The maximum rent-to-income ratio is a critical financial metric used to determine how much of a person's income should ideally be allocated to housing expenses, ensuring affordability and financial stability. Typically recommended at 30% or less, this ratio compares monthly rent to gross monthly income, helping individuals and families avoid becoming rent-burdened. Exceeding this threshold can strain budgets, limit savings, and increase the risk of financial hardship. Landlords and lenders often use this ratio to assess a tenant's or borrower's ability to manage housing costs, while policymakers reference it to address housing affordability issues. Understanding and adhering to this ratio is essential for both renters and homeowners to maintain a balanced and sustainable financial lifestyle.

| Characteristics | Values |

|---|---|

| Definition | The maximum percentage of a tenant's gross income that should be spent on rent. |

| Commonly Accepted Ratio | 30% (widely used as a standard by housing experts and government programs) |

| Purpose | Ensures affordability and prevents financial strain on tenants. |

| Variations by Region | May differ based on local housing markets and cost of living. |

| Lender Requirements | Often used by lenders to assess rental property investment viability. |

| Government Programs | Programs like Section 8 in the U.S. use this ratio to determine eligibility. |

| Impact on Tenants | Helps tenants avoid being "rent-burdened" (spending >30% on housing). |

| Flexibility | Some markets may accept higher ratios due to higher incomes or demand. |

| Latest Trend | Increasing rent prices are pushing ratios higher in many urban areas. |

| Alternative Ratios | Some suggest 25% or 28% for more conservative budgeting. |

Explore related products

What You'll Learn

![]()

Affordable Housing Standards

The concept of affordable housing often hinges on the rent-to-income ratio, a metric that determines whether housing costs are sustainable for individuals or families. A widely accepted standard is that housing should not exceed 30% of gross monthly income. This threshold, established by the U.S. Department of Housing and Urban Development (HUD), serves as a benchmark for affordability. Exceeding this ratio can strain household budgets, leaving insufficient funds for other essentials like food, healthcare, and transportation. For instance, a family earning $4,000 monthly should ideally spend no more than $1,200 on rent to maintain financial stability.

However, this 30% rule is not universally applicable. In high-cost urban areas like San Francisco or New York, where median rents often surpass $3,000, adhering to this ratio is nearly impossible for low- to middle-income households. In such markets, policymakers and housing advocates sometimes adjust the threshold to 40% or even 50% of income to reflect economic realities. These adjustments highlight the need for localized standards that account for regional cost disparities. Without such flexibility, affordability standards risk becoming disconnected from the lived experiences of residents.

Implementing affordable housing standards requires a multi-faceted approach. Governments can incentivize developers through tax credits or density bonuses for building units that meet affordability criteria. For example, the Low-Income Housing Tax Credit (LIHTC) program in the U.S. encourages the construction of affordable units by offering tax benefits to developers. Additionally, rent control policies can cap annual rent increases, preventing costs from outpacing income growth. However, such measures must be balanced to avoid disincentivizing new construction, which could exacerbate housing shortages.

A critical challenge in enforcing affordability standards is ensuring compliance and transparency. Landlords and developers may attempt to circumvent regulations, necessitating robust monitoring mechanisms. Tenants should be empowered to report violations, and governments must impose penalties for non-compliance. For instance, in Berlin, Germany, a rent cap law was introduced in 2020 to curb skyrocketing rents, but its effectiveness relied heavily on tenant activism and legal enforcement. Such examples underscore the importance of active oversight in maintaining affordable housing standards.

Ultimately, affordable housing standards are not just about numbers but about creating equitable communities. By anchoring policies in realistic rent-to-income ratios, governments can prevent displacement and foster inclusive growth. Practical steps include conducting regular housing needs assessments, engaging stakeholders in policy design, and leveraging technology for transparent monitoring. For individuals, understanding these standards empowers them to advocate for fair housing practices. Affordable housing is a cornerstone of social and economic stability, and its standards must evolve to meet the needs of diverse populations.

Student Population: Rent Rates Influenced?

You may want to see also

Explore related products

![]()

Landlord Screening Criteria

A common rule of thumb in the rental market is the 30% rent-to-income ratio, suggesting tenants should spend no more than 30% of their gross monthly income on rent. However, this guideline often falls short in high-cost urban areas, where rents can consume 40-50% of income. Landlords must balance risk and practicality when setting screening criteria, as rigid adherence to a single ratio may exclude otherwise qualified tenants.

Analyzing Tenant Affordability Beyond the Ratio

While the rent-to-income ratio is a starting point, it’s not the sole determinant of a tenant’s ability to pay. Landlords should consider additional factors such as credit history, employment stability, and debt-to-income ratio. For instance, a tenant with a 40% rent-to-income ratio but minimal debt and a high credit score may pose less risk than someone at 28% with maxed-out credit cards. Practical tip: Use a scoring system that weighs income ratio (e.g., 30% = 10 points, 40% = 8 points) alongside other financial metrics to create a holistic tenant profile.

Adjusting Criteria for Market Realities

In competitive markets, landlords may need to relax the rent-to-income threshold to attract tenants. For example, in cities like San Francisco or New York, where rents often exceed 50% of median incomes, a 30% rule is impractical. Instead, consider requiring proof of additional income sources, such as investments or side hustles, or allow co-signers to mitigate risk. Caution: Avoid lowering standards too far, as consistently high rent-to-income ratios increase the likelihood of late payments or defaults.

Incorporating Flexibility for Special Cases

Not all tenants fit neatly into a one-size-fits-all screening model. Retirees, students, or freelancers may have irregular income streams but substantial savings or guarantors. Landlords can adapt by requesting bank statements showing 3-6 months’ worth of rent in savings or requiring a larger security deposit. Example: A retiree with a 45% rent-to-income ratio but $50,000 in savings could be a lower risk than a salaried worker at 30% with no emergency fund.

The rent-to-income ratio is a valuable tool, but it’s most effective when paired with a nuanced screening approach. Landlords should prioritize consistency, fairness, and adaptability, ensuring criteria align with both market conditions and tenant realities. By focusing on the bigger financial picture, landlords can secure reliable tenants while minimizing vacancy risks. Practical takeaway: Regularly review and adjust screening criteria to reflect local rent trends and tenant demographics.

Rent Hikes: A Forced Move?

You may want to see also

Explore related products

![]()

Tenant Financial Stability

A common rule of thumb suggests that tenants should spend no more than 30% of their gross monthly income on rent. This benchmark, often referred to as the 30% rule, is widely accepted as a measure of financial stability for renters. Exceeding this threshold can strain a tenant’s budget, leaving insufficient funds for essentials like groceries, utilities, and savings. For example, a tenant earning $4,000 monthly should ideally pay no more than $1,200 in rent to maintain a balanced budget. However, this rule isn’t one-size-fits-all; individual circumstances, such as debt obligations or high living costs in urban areas, may necessitate adjustments.

Analyzing the 30% rule reveals its limitations in high-cost housing markets. In cities like San Francisco or New York, where rents often surpass $3,000 monthly, even dual-income households may struggle to stay within this ratio. For instance, a couple earning a combined $10,000 monthly would need to spend $3,000 on rent to meet the 30% threshold, yet median rents in these cities frequently exceed this amount. In such cases, tenants may need to allocate closer to 40-50% of their income to housing, but this requires meticulous budgeting to avoid financial instability. Landlords in these markets often look for tenants earning at least three times the monthly rent to mitigate risk.

To ensure tenant financial stability, landlords and property managers should adopt a holistic approach beyond the rent-to-income ratio. Screening tenants based on credit scores, employment history, and debt-to-income ratios provides a more comprehensive financial profile. For example, a tenant with a 700+ credit score and low debt obligations may be a safer bet, even if their rent-to-income ratio slightly exceeds 30%. Additionally, requiring proof of income, such as pay stubs or bank statements, can verify a tenant’s ability to meet rental payments consistently.

Practical tips for tenants include building an emergency fund equivalent to 3-6 months’ rent and prioritizing high-interest debt repayment to free up income. For instance, paying off a credit card with a 20% APR before committing to a higher rent can improve financial flexibility. Tenants should also negotiate lease terms, such as longer rental periods or upfront payments, to secure lower monthly rents. In competitive markets, offering to sign a 2-year lease instead of a 1-year lease might incentivize landlords to reduce rent by 5-10%, easing the financial burden.

Ultimately, tenant financial stability hinges on a balance between affordability and lifestyle choices. While the 30% rule serves as a useful guideline, it’s not absolute. Tenants must weigh their priorities—whether it’s living in a prime location, having extra amenities, or saving for long-term goals—and adjust their budgets accordingly. Landlords, meanwhile, should focus on attracting tenants with stable, verifiable income rather than rigidly adhering to a single ratio. By fostering transparency and flexibility, both parties can achieve a sustainable rental arrangement that minimizes financial risk.

Understanding HUD Rent Limits in Illinois: What Tenants Need to Know

You may want to see also

Explore related products

![]()

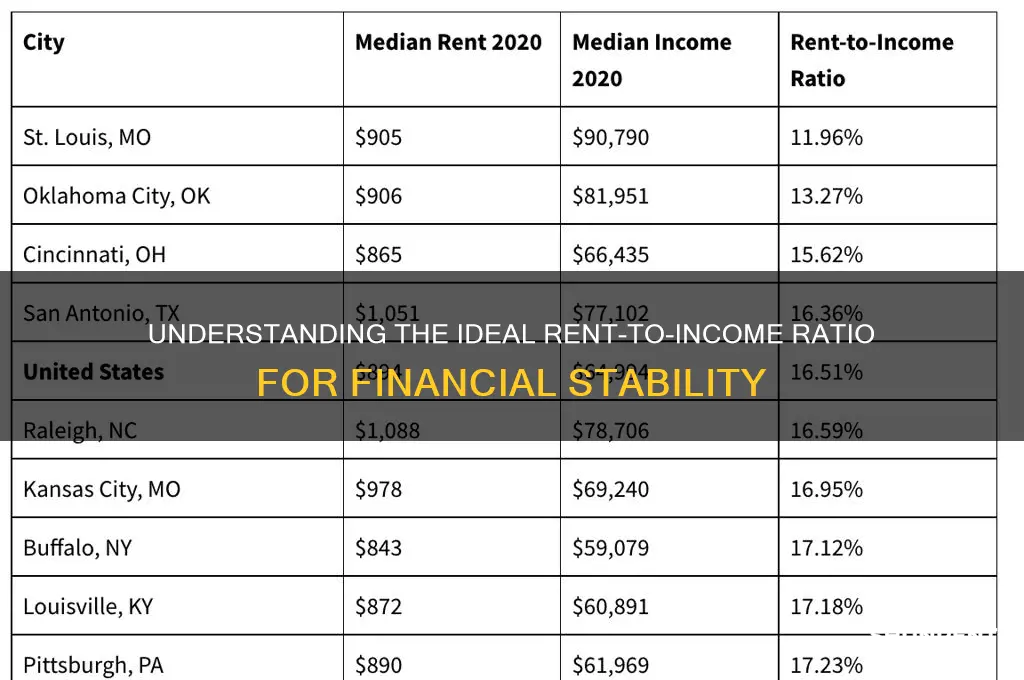

Regional Rent Variations

Rent-to-income ratios are not one-size-fits-all, and regional variations play a significant role in determining what is considered affordable. In high-cost urban centers like New York City or San Francisco, renters often face ratios exceeding 30%, the threshold traditionally deemed manageable. For instance, in San Francisco, where the median rent hovers around $3,700, a household earning the median income of $110,000 would allocate approximately 40% of their earnings to rent. This contrasts sharply with smaller cities like Indianapolis, where the median rent is around $1,200, and the median income of $50,000 results in a ratio of about 29%. These disparities highlight the need for region-specific affordability benchmarks.

To navigate regional rent variations, consider the 50/30/20 budget rule as a flexible framework. In expensive markets, aim to keep housing costs below 40% of income by prioritizing shared living arrangements or seeking rent-controlled units. For example, in Los Angeles, where the average rent is $2,500, a single earner making $60,000 annually could reduce their ratio from 50% to 33% by splitting rent with a roommate. Conversely, in affordable regions like Tulsa, where rent averages $900, households can comfortably allocate 20% of a $45,000 income to housing, freeing up funds for savings or investments.

Policy interventions also reflect regional realities. In Seattle, where the rent-to-income ratio averages 28%, local ordinances cap annual rent increases at 3%, providing stability for tenants. Meanwhile, in Miami, where ratios can reach 45%, initiatives like the Housing Trust Fund aim to subsidize affordable units. Renters should research such programs in their area, as they can significantly mitigate the financial strain of high housing costs. For instance, Miami’s Section 8 voucher program reduces rent burdens for low-income families, effectively lowering their ratio to a sustainable 30%.

Ultimately, understanding regional rent variations empowers renters to make informed decisions. In expensive markets, consider relocating to nearby suburbs or negotiating lease terms, such as longer contracts in exchange for lower monthly payments. In affordable regions, take advantage of lower ratios to build financial resilience through emergency funds or retirement savings. By tailoring strategies to local conditions, renters can achieve housing stability without compromising their overall financial health.

Finding Office Rentals: A Guide to Locating Someone's Workspace

You may want to see also

Explore related products

$61.95 $32

$59.95 $64.99

![]()

Government Rent Guidelines

Governments often intervene in rental markets to ensure housing affordability, particularly for low- and middle-income households. One key tool is establishing rent guidelines that cap annual rent increases, balancing landlord profitability with tenant stability. For instance, New York City’s Rent Guidelines Board annually determines percentage increases for rent-stabilized apartments, considering factors like operating costs, inflation, and tenant affordability. In 2023, the board approved a 2-3% increase for one-year leases, reflecting a compromise between landlord demands and tenant advocacy. Such guidelines prevent sudden, drastic rent hikes that could displace residents, especially in high-demand urban areas.

While rent increase caps address existing tenants, some governments also set maximum rent-to-income ratios for new leases to ensure affordability from the outset. For example, in Germany, many cities enforce a rule that rent should not exceed 30% of a tenant’s net income. This threshold is derived from the widely accepted affordability standard used by housing agencies globally. However, enforcement varies, and tenants often must self-report income, creating loopholes. Advocates argue for stricter verification processes, while critics warn of administrative burdens and reduced housing supply if landlords face excessive regulation.

A contrasting approach emerges in Singapore, where public housing dominates the market. The Housing and Development Board (HDB) ties rent directly to income for low-wage earners, ensuring no household spends more than 25-30% of their monthly earnings on rent. This model relies on extensive government intervention, including subsidies and income verification, which may not be feasible in less centralized systems. However, it demonstrates how rent-to-income ratios can be proactively managed when housing is treated as a public good rather than a purely market-driven commodity.

For policymakers, the challenge lies in designing guidelines that are both enforceable and adaptable. Dynamic rent controls, which adjust based on local economic conditions, offer a middle ground. For instance, Oregon’s statewide rent control law caps annual increases at 7% plus the Consumer Price Index, ensuring flexibility while preventing excessive hikes. Pairing such measures with incentives for landlords, like tax breaks for maintaining affordable units, can mitigate supply concerns. Ultimately, effective government rent guidelines require a nuanced understanding of regional housing markets and a commitment to prioritizing affordability over unfettered market forces.

Renting a Caf in Panama City: Pros, Cons, and Key Considerations

You may want to see also

Frequently asked questions

The maximum rent-to-income ratio is generally considered to be 30%, meaning that a tenant should not spend more than 30% of their gross monthly income on rent and utilities.

The rent-to-income ratio is calculated by dividing the monthly rent by the tenant's gross monthly income. For example, if the rent is $1,000 per month and the tenant's gross monthly income is $4,000, the rent-to-income ratio would be 25% ($1,000 ÷ $4,000 = 0.25).

The 30% rent-to-income ratio is important because it helps tenants avoid financial strain and ensures they have enough income left over for other essential expenses such as food, transportation, and savings. Exceeding this ratio can lead to difficulty in covering unexpected costs and may result in financial instability.