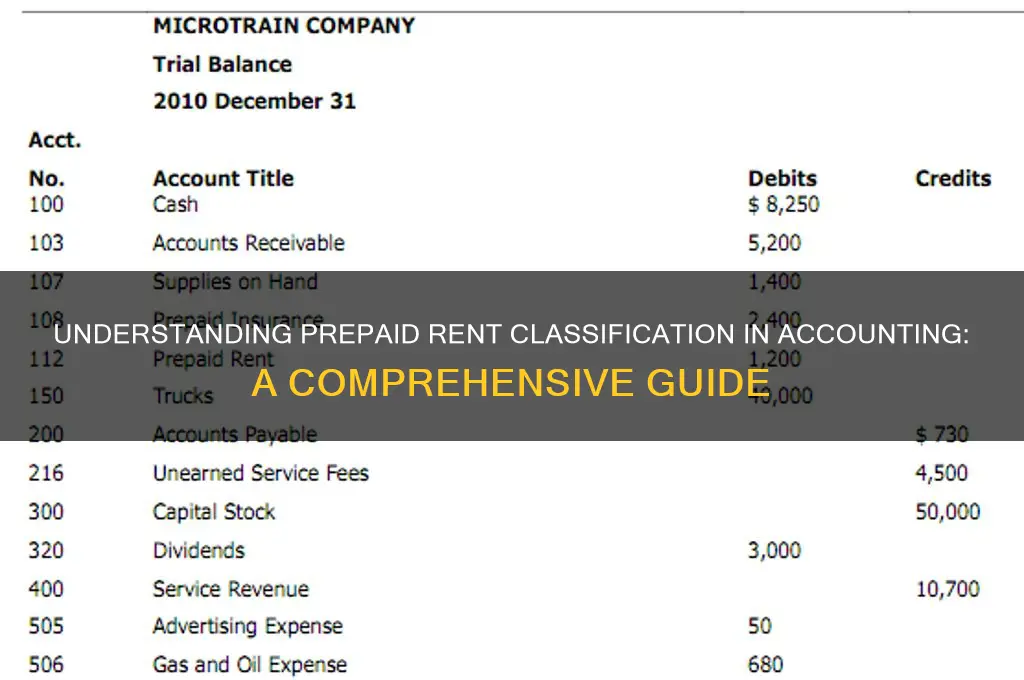

Prepaid rent is classified as a current asset in accounting, reflecting payments made in advance for the use of property or space beyond the current accounting period. It represents a temporary adjustment to ensure expenses are recognized in the period they are incurred, aligning with the matching principle. As the rental period progresses, the prepaid amount is gradually expensed, reducing the asset balance and shifting it to rental expense on the income statement. This classification ensures financial statements accurately reflect the timing of cash outflows and the utilization of resources, maintaining transparency and compliance with accounting standards.

| Characteristics | Values |

|---|---|

| Classification | Asset |

| Type of Asset | Current Asset (if the prepaid period is within one year or operating cycle) |

| Recognition | Recorded on the balance sheet at the amount paid in advance |

| Journal Entry | Debit: Prepaid Rent (Asset), Credit: Cash (Asset) |

| Amortization | Expensed over the period the rent benefits the business (e.g., monthly) |

| Adjusting Entry | Debit: Rent Expense (Expense), Credit: Prepaid Rent (Asset) |

| Financial Statement Impact | Reduces cash initially, then increases rent expense over time |

| Purpose | Represents rent paid in advance for future use of a property |

| Example | Paying $12,000 for a year’s rent in January; $1,000 is expensed each month |

| Reporting | Disclosed under current assets on the balance sheet until fully amortized |

Explore related products

What You'll Learn

- Prepaid Rent Definition: Advance payment for future rent periods, recorded as an asset on the balance sheet

- Classification in Accounting: Prepaid rent is classified as a current asset under the balance sheet

- Journal Entry: Debit prepaid rent (asset), credit cash/bank for the amount paid in advance

- Amortization Process: Expense recognition by allocating prepaid rent over the rental period systematically

- Financial Statement Impact: Reduces cash initially, increases expenses over time, and adjusts asset value

![]()

Prepaid Rent Definition: Advance payment for future rent periods, recorded as an asset on the balance sheet

Prepaid rent is a concept that challenges the traditional notion of expenses, as it represents a unique situation where a company pays for a service in advance. This advance payment for future rent periods is not immediately recognized as an expense but instead finds its place on the balance sheet as an asset. This classification is a strategic move in accounting, allowing businesses to accurately reflect their financial position and ensure that expenses are matched with the appropriate accounting periods.

From an analytical perspective, prepaid rent serves as a buffer against future cash outflows. When a business prepays rent, it essentially converts a future liability into a current asset. This asset is then systematically reduced over time, typically on a monthly basis, as the rented space is utilized. For instance, if a company prepays $12,000 for a year’s rent, it records $1,000 as rent expense each month, while the remaining balance is adjusted in the prepaid rent asset account. This method aligns with the matching principle, ensuring that expenses are recognized in the period they are incurred, not when they are paid.

Instructively, recording prepaid rent involves a straightforward journal entry. At the time of payment, the accountant debits the prepaid rent account (an asset) and credits cash. As each rent period elapses, the entry shifts: the prepaid rent account is credited, and the rent expense account is debited. This process requires meticulous tracking to avoid overstating or understating expenses. For example, a small business prepaying $6,000 for six months of rent would debit prepaid rent for $6,000 and credit cash for the same amount. Each month, $1,000 would be moved from prepaid rent to rent expense, gradually reducing the asset balance.

Comparatively, prepaid rent differs from other prepaid expenses, such as insurance or supplies, in its direct linkage to a specific period of use. While prepaid insurance covers a fixed term, prepaid rent is often tied to monthly or quarterly usage, making its amortization more frequent. This distinction highlights the importance of tailoring accounting practices to the nature of the prepaid item. For instance, a company prepaying $24,000 for two years of insurance would amortize $1,000 monthly, whereas rent prepaid for six months would be fully expensed within that timeframe.

Persuasively, treating prepaid rent as an asset offers several advantages. It provides a clearer picture of a company’s liquidity, as cash is not immediately expensed. Additionally, it supports long-term financial planning by spreading costs over multiple periods. For startups or businesses with tight cash flow, prepaying rent can also serve as a negotiating tool with landlords, potentially securing discounts or favorable terms. However, this strategy requires disciplined financial management to ensure that prepaid amounts are accurately tracked and amortized.

In conclusion, prepaid rent is more than just an advance payment—it’s a strategic accounting tool that enhances financial accuracy and planning. By recording it as an asset, businesses can align expenses with usage periods, maintain liquidity, and optimize their financial statements. Whether for a small business or a large corporation, understanding and properly managing prepaid rent is essential for robust financial health.

Unearthing Old Real Estate Photos: A Guide

You may want to see also

Explore related products

![]()

Classification in Accounting: Prepaid rent is classified as a current asset under the balance sheet

Prepaid rent is classified as a current asset on the balance sheet, a designation that reflects its short-term nature and liquidity. This classification is rooted in the accounting principle that assets are categorized based on their expected conversion into cash or use within one year or the operating cycle, whichever is longer. When a business pays rent in advance, it gains a right to use the property for a specified period, typically within the next 12 months. This right is considered an asset because it provides future economic benefits, specifically the use of the rented space without additional immediate payment. By recording prepaid rent as a current asset, businesses ensure their financial statements accurately represent their short-term resources and obligations.

To illustrate, consider a company that pays $12,000 in January for a year’s worth of rent. Instead of expensing the entire amount immediately, the company records $1,000 as rent expense each month and reduces the prepaid rent asset by the same amount. This method aligns with the matching principle, which requires expenses to be recognized in the period they are incurred. The prepaid rent account is gradually reduced over time, reflecting the consumption of the asset. For example, after six months, the prepaid rent balance would be $6,000, with $6,000 already expensed. This approach ensures financial statements remain accurate and reflective of the business’s financial position.

Classifying prepaid rent as a current asset also impacts financial ratios and analysis. Current assets are used to calculate key metrics such as the current ratio (current assets / current liabilities) and working capital (current assets – current liabilities). Including prepaid rent in this category provides a more comprehensive view of a company’s liquidity and ability to meet short-term obligations. However, analysts should note that prepaid rent is not as liquid as cash or accounts receivable, as it cannot be readily converted into cash. This distinction is crucial when assessing a company’s short-term financial health.

A practical tip for businesses is to maintain detailed records of prepaid rent transactions, including lease agreements, payment schedules, and amortization tables. This documentation ensures compliance with accounting standards and facilitates accurate financial reporting. For instance, using accounting software to automate the amortization process can reduce errors and save time. Additionally, businesses should periodically review their prepaid rent balances to ensure they align with lease terms and consumption patterns. Proper management of prepaid rent not only enhances financial accuracy but also supports informed decision-making.

In conclusion, the classification of prepaid rent as a current asset is a fundamental aspect of accounting that reflects its short-term nature and future economic benefits. By adhering to this classification, businesses ensure their financial statements are transparent and compliant with accounting principles. Understanding this concept is essential for accurate financial reporting, ratio analysis, and strategic planning. Whether you’re a business owner, accountant, or financial analyst, recognizing the role of prepaid rent in the balance sheet is key to interpreting a company’s financial health and performance.

Is Mission: Impossible – Dead Reckoning Available for Rent Yet?

You may want to see also

Explore related products

![]()

Journal Entry: Debit prepaid rent (asset), credit cash/bank for the amount paid in advance

Prepaid rent is classified as a current asset on the balance sheet because it represents a payment made in advance for future benefits. When a business pays rent before the rental period begins, it records this transaction to reflect the preservation of value over time. The journal entry for this scenario is straightforward: debit prepaid rent (an asset account) and credit cash or bank (a reduction in liquidity). This entry ensures that the financial statements accurately portray the company’s resources and obligations.

Consider a practical example: a small business pays $6,000 in December for rent covering January to March of the following year. The journal entry would debit prepaid rent for $6,000 and credit the bank account for the same amount. This records the outflow of cash while simultaneously recognizing the future economic benefit. Over the rental period, the prepaid rent is gradually expensed, typically through monthly adjusting entries, to align expenses with the period in which they are incurred.

The analytical perspective highlights the importance of this entry in maintaining the matching principle, a cornerstone of accrual accounting. By deferring the recognition of rent expense, the company avoids overstating expenses in the period of payment and understating them in subsequent periods. This ensures financial statements reflect the true financial position and performance of the business. For instance, if the $6,000 were immediately expensed in December, it would distort the profitability of that month and mislead stakeholders.

From an instructive standpoint, here’s how to execute the entry correctly: identify the amount paid in advance, ensure it aligns with the rental agreement, and use the exact account titles (e.g., "Prepaid Rent" and "Cash" or "Bank"). Avoid common errors like recording the full amount as an expense or omitting the entry altogether. For businesses using accounting software, double-check that the transaction is categorized under the asset account, not the expense account.

Finally, a persuasive argument for this practice lies in its compliance with Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). Properly classifying prepaid rent as an asset enhances transparency and credibility in financial reporting. Investors, creditors, and auditors scrutinize these details, and accurate entries build trust. For example, a startup seeking funding will find that meticulous handling of prepaid expenses can positively influence investor confidence in its financial management.

In summary, the journal entry for prepaid rent—debiting the asset and crediting cash/bank—is a critical step in accounting. It ensures assets are correctly stated, expenses are matched to the appropriate periods, and financial statements remain compliant and reliable. Whether for a small business or a large corporation, mastering this entry is essential for accurate financial reporting.

Maximize Your Provo Rental: Strategies to Attract More Tenants

You may want to see also

Explore related products

![]()

Amortization Process: Expense recognition by allocating prepaid rent over the rental period systematically

Prepaid rent represents a unique accounting challenge, as it involves recognizing an expense that hasn’t yet been fully consumed. The amortization process systematically allocates this prepaid expense over the rental period, ensuring financial statements accurately reflect the business’s use of the asset. This method aligns with the matching principle, which requires expenses to be recognized in the same period as the revenues they help generate. Without amortization, prepaid rent would distort financial results, overstating expenses in the payment period and understating them in subsequent periods.

The amortization process begins by identifying the total prepaid rent amount and the duration of the rental agreement. For example, if a business pays $12,000 annually for rent in advance, this amount is initially recorded as a prepaid asset. Over the 12-month rental period, $1,000 ($12,000 ÷ 12) is systematically recognized as a rent expense each month. This straight-line approach is the most common method, as it’s straightforward and aligns with the consistent use of the rented space. However, alternative methods, such as allocating expenses based on actual usage or seasonal variations, may be appropriate in specific scenarios.

A critical aspect of the amortization process is consistency. Once a method is chosen, it should be applied uniformly to all similar prepaid rent transactions to ensure comparability across financial periods. For instance, if a company decides to amortize prepaid rent monthly, it must adhere to this schedule for all rental agreements. Deviating from this practice could introduce inconsistencies, complicating financial analysis and potentially misleading stakeholders. Auditors and accountants often scrutinize this area to ensure compliance with accounting standards like GAAP or IFRS.

Practical implementation of the amortization process requires robust record-keeping and accounting software. Businesses should maintain detailed schedules tracking prepaid rent balances, amortization schedules, and expense recognition dates. Automation tools can streamline this process, reducing the risk of errors and saving time. For small businesses, even a simple spreadsheet can suffice, provided it’s updated regularly and reconciled with the general ledger. Regular reviews of these schedules ensure accuracy and allow for adjustments if rental terms change mid-period.

In conclusion, the amortization process is a cornerstone of accurate financial reporting for prepaid rent. By systematically allocating expenses over the rental period, businesses ensure their financial statements reflect the true economic reality of their operations. This approach not only adheres to accounting principles but also provides stakeholders with a clear, transparent view of the company’s financial health. Mastering this process is essential for accountants and business owners alike, as it directly impacts decision-making and compliance.

Weekly or Monthly Rent in Poland: Understanding Payment Frequencies

You may want to see also

Explore related products

![Tamilee Webb's Tighter Assets: Cardio Blast [DVD]](https://m.media-amazon.com/images/I/41PdKwc3YqL._AC_UL320_.jpg)

![]()

Financial Statement Impact: Reduces cash initially, increases expenses over time, and adjusts asset value

Prepaid rent is initially recorded as a current asset on the balance sheet, reflecting the advance payment for future rental periods. This classification is crucial because it represents a resource that will provide economic benefits over time. When a business pays rent in advance, it immediately reduces the cash balance, a direct and immediate impact on liquidity. For instance, if a company prepays $12,000 for six months of rent, its cash account decreases by $12,000, while the prepaid rent asset account increases by the same amount. This transaction highlights the trade-off between current liquidity and future economic benefit.

As time progresses, the prepaid rent asset is gradually expensed, aligning with the matching principle in accounting. Each month, a portion of the prepaid rent is recognized as rent expense, reducing the asset’s value on the balance sheet. For example, in the six-month prepayment scenario, $2,000 would be expensed monthly, decreasing the prepaid rent asset by $2,000 while increasing rent expense by the same amount. This process ensures that expenses are matched with the revenue they help generate, providing a more accurate representation of financial performance over time.

The adjustment of the asset value is a critical aspect of prepaid rent’s financial statement impact. As the prepaid rent is expensed, the asset account is reduced, eventually reaching zero by the end of the prepayment period. This adjustment ensures that the balance sheet accurately reflects the remaining value of the prepaid asset. For instance, after three months of the six-month prepayment, the prepaid rent asset would be valued at $6,000, with $6,000 already expensed. This dynamic process underscores the importance of proper accounting treatment to maintain transparency and accuracy in financial reporting.

From a practical standpoint, businesses must carefully manage prepaid rent to optimize cash flow and expense recognition. For example, a small business prepaying annual rent of $24,000 would need to budget for the immediate cash outflow while planning for the monthly $2,000 expense. This approach ensures that the business maintains sufficient liquidity and accurately tracks its financial obligations. Additionally, proper classification and adjustment of prepaid rent can impact key financial ratios, such as current assets and operating expenses, influencing stakeholder perceptions and decision-making.

In summary, prepaid rent’s financial statement impact is threefold: it reduces cash initially, increases expenses over time, and adjusts asset value as the prepayment is consumed. This treatment aligns with accounting principles, ensuring that financial statements accurately reflect a company’s financial position and performance. By understanding and managing these impacts, businesses can maintain financial health and provide transparent reporting to stakeholders. For instance, a company prepaying rent for a new office space must consider not only the immediate cash outflow but also the long-term expense recognition and asset adjustment to effectively manage its finances.

The Tragic Death of Dana Plato: Diff'rent Strokes Star's Untold Story

You may want to see also

Frequently asked questions

Prepaid rent is classified as a current asset on the balance sheet because it represents rent paid in advance for a period within the next 12 months.

Prepaid rent is considered an asset because it represents a future economic benefit—the right to use rental property—that the company has already paid for but has not yet utilized.

Prepaid rent is initially recorded as a debit to the prepaid rent account (an asset) and a credit to cash or the payment account. As the rent is consumed, it is expensed by debiting rent expense and crediting prepaid rent.

Prepaid rent is typically classified as a current asset because it is expected to be fully utilized within one year or the operating cycle, whichever is longer.

Prepaid rent is the amount paid in advance and recorded as an asset, while rent expense is the portion of prepaid rent that is recognized as an expense in the period it is used.

![The Lotte Berk Method, 4 Disc Set: Basic Essentials, Hip Hugger Abs, Muscle Eats Fat, High Round Assets [DVD]](https://m.media-amazon.com/images/I/61s2oopCj5L._AC_UL320_.jpg)