The concept of a livable income-to-rent ratio is crucial for understanding housing affordability and financial stability. This ratio compares an individual’s or household’s income to their monthly rent, typically expressed as a percentage, and is often used as a benchmark to determine whether housing costs are manageable. A widely accepted guideline suggests that rent should not exceed 30% of gross income to ensure sufficient funds for other essential expenses like food, healthcare, and savings. However, this threshold can vary based on factors such as location, cost of living, and personal financial goals. In high-cost urban areas, for instance, renters may spend significantly more than 30% of their income on housing, while in more affordable regions, the ratio may be lower. Understanding this balance is essential for both renters and policymakers to address housing affordability challenges and promote economic well-being.

| Characteristics | Values |

|---|---|

| Definition | The ratio of a household's income to its rent, indicating affordability. |

| Ideal Ratio | 30% or less of gross income spent on rent (widely accepted standard). |

| Livable Ratio | Below 30% is considered livable; above 30% indicates rent burden. |

| Average U.S. Rent-to-Income Ratio | ~27% (as of 2023, varies by location). |

| Minimum Wage Worker Ratio | Often exceeds 30%, e.g., ~50% in high-cost cities like NYC or San Francisco. |

| Impact on Affordability | Ratios above 30% reduce funds for essentials like food, healthcare, etc. |

| Global Perspective | Varies; e.g., Europe targets 25%, while some developing nations exceed 50%. |

| Policy Implications | Highlights need for affordable housing, rent control, or wage increases. |

| Latest Trend (2023) | Rising rents outpacing wage growth, worsening ratios in many U.S. cities. |

| Household Vulnerability | Low-income households are most affected, often spending >50% on rent. |

Explore related products

What You'll Learn

- Affordable Housing Standards: Defining income thresholds for rent affordability in different regions

- Rent Burden Calculation: How to determine if rent exceeds a livable income percentage

- Regional Cost Variations: Adjusting income-to-rent ratios based on local living expenses

- Policy Implications: Government roles in ensuring fair income-to-rent ratios for citizens

- Minimum Wage Alignment: Comparing minimum wages to livable income-to-rent benchmarks

![]()

Affordable Housing Standards: Defining income thresholds for rent affordability in different regions

The concept of a livable income-to-rent ratio is a cornerstone of affordable housing policies, yet its application varies dramatically across regions. In high-cost urban centers like San Francisco or New York, a widely accepted standard is the "30% rule," where rent should not exceed 30% of gross income. However, this metric falls short in lower-income areas where even 30% may be unsustainable. For instance, in rural Mississippi, where median incomes are significantly lower, a more realistic threshold might be 25% or less. This disparity underscores the need for region-specific income thresholds that account for local economic realities.

Defining these thresholds requires a multi-step approach. First, assess median incomes and rental costs for each region using data from sources like the U.S. Census Bureau or local housing authorities. For example, in Los Angeles, the median rent is $2,500, while the median household income is $67,000, suggesting a 45% rent-to-income ratio—far above the 30% standard. Second, factor in cost of living beyond housing, such as groceries, transportation, and healthcare, which can consume a larger share of income in certain areas. A family in Miami, for instance, might spend 15% of their income on transportation, leaving less for rent.

A persuasive argument for region-specific thresholds lies in their ability to address systemic inequities. In cities like Seattle, where tech industry growth has inflated housing costs, a one-size-fits-all approach exacerbates displacement of low-income residents. By setting a lower income-to-rent threshold—say, 28%—policymakers can prioritize affordability for vulnerable populations. Conversely, in shrinking cities like Detroit, where housing is relatively cheap but incomes are stagnant, a higher threshold (e.g., 35%) could encourage investment without burdening residents.

Practical implementation of these thresholds demands collaboration between governments, developers, and community organizations. For instance, inclusionary zoning policies can mandate that a percentage of new housing units meet the region’s affordability threshold. In Portland, Oregon, developers are required to allocate 20% of units to households earning 80% of the area median income, ensuring rent does not exceed 30% of their earnings. Similarly, rent control measures in cities like Berlin demonstrate how capping rent increases can maintain affordability in high-demand markets.

Ultimately, defining income thresholds for rent affordability is not a one-time task but an ongoing process. Economic shifts, population growth, and policy changes necessitate regular updates to these standards. For example, during the COVID-19 pandemic, many regions saw unemployment spike, prompting temporary reductions in acceptable rent-to-income ratios to prevent evictions. By adopting dynamic, region-specific thresholds, policymakers can ensure that affordable housing remains a reality, not just an ideal, for all residents.

We Don't Rent Pigs": Decoding the Meaning Behind the Phras

You may want to see also

Explore related products

$44.79 $55.99

![]()

Rent Burden Calculation: How to determine if rent exceeds a livable income percentage

A common rule of thumb suggests that rent should not exceed 30% of gross monthly income to maintain financial stability. This benchmark, often cited by housing experts and financial advisors, serves as a starting point for assessing rent burden. However, this percentage alone doesn’t account for regional cost-of-living variations, household size, or other financial obligations. For instance, a single earner in San Francisco may struggle even if rent is 30% of their income, while someone in a lower-cost area might manage comfortably at 35%. To determine if your rent exceeds a livable income percentage, you must first calculate your rent-to-income ratio and then contextualize it within your specific circumstances.

To calculate your rent burden, divide your monthly rent by your gross monthly income and multiply by 100 to get a percentage. For example, if your rent is $1,200 and your income is $4,000, the ratio is 30% ($1,200 ÷ $4,000 = 0.30). While this calculation is straightforward, it’s crucial to consider net income (after taxes and deductions) for a more accurate picture, especially if your take-home pay is significantly lower than your gross income. Additionally, factor in utilities and other housing-related expenses, as these can push the total housing cost beyond the rent alone. A ratio above 30% often indicates rent burden, but this threshold may need adjustment based on individual financial realities.

Rent burden isn’t just a number—it’s a predictor of financial stress and housing insecurity. Households spending more than 30% of their income on rent often struggle to cover other essentials like food, healthcare, and transportation. For low-income families or those with irregular earnings, even a 25% ratio can be unsustainable. Conversely, higher-income households might manage a 40% ratio without strain. The key is to evaluate your overall budget and prioritize savings, debt repayment, and emergency funds. If rent consumes a disproportionate share of your income, consider negotiating rent, seeking a roommate, or exploring housing assistance programs to alleviate the burden.

While the 30% rule is widely accepted, it’s not one-size-fits-all. Urban areas with high living costs may require a higher threshold, while rural regions might allow for a lower one. Households with multiple earners or substantial savings may tolerate higher ratios, whereas single-income families or those with debt may need to stay below 25%. To personalize your assessment, compare your rent-to-income ratio to local averages and evaluate your financial goals. Tools like budgeting apps or housing affordability calculators can provide additional insights. Ultimately, the goal is to ensure rent doesn’t compromise your ability to build financial security and maintain a decent quality of life.

Renting Your Building to Banks: A Comprehensive Guide for Landlords

You may want to see also

Explore related products

![]()

Regional Cost Variations: Adjusting income-to-rent ratios based on local living expenses

The concept of a livable income-to-rent ratio often assumes a one-size-fits-all approach, but this ignores the stark regional cost variations that can make a $1,500 rent burden in one city a bargain in another. For instance, in San Francisco, where the median rent for a one-bedroom apartment hovers around $3,700, a commonly recommended 30% income-to-rent ratio would require an annual salary of at least $148,000. Contrast this with Des Moines, Iowa, where the median rent is $900, and the same ratio demands just $36,000 annually. These disparities highlight the need for localized adjustments to ensure financial viability.

To effectively adjust income-to-rent ratios, start by analyzing the Cost of Living Index (COLI) for your region. This index compares the cost of goods and services, including housing, across different areas relative to a national average. For example, a COLI of 120 means living expenses are 20% higher than the national average. Pair this with the 50/30/20 budget rule, which allocates 50% of income to necessities (including rent), 30% to discretionary spending, and 20% to savings. In high-cost regions, consider raising the rent allocation to 35% or even 40% of income to reflect local realities, while in low-cost areas, aim for 25% to maximize savings.

Another practical step is to benchmark against local median incomes and rents rather than national averages. For instance, in New York City, where the median household income is $63,000 and median rent is $1,600, a 30% ratio is unrealistic. Instead, aim for a 40% ratio, requiring a $48,000 income, and supplement with roommate arrangements or subsidized housing programs. Conversely, in Tulsa, Oklahoma, where median rent is $850 and median income is $48,000, a 20% ratio is achievable, freeing up funds for other financial goals.

Caution must be exercised when applying these adjustments. Over-relying on national guidelines in high-cost regions can lead to financial strain, while underestimating expenses in low-cost areas can result in missed opportunities for wealth-building. For example, a young professional in Austin, Texas, might assume a 30% ratio is sufficient, but rapidly rising rents could quickly erode their budget. To mitigate this, build a 10–15% buffer into your rent allocation, especially in volatile markets, and regularly reassess your budget as local conditions evolve.

Ultimately, the key to a livable income-to-rent ratio lies in its adaptability to regional cost variations. By leveraging local data, adjusting budget allocations, and maintaining flexibility, individuals can navigate the complexities of housing affordability with greater confidence. Whether you’re in a high-cost metropolis or a low-cost rural area, tailoring your ratio to local realities ensures financial stability without sacrificing quality of life.

Renting Hourly Office Space in Durham, NC: A Quick Guide

You may want to see also

Explore related products

![]()

Policy Implications: Government roles in ensuring fair income-to-rent ratios for citizens

A livable income-to-rent ratio, typically defined as spending no more than 30% of gross income on housing, is a cornerstone of financial stability. However, skyrocketing rents and stagnant wages have pushed this ratio out of reach for millions. Governments, as stewards of societal well-being, must intervene to bridge this gap and ensure housing affordability for all citizens.

Here’s how:

Legislative Action: The Hammer of Policy

Governments possess the power to directly influence income-to-rent ratios through targeted legislation. Rent control policies, while controversial, can cap rent increases, preventing sudden spikes that outpace income growth. Consider Berlin’s 2020 rent freeze, which aimed to stabilize costs in a rapidly gentrifying city. While its long-term effectiveness is debated, it demonstrates the potential for bold legislative action. Additionally, inclusionary zoning laws can mandate a percentage of new developments be designated as affordable housing, directly increasing the supply of rent-controlled units.

Similarly, minimum wage laws need to be regularly reviewed and adjusted to reflect the true cost of living, including housing expenses. A $15 minimum wage might seem progressive, but in cities with median rents exceeding $2,000, it falls woefully short of achieving a livable income-to-rent ratio.

Incentivizing Solutions: Carrots Over Sticks

Beyond mandates, governments can incentivize both landlords and developers to contribute to affordable housing solutions. Tax breaks and subsidies for landlords who offer below-market rents can encourage participation in affordable housing programs. Similarly, density bonuses and expedited permitting processes can incentivize developers to include affordable units in their projects.

Investing in the Future: Building a Sustainable Solution

The most sustainable solution to the income-to-rent ratio crisis is a massive investment in public housing. Governments must commit to building and maintaining a robust stock of affordable housing units, ensuring long-term availability for low- and middle-income families. This requires significant upfront investment but pays dividends in social stability, reduced homelessness, and a healthier, more productive population.

Imagine a future where every citizen has access to safe, secure, and affordable housing, regardless of their income. This is not a utopian dream, but a achievable goal if governments prioritize fair income-to-rent ratios and take decisive action.

Renting Construction Security Cameras: A Comprehensive Guide for Site Safety

You may want to see also

Explore related products

![]()

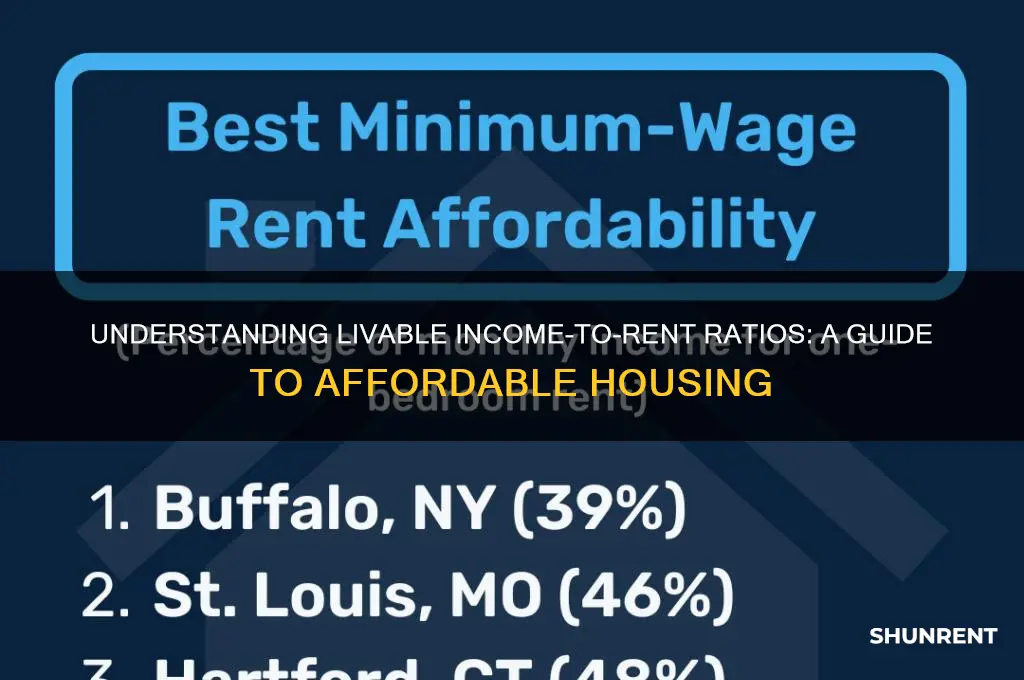

Minimum Wage Alignment: Comparing minimum wages to livable income-to-rent benchmarks

A livable income-to-rent ratio typically suggests that no more than 30% of a household’s gross income should be spent on housing. This benchmark, established by the U.S. Department of Housing and Urban Development (HUD), ensures financial stability by leaving room for other necessities like food, healthcare, and transportation. However, for minimum wage workers, this ratio often becomes unattainable. In states like Texas, where the minimum wage is $7.25 per hour, a full-time worker earns approximately $1,257 monthly before taxes. To meet the 30% threshold, rent should not exceed $377, yet the average one-bedroom rent in Texas is $1,100—nearly three times that amount. This disparity highlights the urgent need to align minimum wages with livable income-to-rent benchmarks.

Consider the steps required to bridge this gap. First, calculate the hourly wage needed to afford fair market rent without exceeding the 30% threshold. For a $1,100 apartment, a worker would need to earn at least $20.38 per hour, assuming full-time employment. Second, compare this to current minimum wages. In California, where the minimum wage is $15.50, a worker still falls short, needing $18.46 more per hour to afford the average $2,000 rent in Los Angeles. Third, advocate for policy changes that tie minimum wage increases to local housing costs, as seen in cities like Seattle, where wages are adjusted annually based on inflation and cost of living. These steps provide a roadmap for policymakers and advocates to address the affordability crisis.

Critics argue that raising minimum wages could burden small businesses, but the alternative—persistent housing insecurity—carries greater societal costs. For instance, in New York City, where the minimum wage is $15, a worker would need to earn $34.88 per hour to afford the average $1,900 rent. This mismatch forces low-wage earners into overcrowded or substandard housing, increasing healthcare costs and reducing productivity. A persuasive counterargument is that aligning wages with livable rent benchmarks stimulates local economies, as workers have more disposable income to spend on goods and services. Studies from the Economic Policy Institute show that wage increases in cities like Chicago led to higher consumer spending without significant job losses.

Descriptive examples further illustrate the challenge. In Phoenix, Arizona, a minimum wage worker earning $12.80 per hour can afford rent of $384, yet the average rent is $1,300. This forces many to work multiple jobs or rely on public assistance, perpetuating cycles of poverty. Conversely, in Minneapolis, where the minimum wage is $15.57, workers can afford $467 in rent, closer to the $1,200 average but still insufficient. These scenarios underscore the need for localized solutions, such as rent control or housing subsidies, paired with wage increases. Without such measures, the gap between minimum wages and livable rent ratios will continue to widen, leaving millions unable to secure stable housing.

In conclusion, aligning minimum wages with livable income-to-rent benchmarks requires a multi-faceted approach. Policymakers must calculate fair wages based on local housing costs, advocate for annual adjustments, and implement complementary measures like rent control. While challenges exist, the economic and social benefits of ensuring housing affordability far outweigh the costs. By addressing this disparity, we can create a more equitable society where work truly pays enough to live.

Mastering Rent Payments: A Step-by-Step Guide to Writing Checks

You may want to see also

Frequently asked questions

A livable income to rent ratio is a financial metric used to determine the affordability of housing based on an individual's or household's income. It is typically expressed as a percentage, representing the proportion of gross income that goes toward paying rent.

A widely accepted guideline is that a healthy income to rent ratio should not exceed 30%. This means that an individual or household should aim to spend no more than 30% of their gross income on rent to maintain a livable and financially stable situation.

To calculate your income to rent ratio, divide your monthly rent by your gross monthly income, then multiply the result by 100 to express it as a percentage. For example, if your monthly rent is $1,200 and your gross monthly income is $4,000, your income to rent ratio would be (1,200 / 4,000) x 100 = 30%.