Determining annual income based solely on rent can be complex, as it depends on various factors such as location, lifestyle, and financial obligations. If your monthly rent is $1,200, it typically represents a significant portion of your income, often recommended to be around 30% or less of your total earnings. To estimate your annual income, you might consider that $1,200 in monthly rent could imply a yearly income of approximately $48,000, assuming rent accounts for 30% of your earnings. However, this is a rough estimate, and actual income could vary widely based on individual circumstances, including other expenses, savings goals, and debt obligations. For a more accurate assessment, it’s essential to evaluate your overall financial situation and consider consulting a financial advisor.

| Characteristics | Values |

|---|---|

| Recommended Annual Income | $48,000 - $60,000 (based on 30% rent-to-income ratio) |

| Monthly Income | $4,000 - $5,000 |

| Rent-to-Income Ratio | 25% - 30% (ideal range) |

| Monthly Rent | $1,200 |

| Annual Rent | $14,400 |

| Common Budget Rule | 30% of income should not exceed rent (e.g., $1,200 ÷ 0.3 = $4,000/mo) |

| Minimum Annual Income | $48,000 (based on 30% rule: $1,200 × 12 ÷ 0.3) |

| Maximum Affordable Rent | $1,200 (if income is $48,000 or higher) |

| Gross Income Multiplier | 40x monthly rent (e.g., $1,200 × 40 = $48,000) |

| Regional Variations | Income requirements may vary by city/state (e.g., higher in NYC, SF) |

| Additional Expenses | Utilities, groceries, transportation, etc. (not included in rent) |

| Savings Recommendation | 20% of income after rent and essentials |

| Debt-to-Income Ratio | Ideally below 36% (including rent and other debts) |

| Emergency Fund | 3-6 months of living expenses (including rent) |

| Source of Data | HUD guidelines, financial advisors, and rental market standards |

Explore related products

What You'll Learn

- Rent-to-Income Ratio: Understanding the standard ratio to estimate income based on rent

- Budgeting Essentials: Allocating income for rent, utilities, and other monthly expenses

- Income Calculation Formula: Using rent as a percentage of total earnings

- Affordable Housing Guidelines: Determining income thresholds for rent affordability

- Financial Planning Tips: Strategies to balance rent with savings and other costs

![]()

Rent-to-Income Ratio: Understanding the standard ratio to estimate income based on rent

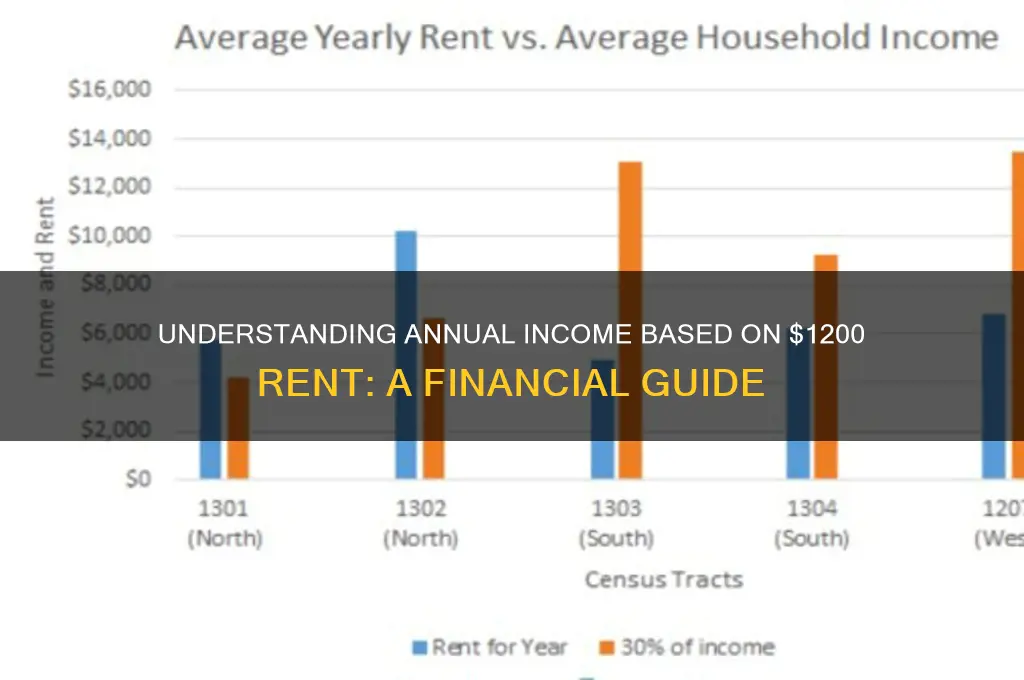

The rent-to-income ratio is a critical metric used by landlords, financial advisors, and renters themselves to gauge affordability and financial stability. Typically, housing expenses should not exceed 30% of gross monthly income, a standard set by financial experts and government agencies. If your rent is $1,200 per month, this rule of thumb suggests your monthly income should be at least $4,000 to maintain a balanced budget. Annually, this translates to a minimum income of $48,000. This ratio ensures that after paying rent, you have sufficient funds for other essentials like utilities, groceries, and savings.

To calculate your rent-to-income ratio, divide your monthly rent by your gross monthly income. For instance, if your rent is $1,200 and your income is $4,000, the ratio is 30% ($1,200 / $4,000 = 0.30). While 30% is the standard benchmark, individual circumstances may allow for flexibility. For example, someone with minimal debt or significant savings might comfortably allocate up to 40% of their income to rent. Conversely, those with high expenses or financial obligations should aim for a lower ratio, closer to 25%. Understanding this ratio helps you assess whether your current rent aligns with your income or if adjustments are needed.

A persuasive argument for adhering to the 30% rule is its role in long-term financial health. Overspending on rent can lead to a cycle of debt, as it leaves little room for emergencies, retirement savings, or leisure. For someone paying $1,200 in rent, an income below $4,000 per month could strain their finances, particularly if unexpected expenses arise. Landlords often use this ratio to evaluate rental applications, as it indicates a tenant’s ability to pay consistently. By staying within this guideline, you not only improve your chances of approval but also foster financial resilience.

Comparatively, the rent-to-income ratio varies by location and lifestyle. In high-cost cities like New York or San Francisco, renters often exceed the 30% threshold due to inflated housing prices. For example, a $1,200 rent in a rural area might be affordable on a $36,000 annual income, but in an urban center, it may require closer to $60,000 to cover additional living expenses. This disparity highlights the importance of contextualizing the ratio based on local cost of living. Tools like rent calculators and budgeting apps can help tailor this metric to your specific situation, ensuring a more accurate assessment of affordability.

In conclusion, the rent-to-income ratio is a versatile tool for estimating income based on rent, particularly when your rent is $1,200. By aiming for the 30% benchmark, you can maintain financial stability and plan for the future. However, it’s essential to consider personal factors like debt, savings, and location when applying this rule. Whether you’re a renter or landlord, understanding this ratio empowers you to make informed decisions and avoid financial pitfalls. Start by calculating your current ratio and adjust your budget or housing choices accordingly to achieve a healthier financial balance.

Landlord's Dilemma: Renting to a Convicted Drug Offender

You may want to see also

Explore related products

![]()

Budgeting Essentials: Allocating income for rent, utilities, and other monthly expenses

Rent typically consumes a significant portion of monthly income, with financial advisors recommending it stay below 30% of gross earnings. If your rent is $1,200, this suggests an annual income of at least $48,000 to meet this guideline. However, this is a baseline; actual income needs vary based on location, lifestyle, and financial goals. For instance, in high-cost cities like San Francisco or New York, $1,200 might only cover a shared room, implying a higher necessary income. Conversely, in rural areas, this rent could secure a spacious apartment, allowing for a lower income threshold. Understanding this relationship is the first step in crafting a realistic budget.

Allocating income effectively requires prioritizing expenses beyond rent. Utilities—electricity, water, internet, and gas—typically account for 5–10% of monthly income. For someone paying $1,200 in rent, this translates to $200–$400 monthly. To manage these costs, consider energy-efficient appliances, LED bulbs, and programmable thermostats. Additionally, bundle services where possible; for example, combining internet and cable can save $20–$50 monthly. Small adjustments in utility usage can free up funds for other essentials or savings.

After rent and utilities, discretionary spending often becomes the budget’s wildcard. Groceries, transportation, and entertainment should collectively not exceed 35–40% of income. For a $1,200 rent scenario, this means $1,400–$1,600 monthly for these categories. To stay within bounds, adopt strategies like meal planning, using public transit, and leveraging free or low-cost entertainment options. For instance, cooking at home instead of dining out can save $200–$300 monthly. Tracking expenses with apps like Mint or YNAB ensures you stay aligned with your budget goals.

Finally, savings and debt repayment must not be overlooked. Aim to allocate 10–15% of your income to savings and emergency funds. For someone with $1,200 rent, this equates to $400–$600 monthly. If you have debt, prioritize high-interest obligations like credit cards while maintaining minimum payments on others. For example, paying an extra $100 monthly toward a 19% APR credit card can save hundreds in interest over time. Balancing these priorities ensures financial stability and progress toward long-term goals.

In summary, if your rent is $1,200, your budgeting strategy should reflect a holistic view of income allocation. By capping rent at 30%, managing utilities efficiently, controlling discretionary spending, and prioritizing savings and debt, you can maintain financial health. Adjustments based on location and lifestyle are key, ensuring your budget remains realistic and sustainable. This approach transforms budgeting from a chore into a tool for achieving financial freedom.

Renting a Park for Your Party: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Income Calculation Formula: Using rent as a percentage of total earnings

A common rule of thumb in personal finance is that rent should not exceed 30% of your gross monthly income. This guideline, often referred to as the 30% rule, provides a quick way to estimate affordability. If your rent is $1,200 per month, applying this rule suggests your monthly income should be at least $4,000. Annually, this translates to $48,000. However, this is a simplified approach and doesn’t account for individual financial situations, such as debt, savings goals, or other expenses. It’s a starting point, not a one-size-fits-all solution.

To refine this calculation, consider using a more detailed formula: Rent as a Percentage of Total Earnings (RAPTE). This formula adjusts the 30% rule based on your financial obligations. First, calculate your total monthly expenses, including rent, utilities, groceries, transportation, and debt payments. Subtract this total from your gross monthly income to find your discretionary income. If your rent is $1,200 and your total expenses are $2,500, your discretionary income is $1,500 (assuming a $4,000 monthly income). Now, divide your rent by your gross income to find the percentage. In this case, $1,200 / $4,000 = 30%, aligning with the rule. However, if your expenses are higher, this percentage may exceed 30%, indicating a need to adjust your budget or income.

For a more dynamic approach, factor in your savings and financial goals. Financial experts often recommend allocating 20% of your income to savings and debt repayment. If your rent is $1,200 and you aim to save $800 monthly, your total income should cover these priorities. Using the RAPTE formula, adjust the percentage to reflect your unique needs. For instance, if rent and savings together should not exceed 50% of your income, your monthly earnings should be at least $4,000 ($1,200 rent + $800 savings = $2,000, which is 50% of $4,000). This tailored approach ensures your income supports both your lifestyle and financial goals.

A cautionary note: relying solely on rent as a percentage of income can overlook regional cost-of-living differences. In high-cost cities like New York or San Francisco, rent may consume 40–50% of income, making the 30% rule impractical. In such cases, prioritize essential expenses and adjust your budget accordingly. For example, if your rent is $1,200 in a high-cost area, your income may need to be closer to $60,000 annually to maintain financial stability. Pair the RAPTE formula with local cost benchmarks for a more accurate assessment.

In conclusion, using rent as a percentage of total earnings provides a flexible framework for income calculation. Start with the 30% rule as a baseline, then customize the formula to reflect your expenses, savings goals, and regional costs. If your rent is $1,200, this method helps determine whether your income aligns with your financial priorities. Remember, the goal isn’t just to afford rent but to build a sustainable budget that supports your long-term financial health.

Easy Guide: Submitting Rent Payments to the Municipal Clerk

You may want to see also

Explore related products

![]()

Affordable Housing Guidelines: Determining income thresholds for rent affordability

A common rule of thumb in budgeting is that rent should not exceed 30% of your monthly income. If your rent is $1,200, this guideline suggests your monthly income should be at least $4,000, or $48,000 annually. However, this is a simplified approach and doesn’t account for regional cost-of-living variations, household size, or other financial obligations. Affordable housing guidelines aim to refine this calculation by setting income thresholds that ensure housing remains within reach for diverse populations. These thresholds are critical for policymakers, landlords, and tenants to determine what constitutes "affordable" rent based on income.

To establish income thresholds, affordable housing programs often use Area Median Income (AMI) as a benchmark. AMI represents the midpoint of a region’s income distribution, and affordability is typically defined as spending no more than 30% of income on housing. For instance, if the AMI in a city is $70,000, a household earning 80% of AMI ($56,000) would be considered eligible for affordable housing programs. In this context, a $1,200 rent would be affordable for someone earning at least $48,000 annually, assuming they fall within the 80% AMI bracket. However, in high-cost areas, even this threshold may not reflect true affordability, necessitating adjustments based on local economic conditions.

Another factor in determining income thresholds is household size. Larger households often require more income to cover basic needs, including housing. Affordable housing guidelines frequently adjust income limits based on family size, ensuring that thresholds are equitable. For example, a single-person household earning $48,000 might find $1,200 rent affordable, but a family of four with the same income would likely struggle. Programs like the Low-Income Housing Tax Credit (LIHTC) account for this by setting tiered income limits, such as 60% of AMI for a family of four versus 50% for a single individual.

Practical implementation of these guidelines requires collaboration between government agencies, developers, and tenants. Landlords can use income thresholds to screen applicants for affordable units, ensuring rents align with tenants’ financial capacity. Tenants, meanwhile, can use these thresholds to assess whether a $1,200 rent fits within their budget. For instance, if a tenant earns $50,000 annually in a region where 80% of AMI is $60,000, they would meet affordability criteria. However, they should also consider other expenses, such as utilities, groceries, and transportation, to ensure housing costs don’t compromise overall financial stability.

In conclusion, determining income thresholds for rent affordability involves more than a one-size-fits-all calculation. By incorporating factors like AMI, household size, and regional economic conditions, affordable housing guidelines provide a nuanced framework for assessing affordability. For someone paying $1,200 in rent, understanding these thresholds can clarify whether their income aligns with sustainable housing costs. Policymakers and individuals alike must leverage these guidelines to promote equitable access to housing, ensuring that affordability remains a cornerstone of housing policy.

Crafting a Comprehensive Rent Agreement for EBT Tenants: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Financial Planning Tips: Strategies to balance rent with savings and other costs

Rent consumes a significant portion of income, often leaving individuals scrambling to balance savings and other expenses. If your rent is $1200 monthly, you’re paying $14,400 annually, which could represent 30-40% of your income if you follow the 30% rule. This rule suggests that rent should not exceed 30% of gross income, implying an annual income of at least $48,000 for a $1200 rent. However, this benchmark varies based on location, lifestyle, and financial goals. To avoid being "house poor," where housing costs dominate your budget, strategic financial planning is essential.

Step 1: Prioritize the 50/30/20 Rule

Allocate 50% of your income to necessities (rent, utilities, groceries), 30% to discretionary spending (entertainment, dining out), and 20% to savings and debt repayment. For a $1200 rent, this means your monthly necessities should not exceed $2400, assuming a $48,000 annual income. If your income is lower, adjust by reducing discretionary spending or finding a cheaper rental. Use budgeting apps like Mint or YNAB to track expenses and ensure alignment with this framework.

Caution: Avoid Lifestyle Inflation

As income grows, resist the urge to increase discretionary spending proportionally. For instance, if you earn $60,000 annually, your rent remains $1200 (24% of income), but discretionary spending should not exceed $1500 monthly. Instead, redirect excess funds to savings, investments, or high-interest debt repayment. This prevents financial strain and accelerates wealth accumulation.

Example: Balancing Rent and Emergency Savings

If your rent is $1200 and you earn $50,000 annually, aim to save at least 3-6 months’ worth of living expenses ($9000-$18,000). Automate savings by setting up monthly transfers of $750-$1500 to a high-yield savings account. Simultaneously, reduce non-essential expenses like subscription services or dining out to free up funds. This dual approach ensures financial stability without sacrificing long-term savings goals.

Balancing rent with savings and other costs requires adaptability. Regularly review your budget to identify areas for optimization. Consider roommates, relocating to a lower-cost area, or negotiating rent reductions if feasible. By staying proactive and disciplined, you can maintain financial equilibrium even with a $1200 rent, ensuring both immediate needs and future goals are met.

Bay Area Rental Trends: How Many Residents Choose to Rent?

You may want to see also

Frequently asked questions

The annual income cannot be determined solely based on rent. It depends on factors like expenses, savings, and financial goals.

A common rule is that rent should not exceed 30% of your gross income. For $1200 rent, your annual income should ideally be at least $48,000.

No, $1200 rent would be 48% of a $30,000 annual income, exceeding the recommended 30% threshold.

Yes, $1200 rent would be 24% of a $60,000 annual income, which is within the affordable range.