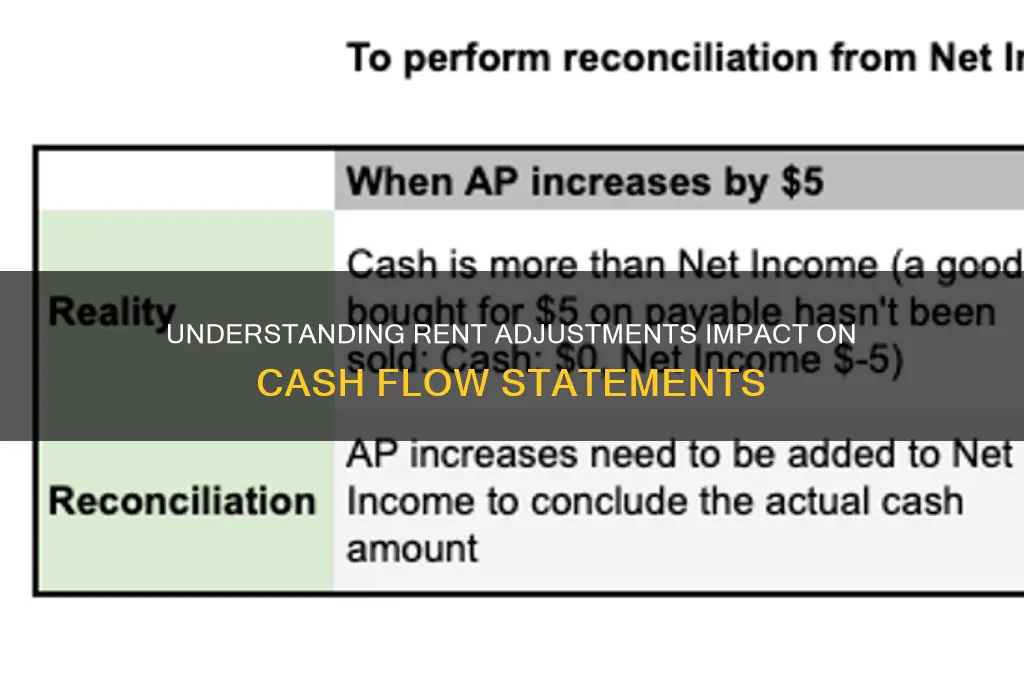

Rent adjustments on a cash flow statement refer to the changes made to reflect the actual cash payments for rent, as opposed to the straight-line rent expense recognized in the income statement. Under accrual accounting, rent expenses are often smoothed out over the lease term, but in reality, rent payments may vary due to factors like escalations, incentives, or free rent periods. These adjustments ensure that the cash flow statement accurately represents the timing and amount of cash outflows related to rent, providing a clearer picture of a company’s liquidity and operational cash usage. This reconciliation is crucial for investors and stakeholders to understand the true cash impact of lease obligations.

| Characteristics | Values |

|---|---|

| Definition | Rent adjustments on a cash flow statement refer to the reconciliation of rent expenses between the income statement (accrual basis) and the actual cash payments made during the period. |

| Purpose | To reflect the timing differences between when rent is recognized as an expense and when it is paid in cash. |

| Location | Typically found in the Operating Activities section of the cash flow statement. |

| Calculation | Rent Adjustments = Rent Expense (Income Statement) - Cash Paid for Rent (Actual Payments) |

| Impact on Cash Flow | Positive adjustment if prepaid rent (cash paid in advance) is more than the expense recognized; negative adjustment if accrued rent (expense recognized but not paid) is more than cash paid. |

| Example | If rent expense for the year is $120,000 but only $100,000 was paid in cash, the adjustment would be $20,000 (added back to cash flow). |

| Relevance | Ensures the cash flow statement accurately reflects the actual cash movements related to rent obligations. |

| GAAP/IFRS Compliance | Required under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) to reconcile accrual-based expenses with cash flows. |

| Frequency | Adjustments are made periodically, typically annually or quarterly, depending on reporting requirements. |

| Key Consideration | Rent adjustments are crucial for investors and stakeholders to understand the liquidity and cash position of a company. |

Explore related products

What You'll Learn

- Rent Escalation Clauses: Annual rent increases tied to inflation or fixed percentages impact cash outflow predictability

- Lease Incentives: One-time rent reductions or free periods temporarily lower cash outflows in early lease terms

- Percentage Rent: Additional rent based on tenant revenue affects cash flow variability in retail leases

- Operating Expense Pass-Throughs: Variable costs like taxes or maintenance increase rent, reducing net cash flow

- Rent Abatement: Temporary rent waivers during disruptions (e.g., renovations) create irregular cash flow patterns

![]()

Rent Escalation Clauses: Annual rent increases tied to inflation or fixed percentages impact cash outflow predictability

Rent escalation clauses are a double-edged sword for tenants and landlords alike. These provisions, embedded in lease agreements, mandate annual rent increases tied to inflation or fixed percentages. While they offer landlords a hedge against rising costs, they introduce variability into a tenant’s cash flow projections. For businesses, especially those operating on thin margins, this unpredictability can strain financial planning. A fixed percentage increase, say 3% annually, may seem manageable initially but compounds over time, significantly inflating rent expenses. Similarly, inflation-linked escalations, though theoretically fair, expose tenants to economic volatility, making budgeting a moving target.

Consider a retail tenant signing a 10-year lease with a 2% annual fixed escalation clause. In year one, rent is $50,000, but by year ten, it balloons to $60,950—a 21.9% increase. If inflation averages 4% during this period, an inflation-tied clause would push rent to $74,536, a 49.1% jump. Such scenarios underscore the importance of scrutinizing escalation terms during lease negotiations. Tenants should assess their long-term financial resilience against projected rent hikes, while landlords must balance risk mitigation with tenant retention.

From a cash flow statement perspective, rent escalation clauses complicate the "operating activities" section, where rent is typically reported. Predictable rent expenses allow for straightforward forecasting, but escalations introduce variability, requiring adjustments in cash flow projections. For instance, a company might initially budget $100,000 annually for rent but face a $3,000 increase the following year due to a 3% escalation. This seemingly minor adjustment can disrupt liquidity, especially if paired with other variable expenses. Accountants must therefore incorporate escalation schedules into their models, treating rent not as a static cost but as a dynamic line item.

Negotiating rent escalation clauses demands strategic foresight. Tenants should seek caps on inflation-linked increases or propose hybrid models combining fixed and variable components. For example, a clause might limit inflation-based hikes to 2% annually or the Consumer Price Index (CPI) increase, whichever is lower. Alternatively, tenants could negotiate rent-free periods or tenant improvement allowances in exchange for accepting higher escalation rates. Landlords, meanwhile, should weigh the benefits of stable, long-term tenants against the risks of overburdening them with steep increases.

In practice, transparency and flexibility are key. Both parties should model various escalation scenarios to understand their financial implications. Tools like Excel or specialized real estate software can simulate rent growth over the lease term, highlighting potential cash flow pressures. Ultimately, rent escalation clauses are not inherently problematic—they are a tool for aligning lease terms with economic realities. However, their impact on cash outflow predictability necessitates careful negotiation, meticulous planning, and ongoing monitoring to ensure financial stability for all stakeholders.

Can You Deduct Rent and Utilities on Your Taxes?

You may want to see also

Explore related products

![]()

Lease Incentives: One-time rent reductions or free periods temporarily lower cash outflows in early lease terms

Lease incentives, such as one-time rent reductions or free periods, are strategic tools landlords use to attract tenants, particularly in competitive or sluggish real estate markets. For tenants, these incentives provide immediate relief by lowering cash outflows during the early lease term, which can be crucial for businesses managing tight budgets or startups with limited capital. For instance, a retail tenant might receive the first three months rent-free, significantly easing their initial financial burden and allowing them to allocate resources to inventory, marketing, or operational setup.

From a cash flow statement perspective, these incentives create a temporary distortion in reported cash outflows. Instead of reflecting the full contractual rent expense, the statement shows reduced payments during the incentive period. This can make a company’s liquidity position appear stronger than it would under normal lease terms. For example, if a tenant signs a $10,000/month lease with a six-month rent-free period, their cash flow statement would show zero rent payments for those months, despite the underlying obligation to pay $60,000 over the lease term.

Analyzing the impact of lease incentives requires careful scrutiny. While they improve short-term cash flow, they do not eliminate the obligation to pay rent in the future. Tenants must consider the long-term implications, such as higher payments later in the lease term or a steeper rent escalation clause. Investors and stakeholders should also adjust their analysis to normalize cash flows, ensuring a clear understanding of the company’s true financial health. For instance, a simple adjustment could involve amortizing the total rent obligation evenly over the lease term, rather than reflecting it as paid in uneven installments.

Practical tips for handling lease incentives include maintaining detailed records of the incentive structure and its timing, as well as clearly disclosing the adjustments in financial statements or footnotes. Tenants should negotiate incentives that align with their cash flow needs, such as front-loaded rent reductions if they anticipate higher expenses early on. Landlords, on the other hand, should structure incentives to balance tenant attraction with long-term revenue stability, perhaps by offering tiered reductions or tying incentives to lease renewal commitments.

In conclusion, lease incentives are a double-edged sword—beneficial for short-term cash flow management but requiring careful analysis to avoid misinterpretation of financial health. By understanding their mechanics and adjusting financial reporting accordingly, both tenants and stakeholders can navigate these incentives effectively, ensuring transparency and informed decision-making.

Renting Books at UF Library West: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Percentage Rent: Additional rent based on tenant revenue affects cash flow variability in retail leases

Retail leases often include a percentage rent clause, a mechanism tying additional rent payments to a tenant's revenue. This structure, while beneficial for landlords seeking to share in a tenant's success, introduces a layer of cash flow variability for both parties. Unlike fixed rent, which provides predictable income and expenses, percentage rent fluctuates based on sales performance. This variability demands careful consideration in cash flow forecasting and financial planning.

Landlords must account for potential shortfalls during slow sales periods, while tenants need to manage cash reserves to meet higher rent obligations when revenue surges.

Imagine a boutique clothing store in a bustling mall. Their lease includes a 5% percentage rent on monthly sales exceeding $100,000. During the holiday season, sales skyrocket to $150,000, triggering an additional $2,500 in rent. Conversely, a slow January sees sales dip to $80,000, resulting in no percentage rent payment. This example illustrates the direct correlation between sales and rent, highlighting the need for both landlord and tenant to anticipate and adapt to these fluctuations.

Tenants, particularly those with seasonal businesses, should factor in percentage rent obligations when setting pricing strategies, managing inventory, and planning marketing campaigns.

The impact of percentage rent on cash flow extends beyond individual transactions. For landlords, it can influence property valuation and financing options. Lenders may view percentage rent as a risk factor, potentially affecting loan terms. Tenants, on the other hand, need to consider the long-term sustainability of their business model under a percentage rent structure. High percentage rent rates can erode profitability during peak seasons, while low rates may limit a landlord's ability to capitalize on a tenant's success.

Negotiating a fair percentage rent threshold and rate is crucial for both parties to ensure a mutually beneficial arrangement.

In conclusion, percentage rent, while offering potential rewards, introduces a dynamic element to retail lease agreements. Both landlords and tenants must carefully assess the implications on cash flow, factoring in sales variability, business cycles, and long-term financial goals. By understanding the mechanics and potential risks, they can navigate this complex arrangement and foster a sustainable and profitable relationship.

Where to Stream Rent-a-Girlfriend Season 2: A Complete Guide

You may want to see also

Explore related products

![]()

Operating Expense Pass-Throughs: Variable costs like taxes or maintenance increase rent, reducing net cash flow

Rent adjustments on a cash flow statement often reflect changes in operating expenses that are passed through to tenants, directly impacting the landlord's net cash flow. One critical aspect of these adjustments is the mechanism of operating expense pass-throughs, where variable costs like property taxes, insurance, or maintenance are shifted to tenants, thereby increasing their rent obligations. This practice is common in commercial leases, where tenants agree to cover a portion of the building’s operating expenses in addition to base rent. While this arrangement can stabilize a landlord’s cash flow by offloading unpredictable costs, it also reduces the tenant’s net cash flow, as they bear the brunt of these increases.

Consider a scenario where a commercial property’s annual property taxes rise by $20,000 due to a reassessment. If the lease includes an operating expense pass-through clause, this increase is distributed among tenants based on their leased square footage. For a tenant occupying 20% of the building, their share would be $4,000, added to their annual rent. This adjustment appears on the landlord’s cash flow statement as an increase in rental income, but it simultaneously decreases the tenant’s available cash, highlighting the dual impact of such pass-throughs.

Analytically, operating expense pass-throughs serve as a risk-sharing mechanism between landlords and tenants. For landlords, they mitigate the volatility of variable costs, ensuring a more predictable cash flow. For tenants, however, they introduce uncertainty, as expenses like maintenance or taxes can fluctuate significantly. This dynamic underscores the importance of lease negotiation, where tenants should seek caps on pass-throughs or detailed expense breakdowns to manage their financial exposure.

From a practical standpoint, tenants can protect themselves by scrutinizing lease terms related to pass-throughs. For instance, insisting on an annual reconciliation statement ensures transparency in how expenses are allocated. Additionally, tenants in multi-use properties should verify that expenses are fairly apportioned, as common area maintenance costs, for example, should not be disproportionately passed to smaller tenants. Landlords, meanwhile, must balance the use of pass-throughs to avoid pricing tenants out of the market, as excessive rent increases can lead to vacancies and reduced overall cash flow.

In conclusion, operating expense pass-throughs are a double-edged sword in rent adjustments. While they stabilize landlord cash flow by shifting variable costs to tenants, they also reduce tenant net cash flow, creating a delicate equilibrium. Both parties must approach these clauses strategically, ensuring fairness and sustainability in their financial arrangements. By understanding this mechanism, stakeholders can better navigate the complexities of rent adjustments on cash flow statements.

Unpaid Rent: Understanding the Statute of Limitations for Landlords

You may want to see also

Explore related products

![]()

Rent Abatement: Temporary rent waivers during disruptions (e.g., renovations) create irregular cash flow patterns

Rent abatement, a temporary waiver or reduction of rent, often arises during property disruptions like renovations, natural disasters, or legal disputes. For tenants, this relief eases financial strain during periods when the property is unusable or diminished in value. However, for landlords, it introduces irregular cash flow patterns, complicating financial planning and reporting. These adjustments must be meticulously recorded on the cash flow statement to reflect the true liquidity position of the business.

Consider a commercial landlord managing a retail space undergoing a six-month renovation. During this period, the landlord agrees to waive 50% of the tenant’s rent. While the tenant benefits from reduced expenses, the landlord’s cash inflow decreases by $15,000 monthly. This reduction appears as a negative adjustment in the operating activities section of the cash flow statement, highlighting the temporary cash shortfall. Without proper documentation, stakeholders might misinterpret this as a decline in operational performance rather than a planned, temporary concession.

Analyzing the impact of rent abatement requires distinguishing between short-term cash flow irregularities and long-term financial health. For instance, if the renovation enhances the property’s value, the abatement could be a strategic investment. However, frequent or prolonged abatements may signal underlying issues, such as tenant dissatisfaction or property mismanagement. Investors and analysts must scrutinize these adjustments to assess whether they are isolated incidents or recurring trends affecting the landlord’s stability.

To manage rent abatement effectively, landlords should adopt proactive strategies. First, establish clear abatement policies in lease agreements, defining triggers (e.g., renovations, pandemics) and terms (duration, percentage waived). Second, maintain a reserve fund to offset temporary cash shortfalls, ensuring liquidity during disruptions. Third, communicate transparently with stakeholders, explaining abatements in financial statements and investor reports. For tenants, negotiating abatements in exchange for lease extensions or higher post-renovation rent can create a win-win scenario, stabilizing cash flow for both parties.

In conclusion, rent abatement serves as a practical tool for addressing temporary disruptions but demands careful financial management. By understanding its mechanics, documenting adjustments accurately, and implementing strategic mitigations, landlords and tenants can navigate these irregularities without compromising long-term financial health. Properly handled, rent abatement becomes not a liability, but a flexible mechanism for sustaining relationships and property value.

Are Water and Sewer Bills Included in Your Rent?

You may want to see also

Frequently asked questions

Rent adjustments on a cash flow statement refer to the reconciliation of rent expenses between the income statement (accrual basis) and the actual cash payments made during the period. This adjustment ensures the cash flow statement accurately reflects the cash outflow related to rent.

Rent adjustments are necessary because the income statement records rent expenses on an accrual basis, which may not align with actual cash payments. Adjustments ensure the cash flow statement reflects the true cash impact of rent, separating prepaid or deferred rent from current cash outflows.

Rent adjustments are calculated by subtracting the cash paid for rent during the period from the rent expense reported on the income statement. The difference accounts for prepaid rent (added back) or deferred rent (deducted) to reconcile the accrual-based expense to actual cash flow.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61gNC08X3PL._AC_UY218_.jpg)