The average rent-to-income ratio is a critical financial metric used to assess housing affordability, representing the proportion of a household’s income spent on rent. Typically expressed as a percentage, it is calculated by dividing monthly rent by monthly income and multiplying by 100. A widely accepted benchmark suggests that households should allocate no more than 30% of their income to rent to maintain financial stability. However, this ratio varies significantly by location, income level, and local housing markets, with urban areas often exceeding this threshold due to higher living costs. Understanding this ratio is essential for both renters and policymakers, as it highlights affordability challenges and informs decisions on housing policies, wage standards, and urban planning.

| Characteristics | Values |

|---|---|

| Definition | Rent-to-Income Ratio = Monthly Rent / Monthly Gross Income |

| Average U.S. Ratio (2023) | ~28-30% (varies by source, e.g., Harvard JCHS, Zillow) |

| Affordable Housing Threshold | ≤30% (HUD standard for cost-burdened households) |

| Severely Cost-Burdened Threshold | >50% (HUD definition) |

| Median U.S. Rent (2023) | ~$1,900/month (Zillow, Realtor.com estimates) |

| Median U.S. Household Income (2023) | $75,000/year ($6,250/month) (U.S. Census Bureau) |

| Top Cities with Highest Ratios | Miami (45%), Los Angeles (43%), New York (42%) (Zillow 2023) |

| Lowest Ratio Cities | Pittsburgh (24%), Cleveland (25%), Detroit (26%) (Zillow 2023) |

| Global Comparison | U.S. (28-30%), UK (35%), Germany (25%), Japan (20%) (OECD 2022) |

| Impact on Households | Ratios >30% linked to reduced spending on healthcare, food, savings |

| Policy Interventions | Rent control, housing vouchers, inclusionary zoning, tax incentives |

| Trends (2010-2023) | Steady rise in ratios due to outpacing rent growth vs. income growth |

| Demographic Disparities | Lower-income households (bottom 20%) face ratios of 50-70% |

| Sources | HUD, Harvard Joint Center for Housing Studies, Zillow, U.S. Census |

Explore related products

What You'll Learn

- National vs. Local Ratios: Comparing national averages to local rent-to-income ratios in specific cities or regions

- Affordable Housing Thresholds: Defining what constitutes an affordable rent-to-income ratio for households

- Income Fluctuations Impact: How changes in income levels affect the rent-to-income ratio over time

- Regional Cost Variations: Analyzing how rent-to-income ratios differ across urban, suburban, and rural areas

- Policy Influences: Examining how government policies and subsidies impact the rent-to-income ratio

![]()

National vs. Local Ratios: Comparing national averages to local rent-to-income ratios in specific cities or regions

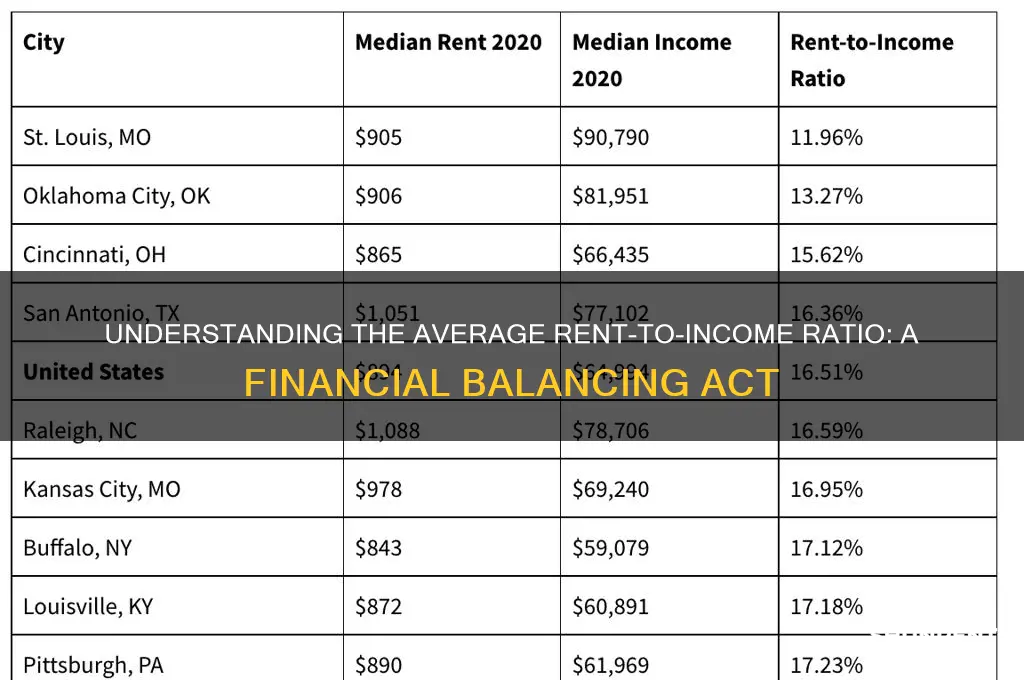

The national average rent-to-income ratio hovers around 25-30%, meaning households typically spend a quarter to a third of their income on rent. This benchmark, however, masks stark disparities when compared to local ratios in specific cities or regions. For instance, in San Francisco, renters often face a ratio exceeding 45%, while in smaller Midwest cities like Indianapolis, it can dip below 20%. These variations highlight the importance of context when interpreting affordability.

Analyzing these discrepancies reveals underlying economic forces. High-demand urban centers like New York or Los Angeles drive up rents faster than incomes can rise, skewing local ratios upward. Conversely, regions with lower living costs or robust job markets, such as Austin or Raleigh, often maintain ratios closer to or below the national average. Policymakers and renters alike must consider these local dynamics to make informed decisions about housing affordability.

To navigate these differences, renters should assess their own situations relative to both national and local benchmarks. For example, if the national average is 30% but your city’s ratio is 40%, budgeting strategies like reducing discretionary spending or seeking roommates become essential. Conversely, in areas with lower ratios, allocating more income to savings or investments might be feasible. Tools like rent-to-income calculators can provide personalized insights based on location-specific data.

A persuasive argument emerges when advocating for localized housing policies. National averages fail to address the unique challenges of cities like Miami, where tourism inflates rents, or Seattle, where tech industry growth outpaces housing supply. Tailored solutions, such as rent control in high-ratio cities or incentives for affordable housing development in low-ratio areas, could bridge the gap between national standards and local realities.

In conclusion, while the national rent-to-income ratio offers a broad reference point, its true utility lies in comparison to local data. Understanding these disparities empowers individuals and policymakers to address affordability challenges more effectively, ensuring that housing remains accessible across diverse geographic and economic landscapes.

Renting a Food Truck for Catering: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Affordable Housing Thresholds: Defining what constitutes an affordable rent-to-income ratio for households

The concept of affordable housing hinges on the rent-to-income ratio, a metric that compares a household’s monthly rent to its gross monthly income. Widely accepted guidelines suggest that housing is affordable if it consumes no more than 30% of a household’s income. For example, a family earning $4,000 monthly should ideally spend no more than $1,200 on rent. This threshold, established by the U.S. Department of Housing and Urban Development (HUD), serves as a benchmark for policymakers, renters, and advocates alike. However, this standard often fails to account for regional variations in living costs, household size, and income disparities, raising questions about its universality.

To refine the affordability threshold, consider the 40% rule for low-income households or those in high-cost urban areas. For instance, a single parent earning $2,500 monthly might allocate up to $1,000 for rent under this adjusted ratio, leaving more room for essentials like childcare and transportation. This approach acknowledges the financial strain on vulnerable populations but requires careful implementation to avoid perpetuating housing insecurity. Pairing this threshold with subsidies or rent control measures can mitigate risks and ensure broader accessibility.

A comparative analysis reveals that international standards vary significantly. In Germany, for example, housing is deemed affordable if rent consumes 25% of income, reflecting robust tenant protections and a culture of long-term rentals. Conversely, in cities like Hong Kong or New York, ratios often exceed 40%, driven by skyrocketing rents and stagnant wages. These disparities underscore the need for context-specific thresholds rather than a one-size-fits-all approach. Policymakers must consider local economic conditions, cultural norms, and demographic profiles when defining affordability.

Practical tips for households navigating rent-to-income ratios include tracking expenses to identify areas for cost-cutting, negotiating rent with landlords, and exploring government assistance programs. For instance, the Low-Income Housing Tax Credit (LIHTC) program in the U.S. offers reduced rents for eligible households. Additionally, households can consider shared housing or relocating to more affordable neighborhoods. By proactively managing their ratio, individuals can achieve housing stability without compromising other financial priorities.

Ultimately, defining an affordable rent-to-income ratio requires balancing standardized benchmarks with localized realities. While the 30% rule remains a useful starting point, it must be supplemented with flexible thresholds, targeted interventions, and a nuanced understanding of household needs. Only then can the goal of affordable housing be realized for all, regardless of income or geography.

Renting a Cabana at Aulani: A Step-by-Step Guide to Luxury Relaxation

You may want to see also

Explore related products

![]()

Income Fluctuations Impact: How changes in income levels affect the rent-to-income ratio over time

Income fluctuations can dramatically alter the rent-to-income ratio, a metric that typically hovers around 30% for financially stable households. When incomes rise, this ratio naturally decreases, easing the burden of rent. Conversely, a drop in earnings can push the ratio above 50%, a threshold often associated with housing stress. For instance, a tenant earning $4,000 monthly with a $1,200 rent payment (30% ratio) would see their ratio spike to 42.8% if their income fell to $2,800. This shift isn’t just a number—it’s a potential gateway to financial instability, missed payments, and even eviction.

Consider the cyclical nature of income volatility, particularly in gig-based or commission-driven careers. A freelance graphic designer earning $6,000 one month and $2,500 the next faces a rent-to-income ratio swinging from 20% to 48%. Such unpredictability demands proactive financial planning. Experts recommend setting aside 20–30% of peak earnings into an emergency fund to buffer low-income periods. Additionally, negotiating rent terms—like seasonal adjustments or deferred payments—with landlords can mitigate the impact of income dips.

The long-term effects of income fluctuations on the rent-to-income ratio are equally concerning. Prolonged periods of high ratios can erode savings, delay wealth-building, and limit opportunities for homeownership. For example, a household consistently spending 45% of income on rent has 50% less disposable income for investments, retirement, or education compared to one maintaining a 30% ratio. Over a decade, this disparity could translate to hundreds of thousands of dollars in lost wealth accumulation.

To counteract these effects, households should adopt dynamic budgeting strategies. Tools like zero-based budgeting, where every dollar is assigned a purpose, can help prioritize rent during lean months. Renters might also consider relocating to areas with lower housing costs or exploring shared living arrangements to stabilize their ratio. Policymakers play a role too—rent control measures, income-based subsidies, and tenant protections can provide a safety net during income downturns. Ultimately, understanding and managing the rent-to-income ratio in the face of income fluctuations is not just about survival; it’s about securing financial resilience for the future.

Is It Legal for Rent Advisors to Ignore Tenants?

You may want to see also

Explore related products

![]()

Regional Cost Variations: Analyzing how rent-to-income ratios differ across urban, suburban, and rural areas

The rent-to-income ratio, a critical metric for financial planning, varies dramatically across urban, suburban, and rural areas, reflecting disparities in cost of living and earning potential. In urban centers like New York City or San Francisco, renters often allocate 40-50% of their income to housing, far exceeding the recommended 30% threshold. This imbalance forces residents to compromise on savings, investments, or quality of life. Suburban areas typically offer a middle ground, with ratios hovering around 25-35%, as housing costs moderate while incomes remain relatively stable. In contrast, rural regions boast the most favorable ratios, often below 20%, due to lower housing expenses and a slower pace of economic activity.

To illustrate, consider a household earning $60,000 annually. In an urban setting, they might pay $2,500 monthly in rent, consuming 50% of their income. The same household in a suburban area could pay $1,500, reducing the ratio to 30%. In a rural area, rent might drop to $800, lowering the ratio to 16%. These examples highlight how geography dictates financial strain, with urban dwellers facing the steepest challenges.

Analyzing these variations reveals systemic issues. Urban areas, despite higher incomes, often fail to keep pace with skyrocketing rents, driven by demand and limited space. Suburban regions benefit from a balance between affordability and accessibility to urban job markets, making them attractive for middle-income families. Rural areas, while affordable, may offer fewer job opportunities, limiting income growth. Policymakers must address these imbalances through zoning reforms, affordable housing initiatives, and rural economic development to ensure equitable living standards across regions.

For individuals navigating these disparities, practical strategies are essential. Urban renters should consider roommates, smaller units, or rent-controlled housing to mitigate costs. Suburban residents can leverage lower ratios to build savings or invest in property. Rural dwellers, while enjoying affordability, should focus on skill development to counterbalance limited income opportunities. Understanding regional rent-to-income ratios empowers informed decisions, ensuring financial stability regardless of location.

In conclusion, regional cost variations in rent-to-income ratios underscore the complexity of housing affordability. Urban, suburban, and rural areas each present unique challenges and opportunities, shaped by economic dynamics and lifestyle trade-offs. By dissecting these differences, individuals and policymakers can work toward solutions that foster affordability and sustainability across all regions.

When to Rent a U-Haul: Timing Your Move Perfectly

You may want to see also

Explore related products

![]()

Policy Influences: Examining how government policies and subsidies impact the rent-to-income ratio

Government policies and subsidies play a pivotal role in shaping the rent-to-income ratio, a critical metric for housing affordability. By directly influencing the supply and cost of housing, as well as household incomes, these interventions can either alleviate or exacerbate the burden of rent on tenants. For instance, rent control policies cap the amount landlords can charge, theoretically keeping housing costs manageable for low- and middle-income families. However, critics argue that such measures can reduce the incentive for new construction, leading to housing shortages over time. Conversely, subsidies like housing vouchers or tax credits for developers can increase the availability of affordable units without distorting market dynamics as severely. Understanding these mechanisms is essential for policymakers aiming to strike a balance between affordability and sustainability.

Consider the case of inclusionary zoning policies, which require developers to allocate a percentage of new units as affordable housing. While this approach increases the stock of low-cost housing, it can also raise construction costs, potentially offsetting some of the intended benefits. Similarly, direct cash subsidies to renters, such as those provided through the U.S. Housing Choice Voucher Program, can significantly reduce the rent-to-income ratio for recipients. However, these programs often face funding limitations and long waitlists, leaving many eligible households without assistance. A comparative analysis reveals that policies combining supply-side incentives (e.g., tax breaks for affordable housing developers) with demand-side support (e.g., renter subsidies) tend to yield more comprehensive results, though their success depends on careful calibration and sufficient funding.

From a persuasive standpoint, governments must prioritize policies that address both the immediate and long-term drivers of housing unaffordability. For example, investing in public housing projects can provide stable, low-cost options for vulnerable populations, while also stimulating local economies through construction jobs. Additionally, linking subsidies to income thresholds ensures that support reaches those who need it most. However, policymakers must remain vigilant about unintended consequences, such as gentrification, which can displace low-income residents despite the creation of new affordable units. A holistic approach, informed by data and community input, is crucial for maximizing the impact of these interventions.

To illustrate, let’s examine the effects of Germany’s *Mietpreisbremse* (rent brake) policy, which limits rent increases in tight housing markets. While it has provided short-term relief for tenants, studies suggest it may have discouraged investment in rental properties, potentially worsening the housing shortage in the long run. In contrast, Singapore’s public housing program, which provides subsidized homes to over 80% of residents, has achieved remarkable affordability by maintaining a strong focus on supply and long-term planning. These examples underscore the importance of tailoring policies to local contexts and continuously evaluating their outcomes.

In conclusion, government policies and subsidies are powerful tools for managing the rent-to-income ratio, but their effectiveness hinges on thoughtful design and implementation. By combining targeted interventions with a commitment to equitable outcomes, policymakers can create housing systems that are both affordable and sustainable. Practical tips for policymakers include conducting regular housing needs assessments, engaging stakeholders in policy development, and ensuring sufficient funding for long-term initiatives. Ultimately, the goal is not just to lower the rent-to-income ratio but to foster housing markets that work for everyone.

Understanding No Fee Rentals: Benefits and Process for Renters

You may want to see also

Frequently asked questions

The average rent-to-income ratio is typically around 30%, meaning that households should spend no more than 30% of their gross monthly income on rent to maintain financial stability.

The rent-to-income ratio is calculated by dividing the monthly rent by the monthly gross income and then multiplying by 100 to get a percentage.

The 30% rule is widely accepted as a benchmark because it helps ensure that individuals and families have enough income left for other essential expenses like utilities, groceries, and savings after paying rent.

If your rent-to-income ratio exceeds 30%, you may struggle to cover other living expenses, potentially leading to financial stress or debt. It’s advisable to seek more affordable housing or increase your income.

Yes, the average rent-to-income ratio can vary significantly by location due to differences in housing costs and income levels. In high-cost cities, the ratio may be higher, while in more affordable areas, it may be lower.