Rent paid less 10% of salary refers to a financial concept where an individual’s housing expense is capped at 10% of their total earnings. This principle is often used as a budgeting guideline to ensure that a significant portion of income is not disproportionately allocated to rent, allowing for better financial management and savings. For example, if someone earns $5,000 per month, their rent should ideally not exceed $500. This approach helps individuals maintain a balanced budget, avoid financial strain, and prioritize other essential expenses or savings goals. It is particularly relevant in personal finance planning and discussions about affordable living.

Explore related products

What You'll Learn

- Rent-to-Income Ratio: Calculating affordability by comparing monthly rent to 10% of gross salary

- Budgeting Tips: Strategies to manage finances when rent exceeds 10% of earnings

- Housing Affordability: Understanding the impact of rent on overall financial stability

- Salary Allocation: How to prioritize expenses when rent consumes a significant portion of income

- Alternative Housing Options: Exploring cheaper living arrangements to stay within the 10% rent threshold

![]()

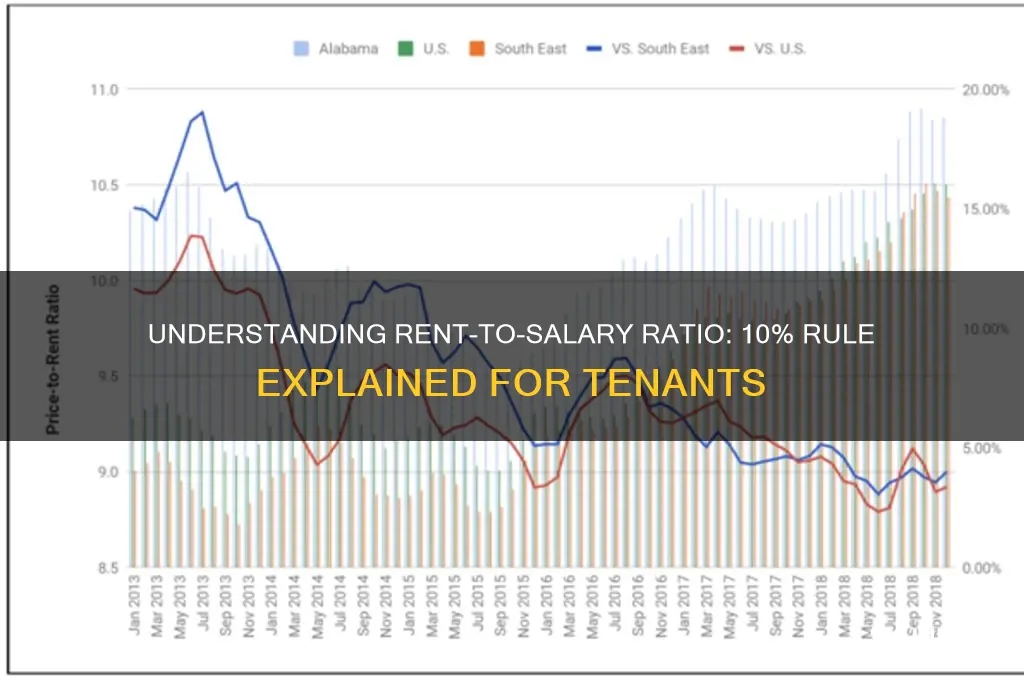

Rent-to-Income Ratio: Calculating affordability by comparing monthly rent to 10% of gross salary

A common rule of thumb in personal finance suggests that rent should not exceed 30% of one's gross monthly income. However, a more conservative approach, often favored by financial advisors, is to limit rent to 10% of gross salary. This stricter guideline, known as the rent-to-income ratio, offers a buffer against financial strain, ensuring that a significant portion of income remains available for savings, investments, and other expenses. For instance, an individual earning $60,000 annually (or $5,000 monthly) would aim to keep rent below $500, a stark contrast to the $1,500 allowed by the 30% rule. This method forces a reevaluation of lifestyle choices and housing priorities, often leading to more sustainable financial decisions.

To calculate this ratio, divide your monthly rent by 10% of your gross monthly salary. For example, if your monthly income is $4,000 and your rent is $600, the ratio is 1.5 ($600 ÷ ($4,000 * 0.10)). A ratio above 1 indicates that rent exceeds the 10% threshold, signaling potential financial strain. This calculation is particularly useful for young professionals or those in high-cost urban areas, where adhering to the 30% rule might still lead to overspending. By aiming for a ratio of 1 or below, individuals can build financial resilience and avoid the pitfalls of living paycheck to paycheck.

Critics argue that the 10% rule is impractical in cities like New York or San Francisco, where median rents often surpass 50% of average incomes. However, this critique highlights the rule’s purpose: to encourage reevaluation of housing choices rather than to dictate impossibility. For instance, opting for a smaller apartment, moving to a less expensive neighborhood, or considering roommates can align rent with this stricter guideline. The 10% rule serves as a financial reality check, prompting individuals to prioritize long-term stability over short-term comfort.

Implementing this ratio requires discipline and planning. Start by assessing your current rent-to-income ratio and identifying areas for adjustment. If your rent exceeds 10% of your income, consider negotiating with your landlord, downsizing, or increasing your income through side gigs or promotions. For those in the housing market, this rule can guide decisions on mortgage affordability, ensuring that monthly payments remain within the 10% threshold. While challenging, adhering to this ratio fosters financial independence and prepares individuals for unexpected expenses or economic downturns.

Ultimately, the rent-to-income ratio of 10% is not a one-size-fits-all solution but a tool for fostering financial mindfulness. It challenges individuals to rethink their relationship with housing, emphasizing affordability over extravagance. By adopting this approach, one can build a robust financial foundation, ensuring that rent remains a manageable expense rather than a burdensome obligation. Whether you’re a recent graduate or a seasoned professional, this ratio offers a clear, actionable framework for achieving long-term financial health.

Renting Out a Condo: Easy or Challenging? What to Expect

You may want to see also

Explore related products

![]()

Budgeting Tips: Strategies to manage finances when rent exceeds 10% of earnings

Rent consuming more than 10% of your income can strain your finances, leaving little room for savings, investments, or leisure. This imbalance often forces individuals to compromise on other essential expenses or rely on debt. To regain control, consider these targeted strategies that address both immediate and long-term financial health.

Step 1: Audit Your Expenses Relentlessly

Begin by categorizing every expense for the past three months. Use budgeting apps like Mint or YNAB to track spending automatically. Identify non-essential costs (e.g., subscription bloat, dining out) that can be reduced or eliminated. For instance, cutting a $5 daily coffee habit saves $1,825 annually—funds that could offset rent overages. Prioritize needs over wants, and allocate savings to a "rent buffer" account to ease monthly pressure.

Step 2: Negotiate or Optimize Housing Costs

If rent exceeds 10% of your income, renegotiate lease terms or explore alternatives. Offer to sign a longer lease in exchange for a rent reduction, or propose taking on minor property management tasks (e.g., landscaping) for a discount. Alternatively, consider downsizing, moving to a less expensive neighborhood, or temporarily sharing housing with roommates. For example, reducing rent by $200 monthly frees up $2,400 annually, equivalent to 12% of a $20,000 salary.

Step 3: Increase Income Strategically

Supplement your primary earnings with side gigs tailored to your skills and time availability. Freelancing, tutoring, or selling unused items can generate $200–$500 monthly. For instance, a graphic designer earning $30/hour could add $480 by working 16 hours monthly. Allocate 70% of this extra income to rent, 20% to savings, and 10% to discretionary spending to maintain balance.

Caution: Avoid Common Pitfalls

Resist the temptation to rely on high-interest debt (e.g., credit cards) to cover rent gaps, as this compounds financial stress. Similarly, avoid neglecting emergency funds—aim to save at least $500 initially, even if rent exceeds 10% of your income. Ignoring this safety net leaves you vulnerable to unexpected expenses, perpetuating the cycle of financial instability.

Managing rent that surpasses 10% of earnings requires discipline, creativity, and proactive planning. By auditing expenses, optimizing housing costs, and boosting income, you can reduce financial strain while building a foundation for future stability. Remember, small adjustments today yield significant dividends tomorrow.

Scooter Rentals in Bermuda: Safety Tips and What You Need to Know

You may want to see also

Explore related products

![]()

Housing Affordability: Understanding the impact of rent on overall financial stability

Rent consuming more than 30% of gross income is widely recognized as a threshold for financial strain, yet the concept of capping rent at 10% of salary presents a more aggressive, stability-focused approach. This principle, often advocated in personal finance circles, challenges conventional budgeting norms by prioritizing savings, investments, and debt repayment over housing costs. For instance, an individual earning $50,000 annually would allocate no more than $416.67 monthly to rent, a figure that may seem unrealistic in high-cost urban areas but underscores the importance of aligning housing expenses with long-term financial goals.

Analyzing this approach reveals both its merits and limitations. On one hand, limiting rent to 10% of salary fosters financial resilience by freeing up resources for emergencies, retirement, and wealth accumulation. For example, a household saving the difference between 30% and 10% of income could redirect $1,250 monthly (based on a $50,000 salary) toward high-interest debt or investments, potentially yielding thousands in returns over time. On the other hand, this model may necessitate lifestyle adjustments, such as relocating to lower-cost areas, downsizing, or adopting shared living arrangements, which may not align with personal or professional priorities.

To implement this strategy, start by calculating your 10% rent threshold and comparing it to current housing costs. If there’s a gap, explore actionable steps like negotiating rent, seeking roommate arrangements, or moving to more affordable neighborhoods. For instance, a $40,000 earner could target rent under $333 monthly, a goal achievable in certain markets or through subsidized housing programs. Caution, however, against compromising safety or essential needs in pursuit of this ideal.

Persuasively, this 10% rule serves as a financial litmus test, encouraging individuals to question societal norms around housing consumption. While it may not be feasible for everyone, particularly in cities like San Francisco or New York, it prompts a critical reevaluation of trade-offs between immediate comfort and future security. For young professionals or those in early career stages, adopting this mindset can lay the foundation for a lifetime of financial independence, even if the 10% target is gradually approached rather than immediately achieved.

In conclusion, the 10% rent-to-salary ratio is less about rigid adherence and more about fostering a mindset that prioritizes financial stability over housing extravagance. By treating rent as a variable expense rather than a fixed burden, individuals can reclaim control over their financial destinies, one budgeting decision at a time. Whether viewed as aspirational or practical, this framework challenges us to rethink the role of housing in our financial lives.

Rent-a-Center Phones: Compatible with All Carriers?

You may want to see also

Explore related products

![]()

Salary Allocation: How to prioritize expenses when rent consumes a significant portion of income

Rent consuming more than 30% of your income can cripple your financial flexibility, leaving little room for other essentials, let alone savings or leisure. This scenario, often dubbed "rent burden," disproportionately affects younger adults and those in high-cost urban areas. For instance, a 25-year-old earning $4,000 monthly, paying $1,400 in rent, is already at 35%—well above the recommended threshold. When rent eclipses this mark, prioritizing expenses becomes less about preference and more about survival.

Step 1: Trim Non-Essentials Relentlessly

Start by dissecting discretionary spending. Streaming services, dining out, and impulse purchases are low-hanging fruit. For example, canceling two $15 subscriptions and reducing weekly takeout from three to one saves $120 monthly. Redirect these funds to high-interest debt or emergency savings. Use budgeting apps like Mint or YNAB to track progress, ensuring every dollar not allocated to rent serves a critical purpose.

Step 2: Negotiate Fixed Costs

Rent may dominate, but other fixed expenses can be renegotiated. Call insurance providers to adjust coverage or shop for cheaper plans—a $20 monthly reduction in car insurance adds up. Similarly, switch to no-fee bank accounts or negotiate lower interest rates on credit cards. For utilities, leverage energy-saving habits (e.g., LED bulbs, unplugging devices) to shrink bills by 10–15%.

Step 3: Allocate the "Less 10%" Strategically

If rent already exceeds 30%, aim to keep all other expenses under 10% of your salary. For the $4,000 earner, that’s $400. Divide this into categories: $150 for groceries, $100 for transportation, $50 for utilities, and $100 for miscellaneous. This forces discipline and highlights areas for further cuts. For instance, meal-prepping can slash grocery costs by 30%, freeing up funds for unexpected expenses.

Caution: Avoid Debt Traps

When rent overwhelms, the temptation to rely on credit cards or payday loans escalates. A $500 payday loan with a 400% APR can spiral into $2,000 in six months. Instead, explore community resources like food banks or low-interest emergency loans from credit unions. Building a $500 emergency fund, even in $20 increments, provides a safety net without debt.

Prioritizing expenses with high rent requires constant reassessment. Quarterly budget reviews ensure alignment with income changes or cost-of-living increases. For those in high-rent areas, consider roommates or relocating to a more affordable neighborhood. Ultimately, the goal isn’t to eliminate spending but to ensure every dollar supports long-term financial stability, even when rent feels insurmountable.

Understanding Healthy Rent-to-Own Ratios: A Smart Homeownership Strategy

You may want to see also

Explore related products

![]()

Alternative Housing Options: Exploring cheaper living arrangements to stay within the 10% rent threshold

Housing costs consume a staggering 30-50% of income for many, far exceeding the recommended 10% threshold. This imbalance forces individuals to compromise on savings, investments, and overall financial stability. To reclaim control, exploring alternative housing options becomes imperative. Let's delve into innovative solutions that challenge traditional renting models and offer pathways to more affordable living.

Co-living spaces present a compelling solution, blending affordability with community. Imagine shared living areas, fully furnished private rooms, and utilities bundled into a single, predictable cost. These spaces cater to young professionals, digital nomads, and those seeking a sense of belonging. Platforms like Bungalow and Common offer curated co-living experiences, often with flexible lease terms and amenities like gyms and coworking spaces. While privacy may be limited, the financial savings and built-in social network make co-living an attractive option for those prioritizing community and cost-effectiveness.

House hacking, a strategy gaining traction, involves leveraging your primary residence to generate income. This can be achieved through renting out spare rooms, converting basements or garages into separate units, or even hosting short-term rentals via platforms like Airbnb. For instance, a homeowner with a 3-bedroom house might rent out two rooms, effectively reducing their housing costs to near zero. However, this approach requires careful consideration of local regulations, maintenance responsibilities, and the potential impact on personal space.

Tiny homes and modular housing offer a radical departure from conventional living spaces, emphasizing minimalism and sustainability. These compact dwellings, typically ranging from 100 to 400 square feet, can be purchased or built at a fraction of the cost of a traditional home. Communities like Spur in Texas and Simplicity in Oregon provide infrastructure and a sense of belonging for tiny home enthusiasts. While downsizing to this extent may not suit everyone, it presents a viable path to homeownership and financial freedom for those willing to embrace a simpler lifestyle.

Negotiating rent and exploring non-traditional leases can yield surprising savings. Many renters overlook the possibility of negotiating their monthly payment, especially in competitive markets. Offering to sign a longer lease, prepaying rent, or taking on minor maintenance responsibilities can incentivize landlords to reduce costs. Additionally, considering month-to-month leases or subletting arrangements can provide flexibility and potentially lower rates. These strategies require research, communication, and a willingness to think outside the box, but they can significantly contribute to staying within the 10% rent threshold.

Jeep Rentals on Big Island: 4-Wheel Drive Adventures

You may want to see also

Frequently asked questions

This phrase refers to a situation where the amount of rent paid by an individual is reduced by 10% of their salary. It is often used in financial planning or budgeting to determine affordability.

To calculate this, first determine 10% of the individual's salary, then subtract that amount from the total rent paid. For example, if the salary is $5,000 and rent is $1,500, 10% of the salary is $500, so the calculation would be $1,500 - $500 = $1,000.

This concept is important because it helps individuals assess whether their rent is affordable relative to their income. By reducing rent by 10% of their salary, it provides a buffer for other expenses and savings, ensuring financial stability and preventing over-commitment to housing costs.