The natural account balance of rent expense is a fundamental concept in accounting that refers to the inherent classification of this account as either a debit or credit. Rent expense, being an operating expense, is typically recorded as a debit in the accounting system. This is because expenses, by their nature, reduce a company's equity and are therefore debited to reflect an outflow of economic resources. As a result, the natural account balance of rent expense is a debit balance, indicating that increases in rent expense are recorded on the debit side, while decreases or payments are recorded on the credit side. Understanding the natural account balance of rent expense is crucial for accurate financial reporting, as it ensures that transactions are properly classified and recorded, providing a clear picture of a company's financial health and performance.

Explore related products

What You'll Learn

![]()

Normal Balance of Rent Expense

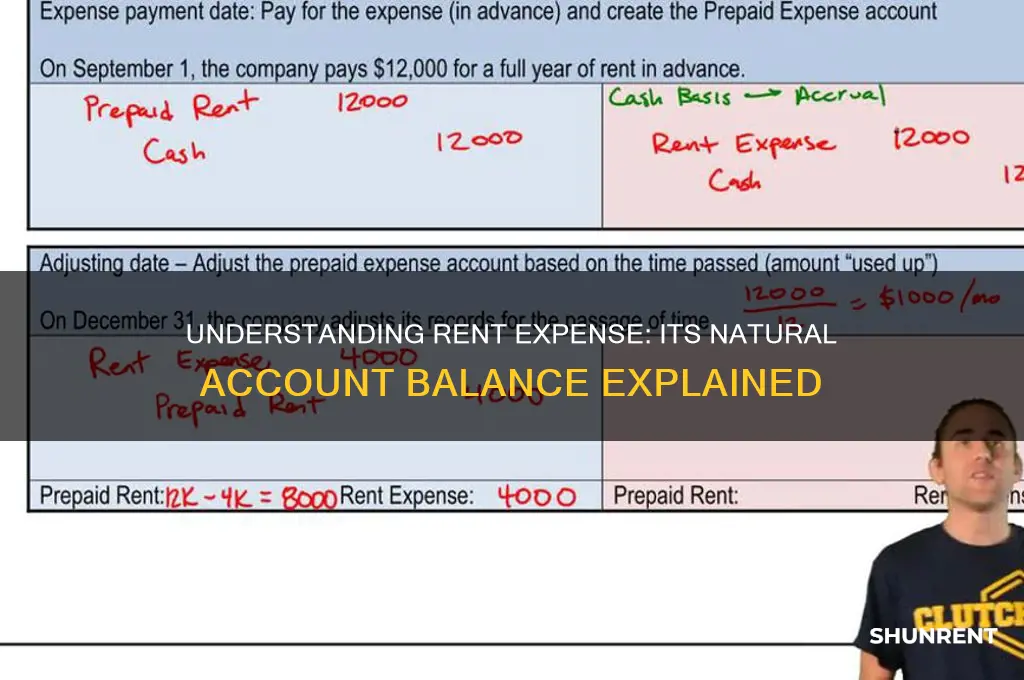

Rent expense, by its very nature, is a cost incurred by businesses and individuals for the use of property, typically on a monthly basis. Understanding its normal balance is crucial for accurate financial reporting and analysis. In accounting, the normal balance of an account refers to the side (debit or credit) where increases are recorded. For rent expense, the normal balance is a debit. This is because rent expense is an operating expense, and expenses are always debited to reflect an outflow of economic resources. When a business pays rent, it reduces its assets (cash) and recognizes the expense, hence the debit entry.

To illustrate, consider a small retail store that pays $2,000 in rent each month. When the rent is paid, the journal entry would debit Rent Expense for $2,000 and credit Cash for $2,000. This entry aligns with the accounting equation (Assets = Liabilities + Equity) and ensures that the financial statements accurately reflect the business’s financial position. The debit to Rent Expense increases the account balance, while the credit to Cash decreases it, maintaining the balance sheet’s equilibrium.

One common misconception is that rent expense could have a credit balance. However, this would only occur in unusual circumstances, such as an error in recording or a refund of prepaid rent. For instance, if a business prepaid $6,000 for six months of rent, the initial entry would debit Prepaid Rent (an asset) and credit Cash. Each month, $1,000 would be debited to Rent Expense and credited to Prepaid Rent, gradually reducing the prepaid balance. A credit to Rent Expense would only appear if the business received a refund, which is rare and not the norm.

Practical tip: Always review the lease agreement to determine the rent payment schedule and any prepaid amounts. This ensures accurate recording and avoids errors in the normal balance of rent expense. For example, if a lease includes a security deposit, it should be recorded separately from rent expense, as it is not an expense but a refundable asset.

In conclusion, the normal balance of rent expense is a debit, reflecting its nature as an operating expense. Properly recording rent expense ensures compliance with accounting principles and provides a clear picture of a business’s financial health. By understanding this concept, businesses can maintain accurate financial records and make informed decisions based on reliable data.

Renting a U-Haul: What's the Deal With G?

You may want to see also

Explore related products

![]()

Debit or Credit Nature

Rent expense, by its very nature, is a cost incurred for the use of property or assets, typically over a period of time. In accounting, understanding whether an account has a debit or credit nature is crucial for accurate financial reporting. The natural account balance of rent expense is a debit balance. This is because rent expense is an expense account, and in the double-entry accounting system, expenses are always recorded on the debit side of the ledger. When rent is paid, the rent expense account is debited, and the corresponding credit is typically made to cash or accounts payable, depending on the payment method.

To illustrate, consider a business that pays $2,000 in monthly rent. The journal entry would debit Rent Expense for $2,000 and credit Cash for $2,000 if paid immediately, or credit Accounts Payable if the payment is deferred. This transaction reflects the outflow of economic resources (rent) and ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced. The debit to Rent Expense increases the account balance, aligning with its natural debit nature.

A common misconception arises when comparing rent expense to prepaid rent, which is an asset account. While rent expense is debited when rent is incurred, prepaid rent is also debited when rent is paid in advance. The key difference lies in the timing of recognition: rent expense reflects the current period’s usage, whereas prepaid rent represents a future benefit. For example, if a business prepays $6,000 for six months of rent, Prepaid Rent (an asset) is debited, and Cash is credited. Each month, $1,000 is then debited to Rent Expense and credited to Prepaid Rent, gradually reducing the prepaid balance.

Understanding the debit nature of rent expense is essential for financial analysis. It directly impacts the income statement, reducing net income, and indirectly affects the balance sheet through changes in cash or payables. For instance, a company with high rent expenses may show lower profitability, prompting stakeholders to assess cost-cutting measures or renegotiate lease terms. Conversely, consistent rent expense recognition ensures compliance with accrual accounting principles, providing a more accurate financial picture.

In practice, accountants should ensure that rent expense is recorded in the correct period to avoid misstatements. For example, if rent is paid quarterly but recognized monthly, adjusting entries are necessary to allocate the expense evenly. This adherence to the matching principle—matching expenses with the revenues they help generate—is critical for financial integrity. By consistently debiting rent expense, businesses maintain transparency and reliability in their financial reporting, reinforcing the account’s natural debit nature.

Renting Your Airbnb on a Corporate Lease: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Impact on Financial Statements

Rent expense, naturally a debit balance account, directly influences a company’s financial statements by reducing profitability and affecting liquidity. On the income statement, it appears as an operating expense, lowering net income. For instance, a retail business paying $10,000 monthly rent sees this amount deducted from revenue, shrinking the bottom line. This reduction is critical for investors and stakeholders assessing operational efficiency. Simultaneously, on the balance sheet, rent expense impacts cash reserves. Prepaid rent, if any, is recorded as a current asset, but as rent is paid, cash decreases, reflecting in the asset section. This dual impact underscores the importance of managing rent costs to maintain financial health.

Analyzing the cash flow statement reveals rent expense’s role in operating activities. Under the indirect method, it’s adjusted back to net income as a non-cash item, but the actual cash outflow is captured in the change in cash balance. For example, a tech startup with $50,000 quarterly rent payments would show this outflow in the operating section, highlighting liquidity pressure. This visibility is crucial for creditors evaluating repayment capacity. Moreover, consistent rent payments improve a company’s creditworthiness, indirectly benefiting future financing activities. However, excessive rent relative to revenue can signal inefficiency, prompting scrutiny from analysts.

From a comparative perspective, rent expense’s impact varies by industry. A manufacturing firm with high rent for warehouse space may see a larger expense relative to a service-based company operating remotely. This disparity affects industry benchmarks and profitability ratios like operating margin. For instance, a 20% rent-to-revenue ratio in retail is manageable, but 30% in hospitality could be unsustainable. Such variations necessitate industry-specific analysis when interpreting financial statements. Additionally, lease accounting standards (e.g., ASC 842 or IFRS 16) require capitalizing leases, shifting rent expense to depreciation and interest, further complicating its impact on financial metrics.

A persuasive argument for proactive rent management lies in its long-term financial implications. High rent expenses not only reduce current profitability but also limit reinvestment in growth. For example, a small business allocating 40% of revenue to rent has less capital for marketing or R&D. Over time, this constraint stifles scalability. Conversely, negotiating lower rent or relocating to cost-effective areas can free up resources, improving financial flexibility. Companies like Starbucks strategically optimize store locations to balance rent costs and foot traffic, showcasing the strategic importance of rent in financial planning.

In practical terms, businesses can mitigate rent expense’s impact through strategic planning. First, negotiate lease terms with landlords, such as rent escalation caps or tenant improvement allowances. Second, consider subleasing unused space to offset costs. Third, adopt hybrid work models to reduce office space needs, a trend accelerated post-pandemic. For instance, a software company cutting office space by 30% saved $200,000 annually, redirecting funds to cloud infrastructure. Such actions not only improve cash flow but also enhance financial statement metrics, making the business more attractive to investors.

Mastering Your Budget: Understanding the Income to Rent Ratio

You may want to see also

Explore related products

![]()

Temporary vs. Permanent Account

Rent expense, a fundamental component of business operations, naturally carries a debit balance. This is because it represents an outflow of resources—cash paid for the use of property—and thus decreases equity. Understanding this natural balance is crucial, but equally important is distinguishing between temporary and permanent accounts, as they dictate how rent expense is treated in financial reporting.

Temporary accounts, also known as nominal accounts, are reset to zero at the end of each accounting period. These accounts track revenues, expenses, gains, and losses. Rent expense falls squarely into this category. For instance, if a company pays $12,000 in rent annually, this amount is expensed over the year, but the rent expense account is closed out at year-end, transferring its balance to retained earnings. This ensures that each new period starts afresh, reflecting current financial activity rather than cumulative historical data.

In contrast, permanent accounts, or real accounts, carry forward their balances from one period to the next. These include assets, liabilities, and equity accounts. While rent expense itself is temporary, the cash account—which decreases when rent is paid—is permanent. For example, if a company pays $1,000 in monthly rent, the cash account balance is reduced by this amount, but the decrease is not erased at year-end. Instead, it continues to reflect the company’s current financial position.

The distinction between temporary and permanent accounts is critical for accurate financial reporting. Misclassifying rent expense as a permanent account would distort the income statement and balance sheet. For instance, if rent expense were not closed out, it would inflate expenses in subsequent periods, misleading stakeholders about the company’s profitability. Conversely, treating a permanent account like cash as temporary would understate the company’s liquidity.

To avoid such errors, follow these steps: 1) Identify whether the account tracks a periodic activity (temporary) or a cumulative balance (permanent). 2) Ensure temporary accounts like rent expense are closed to retained earnings at period-end. 3) Verify that permanent accounts maintain their balances across periods. By adhering to these principles, businesses can maintain transparency and accuracy in their financial statements, ensuring rent expense and other accounts are reported correctly.

The Symbolic Significance of Renting Samuel's Garment in Biblical Context

You may want to see also

Explore related products

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/811AGIXv7PL._AC_UY218_.jpg)

![]()

Journal Entry for Rent Expense

Rent expense is inherently a debit balance account, reflecting the outflow of resources to cover the cost of leased property or space. This natural debit balance aligns with the fundamental accounting principle that expenses reduce equity, thus requiring a debit entry to accurately represent the financial impact. Understanding this characteristic is crucial for proper journal entries, ensuring that the expense is correctly recorded and the financial statements remain balanced.

To record rent expense, a journal entry is made at the time the obligation is incurred, typically at the beginning of the rental period. The entry debits Rent Expense, an income statement account, and credits Cash or Accounts Payable, depending on whether the rent is paid immediately or deferred. For example, if a company pays $2,000 in monthly rent upfront, the entry would be:

Debit: Rent Expense ($2,000)

Credit: Cash ($2,000).

This entry recognizes the expense in the period it is incurred, adhering to the matching principle, which pairs expenses with the revenues they help generate.

In cases where rent is prepaid, the journal entry involves an additional step to reflect the asset created by the advance payment. For instance, if a company prepays $6,000 for six months of rent, the initial entry would be:

Debit: Prepaid Rent ($6,000)

Credit: Cash ($6,000).

Subsequently, each month, an adjusting entry is made to recognize the expense:

Debit: Rent Expense ($1,000)

Credit: Prepaid Rent ($1,000).

This approach ensures that the expense is systematically allocated over the rental period, maintaining accuracy in financial reporting.

A common pitfall in recording rent expense is confusing it with other asset or liability accounts. For instance, rent should not be recorded as a Debit: Rent Payable or Credit: Rent Revenue, as these entries would misclassify the transaction. Rent Payable is a liability account used when rent is owed but not yet paid, while Rent Revenue applies to landlords receiving rent, not tenants paying it. Clear distinctions between these accounts are essential to avoid errors in financial statements.

In conclusion, the journal entry for rent expense is straightforward but requires attention to timing and classification. By debiting Rent Expense and crediting Cash or Accounts Payable, businesses accurately reflect the outflow of resources. For prepaid rent, the use of Prepaid Rent as an asset account ensures proper allocation over time. Mastery of these entries not only maintains compliance with accounting standards but also provides a clear financial picture of a company’s obligations and resource utilization.

Average Rent in Santa Fe: What to Expect in 2023

You may want to see also

Frequently asked questions

The natural account balance of rent expense is a debit balance, as it represents an expense that reduces a company’s net income.

Rent expense is considered a debit account because it follows the accounting equation where expenses increase with a debit, reflecting the outflow of resources.

Rent expense decreases net income on the income statement and reduces retained earnings on the balance sheet, as it is debited in the accounting records.

Rent expense should not have a credit balance under normal circumstances. A credit balance would indicate an error, as expenses are naturally debited.