Rent expense is typically considered an operating expense on a balance sheet, as it represents the cost of leasing property or equipment for business operations. Unlike capital expenditures, which are long-term investments, rent expense is a short-term cost incurred in the normal course of business. It is recorded on the income statement under operating expenses, reducing the company's net income for the period. On the balance sheet, rent expense does not appear directly, as it is not an asset or liability; however, prepaid rent or rent payable may be listed under current assets or current liabilities, respectively, depending on the timing of payments. Understanding how rent expense is treated in financial statements is crucial for accurately assessing a company's financial health and operational efficiency.

Explore related products

What You'll Learn

- Operating Expense Classification: Rent expense is categorized under operating expenses on the income statement

- Prepaid Rent Treatment: Prepaid rent is recorded as a current asset on the balance sheet

- Lease Accounting Impact: Rent under operating leases is not capitalized on the balance sheet

- Accrued Rent Liability: Unpaid rent is shown as a current liability on the balance sheet

- Capital Lease Differentiation: Rent for capital leases is recorded as an asset and liability

![]()

Operating Expense Classification: Rent expense is categorized under operating expenses on the income statement

Rent expense, a fundamental component of a company's financial obligations, is not directly listed on the balance sheet. Instead, its classification lies within the income statement, specifically under operating expenses. This categorization is crucial for understanding a company's financial health and operational efficiency.

Understanding the Income Statement's Role

The income statement, also known as the profit and loss statement, provides a snapshot of a company's revenue, expenses, and profitability over a specific period. It's here that rent expense finds its home, nestled among other operating expenses like salaries, utilities, and marketing costs. This grouping is intentional, as it reflects the ongoing, day-to-day costs associated with running a business.

Why Rent is an Operating Expense

Rent expense is classified as an operating expense because it’s a necessary and recurring cost directly tied to a company's core operations. For instance, a retail store's rent is essential for maintaining its physical presence and facilitating sales. Unlike capital expenditures, which involve long-term investments in assets, rent is a short-term commitment that doesn't contribute to the company's long-term growth in the same way.

Practical Implications for Financial Analysis

Analyzing rent expense as an operating expense allows investors and stakeholders to assess a company's operational efficiency. A high rent-to-revenue ratio, for example, might indicate that a company is overpaying for its space relative to its sales. Conversely, a low ratio could suggest efficient space utilization or strategic location choices.

Industry-Specific Considerations

It's worth noting that the significance of rent expense varies across industries. For a technology company with a primarily digital presence, rent might be a minor expense. In contrast, for a brick-and-mortar retailer or a manufacturing facility, rent can be a substantial portion of operating expenses. Understanding these industry-specific nuances is vital for accurate financial analysis and benchmarking.

Rent the Runway Stock Plunge: What Happened to My Investment?

You may want to see also

Explore related products

![]()

Prepaid Rent Treatment: Prepaid rent is recorded as a current asset on the balance sheet

Rent expense is typically categorized as an operating expense on the income statement, reflecting the cost of using a property over a specific period. However, when rent is paid in advance, it introduces a unique treatment on the balance sheet. Prepaid rent, which occurs when a tenant pays for future occupancy, is not immediately expensed. Instead, it is recorded as a current asset on the balance sheet, representing the value of rent that has been paid but not yet utilized.

This treatment aligns with the accounting principle of matching expenses with the period in which they are incurred. By recording prepaid rent as an asset, businesses ensure that the expense is recognized only when the rented space is actually used. For example, if a company pays $12,000 in January for six months of rent, $2,000 would be expensed each month as rent expense, while the remaining balance is gradually reduced on the balance sheet. This approach provides a more accurate representation of the company’s financial position and operational costs.

Recording prepaid rent as a current asset also enhances liquidity reporting, as it reflects cash that has been spent but retains future economic benefit. Current assets are expected to be consumed or converted into cash within one year, making prepaid rent a fitting inclusion. However, it’s crucial to distinguish prepaid rent from long-term prepaid expenses, which may extend beyond one year and could be classified differently. Proper classification ensures compliance with accounting standards and transparency for stakeholders.

To manage prepaid rent effectively, businesses should maintain a systematic process for tracking and amortizing these payments. This involves creating a prepaid rent account on the balance sheet and periodically transferring the appropriate portion to the income statement as rent expense. For instance, using accounting software can automate this process, reducing the risk of errors and ensuring consistency. Regular reviews of prepaid rent balances are also advisable to verify accuracy and alignment with lease agreements.

In conclusion, prepaid rent treatment as a current asset on the balance sheet is a critical aspect of financial reporting. It ensures expenses are matched with the periods they benefit, maintains accurate liquidity reporting, and adheres to accounting principles. By understanding and properly managing prepaid rent, businesses can improve financial transparency and decision-making, ultimately contributing to their long-term success.

Rent and Taxes: What You Need to Report

You may want to see also

Explore related products

![]()

Lease Accounting Impact: Rent under operating leases is not capitalized on the balance sheet

Rent expense under operating leases is treated as an operating expense on the income statement, not as an asset or liability on the balance sheet. This accounting treatment stems from the nature of operating leases, which are essentially rental agreements where the lessee does not assume ownership or significant risks and rewards of the leased asset. Instead of capitalizing the lease, the lessee records rent payments as they are incurred, reflecting the immediate outflow of cash without altering the balance sheet. This approach simplifies financial reporting but can obscure the true extent of a company’s long-term obligations.

Consider a retail company leasing storefront space under a 10-year operating lease. Despite the long-term commitment, the rent payments are expensed monthly on the income statement, reducing net income. Meanwhile, the balance sheet remains unchanged, showing no asset for the right to use the property or liability for future payments. This contrasts with finance leases, where the lessee recognizes a right-of-use asset and lease liability. The operating lease treatment prioritizes liquidity and avoids overstating assets, but it may underrepresent the company’s financial commitments to stakeholders.

The impact of this accounting method extends beyond the balance sheet. By expensing rent immediately, operating leases can depress profitability metrics like EBITDA, which may mislead investors or lenders. For instance, a company with significant operating leases might appear less profitable than a peer with similar operations but owned assets. Conversely, this treatment can improve cash flow from operations, as rent payments are not treated as financing activities. Companies must therefore provide disclosures about future lease commitments in the footnotes to ensure transparency.

Practical implications arise for financial analysis. Analysts must adjust reported metrics to assess a company’s true financial health. For example, adding back rent expense to EBITDA can provide a clearer picture of operational performance. Additionally, companies with substantial operating leases may face higher financial risk if cash flows become constrained, as rent obligations are fixed and immediate. Understanding this treatment is crucial for accurate valuation and risk assessment, particularly in industries like retail or aviation, where leasing is prevalent.

In summary, rent under operating leases is not capitalized on the balance sheet but expensed as incurred. This treatment simplifies reporting but can distort financial metrics and obscure long-term obligations. Stakeholders must scrutinize footnotes and adjust analyses to account for this nuance. While the approach aligns with the short-term nature of operating leases, it underscores the importance of supplemental disclosures in conveying a complete financial picture.

Rent-to-Own Repossession: What Happens When They Take Your Stuff?

You may want to see also

Explore related products

![]()

Accrued Rent Liability: Unpaid rent is shown as a current liability on the balance sheet

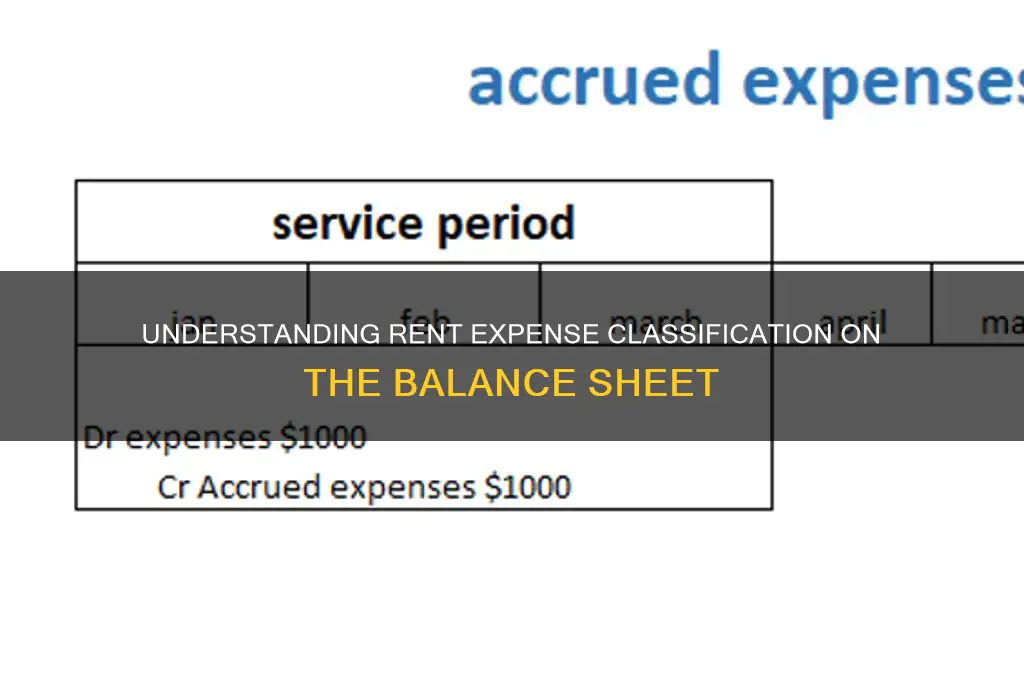

Rent expense, a fundamental component of a company's financial obligations, is not merely a line item on the income statement; it has a direct impact on the balance sheet, particularly when rent remains unpaid. Accrued rent liability is a critical concept in accounting, representing the amount of rent owed by a tenant but not yet paid to the landlord. This liability is a short-term obligation, typically due within one year or less, and is classified as a current liability on the balance sheet.

In the context of financial reporting, accrued rent liability serves as a snapshot of a company's outstanding rent obligations at a specific point in time. For instance, consider a retail business that occupies a commercial space under a lease agreement. If the rent for the last month of the quarter has not been paid by the balance sheet date, the accrued rent liability account would reflect this unpaid amount. This ensures that the company's financial statements accurately represent its financial position, providing stakeholders with a clear understanding of its short-term obligations.

From an analytical perspective, the treatment of accrued rent liability as a current liability highlights the importance of matching expenses with the period in which they are incurred. This principle, known as the matching principle, is a cornerstone of accrual accounting. By recognizing unpaid rent as a liability, companies can more accurately reflect their financial health and avoid overstating their assets or understating their obligations. For example, a company with a significant accrued rent liability may need to reassess its cash flow management strategies to ensure it can meet its short-term obligations.

To effectively manage accrued rent liability, businesses should implement robust accounting practices. This includes maintaining a detailed rent schedule, tracking lease agreements, and regularly reconciling rent payments. For instance, a property management company overseeing multiple rental properties can utilize accounting software to automate rent tracking, generate reminders for upcoming payments, and produce accurate financial reports. By doing so, they can minimize the risk of overlooking unpaid rent and ensure compliance with accounting standards.

In comparison to other current liabilities, such as accounts payable or accrued wages, accrued rent liability is unique in that it often involves a fixed, recurring obligation. This predictability allows companies to forecast their short-term cash outflows more accurately. However, it also underscores the need for careful planning, especially for businesses operating in industries with seasonal fluctuations or uncertain revenue streams. By recognizing and addressing accrued rent liability proactively, companies can maintain a healthy financial position and avoid potential cash flow crises.

In conclusion, accrued rent liability is a vital aspect of financial reporting, providing a clear picture of a company's unpaid rent obligations. Its classification as a current liability on the balance sheet emphasizes the importance of accurate and timely financial reporting. By understanding and effectively managing this liability, businesses can ensure compliance with accounting principles, make informed decisions, and maintain the trust of stakeholders. Practical steps, such as implementing robust accounting systems and regularly reviewing rent schedules, can help companies stay on top of their rent obligations and contribute to their overall financial stability.

Rent Your GPU Power to Pixar: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Capital Lease Differentiation: Rent for capital leases is recorded as an asset and liability

Rent expense typically appears on the income statement, reflecting the cost of using leased assets over time. However, capital leases diverge from this norm, introducing a unique accounting treatment that impacts the balance sheet. Unlike operating leases, where rent payments are expensed directly, capital leases are treated as financed purchases. This distinction stems from the lease’s economic substance, often characterized by long-term commitments, transfer of ownership, or bargain purchase options. As a result, the lessee records the present value of future lease payments as both an asset (right-of-use asset) and a liability (lease obligation) on the balance sheet.

This dual-entry approach aligns with the principle of recognizing the economic reality of the transaction. The asset represents the lessee’s right to use the leased property over the lease term, while the liability reflects the obligation to make future payments. For example, if a company enters a 10-year capital lease for equipment with annual payments of $50,000 and a present value of $400,000, it would record a $400,000 asset and a $400,000 liability. Over time, the asset is depreciated, and the liability is reduced as payments are made, ensuring the balance sheet accurately reflects the lease’s financial impact.

The differentiation between capital and operating leases is critical for financial analysis. Capital leases increase both assets and liabilities, potentially affecting leverage ratios and liquidity metrics. Analysts and stakeholders must scrutinize lease disclosures to understand the true financial position of a company. For instance, a high proportion of capital leases may indicate significant long-term obligations, while operating leases suggest more flexibility. This transparency is particularly important under accounting standards like ASC 842 or IFRS 16, which mandate the capitalization of all leases except short-term or low-value ones.

Practical application of this concept requires careful lease classification. Companies should assess lease terms against criteria such as lease term (e.g., exceeding 75% of the asset’s useful life) or present value (e.g., exceeding 90% of the asset’s fair value). Misclassification can lead to material misstatements in financial statements. For example, incorrectly treating a capital lease as an operating lease would understate assets and liabilities, distorting key financial ratios. Thus, accounting teams must stay vigilant and adhere to standards to ensure accurate reporting.

In summary, capital leases transform rent expense into a balance sheet item by recording it as both an asset and a liability. This treatment reflects the lease’s economic substance as a financed purchase rather than a rental agreement. By understanding this differentiation, businesses and analysts can better interpret financial statements, assess long-term obligations, and make informed decisions. Mastery of this concept is essential for compliance with modern accounting standards and for maintaining financial transparency.

Renting a Food Truck for Catering: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Rent expense is not directly listed on the balance sheet. It is recorded as an expense on the income statement, reducing net income. However, prepaid rent (rent paid in advance) may appear as a current asset on the balance sheet until it is expensed over time.

Rent expense indirectly affects the balance sheet through changes in retained earnings (if the business is profitable) or cash balances (if rent is paid). Prepaid rent is the only direct rent-related item that may appear as an asset on the balance sheet.

Rent expense is not a liability because it represents an expense already incurred or paid. Future rent obligations (e.g., under a lease agreement) may be classified as a liability, but the expense itself is recorded on the income statement.