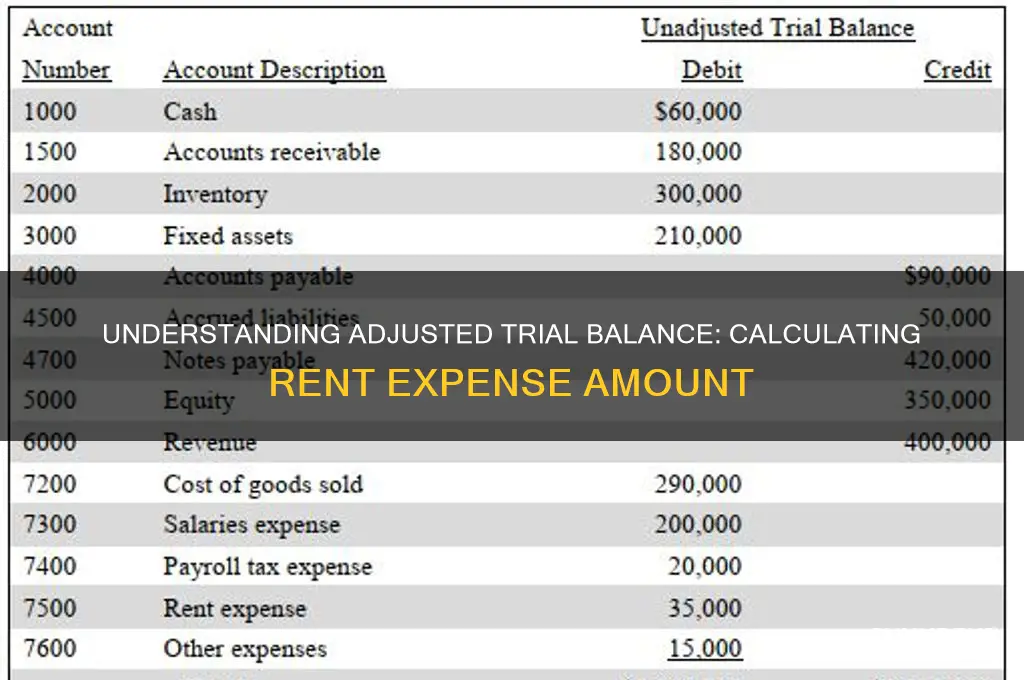

The adjusted trial balance is a critical financial statement that reflects the balances of all accounts after adjusting entries have been made, providing a more accurate representation of a company's financial position. When examining the adjusted trial balance, the amount for rent expense is a key figure that represents the total cost of renting property or space over a specific accounting period, adjusted for any accruals, prepayments, or other necessary corrections. Understanding the adjusted trial balance amount for rent expense is essential for assessing a company's operating costs, cash flow, and overall financial health, as it directly impacts the income statement and can influence decision-making regarding budgeting, leasing agreements, and long-term financial planning.

Explore related products

What You'll Learn

- Rent Expense Calculation: Determine total rent paid during the accounting period for accurate reporting

- Adjusting Entries: Record prepaid or accrued rent to reflect correct expense timing

- Trial Balance Inclusion: Ensure rent expense is properly listed in the trial balance

- Verification Process: Cross-check rent expense with lease agreements and payment records

- Final Adjustment: Confirm the adjusted trial balance amount matches actual rent expense

![]()

Rent Expense Calculation: Determine total rent paid during the accounting period for accurate reporting

Accurate rent expense reporting hinges on a meticulous calculation of total rent paid during the accounting period. This seemingly straightforward task can unravel without a structured approach, leading to discrepancies that ripple through financial statements.

Simply put, every dollar of rent paid must be accounted for, regardless of when the invoice was received or the payment due date.

Identifying Rent Payments: The first step is to gather all rent-related documents for the period. This includes lease agreements, invoices, receipts, and bank statements reflecting rent payments. Scrutinize these documents to ensure every payment is captured, even if it pertains to a partial period (e.g., a prorated rent payment for a mid-month move-in).

Some leases may include additional charges like common area maintenance (CAM) fees or property taxes. While these may be bundled with rent, they should be segregated into their respective expense categories for accurate financial reporting.

Matching Payments to the Period: Rent expense is recognized in the period it is incurred, not necessarily when it is paid. This principle, known as accrual accounting, requires adjusting entries if rent payments span multiple periods. For example, if rent is paid quarterly in advance, only the portion applicable to the current accounting period should be expensed, with the remainder recorded as a prepaid asset. Conversely, if rent is paid in arrears, an accrued expense must be recorded to reflect the obligation incurred during the period.

A helpful tool is a rent schedule, detailing payment dates, amounts, and the corresponding expense recognition periods. This schedule ensures consistency and facilitates year-end adjustments.

Adjusting for Prepayments and Accruals: Adjusting entries are crucial for aligning rent expense with the matching principle. If rent is prepaid, an adjusting entry debits Rent Expense and credits Prepaid Rent for the portion applicable to the current period. Conversely, if rent is accrued, the adjusting entry debits Rent Expense and credits Rent Payable for the amount incurred but not yet paid.

Verifying Accuracy: Cross-referencing the calculated rent expense with the lease agreement and bank statements is essential for accuracy. Any discrepancies should be investigated and resolved promptly. Additionally, comparing the current period's rent expense to previous periods can highlight anomalies or potential errors.

By meticulously following these steps, businesses can ensure their adjusted trial balance reflects the true rent expense for the accounting period, contributing to the overall integrity of their financial statements.

Smart Budgeting Tips for Living Comfortably on a $40k Salary

You may want to see also

Explore related products

![]()

Adjusting Entries: Record prepaid or accrued rent to reflect correct expense timing

Rent expense is a critical line item on the income statement, yet its accuracy often hinges on proper timing. Prepaid and accrued rent are common scenarios that require adjusting entries to align the expense with the period it benefits. For instance, if a company pays $12,000 in January for a year’s rent, recording the entire amount as an expense in January distorts financial statements. Instead, adjusting entries allocate $1,000 monthly to reflect the expense over the year. This ensures the matching principle is upheld, where expenses are recognized in the same period as the revenues they help generate.

To record prepaid rent, assume a company pays $6,000 upfront for six months of rent starting July 1. Initially, the journal entry debits Prepaid Rent (an asset) and credits Cash for $6,000. At month-end, an adjusting entry is needed to recognize one month’s rent expense. Debit Rent Expense for $1,000 and credit Prepaid Rent for $1,000. This reduces the prepaid asset while correctly timing the expense. Without this adjustment, the income statement would underreport rent expense, and the balance sheet would overstate prepaid rent.

Accrued rent, conversely, occurs when rent is owed but unpaid. Suppose a company occupies space in December but pays rent in January. By December 31, an adjusting entry is required to recognize the expense. Debit Rent Expense for the monthly amount (e.g., $1,000) and credit Rent Payable (a liability). This ensures the expense is reflected in the correct period, even if payment occurs later. Omitting this adjustment would understate both expenses and liabilities, misleading stakeholders about financial obligations.

Practical tips for handling these adjustments include maintaining a rent schedule detailing payment dates, amounts, and periods covered. Reconcile prepaid rent accounts monthly to ensure balances align with unexpired periods. For accrued rent, verify lease agreements to confirm payment terms and due dates. Automation tools can streamline these processes, reducing errors and saving time. Properly adjusted rent expenses not only comply with accounting standards but also provide a clearer picture of financial performance and obligations.

In conclusion, adjusting entries for prepaid and accrued rent are essential for accurate financial reporting. They ensure expenses are recognized in the periods they relate to, adhering to the matching principle. By systematically recording these adjustments, businesses maintain transparency, reliability, and compliance in their financial statements. Whether dealing with prepaid or accrued rent, the goal remains the same: to reflect the true economic reality of operations in the correct accounting period.

Mastering Monthly Budgeting: Strategies When Rent Consumes Your Income

You may want to see also

Explore related products

![]()

Trial Balance Inclusion: Ensure rent expense is properly listed in the trial balance

Rent expense is a critical component of a company's financial statements, yet it’s often mishandled in the trial balance due to misclassification or timing errors. Proper inclusion ensures accurate financial reporting and compliance with accounting principles. To verify its presence, cross-reference the general ledger account for rent expense with the trial balance. If the amount matches and aligns with the accounting period, the expense is correctly listed. Discrepancies require immediate investigation to avoid misstated financial statements.

Inclusion of rent expense in the trial balance demands adherence to the matching principle, which dictates that expenses be recognized in the period they are incurred, not paid. For example, if a company pays $12,000 annually for rent in January but records it monthly, $1,000 should appear in the trial balance each month. Failure to allocate the expense correctly distorts monthly financial performance. Use adjusting entries to rectify prepayments or accruals, ensuring the trial balance reflects the true economic activity of the period.

A common pitfall is misclassifying rent expense as a prepaid asset or lumping it with other operating expenses. Rent is a distinct operating expense and should be listed separately in the trial balance for transparency. For instance, if a company pays $5,000 in advance for six months of rent, $4,000 should remain as a prepaid asset at month-end, with $1,000 recorded as rent expense. Clear separation prevents overstatement of expenses and ensures stakeholders can accurately assess financial health.

To ensure proper inclusion, follow a systematic approach: first, review lease agreements to confirm rent amounts and payment schedules. Second, reconcile the rent expense account in the general ledger with supporting documentation, such as invoices or bank statements. Third, perform a trial balance review, focusing on the rent expense line item. Finally, address any discrepancies through adjusting entries before finalizing financial statements. This methodical process minimizes errors and reinforces the reliability of the trial balance.

The adjusted trial balance amount for rent expense should reflect both accuracy and consistency with accounting standards. For example, a retail business leasing a storefront for $3,000 monthly must ensure this amount appears in the trial balance each month, adjusted for any prepaid or accrued amounts. By maintaining meticulous records and applying sound accounting practices, companies can confidently assert that rent expense is properly listed, contributing to a credible and compliant financial narrative.

Rent-to-Own Simplified: Understanding the Process and Benefits

You may want to see also

Explore related products

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/811AGIXv7PL._AC_UL320_.jpg)

![]()

Verification Process: Cross-check rent expense with lease agreements and payment records

The verification process for rent expense is a critical step in ensuring the accuracy of financial statements. By cross-referencing lease agreements and payment records, accountants can identify discrepancies, omissions, or errors that may have occurred during the initial recording of transactions. This process not only validates the reported rent expense but also strengthens internal controls, reducing the risk of fraud or misstatement.

Step-by-Step Verification

Begin by obtaining the latest lease agreements for all rented properties. These documents serve as the primary source of truth for rent terms, including base rent, escalation clauses, and payment schedules. Next, compare the agreed-upon amounts and payment frequencies with the recorded rent expenses in the trial balance. For instance, if a lease stipulates a monthly rent of $2,500, ensure that this amount is consistently reflected in the accounting records. Discrepancies, such as overstated or understated expenses, should be investigated promptly.

Analyzing Payment Records

Payment records, including bank statements and receipts, provide concrete evidence of actual rent payments. Cross-check these records against both the lease agreements and the trial balance. For example, if a payment record shows a $3,000 payment for a particular month but the lease agreement specifies $2,500, the additional $500 could indicate a one-time maintenance fee or an error in recording. Ensure that such variances are properly documented and adjusted in the trial balance.

Cautions and Common Pitfalls

One common pitfall is overlooking prorated rent or partial payments, especially during lease inception or termination months. For instance, if a lease begins mid-month, the rent expense should be prorated accordingly. Failure to account for this can lead to material misstatements. Additionally, be wary of prepaid rent or rent holidays, which may require adjustments to the trial balance. Always verify that these special terms are accurately reflected in both the lease agreement and payment records.

A thorough verification process not only ensures the adjusted trial balance amount for rent expense is accurate but also enhances the reliability of financial reporting. Implement a systematic approach by creating a checklist of lease agreements and payment records for each property. Regularly reconcile these documents with the trial balance, especially during month-end or year-end closings. By adopting these practices, organizations can maintain transparency, comply with accounting standards, and provide stakeholders with trustworthy financial information.

Is Zillow Free for Rental Ads? A Complete Guide for Landlords

You may want to see also

Explore related products

![]()

Final Adjustment: Confirm the adjusted trial balance amount matches actual rent expense

The final adjustment phase is critical in ensuring financial accuracy, particularly when reconciling rent expense. After all preliminary adjustments, the adjusted trial balance should reflect the true financial position regarding rent payments. This step is not merely procedural; it’s a safeguard against errors that could distort financial reporting. By confirming that the adjusted trial balance matches actual rent expense, businesses can maintain credibility with stakeholders and comply with accounting standards.

To execute this step effectively, begin by cross-referencing the adjusted trial balance with source documents such as lease agreements, rent invoices, and payment receipts. For instance, if a company pays $2,000 monthly rent, the adjusted trial balance should show this amount under rent expense for the period. Discrepancies, even minor ones, warrant investigation. Common issues include omitted entries, incorrect accruals, or misclassified expenses. For example, a prepaid rent adjustment might have been overlooked, leading to an understatement of the expense.

A practical tip is to use a reconciliation worksheet to systematically compare the adjusted trial balance with actual rent payments. List all rent transactions for the period, including prepayments and accruals, and ensure they align with the balance sheet and income statement entries. This methodical approach reduces the risk of oversight and provides a clear audit trail. For businesses with multiple leases, categorize expenses by property or department to streamline verification.

While reconciling, be cautious of timing differences between cash payments and expense recognition. Accrual accounting requires rent expense to be matched with the period it benefits, not necessarily when it’s paid. For example, if rent for December is paid in November, the expense should still be recorded in December. Misalignment here can lead to material misstatements. Leveraging accounting software with automated accrual features can mitigate such errors, but manual review remains essential.

In conclusion, confirming that the adjusted trial balance matches actual rent expense is a non-negotiable step in financial reporting. It ensures accuracy, transparency, and compliance, fostering trust among investors, auditors, and management. By adopting a structured approach, leveraging tools, and staying vigilant about timing differences, businesses can achieve a seamless final adjustment. This process not only validates the integrity of financial statements but also reinforces the importance of meticulous bookkeeping in maintaining fiscal health.

Renting a Store in Crown Casino: A Comprehensive Guide

You may want to see also

Frequently asked questions

The adjusted trial balance amount for rent expense is the final balance after all adjustments, such as prepaid rent amortization or accrued rent, have been recorded in the accounting period.

It is calculated by starting with the unadjusted trial balance for rent expense and then adding or subtracting any adjusting entries related to rent, such as prepaid rent or accrued rent.

The adjusted trial balance amount differs because it includes corrections for timing differences, such as prepaid rent being expensed over time or rent owed but not yet paid being accrued.

The adjusted trial balance amount for rent expense is not directly shown in financial statements but is reflected in the income statement under operating expenses after adjustments are made.