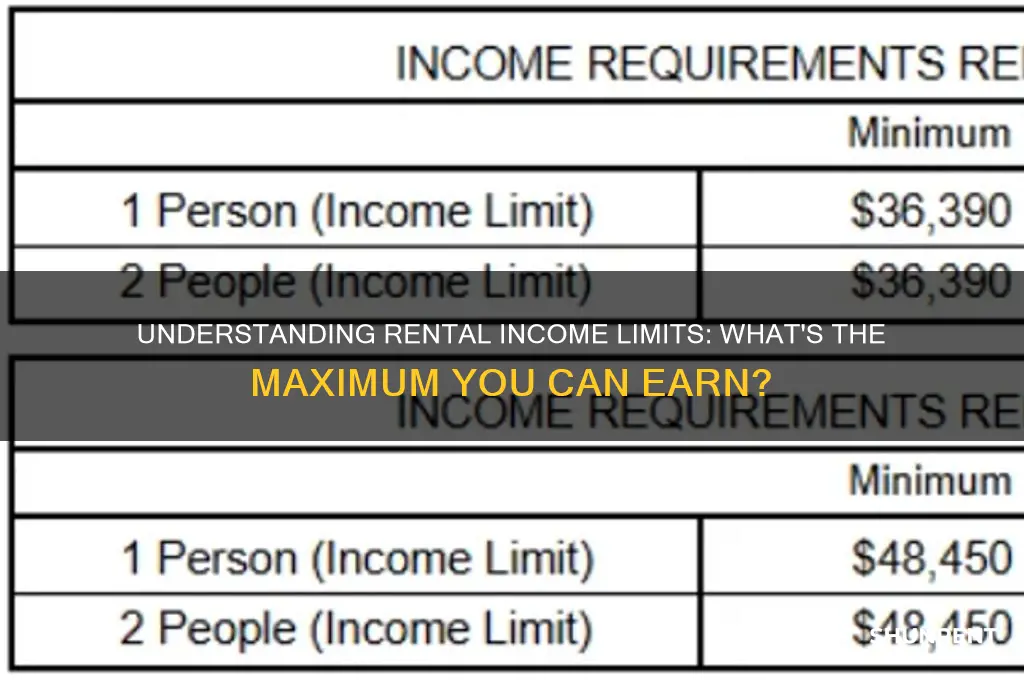

When considering renting a property, one crucial factor that landlords and property managers often evaluate is the prospective tenant's annual income. The maximum annual income limit for renting typically refers to the highest income threshold a tenant can have to qualify for certain types of housing, such as subsidized or affordable housing programs. These limits are usually set by government agencies or housing authorities to ensure that rental assistance or affordable units are allocated to individuals and families who genuinely need them. For market-rate rentals, while there isn’t a strict income cap, landlords commonly require tenants to earn at least 2.5 to 3 times the monthly rent to ensure they can afford the payments. Understanding these income limits is essential for both tenants seeking affordable housing and landlords aiming to comply with regulations and maintain financial stability.

Explore related products

What You'll Learn

- Income Limits by Housing Program: Varies by program (e.g., HUD, Section 8) and location

- Area Median Income (AMI) Role: AMI determines eligibility for affordable housing options

- Rent-to-Income Ratio: Generally, rent should not exceed 30% of gross income

- Local vs. Federal Limits: Local limits may differ from federal guidelines based on cost of living

- Income Verification Process: Landlords require proof of income (e.g., pay stubs, tax returns)

![]()

Income Limits by Housing Program: Varies by program (e.g., HUD, Section 8) and location

Income limits for renting are not one-size-fits-all. They vary significantly depending on the housing program and geographic location, creating a complex landscape for renters to navigate. This variability is intentional, designed to address the diverse needs of low- to moderate-income households across different regions. For instance, the U.S. Department of Housing and Urban Development (HUD) sets income limits for programs like Section 8 Housing Choice Vouchers and Public Housing, but these limits are adjusted annually based on the Area Median Income (AMI) of each locality. A family eligible for assistance in a rural area might exceed the income limit in a high-cost urban center, highlighting the importance of location-specific thresholds.

To illustrate, consider the Section 8 program, which caps eligibility at 50% of the AMI in most cases, but allows for exceptions up to 80% in certain circumstances. In San Francisco, where the AMI is over $100,000, a family of four earning $80,000 might still qualify, whereas in a smaller city with an AMI of $50,000, the same income would likely exceed the limit. HUD’s Low-Income Housing Tax Credit (LIHTC) program further complicates this by allowing states to define income limits within a federal framework, often ranging from 20% to 60% of AMI. This flexibility ensures that housing assistance aligns with local economic realities but requires renters to research limits specific to their area and program.

Navigating these limits requires a proactive approach. Start by identifying the AMI for your county or metropolitan area, which HUD publishes annually. Next, determine the income threshold for your desired housing program—whether it’s 30%, 50%, or 80% of the AMI. For example, if you’re applying for a LIHTC property in Texas, check if the state uses a 50% or 60% AMI limit. Online tools like HUD’s Income Limit Dataset can streamline this process, providing precise figures based on household size and location. Keep in mind that income limits are not static; they are updated each year, so verify the current figures before applying.

A critical takeaway is that income limits are not barriers but tools to ensure housing assistance reaches those who need it most. If your income exceeds the limit for one program, explore alternatives. For instance, Project-Based Section 8 or HOME Investment Partnerships Program may have different eligibility criteria. Additionally, some programs offer exceptions for households with elderly or disabled members, allowing slightly higher incomes. Understanding these nuances can open doors to affordable housing options that might otherwise seem out of reach.

In practice, renters should treat income limits as a starting point, not an endpoint. Gather documentation of your income, household size, and any special circumstances (e.g., disability or veteran status) to present a comprehensive case to housing authorities. Remember, the goal of these programs is to provide stability, not to exclude. By understanding the intricacies of income limits, you can position yourself to access the housing assistance you need, regardless of where you live or which program you pursue.

Renting a Balcony on Bourbon Street: Your Ultimate Guide to NOLA Fun

You may want to see also

Explore related products

![]()

Area Median Income (AMI) Role: AMI determines eligibility for affordable housing options

The concept of Area Median Income (AMI) is pivotal in the realm of affordable housing, acting as a gatekeeper that determines who qualifies for subsidized rent. AMI is not a static figure but a dynamic metric that varies by location, household size, and year, reflecting the economic pulse of a specific region. For instance, in high-cost urban areas like San Francisco, the AMI for a family of four might exceed $120,000, while in rural areas, it could be closer to $60,000. Understanding AMI is the first step for renters to navigate the complex landscape of affordable housing programs.

To illustrate, consider a family of three in Los Angeles, where the 2023 AMI is approximately $86,000. Affordable housing programs often target households earning between 30% and 80% of AMI. For this family, eligibility would mean an annual income between $25,800 and $68,800. However, the calculation isn’t just about income; it’s about how that income stacks up against the local median. A family earning $70,000 in Los Angeles might not qualify for certain programs, while the same income in a lower-cost city could make them eligible. This highlights the importance of local context in AMI calculations.

One practical tip for renters is to use HUD’s Income Limits Dataset, which provides AMI figures for every county and metro area in the U.S. This tool allows individuals to input their location and household size to determine the AMI thresholds. Additionally, many affordable housing applications require proof of income, such as tax returns or pay stubs, to verify eligibility. Renters should gather these documents in advance to streamline the application process. It’s also worth noting that AMI limits are updated annually, so staying informed about the latest figures is crucial.

A common misconception is that AMI limits are universally low, excluding middle-income earners. However, programs like the Low-Income Housing Tax Credit (LIHTC) often serve households earning up to 60% of AMI, while others, like Section 8, may extend to 80% or higher. For example, in Chicago, a household earning up to $70,000 (80% of AMI for a family of four) could qualify for certain affordable units. This broader range underscores the role of AMI in making affordable housing accessible to a wider demographic, not just the lowest earners.

In conclusion, AMI serves as a critical benchmark for affordable housing eligibility, tailored to the economic realities of specific areas. By understanding how AMI is calculated and applied, renters can better assess their eligibility for programs and take proactive steps to secure affordable housing. Whether through online tools, income documentation, or staying updated on annual limits, navigating AMI is essential for anyone seeking rent relief in today’s housing market.

Should You Keep Your Condo? Pros and Cons of Renting It Out

You may want to see also

Explore related products

![]()

Rent-to-Income Ratio: Generally, rent should not exceed 30% of gross income

A widely accepted rule of thumb in personal finance is that rent should not exceed 30% of an individual's gross income. This rent-to-income ratio serves as a benchmark for affordability, ensuring that tenants can comfortably manage their housing expenses without compromising other financial obligations. For instance, if your annual gross income is $60,000, your monthly income is approximately $5,000, and 30% of that would be $1,500—your ideal maximum monthly rent. This guideline helps prevent financial strain and promotes a balanced budget.

However, adhering to the 30% rule isn’t always feasible, especially in high-cost-of-living areas like New York City or San Francisco, where rents often surpass this threshold. In such cases, tenants may need to adjust their budgets by cutting discretionary spending, seeking roommates, or exploring government housing assistance programs. It’s also crucial to consider net income (after taxes and deductions) for a more realistic assessment, as gross income can sometimes paint an overly optimistic picture. For example, if your net monthly income is $4,000, a $1,500 rent would actually consume 37.5% of your take-home pay, pushing you beyond the recommended limit.

Landlords and property managers frequently use the rent-to-income ratio as a screening tool to assess a tenant’s ability to pay rent consistently. Many require that an applicant’s income be at least three times the monthly rent. For instance, to qualify for a $1,500 apartment, you’d need a monthly income of $4,500. This standard helps minimize the risk of default and ensures a stable rental agreement. Prospective tenants should prepare proof of income, such as pay stubs or tax returns, to streamline the application process.

While the 30% rule is a helpful starting point, it’s not one-size-fits-all. Individual circumstances, such as debt obligations, savings goals, or lifestyle choices, may necessitate a lower rent-to-income ratio. For example, someone with significant student loan payments might aim for 25% or less to maintain financial flexibility. Conversely, those with minimal expenses or high disposable income may comfortably exceed the 30% mark. The key is to evaluate your unique financial situation and prioritize long-term stability over short-term convenience.

Ultimately, the rent-to-income ratio is a critical tool for both tenants and landlords, fostering financial responsibility and reducing the risk of eviction or default. By staying within the 30% guideline, tenants can avoid the pitfalls of rent burden, such as accumulating debt or sacrificing essential expenses like healthcare or groceries. For those struggling to meet this threshold, exploring alternatives like relocating to a more affordable area, negotiating rent terms, or increasing income through side gigs can provide much-needed relief. In the end, balancing rent with income isn’t just about affordability—it’s about building a sustainable financial future.

Turo Car Rental Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Local vs. Federal Limits: Local limits may differ from federal guidelines based on cost of living

Income limits for renting are not one-size-fits-all. While federal guidelines provide a baseline, local variations reflect the stark reality of cost-of-living disparities across the United States. For instance, a household earning $75,000 annually might qualify for affordable housing in Tulsa, Oklahoma, but struggle to find eligible rentals in San Francisco, where the median rent exceeds $4,000 per month. This discrepancy highlights the necessity of local adjustments to federal standards.

Federal guidelines, such as those set by the Department of Housing and Urban Development (HUD), typically define income limits as a percentage of the Area Median Income (AMI). For example, a household earning 80% of the AMI may qualify for certain rental assistance programs. However, these thresholds often fail to account for hyper-local economic conditions. In high-cost cities like New York or Los Angeles, even households earning above the federal limit may face housing insecurity due to skyrocketing rents. Conversely, in rural areas with lower living costs, federal limits might exclude households that genuinely need assistance.

Local governments and housing authorities address this gap by implementing region-specific income limits. For example, in Seattle, the income threshold for affordable housing is often set at 60% of the local AMI, while in Detroit, it might be closer to 50%. These adjustments ensure that rental assistance programs remain accessible to those who need them most within their respective communities. Prospective renters should consult local housing authority websites or use online calculators to determine their eligibility based on their city or county’s criteria.

A practical tip for renters navigating these limits is to compare both federal and local guidelines. Start by checking HUD’s income limit tables for your state, then cross-reference with your city or county’s housing authority data. For example, in Austin, Texas, the federal limit for a family of four might be $70,000, but local programs could cap eligibility at $60,000 due to rising housing costs. Understanding these nuances can save time and prevent frustration during the rental search.

Ultimately, the interplay between local and federal income limits underscores the complexity of housing affordability. While federal guidelines provide a framework, local adjustments ensure that rental assistance remains relevant to the economic realities of specific regions. Renters must stay informed about both levels of criteria to make informed decisions and access the support they need.

Mastering Per Diem Rent Calculations: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Income Verification Process: Landlords require proof of income (e.g., pay stubs, tax returns)

Landlords often set a maximum annual income limit for renting to ensure tenants can comfortably afford the rent. This limit typically ranges from 30% to 40% of the tenant’s gross annual income, meaning rent should not exceed this percentage to maintain financial stability. For example, if a tenant earns $60,000 annually, their monthly rent should ideally be between $1,500 and $2,000. However, verifying this income is crucial to avoid rental defaults, which is where the income verification process comes into play.

The income verification process is a critical step in the rental application, designed to confirm a tenant’s financial capability. Landlords typically request pay stubs, tax returns, or bank statements as proof of income. Pay stubs are the most common, offering a snapshot of earnings over recent months, while tax returns provide a broader view of annual income. For self-employed individuals, profit and loss statements or 1099 forms may be required. This documentation ensures transparency and helps landlords assess whether the tenant meets the income threshold.

While the process is straightforward, tenants should be prepared for potential challenges. For instance, freelancers or gig workers may struggle to provide consistent income proof due to fluctuating earnings. In such cases, landlords might request additional documentation, like client contracts or invoices, to verify income stability. Tenants should also be cautious of red flags, such as landlords demanding excessive personal financial information beyond standard proof of income, which could indicate a scam.

To streamline the process, tenants can take proactive steps. Organize financial documents in advance, ensuring pay stubs and tax returns are readily available. If income is irregular, create a summary sheet detailing monthly earnings and sources. Additionally, be transparent about any financial limitations or unique income structures. This not only builds trust but also increases the likelihood of approval, even if income slightly deviates from the ideal limit.

In conclusion, the income verification process is a safeguard for both landlords and tenants, ensuring rental agreements are sustainable. By understanding the required documentation and preparing accordingly, tenants can navigate this step with confidence. Landlords, in turn, gain assurance that tenants meet the income criteria, fostering a stable rental relationship. Whether through pay stubs, tax returns, or alternative proofs, this process is a cornerstone of responsible renting.

Understanding Acceptable Rent-to-Income Ratios for Financial Stability

You may want to see also

Frequently asked questions

The maximum annual income limit for renting varies depending on the specific rental program or housing authority. For example, in subsidized housing programs like Section 8, the limit is typically set at 50% to 80% of the Area Median Income (AMI) for the region.

No, the max annual income limit typically applies only to subsidized or affordable housing programs. Market-rate rentals generally do not have income limits, though landlords may require that your income is at least 2-3 times the monthly rent.

The limit is usually based on the Area Median Income (AMI) for the specific geographic area. Housing authorities or programs set the threshold as a percentage of the AMI, often ranging from 50% to 120%, depending on the program’s target population.

Yes, if your income exceeds the limit for subsidized housing, you can rent market-rate properties without income restrictions. However, you may not qualify for rental assistance programs like Section 8 or affordable housing units.

Some programs may offer exceptions or waivers for certain populations, such as seniors, veterans, or individuals with disabilities. Additionally, income limits may be adjusted for household size or special circumstances, so it’s best to check with the specific program or housing authority.