Grapi Gross Rent as a Percentage of Income (GRAPI) is a financial metric used to assess the affordability of housing relative to an individual's or household's income. It calculates the proportion of gross income that is allocated to rent, providing insight into the financial burden of housing costs. Typically expressed as a percentage, GRAPI helps policymakers, lenders, and renters evaluate whether housing expenses are sustainable or if they pose a risk of financial strain. A lower GRAPI indicates greater affordability, while a higher percentage suggests that a significant portion of income is being spent on rent, potentially leaving less for other essential expenses. Understanding GRAPI is crucial for making informed decisions about housing, budgeting, and economic planning.

Explore related products

What You'll Learn

![]()

Understanding GRAPI Calculation

GRAPI, or Gross Rent as a Percentage of Income, is a critical metric for assessing housing affordability. It measures the proportion of a household’s pre-tax income allocated to rent, offering a snapshot of financial strain. To calculate GRAPI, divide the annual gross rent by the household’s annual gross income, then multiply by 100. For example, if a tenant pays $12,000 in rent annually and earns $60,000, their GRAPI is 20%. This calculation is straightforward but reveals much about a household’s economic stability. A GRAPI above 30% is generally considered a burden, signaling that housing costs may be unsustainable relative to income.

While the formula is simple, its application requires nuance. For instance, gross income includes wages, salaries, and other pre-tax earnings, but excludes deductions like taxes or retirement contributions. Similarly, gross rent encompasses all housing costs paid to the landlord, including utilities if applicable. Misinterpreting these components can skew results. For example, a household earning $50,000 annually with a $10,000 rent might appear to have a 20% GRAPI, but if utilities add $2,000, the actual GRAPI rises to 24%. Precision in input values is essential for accurate analysis.

GRAPI’s utility extends beyond individual households to broader policy and market analysis. Urban planners and policymakers use it to identify affordability gaps in specific regions or demographics. For instance, a study might reveal that renters aged 25–34 in metropolitan areas have an average GRAPI of 40%, highlighting systemic issues like wage stagnation or rising rents. Conversely, landlords and investors can use GRAPI to assess tenant risk or market demand. A neighborhood with an average GRAPI of 25% may be more stable than one at 35%, guiding investment decisions.

However, GRAPI is not without limitations. It fails to account for non-housing expenses, such as healthcare or childcare, which can significantly impact overall affordability. A household with a 28% GRAPI might still struggle if other costs consume 50% of their income. Additionally, GRAPI does not differentiate between temporary financial strain and chronic affordability issues. A recent graduate with a high GRAPI may expect income growth, while a retiree on a fixed income faces a more permanent challenge. Contextualizing GRAPI with other financial metrics provides a fuller picture.

To maximize the utility of GRAPI, consider it as part of a broader affordability toolkit. For individuals, tracking GRAPI annually can highlight trends in housing affordability relative to income growth. Pairing it with a budget analysis ensures a comprehensive view of financial health. For professionals, combining GRAPI with metrics like the Housing Affordability Index or median income-to-rent ratios offers deeper insights into market dynamics. By understanding GRAPI’s strengths and limitations, users can leverage it effectively to make informed decisions, whether managing personal finances or shaping housing policy.

Unlock Rent Assistance: Your Guide to Qualifying at The River Fund

You may want to see also

Explore related products

![]()

Impact on Housing Affordability

The Gross Rent as a Percentage of Income (GRAPI) metric is a critical indicator of housing affordability, revealing how much of a household's income is consumed by rent. When GRAPI exceeds 30%, households are considered cost-burdened, often forcing trade-offs between housing and essentials like food, healthcare, and education. This threshold, established by the U.S. Department of Housing and Urban Development (HUD), highlights the precarious balance many families face in maintaining stable housing.

Consider a single-income household earning $40,000 annually. If their monthly rent is $1,200, their GRAPI is 36%—well above the affordability threshold. This scenario illustrates how even modest rent increases can push households into financial instability. For low-income families, the impact is more severe; a GRAPI of 50% or higher is not uncommon, leaving little room for savings or unexpected expenses. This financial strain perpetuates cycles of poverty and limits opportunities for upward mobility.

To mitigate the impact of high GRAPI on housing affordability, policymakers and advocates often propose rent control measures, housing subsidies, or incentives for affordable housing development. For instance, the Housing Choice Voucher Program (Section 8) caps rent payments at 30% of a household's income, providing relief to millions of low-income families. However, such programs are often underfunded and inaccessible to those who need them most. Additionally, zoning reforms that allow for denser, mixed-income housing can increase supply and reduce rent burdens in high-demand areas.

A comparative analysis of urban and rural areas reveals stark disparities in GRAPI. In cities like San Francisco or New York, where median rents exceed $3,000, even middle-income households struggle to stay below the 30% threshold. In contrast, rural areas often have lower housing costs but limited job opportunities, creating a different set of affordability challenges. This urban-rural divide underscores the need for region-specific solutions, such as rural housing preservation programs or urban rent stabilization policies.

Ultimately, addressing the impact of GRAPI on housing affordability requires a multi-faceted approach. Individuals can benefit from budgeting tools and financial literacy programs to manage housing costs effectively. Communities must advocate for policies that balance housing supply and demand, while governments should invest in affordable housing initiatives and expand access to subsidies. By lowering GRAPI, we can reduce housing insecurity and create more equitable opportunities for all.

Sell Up or Stay Put? Renting vs. Owning in Retirement

You may want to see also

Explore related products

![]()

GRAPI vs. Income Ratios

The Gross Rent as a Percentage of Income (GRAPI) is a critical metric for assessing housing affordability, but it’s often misunderstood when compared to broader income ratios. While both GRAPI and income ratios measure financial burden, they serve distinct purposes. GRAPI specifically focuses on the proportion of income spent on rent, making it a targeted tool for evaluating housing costs. In contrast, income ratios, such as debt-to-income (DTI) or housing expense-to-income ratios, encompass a wider range of financial obligations. For instance, a DTI ratio includes debts like loans and credit card payments, whereas GRAPI isolates rent, providing a clearer picture of housing affordability in isolation.

To calculate GRAPI, divide the annual gross rent by the annual household income and multiply by 100. For example, if a tenant pays $12,000 in rent annually and earns $60,000, their GRAPI is 20%. This calculation is straightforward but powerful, as it highlights whether housing costs are sustainable relative to income. Experts generally recommend a GRAPI of 30% or less, though this threshold can vary based on local cost of living and household size. For instance, a single-income family in a high-cost urban area may struggle even at 25%, while a dual-income household in a rural area might manage comfortably at 35%.

One key advantage of GRAPI over broader income ratios is its specificity. Income ratios can dilute the impact of housing costs by lumping them with other expenses, making it harder to pinpoint affordability issues. For policymakers, GRAPI offers a focused lens to identify housing crises and allocate resources effectively. For renters, it’s a practical tool to assess whether their housing choices align with their financial health. However, GRAPI isn’t without limitations. It doesn’t account for utilities, maintenance, or other housing-related expenses, which can significantly affect overall affordability.

When comparing GRAPI to income ratios, consider the context. For individuals with minimal debt, GRAPI may be a more accurate affordability indicator. Conversely, those with substantial non-housing debts might find income ratios more relevant. For instance, a renter with student loans and car payments may have a DTI of 40%, but a GRAPI of 25%, suggesting housing itself isn’t the primary financial strain. In such cases, addressing debt rather than rent might be the priority.

In practice, combining GRAPI with income ratios provides a comprehensive financial assessment. Renters should calculate both metrics to understand their overall financial health and identify areas for improvement. For example, if GRAPI is high but the DTI is low, negotiating rent or seeking a more affordable unit could be the solution. Conversely, if both ratios are high, reducing non-housing expenses or increasing income might be necessary. By leveraging both tools, individuals and policymakers can make informed decisions to improve housing affordability and financial stability.

Navigating Airbnb Legalities in Atlanta: Hotel Permits Explained

You may want to see also

Explore related products

![]()

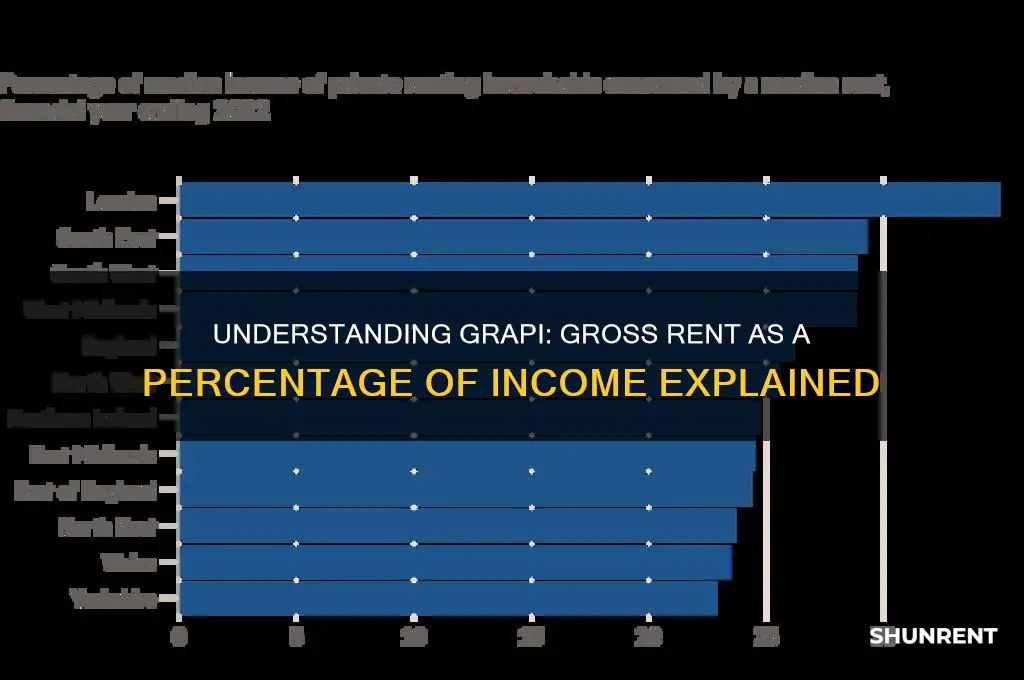

Regional GRAPI Variations

Regional variations in GRAPI (Gross Rent as a Percentage of Income) reveal stark disparities in housing affordability across different areas, often driven by local economic conditions, housing supply, and demographic factors. For instance, urban centers like San Francisco and New York City consistently report GRAPI values exceeding 40%, meaning residents spend nearly half their income on rent. In contrast, rural areas in the Midwest or South often see GRAPI figures below 25%, reflecting lower housing costs and cost of living. These differences highlight the uneven financial burden renters face depending on their location.

Analyzing these variations requires examining both income levels and rental prices. In high-GRAPI regions, wages often fail to keep pace with skyrocketing rents, leaving households vulnerable to housing insecurity. For example, in Los Angeles, the median rent is over $2,500 per month, while the median household income hovers around $65,000 annually. This imbalance forces many residents to allocate a disproportionate share of their earnings to housing, limiting their ability to save or invest in other essentials. Policymakers in such areas must prioritize increasing affordable housing stock and boosting local wages to mitigate this strain.

Conversely, low-GRAPI regions offer insights into sustainable housing models. In cities like Indianapolis or Memphis, where GRAPI averages around 20%, a combination of lower housing demand and higher vacancy rates keeps rents affordable. However, these areas often struggle with economic growth and job opportunities, creating a trade-off between housing affordability and economic prosperity. Renters in these regions may benefit from lower housing costs but face challenges in career advancement or access to amenities. Balancing affordability with economic development is key to maintaining healthy GRAPI levels in such areas.

Practical steps for addressing regional GRAPI disparities include targeted interventions tailored to local contexts. In high-cost cities, implementing rent control policies, expanding housing subsidies, and incentivizing developers to build affordable units can help reduce GRAPI. For low-income regions, investing in infrastructure, education, and job creation can stimulate economic growth while preserving housing affordability. Additionally, renters can mitigate their GRAPI burden by exploring shared housing arrangements, negotiating lease terms, or relocating to areas with lower costs. Understanding these regional nuances is essential for crafting effective solutions to the housing affordability crisis.

Writing a Rent Check with Chase Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Policy Implications of High GRAPI

High GRAPI (Gross Rent as a Percentage of Income) indicates that households are spending a disproportionate amount of their earnings on housing, often exceeding the affordability threshold of 30% recommended by the U.S. Department of Housing and Urban Development (HUD). For example, in cities like San Francisco or New York, GRAPI can soar above 50% for low- to middle-income families, leaving little room for other essentials like healthcare, education, or savings. This financial strain has cascading effects on both individuals and communities, necessitating targeted policy interventions.

Step 1: Expand Housing Supply Through Incentives

Policymakers must address the root cause of high GRAPI—housing scarcity—by incentivizing developers to build affordable units. Tax credits, density bonuses, and streamlined permitting processes can reduce construction costs, making it feasible to offer lower rents. For instance, the Low-Income Housing Tax Credit (LIHTC) program has successfully funded over 3 million affordable units since 1986. Pairing such incentives with mandates for mixed-income developments ensures that new supply benefits a broader demographic, not just high-income earners.

Caution: Avoid Gentrification Pitfalls

While increasing supply is critical, policies must guard against gentrification, which often displaces the very populations they aim to help. Rent control, while controversial, can stabilize costs in high-demand areas, but it must be paired with anti-displacement measures like tenant relocation assistance or community land trusts. For example, Minneapolis’s 2021 rent control ordinance caps annual rent increases at 3%, providing predictability for tenants without stifling development.

Analysis: Targeted Subsidies for Vulnerable Populations

High GRAPI disproportionately affects seniors, low-wage workers, and single-parent households. Direct subsidies, such as Housing Choice Vouchers, can bridge the affordability gap, but their effectiveness hinges on funding levels and landlord participation. Expanding eligibility criteria and increasing voucher amounts to match local market rents could alleviate immediate burdens. For instance, a 2021 study found that households using vouchers had a median GRAPI of 24%, compared to 47% for eligible non-recipients.

Addressing high GRAPI requires a holistic approach that links housing affordability to economic mobility, public health, and education. Policies like rent-to-own programs or down payment assistance can help renters transition to homeownership, building wealth over time. Simultaneously, investing in public transportation and remote work infrastructure can reduce the need to live in high-cost urban centers. By treating housing as a cornerstone of social policy, governments can mitigate the systemic impacts of high GRAPI and foster more equitable communities.

Renting an RV in Los Angeles: Your Ultimate Guide to Adventure

You may want to see also

Frequently asked questions

GRAPI is a financial metric that calculates the percentage of a household's gross income spent on rent, including utilities, before taxes or deductions.

GRAPI is calculated by dividing the household's gross annual rent by its gross annual income, then multiplying by 100 to get the percentage.

A GRAPI ratio of 30% or less is generally considered affordable, as it aligns with the U.S. Department of Housing and Urban Development's (HUD) affordability standard.

GRAPI helps renters assess housing affordability and ensures they are not overburdened by rent. Landlords use it to evaluate tenant financial stability and set competitive rental rates.

GRAPI uses gross income and rent (including utilities), while net rent as a percentage of income considers after-tax income and may exclude utilities, providing a different affordability perspective.