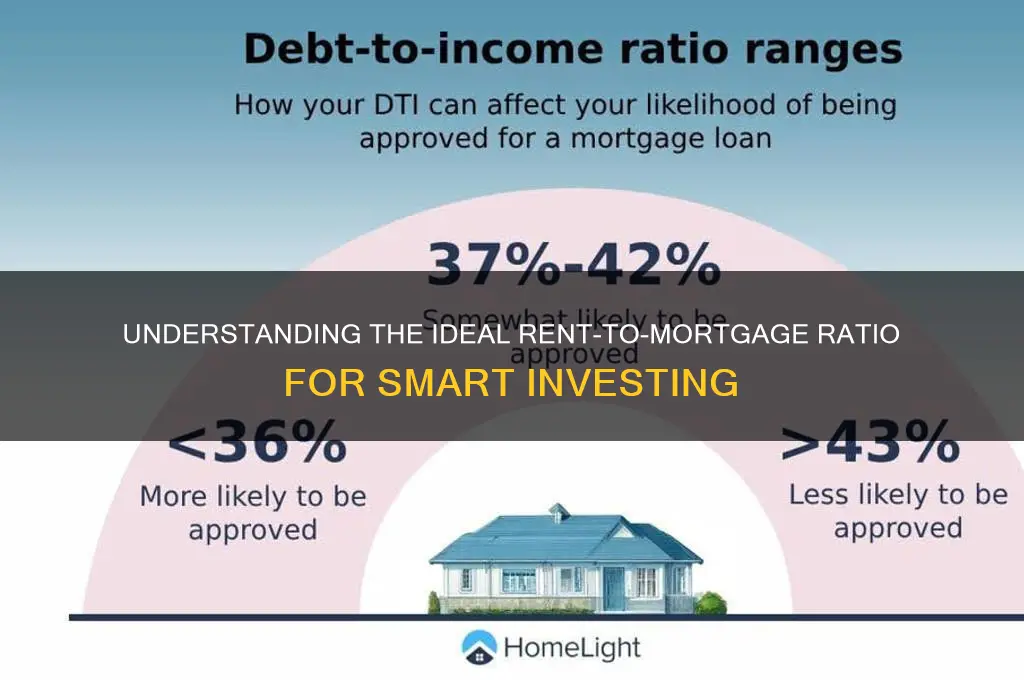

The rent-to-mortgage ratio is a critical metric used by real estate investors and homeowners to assess the financial viability of a rental property. It compares the potential rental income of a property to its monthly mortgage payment, providing insight into whether the property can generate enough cash flow to cover expenses and yield a profit. A good rent-to-mortgage ratio typically falls between 1.2 and 1.5, meaning the monthly rent is 20% to 50% higher than the mortgage payment. This ensures that the property not only covers its costs but also contributes to long-term financial goals, making it a key consideration for anyone looking to invest in rental real estate.

Explore related products

What You'll Learn

![]()

Ideal Rent-to-Mortgage Ratio

A commonly cited benchmark for the ideal rent-to-mortgage ratio is 1.2 to 1.5, meaning the monthly rent should be 20% to 50% higher than the mortgage payment. This range is rooted in the principle that rental income should cover mortgage costs while leaving a buffer for maintenance, vacancies, and unexpected expenses. For instance, if a property’s mortgage is $1,000 per month, the ideal rent would fall between $1,200 and $1,500. This ratio ensures the property remains profitable without pricing out potential tenants. However, this benchmark isn’t one-size-fits-all; it depends on factors like local market conditions, property type, and operating costs.

To determine your ideal rent-to-mortgage ratio, follow these steps: 1. Calculate your total monthly mortgage payment, including principal, interest, taxes, and insurance (PITI). 2. Add estimated monthly expenses such as maintenance, property management fees, and repairs (typically 10% to 20% of the rent). 3. Set the rent to cover these costs while maintaining the desired ratio. For example, if your PITI is $1,200 and monthly expenses are $200, a 1.2 ratio would require rent of $1,680 (1.2 × $1,400). This method ensures financial viability while remaining competitive in the rental market.

Critics argue that a rigid rent-to-mortgage ratio overlooks critical variables like location, property appreciation, and tenant demand. In high-demand urban areas, landlords can often command higher rents, pushing the ratio above 1.5. Conversely, in rural or less desirable markets, a ratio below 1.2 might be necessary to attract tenants. Additionally, long-term investors may prioritize cash flow over immediate profitability, accepting lower ratios in exchange for steady income and equity growth. Thus, while the 1.2 to 1.5 range is a useful starting point, it should be adjusted based on local dynamics and investment goals.

A persuasive case for maintaining a higher rent-to-mortgage ratio is its role in risk mitigation. A ratio of 1.5 or above provides a cushion during vacancies or unexpected repairs, ensuring the property remains cash-flow positive. For example, if a property with a $1,000 mortgage is rented for $1,500, a two-month vacancy would still allow the landlord to cover mortgage payments. This approach is particularly valuable for first-time investors or those with limited financial reserves. While it may mean leaving some rental income on the table, the added security can outweigh the opportunity cost.

Ultimately, the ideal rent-to-mortgage ratio is a balancing act between profitability and market competitiveness. Too high, and you risk prolonged vacancies; too low, and you may struggle to cover expenses. A practical tip is to research local rental rates and compare them to your mortgage and operating costs. Tools like rental market reports or real estate investment calculators can provide data-driven insights. By striking the right balance, you can maximize returns while minimizing risk, ensuring your investment remains both lucrative and sustainable.

Indiana Rent Increase Notice: Understanding Timelines for Tenants and Landlords

You may want to see also

Explore related products

![]()

Calculating Rent-to-Mortgage Ratio

A good rent-to-mortgage ratio is often cited as a key metric for landlords and real estate investors, but calculating it accurately requires a clear understanding of its components. At its core, the ratio compares the monthly rent you can charge against the monthly mortgage payment, expressed as a percentage. For instance, if your monthly mortgage payment is $1,200 and you charge $1,500 in rent, the ratio is 125% ($1,500 ÷ $1,200 × 100). This simple calculation provides a snapshot of potential cash flow, but it’s only the beginning of a deeper analysis.

To calculate the rent-to-mortgage ratio effectively, start by gathering precise figures. Include all components of the mortgage payment: principal, interest, property taxes, insurance, and any homeowner association fees. For rent, use the market rate for comparable properties in your area, not an inflated ideal. A common mistake is omitting additional costs or overestimating rental income, which skews the ratio and leads to unrealistic expectations. For example, if your mortgage payment is $1,000 but you fail to account for $200 in property taxes, your actual ratio will be lower than initially calculated.

While the ratio itself is straightforward, its interpretation varies by context. A ratio above 100% indicates positive cash flow, but experts often recommend aiming for at least 120–150% to account for vacancies, maintenance, and unexpected expenses. For instance, a property with a 125% ratio might seem profitable, but if 5% of the rent is lost to vacancies annually, the effective ratio drops to 119%. This highlights the importance of building a buffer into your calculations, especially in competitive rental markets.

One practical tip is to use the 1% rule as a quick benchmark: a property should rent for about 1% of its purchase price monthly. For a $200,000 home, this suggests a $2,000 rent. However, this rule is a starting point, not a definitive guide. Local market conditions, property condition, and tenant demand all influence the actual rent you can charge. Pairing the 1% rule with a detailed rent-to-mortgage ratio calculation provides a more nuanced understanding of a property’s potential.

Finally, consider the long-term implications of your ratio. A high rent-to-mortgage ratio is attractive, but it may not be sustainable if it prices out potential tenants or fails to cover future expenses. Conversely, a lower ratio might be acceptable if the property is in a high-appreciation area or if you plan to pay off the mortgage quickly. By combining precise calculations with strategic thinking, you can use the rent-to-mortgage ratio as a tool to make informed, profitable investment decisions.

Is Venmo a Reliable Choice for Receiving Rent Payments?

You may want to see also

Explore related products

![]()

Impact on Cash Flow

A rent-to-mortgage ratio below 80% is often considered ideal for landlords, ensuring positive cash flow after expenses. This metric, calculated by dividing monthly rent by mortgage payment, directly influences a property’s profitability. For instance, a $1,500 rent with a $1,000 mortgage yields a 150% ratio, leaving $500 for taxes, maintenance, and savings. Conversely, a 100% ratio means rent barely covers the mortgage, leaving no buffer for unexpected costs. This simple calculation is a critical tool for assessing whether an investment property will drain or enhance your financial stability.

Analyzing cash flow impact requires looking beyond the ratio itself. A 75% ratio might seem low, but if the property is in a high-demand area with consistent rent increases, it could still be a wise investment. Conversely, a 120% ratio in a volatile market may not sustain long-term profitability. For example, a landlord with a $2,000 mortgage might accept $2,500 rent (125% ratio) in a growing neighborhood, anticipating higher rents in 2–3 years. However, in a declining market, the same ratio could become risky if vacancy rates rise or maintenance costs spike. Context matters as much as the number.

To optimize cash flow, aim for a ratio that accounts for all expenses, not just the mortgage. A rule of thumb is to ensure rent covers 125–150% of total housing costs, including property taxes, insurance, and maintenance. For instance, if monthly expenses total $1,800, target $2,250–$2,700 in rent. This buffer allows for unforeseen repairs or vacancies without dipping into personal savings. Landlords should also factor in a 5–10% vacancy rate annually, adjusting rent expectations accordingly to maintain steady cash flow.

Persuasively, a conservative rent-to-mortgage ratio is a hedge against economic uncertainty. While a higher ratio maximizes short-term income, it leaves little room for error. For example, a landlord with a 90% ratio might struggle during a recession if tenants default or maintenance costs surge. In contrast, a 70% ratio provides resilience, ensuring cash flow even in downturns. This approach aligns with Warren Buffett’s principle of maintaining a margin of safety in investments. Prioritizing stability over immediate returns can safeguard long-term financial health.

Finally, consider the opportunity cost of a high rent-to-mortgage ratio. While a 150% ratio might seem attractive, it could indicate overpriced rent, leading to higher vacancy rates or tenant turnover. For instance, if comparable properties rent for $1,800 and yours is $2,200 (150% ratio), tenants may opt for cheaper options. Balancing competitiveness with profitability is key. A slightly lower ratio with consistent occupancy often outperforms a higher ratio with frequent vacancies. Practical tip: Research local rental trends and adjust pricing to stay within 10–15% of market rates while maintaining a healthy cash flow buffer.

Is Rental Income Taxable? Understanding Real Estate Earnings and Taxes

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

Industry Standards and Benchmarks

A commonly cited benchmark in the real estate industry is the 1% rule, which suggests that monthly rent should equal at least 1% of the property's purchase price. For instance, a $200,000 property should generate $2,000 in monthly rent to meet this standard. This rule serves as a quick litmus test for investors assessing the income potential of a rental property. However, it’s a broad guideline and may not account for regional market variations, property condition, or operating expenses. While useful for initial screening, it should be supplemented with more detailed analysis.

Industry professionals often refine the rent-to-mortgage ratio by incorporating debt service coverage ratio (DSCR), which measures a property’s ability to cover its mortgage payments. A DSCR of 1.25 or higher is typically considered healthy, meaning the property’s net operating income (NOI) is at least 25% greater than its mortgage payment. For example, if a mortgage payment is $1,200, the NOI should be at least $1,500. This metric is particularly valuable for lenders and investors, as it provides a buffer for unexpected expenses or vacancies.

Another benchmark gaining traction is the 50% rule, which posits that approximately half of a property’s gross income will be consumed by operating expenses (excluding mortgage payments). While not directly a rent-to-mortgage ratio, it helps contextualize what constitutes a "good" ratio by highlighting the importance of cash flow. For instance, if a property’s gross rent is $2,400, operating expenses are estimated at $1,200, leaving $1,200 for mortgage payments. This rule underscores the need to balance rental income with both fixed and variable costs.

Regional benchmarks also play a critical role in defining a good rent-to-mortgage ratio. In high-cost markets like San Francisco or New York, ratios may be lower due to inflated property values and competitive rental markets. Conversely, in more affordable areas like the Midwest, ratios tend to be higher, reflecting lower property costs and steady rental demand. Investors should consult local market data, such as average rent prices and median home values, to calibrate their expectations. Tools like the Zillow Rent Index or the U.S. Census Bureau’s American Community Survey can provide valuable insights.

Finally, while industry standards offer a framework, they are not one-size-fits-all. A practical approach is to stress-test your ratio by factoring in vacancy rates, maintenance costs, and potential rent increases. For example, if a property’s rent-to-mortgage ratio is 1.5 during full occupancy, calculate how it would fare with a 10% vacancy rate or a 5% increase in property taxes. This proactive analysis ensures that your ratio remains robust under various scenarios, aligning with long-term investment goals rather than short-term benchmarks.

Renting After School Starts: A Cost-Effective Housing Strategy?

You may want to see also

Explore related products

![]()

Adjusting for Market Conditions

Market conditions fluctuate, rendering static rent-to-mortgage ratios unreliable. A 1:1 ratio might be ideal in a balanced market, but in a seller’s market with soaring property values, landlords often charge premiums, pushing the ratio higher. Conversely, in a buyer’s market, lower property values and competitive rents can create a more favorable ratio for investors. Understanding these dynamics is crucial for both landlords and tenants to make informed decisions.

To adjust for market conditions, start by analyzing local vacancy rates. A vacancy rate below 4% indicates a tight rental market, where landlords can afford to set higher rents, potentially increasing the rent-to-mortgage ratio. Conversely, a vacancy rate above 7% suggests oversupply, forcing landlords to lower rents to attract tenants, thereby decreasing the ratio. Pair this data with median home prices and rental rates in your area for a clearer picture.

Next, consider the economic health of the region. In areas with strong job growth and population influx, demand for housing typically outpaces supply, driving up rents and property values. Here, a higher rent-to-mortgage ratio may be sustainable. In contrast, regions with declining industries or population exodus often see stagnant or falling rents, making it harder to maintain a favorable ratio. Use tools like the U.S. Bureau of Labor Statistics or local economic reports to gauge these trends.

Finally, factor in interest rates and financing costs. In a low-interest-rate environment, mortgage payments are lower, allowing landlords to accept a slightly lower rent-to-mortgage ratio while still achieving profitability. However, when interest rates rise, mortgage costs increase, necessitating higher rents to maintain the same ratio. For instance, a 1% increase in mortgage rates can reduce purchasing power by 10%, directly impacting the ratio. Monitor Federal Reserve announcements and consult with lenders to stay ahead of these shifts.

Practical tip: Use a dynamic rent-setting strategy. Instead of relying on a fixed ratio, adjust rents annually based on market conditions. For example, if your mortgage payment is $1,200 and the current market rent is $1,500, a 1.25:1 ratio is reasonable. However, if market rents rise to $1,700, consider increasing rent to $1,600 to maintain a buffer while staying competitive. Conversely, if market rents drop to $1,400, a $1,300 rent keeps the property occupied and cash flow positive. Flexibility is key in volatile markets.

Rent-to-Own TVs: Smart Investment or Costly Mistake?

You may want to see also

Frequently asked questions

The rent-to-mortgage ratio compares the monthly rent a property can generate to the monthly mortgage payment, expressed as a percentage. It helps investors assess the potential cash flow from a rental property.

A good rent-to-mortgage ratio typically ranges from 1.2 to 1.5 or higher, meaning the monthly rent is 20-50% higher than the mortgage payment. This ensures positive cash flow and covers expenses like maintenance and property taxes.

To calculate the ratio, divide the monthly rent by the monthly mortgage payment (including principal, interest, taxes, insurance, and HOA fees, if applicable). Multiply the result by 100 to express it as a percentage.

The ratio is crucial because it helps determine the profitability of a rental property. A higher ratio indicates better cash flow, while a lower ratio may suggest potential financial strain or insufficient income to cover expenses.