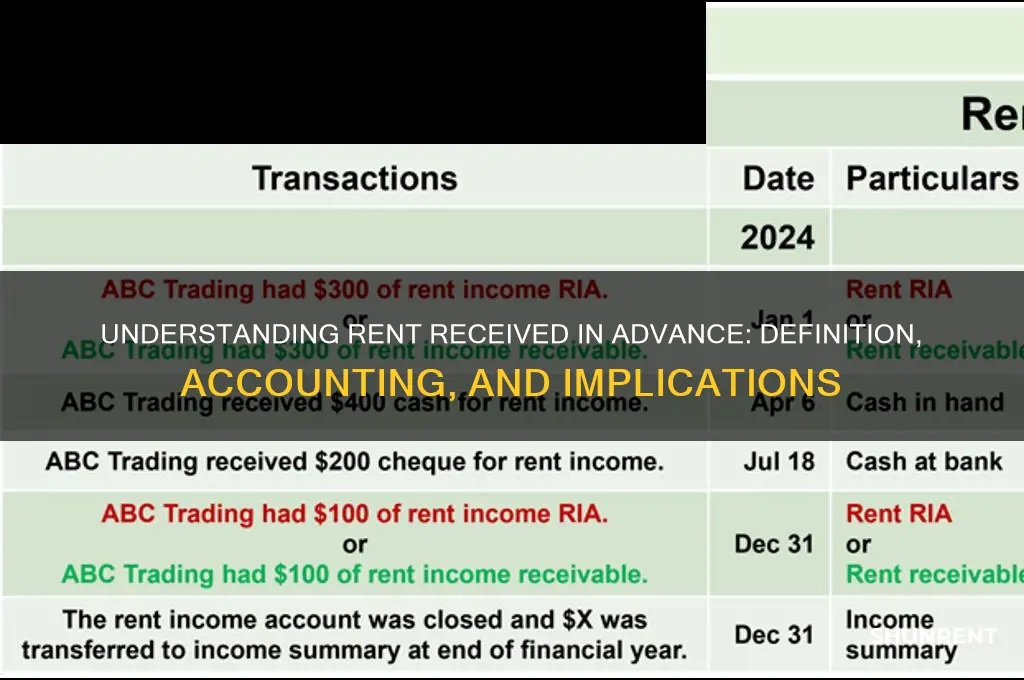

Rent received in advance refers to payments made by a tenant to a landlord for the use of a property before the rental period to which the payment corresponds. Essentially, it is a prepayment for future occupancy or usage of the property. This type of payment is recorded as a liability on the landlord's balance sheet under deferred revenue or unearned revenue, as the landlord has not yet provided the service (i.e., the rental period) for which the payment was made. Over time, as the rental period progresses, the landlord recognizes the advance payment as income, typically on a monthly basis, to reflect the earned portion of the rent. Proper accounting for rent received in advance is crucial for accurate financial reporting and tax compliance.

| Characteristics | Values |

|---|---|

| Definition | Rent received in advance refers to the payment of rent by a tenant to a landlord before the rental period it covers. |

| Accounting Treatment | It is recorded as a liability (unearned revenue) on the landlord's balance sheet until the rental period is completed. |

| Recognition | Revenue is recognized over the period the rent covers, not at the time of receipt. |

| Example | A tenant pays $1,200 on January 1 for rent covering February 1 to February 28. The landlord records $1,200 as a liability in January and recognizes $1,200 as revenue in February. |

| Tax Implications | In many jurisdictions, rent received in advance is taxable in the year it is earned, not when it is received. |

| Reporting | It is typically reported under current liabilities on the balance sheet and adjusted in the income statement over the rental period. |

| Importance | Ensures accurate financial reporting by matching revenue with the period it is earned, adhering to the accrual accounting principle. |

| Common Practice | Widely used in real estate and leasing industries to manage cash flow and financial obligations. |

| Adjustment | Requires periodic adjustments to transfer the liability to revenue as the rental period progresses. |

| Compliance | Must comply with accounting standards such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards). |

Explore related products

What You'll Learn

![]()

Definition of Rent Received in Advance

Rent received in advance refers to a payment made by a tenant to a landlord before the rental period it covers. This scenario is common in both residential and commercial leasing, where tenants may pay one or more months’ rent upfront. For instance, a tenant might pay the first and last month’s rent at the beginning of a lease, with the last month serving as a security deposit or future rent payment. This practice benefits landlords by ensuring cash flow stability and reducing the risk of late payments, while tenants may secure favorable terms or avoid monthly transactions.

From an accounting perspective, rent received in advance is classified as a liability on the landlord’s balance sheet. This is because the landlord has an obligation to provide rental services in the future, even though the payment has already been collected. For example, if a tenant pays $1,200 in January for rent covering February, the landlord records $1,200 as a liability until February, when it is recognized as revenue. This treatment aligns with the accrual accounting principle, which matches income with the period it earns.

Tax implications of rent received in advance vary by jurisdiction but generally follow the same principle: income is taxable in the year it is earned, not when it is received. For instance, in the U.S., landlords must report advance rent as income in the tax year corresponding to the rental period, not the year of receipt. This requires careful record-keeping to avoid overpaying taxes in the current year and underpaying in the future. Tenants, meanwhile, cannot claim deductions for prepaid rent until the period it covers.

Practical management of rent received in advance involves clear lease agreements and meticulous tracking. Landlords should specify in the lease how advance payments will be applied, whether as security deposits, last month’s rent, or future rent. Using accounting software can automate the process, ensuring liabilities are correctly recorded and revenue is recognized in the appropriate period. For tenants, verifying how advance payments are handled can prevent disputes over refunds or deductions at the end of the lease.

In summary, rent received in advance is a prepaid rental payment that serves as a liability until the period it covers. Its benefits include financial security for landlords and convenience for tenants, but it requires precise accounting and tax compliance. By understanding its definition, classification, and management, both parties can navigate this common leasing practice effectively, ensuring transparency and adherence to financial principles.

Understanding Rent's Iconic Contact Scene: Themes, Symbolism, and Impact

You may want to see also

Explore related products

![]()

Accounting Treatment for Advance Rent

Rent received in advance presents a unique accounting challenge: how to recognize revenue when cash is received before the service (occupancy) is provided. This scenario demands a departure from simple cash-basis accounting, where revenue is recorded upon receipt. Instead, accrual accounting principles dictate matching revenue with the period it is earned, not when payment is received.

Here’s the crux: advance rent is a liability, not revenue, until the rental period it covers has elapsed. This is because the landlord has an obligation to provide future occupancy, and recognizing the full amount as income upfront would distort the financial picture.

The Accounting Treatment:

A common approach is to establish a deferred revenue account. When rent is received in advance, the full amount is credited to this account, reflecting the liability. As each rental period passes, a portion of the deferred revenue is recognized as rental income on the income statement. This method ensures revenue is matched with the period the service is actually rendered.

For example, if a tenant pays $12,000 annually in advance on January 1st, $1,000 would be recognized as rental income each month, with the remaining balance in the deferred revenue account decreasing accordingly.

Practical Considerations:

- Lease Term: The length of the lease dictates the recognition period. A one-year lease would spread the advance rent over 12 months, while a multi-year lease would require a longer recognition period.

- Accounting Software: Most accounting software allows for automated recognition of deferred revenue, simplifying the process and reducing the risk of errors.

- Disclosure: Financial statements should clearly disclose the amount of rent received in advance and the accounting policy used for its recognition.

Cautions:

- Misclassification: Avoid the temptation to record advance rent as immediate income. This inflates revenue and misrepresents the financial health of the business.

- Consistency: Apply the chosen accounting treatment consistently across all advance rent transactions to ensure comparability of financial statements.

Proper accounting treatment for advance rent is crucial for accurate financial reporting. By recognizing revenue over the rental period and maintaining a deferred revenue account, businesses ensure their financial statements reflect the true economic reality of their operations. This transparency is essential for informed decision-making by investors, creditors, and other stakeholders.

Rent-to-Own Homes: Smart Investment or Costly Mistake?

You may want to see also

Explore related products

![]()

Impact on Cash Flow Statements

Rent received in advance represents a unique accounting challenge, particularly when examining its impact on cash flow statements. This scenario occurs when a tenant pays rent before the rental period begins, creating a timing difference between cash receipt and revenue recognition. Understanding this distinction is crucial for accurately reflecting a company’s liquidity and financial health.

From a cash flow perspective, rent received in advance is classified as an operating activity. When a landlord receives advance rent, it increases cash inflows in the period of receipt. However, this cash is not immediately recognized as revenue. Instead, it is recorded as a liability (often termed "deferred revenue" or "unearned revenue") on the balance sheet. This liability reflects the obligation to provide future rental services. As the rental period progresses, the liability is gradually recognized as revenue on the income statement, typically on a straight-line basis over the lease term.

The timing mismatch between cash receipt and revenue recognition can distort the cash flow statement if not properly adjusted. For instance, a large advance payment might inflate operating cash flows in the period received, while future periods could appear artificially low. To address this, accountants often use a supplemental schedule or disclose the non-cash nature of the transaction in the notes to the financial statements. This ensures stakeholders can accurately assess the company’s cash generation capabilities without being misled by the timing of rent payments.

Consider a practical example: a landlord receives $12,000 in January for a year-long lease. While the cash flow statement shows a $12,000 inflow in January, only $1,000 is recognized as revenue each month. Without proper adjustments, this could misrepresent the company’s monthly cash flow stability. By reconciling the timing difference, investors and analysts can better evaluate the sustainability of cash flows and the underlying operational performance.

In conclusion, rent received in advance significantly impacts cash flow statements by creating a temporal gap between cash inflows and revenue recognition. Proper accounting treatment, including accurate classification and disclosure, is essential to maintain transparency and reliability in financial reporting. Companies must ensure their cash flow statements reflect not just the cash movements but also the economic substance of these transactions, enabling stakeholders to make informed decisions.

Is 4060 Alto St in Oceanside, CA 92056 Available for Rent?

You may want to see also

Explore related products

![]()

Tax Implications of Advance Rent

Advance rent payments, while providing landlords with immediate cash flow, introduce complexities in tax reporting and liability. The IRS mandates that rent be recognized as income in the year it is received, regardless of the period it covers. For instance, if a tenant pays $12,000 in December 2023 for rent spanning January to December 2024, the landlord must report the full $12,000 as income in 2023. This accrual-based approach contrasts with the cash basis method, where income is reported when earned, not received. Landlords must carefully align their accounting practices with IRS rules to avoid penalties.

From a tax planning perspective, receiving advance rent can artificially inflate income in the year of receipt, potentially pushing the landlord into a higher tax bracket. For example, a landlord earning $80,000 annually who receives $12,000 in advance rent might face a 24% tax rate instead of 22%. To mitigate this, landlords can explore strategies like deferring deductible expenses to the year of advance rent receipt or consulting a tax professional to restructure rental agreements. Small business landlords, in particular, should consider these implications, as they may also affect self-employment tax calculations.

Tenants, too, must be aware of the tax treatment of advance rent payments. While tenants cannot deduct rent payments in advance as a current-year expense, they may need to account for prepaid rent on their balance sheets if they operate a business. For instance, a small business tenant paying $6,000 in advance rent for six months would record this as a prepaid asset, expensing $1,000 monthly. This ensures compliance with accounting standards and provides a clear financial picture for tax purposes.

A comparative analysis reveals that tax treatment varies internationally. In the UK, for example, landlords can choose between the cash basis and accrual basis for reporting rental income, offering more flexibility. In contrast, the U.S. system is rigid, requiring income recognition upon receipt. Canadian landlords, meanwhile, may defer tax on advance rent if they use the accrual method and can demonstrate the payment is for a future period. Understanding these differences is crucial for landlords operating across borders or benchmarking against global practices.

In conclusion, the tax implications of advance rent demand proactive management. Landlords should maintain meticulous records, consult tax professionals, and consider restructuring agreements to align with financial goals. Tenants, especially business owners, must ensure proper accounting treatment to avoid discrepancies. By navigating these complexities, both parties can optimize their tax positions while remaining compliant with IRS regulations.

Wheelchair Rentals at Legoland Florida: Accessibility Options for Visitors

You may want to see also

Explore related products

![]()

Differences Between Rent Received and Accrued Rent

Rent received in advance and accrued rent are two distinct accounting concepts that reflect different aspects of rental income. Understanding their differences is crucial for accurate financial reporting and cash flow management. Rent received in advance refers to payments made by tenants for future rental periods, recorded as a liability on the landlord’s balance sheet until the rental period is fulfilled. Accrued rent, on the other hand, represents income earned but not yet received, recorded as an asset on the landlord’s balance sheet. These differences impact how rental income is recognized and reported, influencing both short-term cash flow and long-term financial health.

Consider a scenario where a tenant pays $12,000 upfront for a year’s rent. This $12,000 is rent received in advance. The landlord cannot recognize the entire amount as income immediately. Instead, it is recorded as a liability, with $1,000 recognized as income each month as the rental period progresses. Conversely, if a tenant fails to pay rent on time, the landlord records the unpaid amount as accrued rent, an asset reflecting the income earned but not yet collected. This distinction ensures that financial statements accurately represent the timing of income recognition, aligning with accounting principles like accrual accounting.

From a practical standpoint, managing rent received in advance requires meticulous tracking to avoid overstating income. For instance, if a tenant pays six months’ rent upfront, the landlord must allocate $1,000 monthly to income and reduce the liability by the same amount. Accrued rent, however, demands proactive follow-up on overdue payments to ensure cash flow stability. Landlords should establish clear policies for handling both scenarios, such as setting aside a portion of advance payments in a separate account or implementing late payment penalties for accrued rent.

The implications of these differences extend beyond bookkeeping. Rent received in advance provides landlords with immediate liquidity, which can be reinvested or used to cover expenses. However, it also creates a future obligation to deliver the rental service. Accrued rent, while reflecting earned income, poses a risk of non-payment, requiring careful monitoring and collection strategies. For tenants, understanding these concepts ensures transparency in lease agreements and helps avoid disputes over payment timing or income recognition.

In summary, while rent received in advance and accrued rent both relate to rental income, they serve opposite purposes in accounting. One represents a liability, the other an asset; one reflects payments for future periods, the other income for past periods. By distinguishing between the two, landlords and tenants can maintain accurate financial records, optimize cash flow, and ensure compliance with accounting standards. This clarity is essential for sustainable property management and financial planning.

Renting the 7th Edition: Is It Worth It?

You may want to see also

Frequently asked questions

Rent received in advance refers to payment received by a landlord or property owner for a rental period that has not yet begun. It is recorded as a liability (unearned revenue) on the balance sheet until the rental period is completed and the income is earned.

Rent received in advance is initially recorded as a liability under "Unearned Revenue" or "Deferred Income." As the rental period progresses, the amount is gradually recognized as rental income on the income statement, reducing the liability.

Rent received in advance is considered a liability because the landlord has an obligation to provide rental services in the future. Until the services are rendered, the payment is not considered earned income and is treated as a debt owed to the tenant.