Charging rent to your child can be a sensitive but practical decision, often aimed at teaching financial responsibility or preparing them for independence. The average rent to charge varies widely based on factors like location, household income, and the child’s age or employment status. In many cases, parents charge a nominal fee, such as 10% to 20% of the child’s income or a reduced rate compared to local market prices, ensuring it remains affordable while fostering accountability. Some families opt for a flat rate, like $200 to $500 monthly, depending on the cost of living in their area. Ultimately, the goal is to strike a balance between supporting your child and encouraging self-sufficiency.

Explore related products

What You'll Learn

![]()

Factors Influencing Rent: Age, Income, Location

Charging rent to your child is a decision influenced by a complex interplay of factors, with age, income, and location standing out as the most critical. Each of these elements shapes not only the amount you might consider fair but also the broader implications of this arrangement on your child’s financial independence and your familial relationship. Understanding how these factors interact can help you set a rent that is both supportive and realistic.

Age plays a pivotal role in determining the appropriate rent for your child. For younger adults, aged 18 to 25, who are likely still in education or starting their careers, a nominal rent—perhaps 10-20% of their monthly income—can instill financial responsibility without overwhelming them. For instance, if your child earns $2,000 monthly, charging $200-$400 strikes a balance between contribution and affordability. Older children, aged 26 and above, with more established careers, may be expected to pay closer to market rates, especially if they are saving for their own homes. However, always consider their overall financial obligations, such as student loans or car payments, to avoid burdening them excessively.

Income is another critical factor, as it directly dictates how much your child can reasonably afford. A general rule of thumb is that rent should not exceed 30% of their monthly income. For example, if your child earns $3,000 per month, a rent of $900 would align with this guideline. However, this percentage can be adjusted based on their financial goals. If they are aggressively saving for a down payment on a house, a lower rent might be more appropriate. Conversely, if they have a high disposable income, you might consider charging closer to market rates to encourage financial discipline.

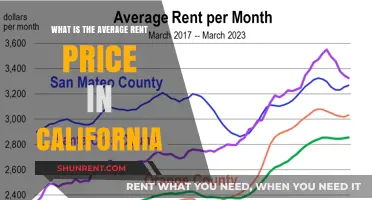

Location significantly impacts the rent you charge, as it reflects the cost of living in your area. In high-cost cities like New York or San Francisco, even a reduced rent might still be substantial due to the overall housing market. For instance, charging $800 in a rural area is vastly different from charging the same amount in a metropolitan area. To ensure fairness, research local rental averages and consider offering a discount based on your child’s income or age. For example, if the average one-bedroom apartment in your area rents for $1,500, you might charge your child $700-$1,000, depending on their financial situation.

Balancing these factors requires a nuanced approach. Start by assessing your child’s income and age to establish a baseline. Then, factor in your location to ensure the rent is both affordable and reflective of local costs. For instance, a 22-year-old earning $2,500 in a mid-sized city might pay $500-$600, while a 30-year-old earning $5,000 in the same area could contribute $1,200-$1,500. Regularly revisit this arrangement as their financial situation evolves, ensuring it remains fair and supportive. By thoughtfully considering age, income, and location, you can set a rent that fosters financial responsibility while maintaining a positive parent-child relationship.

Rent Info: State or Federal Taxes?

You may want to see also

Explore related products

![]()

Setting Fair Rent: Covering Costs vs. Teaching Responsibility

Charging rent to your child can be a delicate balance between financial practicality and fostering independence. While some parents aim to cover household expenses, others see it as a tool for teaching financial responsibility. The average rent charged to adult children living at home varies widely, typically ranging from $300 to $800 monthly, depending on location, family income, and living standards. However, setting a fair amount requires more than just mimicking market rates—it demands a thoughtful approach that aligns with your family’s goals.

Step 1: Calculate Actual Costs

Begin by determining the tangible expenses your child’s presence adds to the household. This includes a portion of utilities, groceries, and maintenance. For instance, if monthly utilities are $200 and your child uses 20% of the resources, allocate $40 to their share. Avoid inflating costs to punish or save for unrelated expenses; transparency builds trust. Use a spreadsheet to break down expenses, ensuring fairness and clarity.

Step 2: Consider Their Financial Reality

A fair rent should not cripple your child’s ability to save or invest in their future. If they earn minimum wage ($15/hour), charging $600 monthly (40 hours/week) leaves little for emergencies or goals. Instead, cap rent at 20–30% of their income—a widely accepted affordability benchmark. For a child earning $2,000 monthly, this translates to $400–$600. Adjust for part-time work or students by offering reduced rates or payment plans.

Step 3: Weigh Financial vs. Educational Goals

If covering costs is your priority, tie rent directly to expenses. However, if teaching responsibility is key, structure payments to mimic real-world renting. Include a “savings” component, where part of their rent goes into a shared account for emergencies or future goals. For example, $500 monthly could be $300 for household costs and $200 into a savings fund they can access later. This dual approach ensures they learn budgeting while contributing fairly.

Caution: Avoid Hidden Agendas

Resist using rent as leverage for control or punishment. Charging exorbitant rates to force them out or waiving payments to avoid conflict undermines the lesson. Similarly, don’t tie rent to chores or grades unless explicitly agreed upon as part of a larger responsibility plan. Consistency and clarity prevent resentment and foster mutual respect.

There’s no one-size-fits-all formula for setting rent. For younger adults (18–22), start with nominal contributions ($100–$200) to ease them into financial habits. For older children (23–30), align rent with their income and your costs. Regularly review the arrangement as their earnings or household needs change. By balancing fairness with educational intent, you create a win-win scenario: they gain life skills, and you maintain a harmonious home.

Discover the Real Renting Price of Your Home: A Guide

You may want to see also

Explore related products

![]()

Legal Considerations: Tenant Rights and Family Agreements

Charging rent to a family member transforms a familial relationship into a landlord-tenant dynamic, triggering legal obligations that vary by jurisdiction. In most regions, tenant rights apply regardless of the relationship between landlord and tenant, meaning your child gains protections like privacy, habitability standards, and eviction procedures. For instance, in California, landlords must provide 30 to 60 days’ notice before terminating a month-to-month tenancy, even for family members. Ignoring these laws can lead to legal disputes, fines, or even lawsuits, making it essential to understand local tenant laws before setting rent.

To navigate this legally, draft a formal family rental agreement that mirrors standard lease contracts. Include specifics such as rent amount, due dates, late fees (if applicable), and the length of the tenancy. For example, a six-month fixed-term lease provides stability for both parties, while a month-to-month agreement offers flexibility. Explicitly outline responsibilities for repairs, utilities, and property maintenance to avoid ambiguity. Even if the agreement feels overly formal for family, it serves as a legal safeguard and clarifies expectations, reducing the risk of misunderstandings.

One critical yet often overlooked aspect is the distinction between rent and financial contributions. In some jurisdictions, courts may interpret regular payments from a child as a gift rather than rent if there’s no formal agreement. This could complicate matters in case of disputes over property rights or financial obligations. For instance, in New York, a verbal agreement to charge $500 monthly might not hold up if challenged, whereas a written contract signed by both parties provides clear evidence of intent. Always consult local laws or a legal professional to ensure your arrangement is legally binding.

Finally, consider the emotional and practical implications of enforcing tenant rights within a family. While legally you may have the right to evict a non-paying tenant, doing so with a family member carries significant emotional weight. Balance legal compliance with familial compassion by setting realistic expectations and maintaining open communication. For example, if your child faces temporary financial hardship, a written amendment to the agreement could temporarily reduce rent or allow deferred payments, preserving both legal integrity and family harmony.

Budget Truck Rental Insurance Costs: What You Need to Know

You may want to see also

Explore related products

![]()

Financial Benefits: Saving for Future or Building Credit

Charging your child rent can serve as a powerful financial tool, but its value extends beyond the immediate income. It becomes a strategic decision when framed as either a savings mechanism for their future or a credit-building opportunity. Each approach has distinct advantages, tailored to different long-term goals.

Savings for the Future:

If your child’s financial independence is the priority, directing their rent payments into a dedicated savings account or investment vehicle can yield significant returns. For instance, depositing $200 monthly into a high-yield savings account with a 4% annual interest rate could accumulate over $12,000 in five years, excluding compound interest. Alternatively, investing in a 529 plan for education or a Roth IRA for retirement leverages tax advantages and long-term growth. This method not only preserves capital but also teaches your child the value of delayed gratification and financial planning.

Building Credit:

Alternatively, rent payments can be reported to credit bureaus to establish or improve your child’s credit score, a critical asset for future loans, housing, and employment. Services like RentReporters or rental credit reporting agencies can add these payments to their credit history for a small fee. For young adults aged 18–25, this is particularly impactful, as it accelerates their credit-building timeline. A consistent rental payment history can raise their score by 50–100 points within 6–12 months, provided other financial behaviors remain positive.

Practical Implementation:

To maximize benefits, consider a hybrid approach. Allocate 70% of the rent to a savings or investment account and use the remaining 30% to cover reporting fees for credit-building. For example, if rent is $500 monthly, $350 goes into a savings account, and $150 funds credit reporting and any associated costs. This balance ensures both financial security and credit readiness.

Cautions and Considerations:

While these strategies are beneficial, they require transparency and agreement. Discuss the purpose of the rent with your child to ensure they understand its role in their financial future. Avoid overburdening them with high rent, especially if they are still establishing their career or education. Additionally, monitor credit reports annually to correct any errors and ensure the strategy is effective.

Charging rent isn’t just about recouping costs—it’s an opportunity to empower your child financially. Whether saving for their future or building their credit, the approach you choose should align with their needs and your shared goals. With careful planning, this seemingly routine transaction can become a cornerstone of their financial success.

Renting a Billboard for a Day: A Quick Guide

You may want to see also

Explore related products

![Child's Play (1988) - Collector's Edition 4K Ultra HD + Blu-ray [4K UHD]](https://m.media-amazon.com/images/I/71DqkIxjJIL._AC_UL320_.jpg)

![Rent-an-Elf [ NON-USA FORMAT, PAL, Reg.0 Import - Denmark ]](https://m.media-amazon.com/images/I/51MODMZHO1L._AC_UL320_.jpg)

![]()

Emotional Impact: Balancing Independence and Family Dynamics

Charging rent to adult children living at home is a delicate dance, one that can either foster financial responsibility or fracture familial bonds. The emotional impact of this decision ripples far beyond the monthly payment, influencing the dynamics of independence, trust, and love within the family unit.

While a nominal rent can teach valuable lessons in budgeting and self-sufficiency, an excessive amount can breed resentment and feelings of exploitation. Striking the right balance requires a nuanced understanding of both financial realities and the unique emotional landscape of your family.

Consider the stage of your child's life. A recent college graduate struggling to find their footing in a competitive job market may require a lower rent, or even a temporary rent-free period, to alleviate financial stress and allow them to focus on career building. Conversely, a young professional with a stable income might be ready for a more substantial contribution, signaling their growing independence and commitment to shared household expenses.

Flexibility is key. Open communication is paramount. Discuss expectations openly, acknowledging the emotional complexities involved. Frame the rent as a contribution to the household, emphasizing shared responsibility rather than a transactional exchange.

The emotional impact of charging rent extends beyond the financial. It can be a catalyst for important conversations about boundaries, expectations, and the evolving nature of the parent-child relationship. By approaching this decision with empathy, understanding, and a willingness to adapt, parents can navigate this delicate terrain, fostering both financial responsibility and a stronger, more mature bond with their adult children.

Renting Without History: Tips to Secure Your First Lease

You may want to see also

Frequently asked questions

There is no one-size-fits-all average rent to charge your child, as it depends on factors like your location, household income, and the child's financial situation. Many parents charge a percentage of their child's income, typically 10-30%, or a nominal amount to teach financial responsibility.

If your child is a full-time student with limited income, consider charging a reduced or symbolic rent to help them learn budgeting without causing financial strain. Alternatively, you could ask them to contribute through chores or other responsibilities.

For adult children with steady jobs, charging 10-30% of their income or a fair market rate (adjusted for your local area) is common. Ensure the amount is reasonable and aligns with your goals, whether it’s helping them save for independence or covering household expenses.

Yes, charging rent can still be appropriate, but consider adjusting the amount to support their savings goals. You could charge a lower rate or allow them to pay a portion of utilities and groceries instead of full rent. Communication is key to finding a balance that works for both parties.

![Child's Play (1988) (FP/RPKG/BD) [Blu-ray]](https://m.media-amazon.com/images/I/91D9zlUz3nL._AC_UL320_.jpg)

![Child's Play [DVD]](https://m.media-amazon.com/images/I/81WrVee1DIL._AC_UL320_.jpg)

![DSS Games Our Family is So Weird [A Family Card Game to Decide Who’s Most Likely to | Game Night Idea for Kids, Adults & Groups | Great for Halloween, Stocking Stuffers, Friendsgiving, Thanksgiving]](https://m.media-amazon.com/images/I/61LDUlN7NVL._AC_UY218_.jpg)