Determining the ideal percentage of income for rent is a crucial financial consideration for individuals and families, as it directly impacts overall financial stability and quality of life. A widely accepted guideline, often referred to as the 30% rule, suggests that households should allocate no more than 30% of their gross monthly income to housing costs, including rent. This benchmark helps ensure that individuals have sufficient funds for other essential expenses, such as utilities, groceries, transportation, and savings. However, the ideal percentage can vary based on factors like location, income level, and personal financial goals. For instance, in high-cost urban areas, renters might need to exceed this threshold, while those with lower incomes may aim for a smaller percentage to avoid financial strain. Ultimately, striking the right balance requires careful budgeting and an understanding of one's unique financial circumstances.

Explore related products

What You'll Learn

- Affordability Rules: Common guidelines like 30% rule, its origins, and applicability to different incomes

- Regional Variations: How rent percentages differ by city, state, or country due to cost of living

- Budgeting Tips: Strategies to manage rent within income, including saving and expense prioritization

- Income Fluctuations: Adjusting rent percentage during job changes, raises, or financial instability

- Housing Alternatives: Exploring options like roommates, subsidized housing, or smaller spaces to lower rent burden

![]()

Affordability Rules: Common guidelines like 30% rule, its origins, and applicability to different incomes

The 30% rule, a widely cited guideline for rent affordability, suggests that households should allocate no more than 30% of their gross income to housing costs. This rule originated in the United States during the 1960s as part of federal housing programs, designed to ensure that subsidized housing remained affordable for low-income families. Over time, it has become a benchmark for financial planners, policymakers, and individuals assessing housing budgets. However, its applicability varies significantly depending on income levels, geographic location, and personal financial circumstances.

Analytically, the 30% rule assumes a one-size-fits-all approach, which can be problematic. For high-income earners, spending 30% on rent might be feasible and even conservative, leaving ample funds for savings, investments, and discretionary spending. For instance, someone earning $150,000 annually could comfortably allocate $45,000 to rent without straining their budget. Conversely, for low-income households, this rule often falls short. A family earning $30,000 a year would need to limit rent to $9,000 annually, or $750 per month, which is unrealistic in many urban areas where rents far exceed this threshold. This disparity highlights the rule’s limitations in addressing the diverse financial realities of different income groups.

Instructively, individuals should use the 30% rule as a starting point rather than a rigid mandate. To apply it effectively, calculate your gross monthly income and multiply it by 0.3 to determine your maximum rent budget. For example, if your monthly income is $4,000, your rent should not exceed $1,200. However, adjust this guideline based on your financial obligations, such as debt payments, childcare, or healthcare costs. Additionally, consider regional cost-of-living differences; in high-cost cities like New York or San Francisco, exceeding the 30% threshold might be unavoidable, necessitating trade-offs in other areas of spending.

Persuasively, while the 30% rule has its merits, it fails to account for the complexity of modern financial landscapes. Rising housing costs, stagnant wages, and increasing debt burdens have made this rule less practical for many. Policymakers and financial advisors should advocate for more nuanced affordability metrics that consider factors like local housing markets, household size, and income volatility. For instance, a 40% rule might be more realistic in expensive urban areas, while a 25% rule could encourage savings in lower-cost regions. Tailoring guidelines to specific circumstances would provide more accurate and actionable advice.

Comparatively, other countries have adopted alternative affordability standards. In the UK, the Financial Conduct Authority recommends that housing costs should not exceed 35% of net income, acknowledging the difference between gross and net earnings. In Canada, some financial experts suggest a 25% rule to prioritize savings and debt repayment. These variations underscore the need for context-specific guidelines that reflect local economic conditions and cultural priorities. By learning from global practices, we can refine our approach to rent affordability and create more inclusive financial frameworks.

Descriptively, the 30% rule remains a cornerstone of financial planning, but its effectiveness hinges on thoughtful application. Imagine a young professional earning $60,000 annually in a mid-sized city. Following the 30% rule, their rent budget would be $1,500 per month, allowing them to live comfortably while saving for future goals. Now contrast this with a single parent earning $25,000 in the same city. Their $625 rent budget would likely force them into substandard housing or require them to seek subsidies. This vivid disparity illustrates why a single rule cannot address the spectrum of financial experiences. By acknowledging its limitations and adapting it to individual needs, the 30% rule can remain a useful tool in the broader conversation about housing affordability.

Double Wide Trailers for Rent Near Blue Heron: Availability and Options

You may want to see also

Explore related products

![]()

Regional Variations: How rent percentages differ by city, state, or country due to cost of living

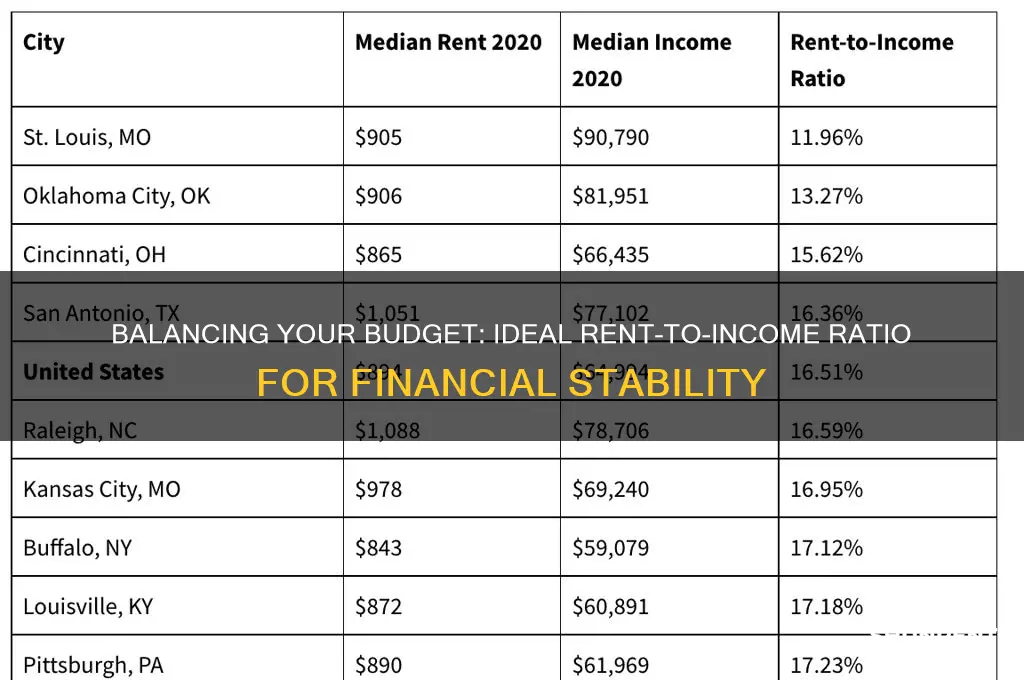

The ideal percentage of income allocated to rent is not a one-size-fits-all figure. A commonly cited rule of thumb is the 30% threshold, but this guideline crumbles under the weight of regional disparities. In San Francisco, where the median rent hovers around $3,700, even dual-income households earning above the national average may find themselves dedicating closer to 45-50% of their income to housing. Conversely, in Tulsa, Oklahoma, where median rents are approximately $850, adhering to the 30% rule is not only feasible but leaves substantial room for savings and discretionary spending.

Consider the case of Berlin, Germany, where rent control policies have historically kept housing costs at roughly 20-25% of the average resident’s income. This contrasts sharply with London, where renters often allocate 40-50% of their earnings to housing, despite having higher average incomes. The divergence highlights how government intervention, market dynamics, and local economies shape affordability. For instance, Berlin’s recent rent freeze aimed to curb skyrocketing costs, while London’s housing market remains largely unregulated, allowing prices to climb unchecked.

Instructively, understanding regional variations requires analyzing both income levels and housing costs. In Mumbai, India, where median incomes are significantly lower than in Western cities, renters often spend 50-60% of their earnings on housing, not due to extravagance but necessity. Here, the 30% rule is not just impractical—it’s unattainable. Conversely, in Zurich, Switzerland, where high wages align with steep rents, the percentage of income spent on housing remains around 30%, demonstrating a balanced affordability model.

Persuasively, policymakers and individuals alike must acknowledge these disparities to create realistic financial plans. For instance, a young professional in New York City should budget closer to 40% of their income for rent, while someone in Austin, Texas, can comfortably aim for 25%. Ignoring regional realities can lead to financial strain or missed opportunities. Tools like cost-of-living calculators and local housing reports can provide tailored insights, ensuring that rent remains a manageable expense rather than a burden.

Comparatively, the global spectrum of rent-to-income ratios reveals systemic issues. In Tokyo, Japan, compact living spaces and efficient public transit allow residents to spend around 30% of their income on rent despite high urban density. Meanwhile, in Nairobi, Kenya, informal settlements and low wages push housing costs to 60% or more of income. These examples underscore the interplay between infrastructure, policy, and economic development in shaping affordability. By studying such variations, we can identify strategies—from zoning reforms to wage adjustments—that address regional challenges effectively.

Unlock Your J7: Removing Rent-A-Center Phone Lock Easily

You may want to see also

Explore related products

![]()

Budgeting Tips: Strategies to manage rent within income, including saving and expense prioritization

A common rule of thumb suggests allocating no more than 30% of your gross income to rent, a guideline rooted in decades of financial planning. This benchmark, however, assumes a stable income, predictable expenses, and a balanced budget—conditions not everyone enjoys. For those earning minimum wage or living in high-cost urban areas, rent often consumes 50% or more of their income, leaving little room for savings, emergencies, or leisure. Understanding this disparity is the first step in crafting a realistic rent-management strategy.

To rein in rent expenses, start by auditing your income and fixed costs. Calculate your monthly take-home pay, then subtract essentials like utilities, groceries, and transportation. What remains is your discretionary income, which should ideally cover rent and still allow for savings. If rent exceeds 30% of your income, consider negotiating with your landlord for a lower rate, especially if you’ve been a reliable tenant. Alternatively, explore roommate arrangements or smaller, more affordable housing options. These steps, though sometimes uncomfortable, can free up funds for other financial priorities.

Saving while paying high rent requires deliberate expense prioritization. Adopt a zero-based budget, where every dollar is assigned a purpose, ensuring no money is wasted on non-essentials. Cut discretionary spending by cooking at home, canceling unused subscriptions, and opting for free activities. Redirect these savings into an emergency fund, aiming to cover at least three months’ worth of living expenses. For renters in their 20s and 30s, consider high-yield savings accounts or retirement plans to maximize growth, even with limited contributions.

A comparative analysis of urban vs. suburban living reveals trade-offs worth considering. While city dwellers often face higher rents, they may save on commuting costs and have access to higher-paying jobs. Suburban renters typically pay less but may incur additional transportation expenses. Weigh these factors based on your lifestyle and career goals. For instance, a remote worker might find relocating to a lower-cost area financially advantageous, while a professional tied to a city center may need to optimize other expenses to balance their budget.

Finally, leverage technology to streamline rent management. Apps like Mint or YNAB can track spending, alert you to overspending, and help you stick to a budget. Set up automatic transfers to a savings account to ensure consistent contributions, even if they’re modest. For renters struggling to meet the 30% threshold, consider government assistance programs or local housing subsidies. These resources, combined with disciplined budgeting, can make rent more manageable and pave the way for financial stability.

Discover Manchester, NH Rentals: Available Properties in a Thriving City

You may want to see also

Explore related products

![]()

Income Fluctuations: Adjusting rent percentage during job changes, raises, or financial instability

Income fluctuations can turn the widely accepted 30% rent-to-income rule into a moving target. A sudden job loss, a raise, or a career shift can drastically alter your financial landscape, making that 30% benchmark feel either overly generous or impossibly tight. For instance, a recent graduate earning $40,000 annually might comfortably allocate $1,000 monthly for rent, but a layoff reducing their income to $25,000 would push that same rent to 48% of their earnings—a financially unsustainable burden. Conversely, a promotion boosting income to $60,000 would lower the rent percentage to 20%, freeing up funds for savings or investments. The key takeaway? Rigidly adhering to a single percentage ignores the dynamic nature of personal finances.

When navigating income changes, a proactive approach is essential. Start by reassessing your budget immediately after a financial shift. If you’ve lost income, prioritize renegotiating rent, downsizing, or temporarily relocating to a more affordable area. For example, someone transitioning from a $70,000 to a $45,000 salary might need to reduce rent from $1,750 to $1,125 to stay within the 30% threshold. Conversely, if your income increases, resist the urge to upscale your housing immediately. Instead, allocate the surplus to emergency funds, debt repayment, or long-term investments. A $10,000 raise doesn’t necessitate a $300 rent increase; it could instead fund a retirement account or pay off high-interest debt.

Financial instability demands a conservative approach to rent allocation. During periods of uncertainty, aim for a lower rent percentage—closer to 25% or even 20%—to build a financial buffer. For instance, a freelancer with irregular income might opt for a studio apartment at $800 instead of a one-bedroom at $1,200, even if their average monthly earnings technically support the latter. This strategy minimizes risk during low-income months. Conversely, those with stable, high-income jobs can afford to push closer to 35% if it means living in a location that enhances career prospects or quality of life.

Finally, consider rent as part of a broader financial ecosystem, not an isolated expense. During job transitions, factor in other costs like commuting, utilities, and groceries, which may fluctuate alongside your income. For example, a remote worker might save on transportation but incur higher utility costs, offsetting some of the rent savings. Similarly, a move to a higher-paying job in a new city might come with increased living expenses, necessitating a more nuanced approach than simply applying the 30% rule. By viewing rent as one piece of a larger financial puzzle, you can adapt more effectively to income changes and maintain financial stability.

The Trade-off: Drugs Over Rent for the Homeless

You may want to see also

Explore related products

$15.99 $15.99

![]()

Housing Alternatives: Exploring options like roommates, subsidized housing, or smaller spaces to lower rent burden

The 30% rule, a widely accepted guideline, suggests that households should allocate no more than 30% of their gross income to housing costs. However, in high-cost urban areas, this threshold is often exceeded, leaving many individuals and families struggling to make ends meet. To alleviate this burden, exploring alternative housing options can be a strategic move. One of the most straightforward methods is sharing living spaces with roommates. By splitting rent and utilities, individuals can significantly reduce their monthly expenses. For example, a $1,500 studio apartment shared by two people effectively lowers each person’s housing cost to $750, freeing up income for savings, investments, or other necessities. This approach not only eases financial strain but also fosters a sense of community and shared responsibility.

Subsidized housing programs offer another viable alternative for those who qualify. These initiatives, often funded by government or nonprofit organizations, provide rental assistance to low- and moderate-income households. For instance, Section 8 Housing Choice Vouchers in the United States cap rent payments at 30% of a tenant’s income, with the program covering the remainder. Eligibility typically depends on income level, family size, and local median income thresholds. While application processes can be lengthy and competitive, securing subsidized housing can dramatically reduce rent burden, allowing individuals to allocate more resources to education, healthcare, or debt repayment.

Downsizing to smaller living spaces is a third strategy to lower rent costs. A shift from a two-bedroom apartment to a studio or micro-unit can result in savings of 20–40%, depending on the market. This approach requires a mindful reassessment of needs versus wants, such as prioritizing location over square footage or opting for minimalist living. For young professionals or empty nesters, smaller spaces often align with lifestyle goals, reducing not only rent but also utility and maintenance costs. Practical tips include decluttering before moving, investing in multifunctional furniture, and leveraging vertical storage solutions to maximize limited space.

Each of these alternatives—roommates, subsidized housing, and smaller spaces—offers distinct advantages but also requires careful consideration. Sharing living spaces demands compatibility and clear communication to avoid conflicts. Subsidized housing necessitates navigating bureaucratic processes and meeting strict eligibility criteria. Downsizing, while cost-effective, may entail sacrificing comfort or privacy. However, when executed thoughtfully, these strategies can significantly reduce rent burden, bringing housing expenses closer to the ideal 30% threshold. By exploring these options, individuals can regain financial flexibility and build a more sustainable living situation tailored to their unique circumstances.

Who Rents Out 1448 South Kiel Indianapolis Indiana?

You may want to see also

Frequently asked questions

The ideal percentage of income for rent is generally considered to be around 30% or less. This guideline, often referred to as the "30% rule," helps ensure that you have enough income left for other expenses and savings.

The 30% rule is recommended because it balances housing costs with other financial responsibilities. Spending more than 30% on rent can strain your budget, making it harder to cover essentials like groceries, utilities, and savings for emergencies or long-term goals.

No, the 30% rule is a general guideline and may not fit everyone’s financial situation. Factors like high cost of living, income level, debt obligations, and personal financial goals can influence what percentage of income is reasonable for rent.

If your rent exceeds 30% of your income, consider downsizing, finding a roommate, or relocating to a more affordable area. Additionally, increasing your income through side jobs or negotiating a raise can help bring your rent-to-income ratio closer to the ideal range.