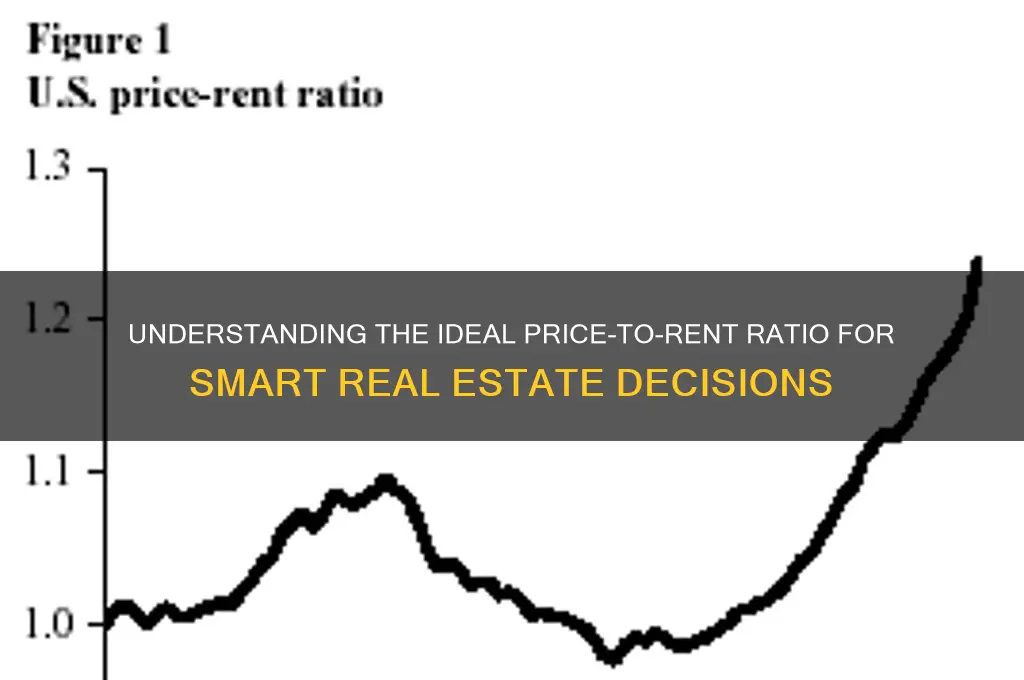

The price-to-rent ratio is a valuable metric used by real estate investors and analysts to assess whether it is more cost-effective to rent or buy a property in a given market. This ratio compares the purchase price of a home to the annual rental income it could generate, providing insight into the relative affordability and potential return on investment. A lower price-to-rent ratio typically indicates that renting is more economical, while a higher ratio suggests buying might be the better option. Understanding this ratio helps individuals make informed decisions about housing, balancing long-term financial goals with current market conditions.

Explore related products

What You'll Learn

![]()

Understanding Price-to-Rent Ratio Basics

The price-to-rent ratio, a key metric in real estate, compares the cost of buying a property to the cost of renting it. For instance, a ratio of 15 means that buying a home costs 15 times more than renting it annually. This figure is crucial for determining whether it’s more financially prudent to buy or rent in a given market. Historically, a ratio of 15 to 20 is considered balanced, but this varies by location and economic conditions. Understanding this baseline helps investors and homeowners gauge market trends and make informed decisions.

To calculate the price-to-rent ratio, divide the property’s purchase price by its annual rental income. For example, a $300,000 home that rents for $20,000 annually has a ratio of 15 ($300,000 / $20,000). This simple calculation provides a snapshot of affordability and investment potential. However, it’s essential to consider local factors like property taxes, maintenance costs, and rental demand, which can skew the ratio’s accuracy. Use this metric as a starting point, not the sole determinant of value.

A low price-to-rent ratio (below 15) often indicates a buyer’s market, where purchasing may be more advantageous than renting. Conversely, a high ratio (above 20) suggests renting could be the better option. For example, in cities like San Francisco or New York, ratios frequently exceed 30 due to high home prices and limited inventory, making renting more appealing. Compare these figures across regions to identify undervalued or overvalued markets and align your strategy accordingly.

While the price-to-rent ratio is a valuable tool, it’s not without limitations. It doesn’t account for long-term appreciation, mortgage interest rates, or personal financial goals. For instance, buying may still be preferable for those seeking stability or equity building, even in high-ratio markets. Pair this metric with other analyses, such as cash flow projections or local economic forecasts, to create a comprehensive evaluation. Practical tip: Track ratios over time to spot emerging trends and adjust your approach proactively.

Understanding Bond Appearance for Unpaid Rent: Legal Process Explained

You may want to see also

Explore related products

![]()

Calculating the Ratio Effectively

A good price-to-rent ratio is a critical metric for real estate investors and homeowners alike, but its calculation is often oversimplified. To determine this ratio effectively, start by understanding its core components: the property’s purchase price and its annual rental income. The formula is straightforward—divide the property’s market value by its yearly rental revenue. For instance, a $200,000 home that rents for $16,000 annually yields a ratio of 12.5. However, accuracy hinges on using *current* market data, not historical prices or inflated rental estimates. Always source property values from recent sales or appraisals and rental figures from active listings or local market reports.

While the formula is simple, pitfalls abound. One common mistake is neglecting vacancy rates or maintenance costs, which can skew the ratio. For a more realistic calculation, adjust the annual rental income to reflect net earnings after expenses. Assume a 5–10% vacancy rate and factor in repairs, property management fees, and taxes. For example, if a $1,500 monthly rent drops to $1,300 after deductions, the annual income becomes $15,600 instead of $18,000, significantly altering the ratio. This adjusted approach provides a clearer picture of the property’s true performance.

Comparative analysis is another layer of effectiveness. A ratio of 15 might seem high in one market but average in another. Benchmark your result against local averages or similar properties. Tools like the Federal Housing Finance Agency’s price-to-rent ratio data offer regional insights, while platforms like Zillow provide neighborhood-specific trends. For instance, a ratio of 20 in San Francisco may align with market norms, whereas the same figure in Indianapolis could signal overvaluation. Contextualizing your calculation ensures it’s not just mathematically correct but also market-relevant.

Finally, leverage the ratio as a decision-making tool, not a standalone metric. A low ratio (e.g., 10–12) often indicates a favorable buying opportunity, suggesting the property’s rental income aligns well with its price. Conversely, a high ratio (e.g., 20+) may signal an overpriced market or a poor investment for long-term rental income. Pair this analysis with other factors like cash flow projections, local economic growth, and property appreciation potential. For instance, a high ratio in a rapidly growing city might still be worthwhile if future demand is expected to drive rents upward. Calculating the ratio effectively isn’t just about crunching numbers—it’s about interpreting them within a broader financial and market context.

Assessing Rental Demand: Strategies to Measure Local Market Needs

You may want to see also

Explore related products

![]()

Ideal Ratio for Investments

A good price-to-rent ratio typically falls between 15 and 20, though this range can vary by market. This metric, calculated by dividing a property’s purchase price by its annual rental income, serves as a benchmark for comparing real estate investments across locations. For instance, a ratio of 15 suggests that the property’s price is equivalent to 15 years of rent, often considered a balanced entry point for investors. However, this ideal ratio isn’t universal—it hinges on factors like local demand, economic growth, and property appreciation potential.

To determine the ideal ratio for your investment, start by analyzing the market’s historical trends. In high-demand urban areas like San Francisco or New York, ratios often exceed 25, reflecting inflated property prices relative to rent. Conversely, smaller markets like Indianapolis or Memphis may hover around 10, signaling more affordable entry points. Cross-reference these figures with vacancy rates and rental yield projections to gauge sustainability. For example, a ratio of 18 in a market with 3% vacancy and 4% annual rent growth could outperform a ratio of 12 in a stagnant economy.

Investors should also consider their exit strategy when evaluating ratios. If the goal is long-term appreciation, a higher ratio might be justified in markets with strong economic indicators. However, for cash flow-focused investors, lower ratios (12–16) in stable, high-yield areas are preferable. A practical tip: use the 1% rule as a quick filter—a property priced at $200,000 should ideally rent for $2,000/month, yielding a ratio of 12.5. While not foolproof, this rule highlights alignment between price and rental income.

Caution is warranted when ratios deviate significantly from the norm. A ratio below 10 might indicate undervalued properties but could also signal declining neighborhoods or hidden costs. Conversely, ratios above 25 often point to overpriced markets, where rental income may struggle to cover expenses. To mitigate risk, stress-test your investment by modeling scenarios with 5–10% rent increases and 3–5% property value appreciation. If the ratio remains favorable under these conditions, the investment is likely resilient.

Ultimately, the ideal price-to-rent ratio is a tool, not a rule. It should complement other metrics like cap rates, cash-on-cash returns, and local economic health. For instance, a ratio of 16 in a growing market with low unemployment may outperform a ratio of 14 in a declining area. Tailor your approach by prioritizing ratios that align with your investment horizon, risk tolerance, and market dynamics. By blending data-driven analysis with strategic foresight, you can identify ratios that maximize returns while minimizing exposure to volatility.

Renting a BMW 750iL in Florida: Ultimate Luxury Guide

You may want to see also

Explore related products

![]()

Regional Variations in Ratios

Regional disparities in price-to-rent ratios reveal a complex interplay of economic, demographic, and geographic factors. For instance, in high-demand urban centers like San Francisco or New York, ratios often exceed 30:1, indicating a skewed market where purchasing is significantly more expensive than renting. Conversely, in smaller cities or rural areas, ratios may dip below 15:1, reflecting lower property values and more affordable housing options. These variations underscore the importance of local context when evaluating investment potential or personal housing decisions.

Analyzing these ratios geographically highlights the impact of supply and demand dynamics. Coastal cities with limited land availability and high population density tend to exhibit higher ratios, as property prices outpace rental income potential. In contrast, inland regions with expanding housing stock and slower population growth often present more balanced ratios, making them attractive for both renters and buyers. Investors should consider these trends when diversifying portfolios, as regions with lower ratios may offer better long-term yields.

A persuasive argument for understanding regional variations lies in their predictive power for market shifts. For example, areas with rapidly rising price-to-rent ratios may signal an impending housing bubble, while declining ratios could indicate oversupply or economic stagnation. Prospective homeowners and investors alike can use these insights to time their entries or exits strategically. Monitoring regional trends through tools like the Federal Housing Finance Agency’s data can provide actionable intelligence for informed decision-making.

Comparatively, international markets further illustrate the diversity of price-to-rent ratios. In cities like Berlin or Tokyo, ratios hover around 20:1, influenced by stringent rent control policies and cultural preferences for renting. Meanwhile, in emerging markets such as Mumbai or São Paulo, ratios can fluctuate wildly due to economic volatility and urbanization pressures. These global examples emphasize the need to account for regional nuances, as one-size-fits-all approaches rarely apply in real estate analysis.

Practically, individuals can leverage regional ratio insights to optimize their housing strategies. For instance, in areas with high ratios, renting may be more financially prudent, while low-ratio regions could favor buying. A useful tip is to calculate the breakeven horizon—the number of years it takes for buying to become cheaper than renting—using local ratio data. Online calculators or consulting with a real estate analyst can simplify this process, ensuring decisions align with both personal finances and regional market conditions.

Consequences of Unpaid Rent: What Happens When You Move Out?

You may want to see also

Explore related products

![]()

Using Ratios for Buy vs. Rent Decisions

A good price-to-rent ratio, typically ranging between 15 and 20, serves as a benchmark for comparing the cost of buying versus renting a property. This ratio, calculated by dividing the home price by its annual rent, offers a snapshot of market conditions. For instance, a ratio of 15 suggests that buying is more financially sound, as the property price aligns with rental costs over time. However, ratios above 20 often indicate an overheated housing market, where renting may be the wiser choice. Understanding this metric is the first step in leveraging ratios for informed buy-vs.-rent decisions.

To use the price-to-rent ratio effectively, start by gathering local data. Compare the median home price in your area to the average annual rent for similar properties. For example, if the median home price is $300,000 and the annual rent is $20,000, the ratio is 15—a favorable number for buying. However, if the ratio climbs to 25, renting becomes more attractive. Pair this analysis with other factors, such as mortgage rates and property taxes, to build a comprehensive financial picture. Remember, a single ratio is a starting point, not the final answer.

Consider the 1% rule of thumb as a complementary tool. This rule suggests that a property’s monthly rent should be at least 1% of its purchase price. For a $200,000 home, the rent should be $2,000 or more to align with this guideline. While not a ratio, this rule reinforces the price-to-rent ratio’s insights. If both metrics point toward buying, the decision becomes clearer. Conversely, discrepancies between the two may signal a need for deeper analysis, such as evaluating long-term appreciation potential or maintenance costs.

One caution: ratios alone cannot account for personal circumstances. A price-to-rent ratio of 16 may favor buying, but if you plan to move in two years, transaction costs and limited equity growth could outweigh the benefits. Similarly, a ratio of 22 might discourage buying, but if you prioritize stability and plan to stay long-term, the investment could still pay off. Always factor in your financial goals, job stability, and lifestyle preferences alongside these metrics.

In conclusion, the price-to-rent ratio is a powerful tool for buy-vs.-rent decisions, but it’s most effective when paired with other analyses and personal considerations. Start with local data, apply complementary rules like the 1% guideline, and weigh your unique circumstances. By doing so, you’ll transform a simple ratio into a strategic framework for one of life’s biggest financial choices.

How to Watch Rent Live in the UK: A Complete Guide

You may want to see also

Frequently asked questions

A good price to rent ratio typically falls between 15 and 20. This means that if the price of a property is 15 to 20 times its annual rent, it is generally considered a balanced investment in terms of buying versus renting.

The price to rent ratio is calculated by dividing the price of a property by its annual rental income. For example, if a property costs $200,000 and rents for $1,500 per month ($18,000 annually), the ratio is $200,000 / $18,000 = 11.11.

The price to rent ratio helps investors determine whether buying a property is a better financial decision than renting. A lower ratio suggests buying might be more advantageous, while a higher ratio indicates renting could be more cost-effective.

Yes, a good price to rent ratio can vary significantly by location due to differences in property prices, rental demand, and local market conditions. Urban areas with high property prices and lower rents may have higher ratios, while suburban or rural areas might have lower ratios.