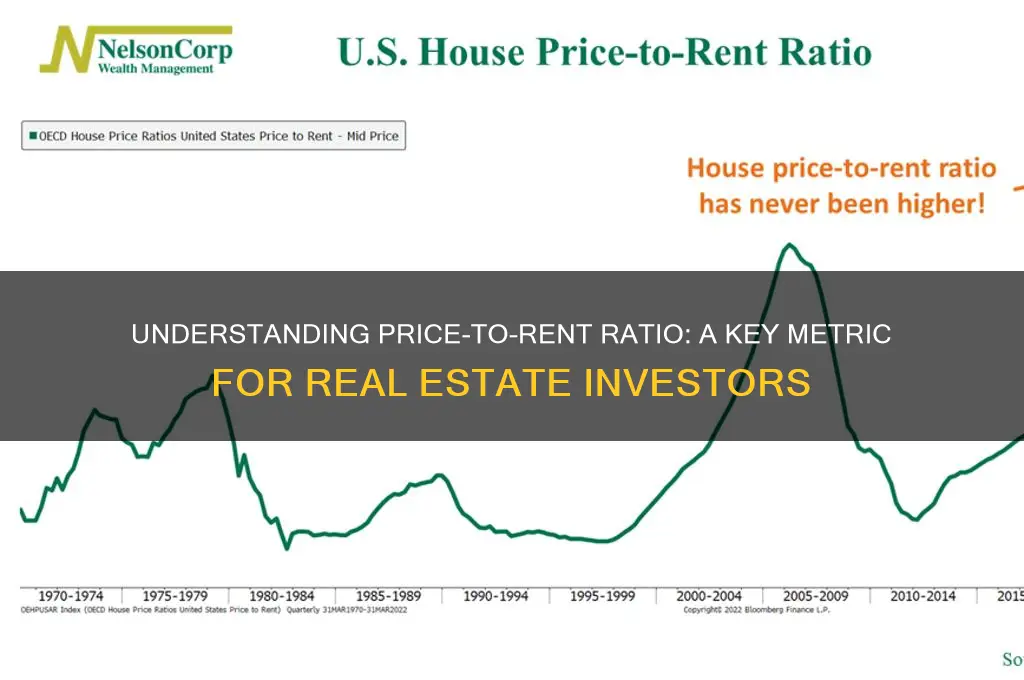

The Price-to-Rent Ratio is a widely used metric in real estate that compares the relative affordability of purchasing a property versus renting it. Calculated by dividing the median home price by the annual median rent in a given market, this ratio helps investors, homebuyers, and analysts assess whether buying or renting is more financially advantageous. A lower ratio typically indicates that renting is more cost-effective, while a higher ratio suggests that purchasing might be a better long-term investment. By providing a standardized measure, the Price-to-Rent Ratio allows for comparisons across different cities, regions, or time periods, offering valuable insights into housing market dynamics and investment potential.

| Characteristics | Values |

|---|---|

| Definition | The Price-to-Rent Ratio (P/R Ratio) is a financial metric used to compare the relative affordability of purchasing versus renting a property. |

| Formula | (Median Home Price) / (Annual Median Rent) |

| Purpose | 1. Assessing housing market valuation 2. Identifying potential real estate bubbles 3. Comparing affordability across different cities or regions 4. Guiding investment decisions in real estate |

| Interpretation | - A high P/R Ratio (>20) suggests that buying is less affordable compared to renting. - A low P/R Ratio (<15) indicates that buying might be more affordable than renting. |

| Latest Global Average (2023) | Approximately 18-20 (varies by country and city) |

| Limitations | 1. Does not account for financing costs (e.g., mortgage interest rates) 2. Ignores property taxes, maintenance, and other homeownership expenses 3. Assumes consistent rental yields over time |

| Example Usage | In Q1 2023, the P/R Ratio in Miami was ~28, suggesting renting is more affordable than buying, while in Detroit, it was ~12, indicating buying is more favorable. |

| Data Sources | 1. Zillow 2. Numbeo 3. OECD Housing Statistics 4. Local real estate agencies and government data |

| Trend (2020-2023) | P/R Ratios have increased in many major cities due to rising home prices and relatively stable rents, making renting more attractive in some markets. |

Explore related products

What You'll Learn

![]()

Housing Market Affordability

The price-to-rent ratio, a key metric in real estate, compares the cost of buying a property to the cost of renting a similar one. It’s calculated by dividing the home’s purchase price by its annual rental income. For instance, a $300,000 home that rents for $18,000 annually has a ratio of 16.7. This figure helps determine whether buying or renting is more financially prudent in a given market. In housing market affordability discussions, this ratio serves as a thermometer, revealing whether home prices are outpacing rental costs, a red flag for potential affordability crises.

Consider a scenario where a city’s price-to-rent ratio jumps from 15 to 25 in five years. This indicates that home prices are rising faster than rents, making buying less affordable relative to renting. For first-time homebuyers, especially those under 35 with median incomes, this shift can be devastating. A ratio above 20 often signals an overheated market, where purchasing a home becomes a luxury rather than a feasible investment. To mitigate this, policymakers could incentivize affordable housing projects or introduce rent-to-own programs, bridging the gap between renting and buying.

From a comparative perspective, the price-to-rent ratio varies dramatically across regions. In San Francisco, the ratio hovers around 30, while in Detroit, it’s closer to 10. Such disparities highlight the importance of local context in affordability discussions. For investors, markets with lower ratios present opportunities for rental income, while buyers might prioritize areas where the ratio aligns with historical averages. A practical tip for prospective buyers: use online calculators to compare ratios across neighborhoods, ensuring you’re not overpaying in an inflated market.

Persuasively, the price-to-rent ratio isn’t just a number—it’s a call to action. When ratios exceed 20, renters should reconsider the urgency to buy, opting instead to save or invest elsewhere. Conversely, ratios below 15 suggest buying could be more cost-effective than renting long-term. For instance, a family renting a $2,000 monthly apartment ($24,000 annually) might find purchasing a $300,000 home (ratio of 12.5) more financially sound, assuming stable mortgage rates. This ratio empowers individuals to make data-driven decisions, shifting the narrative from “Can I afford to buy?” to “Should I buy now?”

Finally, while the price-to-rent ratio is invaluable, it’s not infallible. It doesn’t account for maintenance costs, property taxes, or emotional factors like neighborhood desirability. For example, a high ratio in a thriving urban area might still attract buyers prioritizing lifestyle over affordability. Pair this metric with others, like the housing affordability index or income-to-price ratios, for a comprehensive view. Ultimately, understanding this ratio transforms passive market observers into active participants, capable of navigating affordability challenges with clarity and confidence.

Pin Holes: Rental Decorating and Repairing Walls

You may want to see also

Explore related products

$19.95

![]()

Investment Property Viability

The price-to-rent ratio, a critical metric in real estate, compares the cost of purchasing a property to the annual rental income it generates. For investors, this ratio is a litmus test for Investment Property Viability, offering a snapshot of whether buying or renting is more financially prudent in a given market. A low ratio suggests that purchasing might be more advantageous, while a high ratio indicates renting could be the better option. However, this metric is just the starting point; its true value lies in how it’s contextualized with other factors.

To assess viability, begin by calculating the ratio: divide the property’s purchase price by its annual rental income. For instance, a $200,000 property generating $16,000 in yearly rent has a ratio of 12.5. Historically, a ratio below 15 is considered favorable for buyers, but this threshold varies by location. Urban markets like San Francisco or New York often exceed 20, while smaller cities may hover around 10. The key is to compare the ratio against local averages, not national benchmarks, as regional economic conditions heavily influence its interpretation.

Beyond the ratio itself, investors must consider cash flow potential. A property with a low price-to-rent ratio might still be unviable if maintenance, taxes, or vacancy rates erode profitability. For example, a $150,000 property with a 10 ratio may seem attractive, but if annual expenses exceed $10,000, the net return diminishes. Use the 50% rule of thumb: estimate that 50% of rental income will cover expenses, and ensure the remaining 50% aligns with your investment goals.

Another critical factor is market appreciation. A property in an appreciating market can offset a higher price-to-rent ratio if its value grows significantly over time. Conversely, a low ratio in a stagnant or declining market may signal hidden risks. Research local economic indicators, such as job growth, population trends, and development plans, to gauge long-term potential. Tools like Zillow’s Home Value Index or Census Bureau data can provide actionable insights.

Finally, leverage the price-to-rent ratio as part of a broader strategy. For instance, if the ratio is high but rental demand is strong, consider a rent-to-own model to attract tenants who may later purchase. Alternatively, in markets with low ratios, explore house hacking—living in one unit while renting others—to maximize cash flow. Pairing the ratio with creative strategies can turn marginal opportunities into viable investments.

In essence, the price-to-rent ratio is not a standalone decision-maker but a powerful tool when combined with cash flow analysis, market research, and innovative approaches. By mastering its application, investors can identify properties that not only meet viability thresholds but also align with long-term financial objectives.

Understanding Rent-to-Own Homes in New Hampshire: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Rent vs. Buy Decisions

The price-to-rent ratio, a key metric in real estate, compares the cost of buying a home to the cost of renting a similar property. It’s calculated by dividing the home’s price by its annual rent. For instance, a $300,000 home with an annual rent equivalent of $18,000 yields a ratio of 16.67. This figure helps determine whether buying or renting is more financially prudent in a given market. A lower ratio suggests buying might be more advantageous, while a higher ratio leans toward renting. However, this metric is just one piece of the puzzle in the rent vs. buy decision.

Analyzing the price-to-rent ratio requires context. In cities like San Francisco or New York, ratios often exceed 25, making renting more appealing due to high home prices and relatively lower rents. Conversely, in smaller markets like Detroit or Cleveland, ratios may dip below 10, tipping the scales toward buying. Yet, this ratio doesn’t account for long-term costs like maintenance, property taxes, or mortgage interest, which can significantly impact affordability. For example, a homeowner might spend 1–4% of a home’s value annually on maintenance, a cost renters avoid entirely.

To use the price-to-rent ratio effectively, consider your time horizon. Financial experts often suggest buying if you plan to stay in a home for at least 5–7 years, as this allows time to build equity and offset transaction costs like closing fees. Renting, however, offers flexibility and lower upfront costs, making it ideal for short-term stays or uncertain life plans. Pair the ratio with other tools, such as calculating the breakeven point between renting and buying, to make a more informed decision. For instance, if the ratio is 15, compare it to the historical average (around 14 in the U.S.) to gauge market conditions.

A persuasive argument for renting emerges when the ratio is high and rental prices are stable or declining. In such scenarios, renters can lock in affordable monthly payments while avoiding the risks of homeownership, such as market downturns. Conversely, buying becomes compelling when the ratio is low and mortgage rates are favorable. For example, a 30-year fixed-rate mortgage at 4% or lower can make monthly payments comparable to rent while building equity. However, buyers must factor in the opportunity cost of tying up a large down payment, which could otherwise be invested elsewhere.

Ultimately, the rent vs. buy decision hinges on personal circumstances and market dynamics. The price-to-rent ratio serves as a starting point, but it should be complemented by a holistic financial assessment. Consider your cash flow, savings goals, and risk tolerance. For instance, a young professional with limited savings might prioritize renting to avoid depleting emergency funds, while a family with stable income could benefit from the long-term wealth-building potential of homeownership. By combining this ratio with practical considerations, you can navigate this decision with greater clarity and confidence.

Renting Office Space in Clonmel: A Comprehensive Guide for Businesses

You may want to see also

Explore related products

![]()

Real Estate Valuation

The price-to-rent ratio, a key metric in real estate valuation, compares the cost of purchasing a property to the cost of renting a similar one. This ratio is calculated by dividing the property's price by its annual rental income. For instance, a $300,000 home that rents for $1,500 per month (or $18,000 annually) would have a price-to-rent ratio of 16.67. This figure provides valuable insights into whether buying or renting is more financially advantageous in a given market. A lower ratio suggests that buying might be a better option, while a higher ratio indicates that renting could be more cost-effective.

Analyzing the price-to-rent ratio requires context. In high-demand urban areas like San Francisco or New York, ratios often exceed 25, reflecting the premium on homeownership. Conversely, in more affordable markets such as Detroit or Cleveland, ratios may hover around 10. Historical data also matters; during the 2008 housing bubble, ratios in many U.S. cities spiked unsustainably, signaling overvaluation. Investors and homebuyers should compare current ratios to long-term averages to gauge market conditions. For example, a ratio of 15 might be considered high in one region but average in another, underscoring the importance of local market analysis.

To effectively use the price-to-rent ratio in real estate valuation, follow these steps: First, gather accurate data on both property prices and rental rates for comparable homes in the area. Second, calculate the ratio for multiple properties to identify trends. Third, compare these ratios to historical benchmarks and neighboring markets. Finally, consider additional factors like property taxes, maintenance costs, and mortgage interest rates, as these can influence the buy-versus-rent decision. For instance, a property with a low price-to-rent ratio might still be a poor investment if maintenance costs are exorbitant.

A persuasive argument for using the price-to-rent ratio is its ability to simplify complex financial decisions. For first-time homebuyers, this metric offers a clear, quantifiable way to assess affordability. For investors, it helps identify undervalued markets with strong rental demand. However, it’s not without limitations. The ratio doesn’t account for emotional factors like the desire for homeownership or the flexibility of renting. Additionally, it assumes consistent rental income, which may not hold true in volatile markets. Despite these caveats, the price-to-rent ratio remains a powerful tool for informed decision-making in real estate.

In conclusion, the price-to-rent ratio is a versatile metric that serves both individual homebuyers and institutional investors. By providing a snapshot of market dynamics, it helps stakeholders determine whether buying or renting aligns with their financial goals. However, it should be used in conjunction with other valuation methods, such as cap rates or cash-on-cash returns, for a comprehensive analysis. For example, a property with a favorable price-to-rent ratio but low appreciation potential might be less attractive than one with a higher ratio but stronger long-term growth prospects. Ultimately, the ratio is a starting point, not the final word, in real estate valuation.

Hosting a Party at an Airbnb: Tips for a Smooth Rental Experience

You may want to see also

Explore related products

![]()

Market Trend Analysis

The price-to-rent ratio, a critical metric in real estate analysis, compares the cost of purchasing a property to the cost of renting a similar one. This ratio is a powerful tool for market trend analysis, offering insights into whether buying or renting is more financially advantageous in a given market. By examining historical and current price-to-rent ratios, investors and homeowners can identify emerging trends, predict future market movements, and make informed decisions.

Analyzing Market Cycles: A key application of the price-to-rent ratio in market trend analysis is identifying phases of the real estate cycle. During a boom, property prices often outpace rental rates, leading to a high price-to-rent ratio. Conversely, in a downturn, rental rates may hold steady or rise relative to declining property prices, resulting in a lower ratio. For instance, in the lead-up to the 2008 housing crisis, many U.S. cities saw price-to-rent ratios soar above historical averages, signaling an overheated market. Tracking this ratio over time allows analysts to spot these cycles and anticipate shifts, providing a valuable early warning system for investors.

Regional Comparisons and Investment Opportunities: Market trend analysis using the price-to-rent ratio also enables comparisons across different regions, highlighting areas where buying or renting may be more attractive. For example, a city with a price-to-rent ratio of 15 (indicating that buying is equivalent to paying 15 years of rent) might be considered overvalued compared to a neighboring city with a ratio of 10. Investors can use this information to identify undervalued markets with potential for growth. Additionally, this analysis can guide individual homebuyers in deciding whether to enter the market or continue renting based on local conditions.

Impact of Economic Factors: Economic factors such as interest rates, employment levels, and population growth significantly influence the price-to-rent ratio and, consequently, market trends. Lower interest rates typically make buying more affordable, driving up property prices and the price-to-rent ratio. Conversely, high unemployment or stagnant wage growth can suppress property prices while rental demand remains stable, lowering the ratio. By integrating these economic indicators into market trend analysis, stakeholders can better understand the underlying forces shaping the ratio and make more accurate predictions.

Practical Tips for Application: To effectively use the price-to-rent ratio in market trend analysis, start by gathering reliable data from sources like the Federal Housing Finance Agency or local real estate boards. Calculate the ratio for multiple time periods to identify trends and compare them to historical benchmarks. For instance, a ratio consistently above 20 might indicate a bubble, while one below 15 could suggest a buyer’s market. Combine this analysis with other metrics, such as affordability indices and vacancy rates, for a comprehensive view. Finally, consider consulting with real estate professionals or economists to interpret findings and tailor strategies to specific goals, whether investing, buying a home, or managing rental properties.

Rent Kindle Books with Amazon Prime: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The Price to Rent Ratio is used to measure the relative affordability of purchasing a home versus renting in a specific market. It compares the cost of buying a property to the cost of renting a similar property.

The Price to Rent Ratio is calculated by dividing the median home price by the annual median rent for similar properties in the same area. A higher ratio indicates that buying is relatively more expensive compared to renting, while a lower ratio suggests the opposite.

A high Price to Rent Ratio indicates that purchasing a home is relatively expensive compared to renting in that market. It may suggest that the housing market is overvalued or that renting is a more cost-effective option for residents.