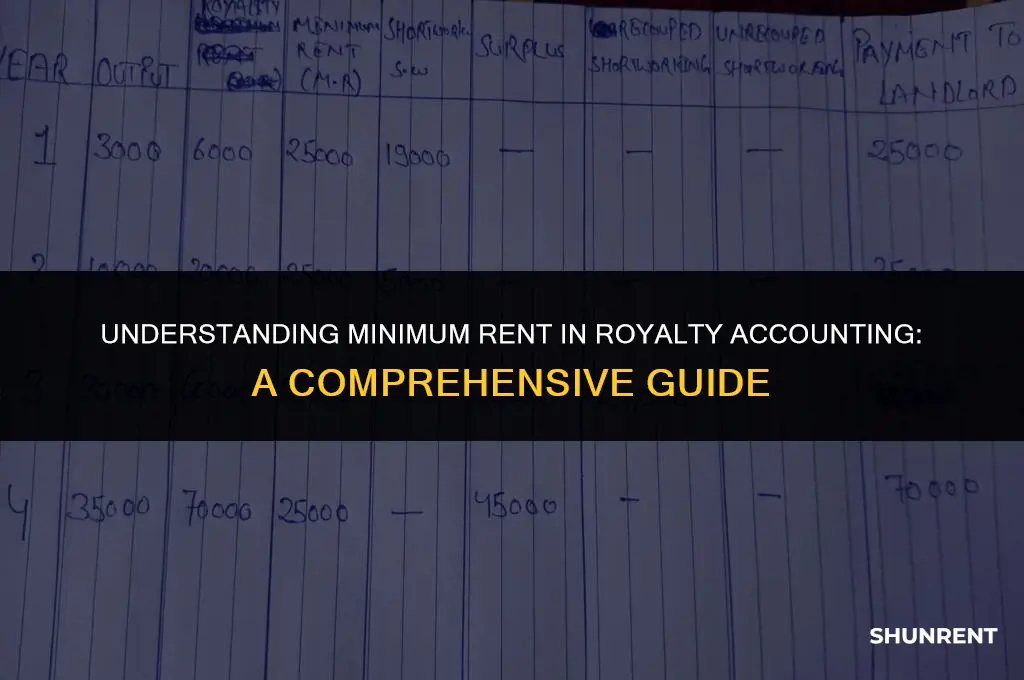

Minimum rent in royalty accounting refers to the predetermined minimum amount that a lessor must receive from a lessee, regardless of the actual sales or profits generated by the leased property. This concept is crucial in ensuring that the lessor receives a fair return on their investment, even if the lessee's business does not perform as expected. The minimum rent is typically negotiated and agreed upon in the lease agreement, and it can be a fixed amount or a percentage of the property's value. In some cases, the minimum rent may be adjusted periodically to reflect changes in market conditions or inflation. Understanding the implications of minimum rent is essential for both lessors and lessees, as it can significantly impact the financial viability of a business venture.

| Characteristics | Values |

|---|---|

| Definition | The minimum amount of royalty payment due to the copyright holder, regardless of the actual sales or revenue generated. |

| Purpose | Ensures that the copyright holder receives a fair and consistent income from the use of their intellectual property. |

| Calculation | Typically calculated as a percentage of the retail price or revenue generated from the sale of the copyrighted material. |

| Industry Standard | Varies by industry, but common rates include 5-10% for music, 10-15% for publishing, and 5-7% for film and television. |

| Payment Frequency | Usually paid quarterly or annually, depending on the agreement between the parties involved. |

| Minimum Threshold | Often subject to a minimum threshold, where no payment is due until the revenue generated exceeds a certain amount. |

| Audit and Compliance | Subject to audit and compliance requirements to ensure accurate reporting and payment of royalties. |

| Legal Requirements | Governed by copyright laws and regulations, which vary by country and jurisdiction. |

Explore related products

What You'll Learn

![]()

Definition of Minimum Rent

Minimum rent in royalty accounting refers to a predetermined fixed payment that a lessee must pay to a lessor, regardless of the actual sales or profits generated from the leased property. This concept is crucial in lease agreements, particularly in the context of commercial real estate and intellectual property licensing. The minimum rent serves as a financial safeguard for the lessor, ensuring a steady income stream even if the lessee's business does not perform as expected.

In the realm of commercial real estate, minimum rent is often calculated based on the fair market value of the property, taking into account factors such as location, size, and amenities. For instance, if a retail store leases a space in a prime shopping center, the minimum rent would likely be higher than that of a similar space in a less desirable location. This is because the lessor assumes a higher risk by leasing to a business that may not generate sufficient revenue to cover the rent.

In intellectual property licensing, minimum rent can be determined by the perceived value of the licensed property, such as a patent, trademark, or copyright. For example, a pharmaceutical company licensing a patent for a blockbuster drug would likely agree to a higher minimum rent than a small business licensing a less valuable trademark. This is because the pharmaceutical company has a greater potential to generate significant profits from the licensed property, and the lessor seeks to share in that potential upside.

Minimum rent agreements can also include provisions for rent escalation, where the rent increases over time based on a predetermined formula, such as a percentage increase or a consumer price index (CPI) adjustment. This helps to protect the lessor from inflation and ensures that the rent remains fair and competitive over the course of the lease.

In conclusion, minimum rent is a critical component of lease agreements, providing financial security for lessors and incentivizing lessees to maximize their use of the leased property. By understanding the factors that influence minimum rent calculations and the various provisions that can be included in a lease agreement, both lessors and lessees can negotiate terms that are mutually beneficial and aligned with their business objectives.

Renting the George Brett Suite at Kauffman Stadium: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Types of Minimum Rent

Minimum rent in royalty accounting refers to the guaranteed payment a licensor receives from a licensee, regardless of the licensee's sales or profits. This payment serves as a form of financial security for the licensor, ensuring they receive a minimum income from the licensing agreement. There are several types of minimum rent, each with its own unique characteristics and implications for both parties involved.

One type of minimum rent is the fixed minimum rent, which is a predetermined amount agreed upon by both parties. This amount is paid periodically, such as monthly or quarterly, and does not fluctuate based on the licensee's performance. Fixed minimum rent provides a stable income stream for the licensor but may not be as lucrative if the licensee's sales exceed expectations.

Another type is the sliding scale minimum rent, which adjusts based on the licensee's sales or profits. This type of minimum rent typically starts at a lower amount and increases as the licensee's performance improves. Sliding scale minimum rent allows the licensor to benefit from the licensee's success while still providing a financial safety net.

A third type is the percentage minimum rent, which is calculated as a percentage of the licensee's sales or profits. This type of minimum rent ensures that the licensor receives a proportionate share of the licensee's success, but it may not provide a consistent income stream if the licensee's performance varies significantly.

In addition to these types, there may be other variations or hybrid models that combine elements of fixed, sliding scale, and percentage minimum rent. The specific type of minimum rent chosen will depend on the negotiation between the licensor and licensee, as well as the industry standards and market conditions.

When drafting a licensing agreement, it is crucial for both parties to carefully consider the type of minimum rent that best suits their needs and expectations. A well-structured minimum rent provision can help ensure a mutually beneficial and sustainable licensing relationship.

Rent or Mortgage: Fixed Expense Essentials for Budgeting Success

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![]()

Calculation of Minimum Rent

The calculation of minimum rent in royalty accounting involves determining the lowest amount of royalty payments that a lessor must receive from a lessee. This calculation is crucial for ensuring that the lessor's interests are protected and that they receive fair compensation for the use of their property. To calculate the minimum rent, several factors must be considered, including the fair market value of the property, the term of the lease, and the expected revenue generated by the property.

One approach to calculating the minimum rent is to use the capitalization rate method. This method involves estimating the fair market value of the property and then applying a capitalization rate to determine the annual rental income. The capitalization rate is typically based on the prevailing interest rates and the expected return on investment for similar properties. Once the annual rental income is determined, it can be divided by the number of months in the lease term to calculate the minimum monthly rent.

Another approach is to use the discounted cash flow method. This method involves projecting the future cash flows generated by the property and then discounting them back to their present value. The present value of the cash flows can then be used to determine the minimum rent required to achieve a desired return on investment. This method takes into account the time value of money and can be more accurate in cases where the cash flows are expected to vary over time.

In addition to these methods, it is also important to consider any applicable laws or regulations that may impact the calculation of minimum rent. For example, some jurisdictions may have specific requirements or restrictions on the amount of rent that can be charged. It is also important to consider the terms of the lease agreement, as these may include provisions that affect the calculation of minimum rent.

Ultimately, the calculation of minimum rent in royalty accounting requires a thorough understanding of the relevant factors and methods. By carefully considering these factors and applying the appropriate calculation methods, lessors can ensure that they receive fair compensation for the use of their property.

Renting 'The Affair' on Dish: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Implications of Minimum Rent

Minimum rent in royalty accounting can have significant implications for both licensors and licensees. One key implication is that it sets a baseline for revenue that the licensor can expect to receive, regardless of the actual sales or usage of the licensed property. This can provide a sense of financial security for the licensor, as they are guaranteed a certain level of income. However, it also means that if the licensed property performs exceptionally well, the licensor may not benefit from the increased revenue, as they are only entitled to the minimum rent.

For licensees, minimum rent can represent a fixed cost that they must budget for, regardless of their own financial performance. This can be beneficial in terms of financial planning, as they know exactly how much they will need to pay each period. However, it can also be a burden if the minimum rent is set too high, as it may limit their ability to invest in other areas of their business.

Another implication of minimum rent is that it can impact the negotiation process between licensors and licensees. If the minimum rent is set too high, it may deter potential licensees from entering into an agreement, as they may not be able to afford the upfront costs. On the other hand, if the minimum rent is set too low, it may not provide sufficient incentive for the licensor to enter into the agreement.

In some cases, minimum rent may also be tied to specific performance metrics or milestones. For example, a licensor may require a higher minimum rent if the licensee reaches certain sales targets or achieves specific marketing goals. This can create an incentive for the licensee to perform well, as they will be rewarded with a higher minimum rent. However, it can also add pressure to the licensee, as they may feel compelled to meet these targets in order to maintain their agreement.

Overall, the implications of minimum rent in royalty accounting are complex and multifaceted. It is important for both licensors and licensees to carefully consider the terms of their agreement and to negotiate a minimum rent that is fair and reasonable for both parties. By doing so, they can ensure that their agreement is mutually beneficial and that they are able to achieve their respective goals.

Discovering Cash Payment Options for Rent: A Comprehensive Guide

You may want to see also

![]()

Minimum Rent vs. Excess Rent

In royalty accounting, the concepts of minimum rent and excess rent are crucial for both licensors and licensees to understand. Minimum rent refers to the fixed amount that a licensee must pay to a licensor regardless of the actual sales or revenue generated from the licensed product or service. This amount is typically negotiated upfront and serves as a guarantee to the licensor that they will receive a certain level of income from the licensing agreement.

On the other hand, excess rent is the additional amount that a licensee pays to a licisor when the actual sales or revenue generated from the licensed product or service exceeds a certain threshold. This threshold is often referred to as the "royalty base" and is calculated by subtracting the minimum rent from the total revenue. Excess rent is typically calculated as a percentage of the revenue above the royalty base and is paid in addition to the minimum rent.

For example, let's say a licensor and licensee agree on a minimum rent of $10,000 per year and an excess rent rate of 5% on any revenue above $20,000. If the licensee generates $30,000 in revenue from the licensed product, they would pay the licensor the $10,000 minimum rent plus an additional $500 in excess rent (5% of $10,000, which is the amount above the $20,000 threshold).

Understanding the difference between minimum rent and excess rent is important for both parties involved in a licensing agreement. For licensors, it ensures that they receive a minimum level of income from the agreement, while also allowing them to benefit from any additional revenue generated by the licensee. For licensees, it provides a clear understanding of their financial obligations and helps them to budget accordingly.

In practice, the negotiation of minimum rent and excess rent rates can be complex and may involve considerations such as the market value of the licensed product or service, the expected revenue potential, and the level of risk involved for both parties. It is essential for both licensors and licensees to carefully consider these factors and to seek professional advice if necessary to ensure that the agreement is fair and mutually beneficial.

Understanding Security Deposits: Protecting Landlords and Tenants in Rental Agreements

You may want to see also

Frequently asked questions

The minimum rent in royalty accounting refers to the lowest amount of royalty payments that a lessor (property owner) can charge a lessee (tenant) for the use of their property. This amount is typically specified in the lease agreement and can vary based on factors such as the type of property, its location, and the terms of the lease.

The minimum rent impacts both the lessor and lessee in a royalty lease agreement. For the lessor, it ensures a guaranteed minimum income from the lease, regardless of the actual usage or revenue generated by the lessee. For the lessee, it represents the minimum financial commitment they must make to the lessor, which can influence their decision-making regarding the lease and the potential profitability of their business operations on the leased property.

Yes, there are circumstances under which the minimum rent in a royalty lease agreement can be adjusted. These adjustments can be based on factors such as changes in market conditions, inflation, or the performance of the lessee's business. The specific terms and conditions for rent adjustments are usually outlined in the lease agreement, and both parties must agree to any changes. In some cases, an independent appraisal may be required to determine the new minimum rent amount.