, credit card debt, or other financial commitments when setting a rent limit. |

| Savings Goals | Ensure rent allows for meeting savings targets (e.g., emergency fund, retirement). |

| Utilities and Additional Costs | Include estimated costs for utilities, internet, parking, or other housing-related expenses in the rent limit. |

| Roommates or Shared Housing | Consider splitting rent with roommates to stay within budget. |

| Personal Lifestyle | Adjust rent limit based on priorities (e.g., living in a desirable neighborhood vs. saving more). |

| Market Rent Trends | Research average rent prices in your area to ensure your limit aligns with current market conditions. |

Explore related products

What You'll Learn

- Affordable Rent Percentage: Limit rent to 30% of monthly income for financial stability

- Local Market Rates: Research average rents in your area to set a competitive limit

- Budget Prioritization: Ensure rent leaves room for savings, utilities, and other expenses

- Roommate Sharing: Split rent proportionally based on room size or amenities

- Emergency Fund Impact: Keep rent low enough to maintain a 3-6 month emergency fund

![]()

Affordable Rent Percentage: Limit rent to 30% of monthly income for financial stability

A widely accepted rule of thumb suggests that rent should not exceed 30% of your monthly income. This guideline, often referred to as the 30% rule, has been a cornerstone of financial advice for decades, offering a simple yet effective way to ensure housing costs don't jeopardize overall financial stability. By adhering to this limit, individuals can better manage their budgets, allocate funds to other essential expenses, and build savings for future goals.

To apply this rule, calculate your monthly income after taxes and multiply it by 0.3. For instance, if your monthly take-home pay is $4,000, your rent should ideally not surpass $1,200. This calculation provides a clear boundary, helping you avoid the pitfalls of overcommitting to housing expenses. However, it's crucial to consider regional cost-of-living variations; in high-cost urban areas, finding rentals within this limit might require compromise on location or amenities.

Critics argue that the 30% rule may not be universally applicable, especially in cities with skyrocketing housing costs. For young professionals or low-income households, even this percentage can strain finances. In such cases, adjusting the rule to a more realistic 40% or exploring shared housing options might be necessary. Conversely, those with higher incomes or in lower-cost areas may aim for a 25% threshold to accelerate savings or debt repayment.

Despite its limitations, the 30% rule remains a valuable starting point for budgeting. It encourages individuals to prioritize financial health by balancing housing costs with other life expenses. Pairing this rule with additional strategies, such as tracking spending, building an emergency fund, and negotiating rent when possible, can further enhance financial resilience. Ultimately, while the 30% guideline isn't one-size-fits-all, it provides a practical framework for making informed decisions about rent affordability.

Where to Rent a Power Washer: Your Ultimate Cleaning Solution

You may want to see also

Explore related products

![]()

Local Market Rates: Research average rents in your area to set a competitive limit

Setting a rent limit without understanding local market rates is like navigating a maze blindfolded. You risk overpricing and scaring away tenants or underpricing and leaving money on the table. The first step to a smart rent limit is research—specifically, analyzing average rents in your area. This isn’t just about checking a single listing; it’s about gathering data from multiple sources, including rental websites, local real estate reports, and even word-of-mouth from neighbors. Tools like Zillow, Rentometer, and Craigslist can provide a snapshot of current trends, but don’t stop there. Dive into specifics: What’s the average rent for a two-bedroom apartment in your neighborhood? How do amenities like parking, laundry, or pet policies affect pricing? The more granular your research, the more accurate your limit will be.

Once you’ve gathered data, analyze it critically. Look for patterns—are rents rising or falling? Are certain areas or property types in higher demand? For example, if you’re in a college town, studio apartments might command higher rents during the school year. Conversely, family-sized homes in suburban areas could have a different pricing dynamic. Compare your property’s features (location, size, condition, amenities) to similar listings. If your unit has recent renovations or is closer to public transit, you might justify a slightly higher rent. Conversely, if it lacks modern updates or is in a less desirable area, you may need to price competitively to attract tenants.

A common mistake is setting a rent limit based solely on what you *want* to charge, rather than what the market will bear. To avoid this, calculate a range rather than a fixed number. For instance, if comparable units in your area rent for $1,200 to $1,500, set your limit within that range based on your property’s unique selling points. This flexibility allows you to adjust pricing if you’re not getting interest or if demand surges. Additionally, consider seasonal fluctuations—rents often peak in spring and summer, so timing your listing can impact how aggressively you price.

Finally, don’t overlook the human element. Talk to local landlords or property managers to get insider insights. They might share information about tenant turnover, common complaints, or unadvertised trends that online data misses. For example, a landlord might tell you that tenants are willing to pay a premium for units with flexible lease terms or included utilities. Armed with this knowledge, you can fine-tune your rent limit to not only compete but also stand out in the local market. Research isn’t just a step—it’s the foundation of a rent limit that balances profitability with tenant appeal.

Quick Guide: Removing Your Rental Listing from Zillow Easily

You may want to see also

Explore related products

![]()

Budget Prioritization: Ensure rent leaves room for savings, utilities, and other expenses

A common rule of thumb suggests spending no more than 30% of your gross monthly income on rent. However, this guideline often overlooks the complexity of individual financial situations. For instance, a young professional earning $4,000 monthly might comfortably allocate $1,200 to rent, but if their student loan payments consume $500 and utilities average $200, that leaves only $2,100 for groceries, transportation, and savings. Suddenly, the 30% rule feels less secure. This highlights the need for a more nuanced approach to budgeting, one that prioritizes not just rent but the entire financial ecosystem.

Consider this scenario: a couple earning a combined $6,000 monthly aims to save for a down payment on a house within five years. If they adhere strictly to the 30% rule, their $1,800 rent could hinder their savings goal. Instead, they could cap rent at 25%, freeing up $1,500 for savings, utilities, and other expenses. By allocating $1,000 monthly to savings, they’d accumulate $60,000 in five years—a substantial down payment. This example underscores the importance of aligning rent limits with long-term financial goals, not just arbitrary percentages.

To effectively prioritize your budget, start by listing all fixed and variable expenses. Fixed costs like utilities, insurance, and subscriptions provide a baseline. Variable expenses, such as groceries and entertainment, require flexibility but should still be estimated. Once these are accounted for, subtract them from your monthly income. The remaining amount should cover rent while leaving a buffer for emergencies and savings. For example, if your post-expense income is $2,500, capping rent at $1,000 ensures $1,500 for savings and unexpected costs.

A cautionary note: underestimating utilities and other expenses can derail even the most carefully planned budget. For instance, a tenant who assumes $100 monthly for electricity might be shocked by a $200 winter bill. To avoid this, research average utility costs in your area and factor in seasonal fluctuations. Similarly, don’t neglect irregular expenses like car maintenance or medical bills. Setting aside 5–10% of your income for these can prevent rent from consuming funds meant for emergencies.

Ultimately, the ideal rent limit is one that integrates seamlessly into your broader financial strategy. It’s not about adhering to a one-size-fits-all rule but about creating a sustainable balance. For a single parent earning $3,000 monthly, a 20% rent limit ($600) might be more realistic, allowing room for childcare and savings. Conversely, a high-earning individual might allocate 35% to rent if it aligns with their lifestyle and goals. The key is intentionality—ensuring rent supports, rather than sabotages, your financial well-being.

Gatlinburg Wheelchair Rentals: Where to Find Accessible Options for Visitors

You may want to see also

Explore related products

![]()

Roommate Sharing: Split rent proportionally based on room size or amenities

In shared living arrangements, fairness in rent division is crucial for maintaining harmony. One effective method is to split rent proportionally based on room size or amenities. This approach ensures that each roommate pays a share that reflects the value of their living space. For instance, if one room is significantly larger or includes a private bathroom, the occupant should contribute more to the rent. This system prevents resentment and fosters a sense of equity among housemates.

To implement this method, start by measuring each room’s square footage and listing additional amenities like en-suite bathrooms, walk-in closets, or private balconies. Assign a value to each feature based on its perceived worth. For example, a private bathroom might add 15% to the base rent, while a larger room could increase the share by 10% per additional 50 square feet. Sum the total value of all rooms and amenities, then calculate each roommate’s share as a percentage of this total. This ensures a transparent and data-driven approach to rent splitting.

Consider a practical example: In a three-bedroom apartment with a total rent of $2,000, one room is 200 sq. ft. with a private bathroom, another is 150 sq. ft. with a shared bathroom, and the third is 120 sq. ft. with no additional amenities. The larger room might account for 40% of the total value, the medium room 35%, and the smallest room 25%. This would result in rent shares of $800, $700, and $500, respectively. This method aligns cost with the benefits each roommate receives.

However, proportional splitting isn’t without challenges. Roommates may disagree on the value of certain amenities or feel that subjective factors, like natural light or closet space, aren’t adequately considered. To mitigate this, involve all parties in the valuation process and use objective criteria whenever possible. For instance, use market rates for similar rooms or consult real estate listings to determine fair premiums for amenities. Document the agreement in writing to avoid future disputes.

Ultimately, splitting rent proportionally based on room size or amenities is a fair and logical solution for shared living. It requires initial effort to measure, value, and agree on terms but pays off in long-term roommate satisfaction. By aligning cost with space and benefits, this method ensures that everyone contributes equitably, reducing financial stress and fostering a positive living environment.

Renting Your Dream Shop: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Emergency Fund Impact: Keep rent low enough to maintain a 3-6 month emergency fund

A common rule of thumb suggests spending no more than 30% of your monthly income on rent. However, this guideline fails to account for the critical role of an emergency fund in financial stability. To maintain a 3-6 month emergency fund, consider capping rent at 25% of your take-home pay. This adjustment ensures that even after housing costs, you can allocate 10-15% of your income to savings, a realistic target for building and preserving a safety net.

Imagine earning $4,000 monthly after taxes. A 25% rent limit translates to $1,000, leaving $3,000 for other expenses and savings. Allocating $600 (15%) to an emergency fund allows you to save $3,600 in six months, meeting the minimum threshold. Conversely, a 30% rent allocation ($1,200) reduces savings to $400 monthly, requiring nine months to reach the same goal. This comparison highlights how a slightly lower rent percentage accelerates emergency fund growth.

Critics might argue that reducing rent expenditure limits housing options, particularly in high-cost areas. However, the trade-off is intentional: prioritizing financial resilience over immediate comfort. For instance, choosing a $900 studio over a $1,200 one-bedroom in a competitive market frees up $300 monthly, enabling faster emergency fund accumulation. This strategic decision aligns with the principle that housing should support, not hinder, long-term financial security.

To implement this approach, start by calculating your monthly emergency fund target (e.g., $3,000 for three months at $1,000/month). Reverse-engineer your budget: subtract this savings goal and essential expenses (groceries, utilities) from your income, then allocate the remaining amount to rent. For example, if $2,000 covers essentials and savings, a $4,000 income allows for a $2,000 rent maximum—though sticking to $1,000 (25%) ensures a buffer for unexpected costs.

Ultimately, keeping rent low enough to sustain a 3-6 month emergency fund is less about frugality and more about strategic financial planning. It requires balancing current lifestyle preferences with future stability. By adopting the 25% rent rule and prioritizing savings, individuals can build a robust financial foundation capable of withstanding emergencies without derailing long-term goals. This disciplined approach transforms rent from a mere expense into a tool for achieving financial resilience.

Reporting Rental Income: A Step-by-Step Guide for Tax Returns

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent to ensure financial stability.

Consider your monthly income, essential expenses (utilities, groceries, transportation), savings goals, and any debts or financial obligations.

While it may be necessary in high-cost areas, exceeding 30% increases financial strain. Aim to balance rent with other expenses and prioritize saving.

Yes, factor in utilities, internet, parking, and other housing-related expenses to get a realistic picture of your total housing costs.

Consider sharing housing, moving to a less expensive area, or increasing your income through side jobs or promotions to align with your budget.