The rent-to-income ratio is a critical financial metric used to assess the affordability of housing for individuals or households. It is calculated by dividing the monthly rent payment by the monthly gross income, expressed as a percentage. This ratio helps both renters and landlords determine whether the rent is sustainable relative to earnings, with a commonly recommended threshold being around 30% or less. Exceeding this threshold may indicate financial strain, as a larger portion of income is allocated to housing, leaving less for other essential expenses. Understanding this ratio is essential for budgeting, financial planning, and ensuring long-term housing stability.

| Characteristics | Values |

|---|---|

| Definition | The percentage of a tenant's monthly income that goes toward rent. |

| Ideal Ratio | 30% or less (as recommended by HUD and financial advisors). |

| Calculation Formula | (Monthly Rent / Monthly Gross Income) × 100. |

| Purpose | Helps determine affordability and financial stability for renters. |

| Industry Standard | Landlords often require a ratio of 30% or lower for rental approval. |

| Impact on Approval | Higher ratios may lead to rental application rejections or additional requirements (e.g., co-signers). |

| Regional Variations | Ratios vary by city; e.g., in high-cost cities like San Francisco or New York, ratios may exceed 40%. |

| Average U.S. Ratio (2023) | Approximately 28-30% nationally, but varies widely by location. |

| Affordability Crisis Indicator | Ratios above 30% often signal housing affordability challenges. |

| Government Assistance Threshold | Households spending >30% on rent are considered "rent-burdened" by HUD. |

| Global Comparison | U.S. average is higher than some European countries (e.g., Germany: ~24%). |

| Trends (2020-2023) | Increasing in urban areas due to rising rents and stagnant wages. |

| Minimum Income Requirement | Landlords often require tenants to earn 3x the monthly rent (e.g., $3,000 income for $1,000 rent). |

| Alternative Metrics | Some landlords use gross annual income (e.g., 40x monthly rent). |

| Impact on Credit Score | High rent-to-income ratios may indirectly affect credit if it leads to missed payments. |

| Policy Implications | Used in housing policy discussions to address affordability and homelessness. |

Explore related products

What You'll Learn

![]()

Understanding Rent Burden

A rent-to-income ratio exceeding 30% signals rent burden, a threshold established by the U.S. Department of Housing and Urban Development (HUD). This metric, calculated by dividing monthly rent by gross monthly income, serves as a critical indicator of housing affordability. For instance, a tenant earning $4,000 monthly spending $1,300 on rent is precisely at the 30% mark, while someone earning $3,000 and paying $1,200 is already at 40%, indicating financial strain. Understanding this ratio helps individuals and policymakers gauge the sustainability of housing costs relative to income.

Analyzing rent burden reveals its cascading effects on financial stability. When rent consumes more than 30% of income, households often sacrifice other essentials like healthcare, groceries, or savings. For example, a family earning $50,000 annually with a $1,500 monthly rent (36% of income) may struggle to build an emergency fund or invest in education. Over time, this imbalance can lead to debt accumulation or eviction risks, particularly in high-cost urban areas like San Francisco or New York, where median rents often surpass $3,000.

To mitigate rent burden, practical strategies include negotiating rent reductions, seeking roommate arrangements, or relocating to more affordable neighborhoods. For instance, moving from a downtown apartment to a suburban area can reduce rent by 20–30%. Additionally, leveraging government assistance programs like Section 8 vouchers or Low-Income Housing Tax Credit properties can provide relief. A proactive approach involves budgeting tools to track expenses and identifying areas to cut costs, such as reducing dining out or subscription services.

Comparatively, rent burden disproportionately affects low-income households and renters in competitive markets. In cities like Los Angeles, where the average rent is $2,500, a household earning $40,000 annually would spend 75% of their income on housing—an unsustainable scenario. In contrast, rural areas with lower housing costs may see ratios below 20%, allowing for greater financial flexibility. This disparity underscores the need for localized solutions, such as rent control policies or incentivizing affordable housing development in high-demand regions.

Ultimately, understanding rent burden empowers individuals to make informed housing decisions and advocates for systemic changes. By monitoring the rent-to-income ratio and adopting strategies to stay below the 30% threshold, renters can avoid financial instability. Policymakers, meanwhile, can address the root causes by increasing housing supply, regulating rent increases, and expanding access to subsidies. Together, these efforts can alleviate the strain of rent burden and promote equitable housing opportunities.

Is Pressure Washing a Renter's Duty or Landlord's Responsibility?

You may want to see also

Explore related products

![]()

Calculating the Ratio

The rent-to-income ratio is a critical metric for both tenants and landlords, serving as a benchmark to ensure housing affordability. Calculating this ratio involves dividing the monthly rent by the monthly gross income, then multiplying by 100 to express it as a percentage. For instance, if a tenant earns $5,000 monthly and pays $1,500 in rent, the ratio is 30%—a figure often cited as the maximum threshold for financial stability. This calculation provides a snapshot of how much of one’s income is allocated to housing, helping to assess whether the rent is sustainable.

While the formula itself is straightforward, accuracy hinges on using the correct income figure. Gross income—total earnings before taxes and deductions—is the standard measure. For salaried individuals, this is typically their monthly paycheck before withholdings. Freelancers or those with variable income should average their earnings over the past 6–12 months to account for fluctuations. Misreporting income, even unintentionally, can skew the ratio and lead to overcommitment. For example, a freelancer earning $6,000 one month and $3,000 the next should use an average of $4,500 for a realistic assessment.

A common pitfall in calculating the rent-to-income ratio is overlooking additional housing costs. While the ratio traditionally focuses on rent alone, utilities, maintenance fees, or homeowners’ association dues can significantly impact affordability. For instance, a tenant with a 28% rent-to-income ratio might actually be spending 35% of their income on housing when utilities are factored in. To avoid this, consider a modified ratio that includes all housing-related expenses, providing a more comprehensive view of financial burden.

Persuasively, the rent-to-income ratio isn’t just a number—it’s a tool for financial planning. Landlords use it to screen tenants, ensuring they can afford rent without defaulting. Tenants, meanwhile, can use it to negotiate rent or decide between properties. For example, a tenant with a 40% ratio might be at risk of financial strain, while one at 25% has more flexibility for savings or other expenses. By regularly recalculating this ratio, individuals can adapt to income changes or rising rents, maintaining a balanced budget.

Comparatively, the ideal rent-to-income ratio varies by region and circumstance. In high-cost cities like New York or San Francisco, ratios of 40–50% are not uncommon, though they often necessitate roommates or subsidized housing. In contrast, rural areas may see ratios as low as 20–25%. Age and life stage also play a role: young professionals might accept higher ratios for prime locations, while families prioritize lower ratios for stability. Understanding these nuances ensures the ratio is applied contextually, not universally.

Leasing vs. Renting Equipment: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Ideal Ratio Standards

The rent-to-income ratio is a critical metric for both tenants and landlords, serving as a financial benchmark to ensure housing affordability and stability. Ideal ratio standards typically suggest that a tenant’s monthly rent should not exceed 30% of their gross monthly income. This threshold is widely accepted by financial advisors, housing authorities, and lenders as a sustainable balance between housing costs and other living expenses. For example, if an individual earns $4,000 per month, their rent should ideally stay below $1,200 to maintain financial health. Exceeding this ratio can strain budgets, limit savings, and increase the risk of eviction or debt.

However, the 30% rule is not one-size-fits-all. Regional variations in housing markets and cost of living often necessitate adjustments. In high-cost cities like New York or San Francisco, where rents can consume 40-50% of income, tenants may need to prioritize shared housing or smaller spaces to stay within budget. Conversely, in more affordable areas, a lower ratio, such as 25%, might be achievable and advisable. Additionally, income volatility, such as that experienced by gig workers or freelancers, requires a more conservative approach, with ratios closer to 20-25% to account for unpredictable earnings.

For landlords, adhering to ideal rent-to-income ratios is not just ethical but practical. Screening tenants based on this metric reduces the likelihood of payment defaults and turnover. A common practice is to require tenants to earn at least three times the monthly rent. For instance, a $1,500 rental would ideally suit someone earning $4,500 or more. Landlords can also offer flexibility, such as accepting co-signers or allowing roommates, to accommodate tenants who fall slightly outside the ideal ratio but demonstrate financial responsibility.

Achieving the ideal rent-to-income ratio often requires proactive financial planning. Tenants should assess their income stability, savings, and debt obligations before committing to a lease. Tools like budgeting apps or rent calculators can help determine affordability. For those struggling to meet the 30% threshold, negotiating rent, seeking government housing assistance, or relocating to a more affordable area are viable strategies. Conversely, tenants with lower ratios can allocate savings to emergency funds, investments, or higher-quality housing options.

In conclusion, while the 30% rent-to-income ratio remains a gold standard, its application must be tailored to individual and regional circumstances. Tenants and landlords alike benefit from understanding and adapting to these standards, fostering financial security and sustainable housing arrangements. By prioritizing this metric, both parties can navigate the complexities of the rental market with greater confidence and clarity.

Unlocking Tax Savings: Rental Property Deductions You Need to Know

You may want to see also

Explore related products

![]()

Impact on Affordability

The rent-to-income ratio, typically recommended at 30% or below, directly shapes housing affordability. Exceeding this threshold forces households to allocate a larger share of their income to rent, leaving less for essentials like food, healthcare, and savings. For instance, a household earning $4,000 monthly should ideally spend no more than $1,200 on rent. However, in high-cost cities like San Francisco or New York, where median rents often surpass $3,000, this ratio frequently climbs to 50% or higher, creating financial strain.

Analyzing the impact reveals a cascading effect on economic stability. When rent consumes a disproportionate amount of income, households are more vulnerable to unexpected expenses, such as medical emergencies or job loss. This vulnerability increases reliance on credit cards or payday loans, leading to debt accumulation and long-term financial instability. For example, a Pew Charitable Trusts study found that renters spending over 50% of their income on housing are twice as likely to experience eviction compared to those within the 30% guideline.

To mitigate this, policymakers and individuals can adopt targeted strategies. Cities can implement rent control measures or incentivize affordable housing development to reduce market pressures. On a personal level, renters should prioritize budgeting tools like the 50/30/20 rule (50% on needs, 30% on wants, 20% on savings) to ensure rent fits within a sustainable framework. Additionally, exploring roommate arrangements or relocating to lower-cost neighborhoods can help align rent expenses with income levels.

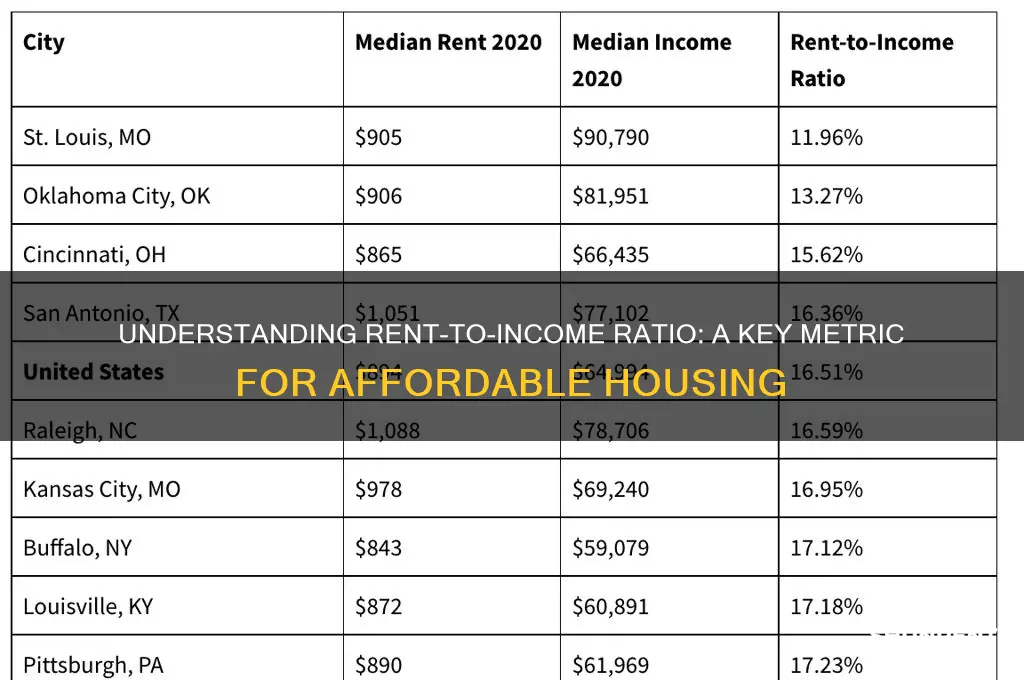

Comparatively, regions with lower rent-to-income ratios, such as the Midwest or Southeast U.S., demonstrate greater financial resilience among residents. In Indianapolis, where the median rent is $1,100 and the median household income is $50,000, the ratio hovers around 26%, allowing residents to allocate more funds toward savings, education, or investments. This contrast highlights the importance of geographic considerations in achieving housing affordability.

Ultimately, the rent-to-income ratio serves as a critical metric for assessing financial health and affordability. By understanding its implications and taking proactive steps, both individuals and communities can navigate housing challenges more effectively. Whether through policy interventions, personal budgeting, or strategic relocation, maintaining a balanced ratio is essential for long-term economic stability.

Renting an Airbnb for Your Dream Wedding: A Step-by-Step Guide

You may want to see also

Explore related products

$15 $32

![]()

Landlord Requirements Explained

Landlords often require tenants to meet a specific rent-to-income ratio, typically 30% or less, to ensure financial stability and timely rent payments. This means if your monthly rent is $1,200, your gross monthly income should be at least $4,000. This threshold isn’t arbitrary; it’s rooted in affordability guidelines established by housing authorities and financial advisors. Exceeding this ratio increases the risk of tenants falling behind on payments, which can lead to eviction or financial strain for both parties.

To calculate this ratio, divide your monthly rent by your gross monthly income and multiply by 100. For example, if your rent is $1,500 and your income is $5,000, the ratio is 30% ($1,500 ÷ $5,000 = 0.30). Landlords may also consider additional factors, such as credit scores and employment history, but the rent-to-income ratio is often the first filter. If you’re self-employed or have irregular income, provide bank statements or tax returns to demonstrate consistent earnings.

Some landlords may require a lower ratio, such as 25%, especially in competitive markets or for high-end properties. Others might accept a higher ratio if you have a strong credit profile or a co-signer. However, exceeding 30% can be a red flag, signaling potential financial instability. If your ratio is too high, consider finding a roommate, negotiating rent, or choosing a more affordable property.

Tenants should also be aware of exceptions and workarounds. For instance, some landlords may waive strict ratio requirements if you can pay several months’ rent upfront or provide a larger security deposit. Additionally, government-subsidized housing programs often have different criteria, sometimes allowing ratios up to 40% for low-income applicants. Always ask about flexibility and be prepared to provide additional documentation to support your case.

In conclusion, understanding landlord requirements for the rent-to-income ratio is crucial for a smooth rental application process. Aim for a ratio of 30% or less, but be ready to adapt if your situation doesn’t fit the standard mold. By knowing the rules and preparing accordingly, you can increase your chances of securing the rental property you want.

Single Family Rent Schedule: Appraisal Report or Separate Document?

You may want to see also

Frequently asked questions

The rent-to-income ratio is a financial metric used to determine the affordability of rent relative to an individual's or household's income. It is calculated by dividing the monthly rent by the monthly gross income.

The rent-to-income ratio is calculated by dividing the monthly rent payment by the monthly gross income. For example, if the monthly rent is $1,200 and the monthly gross income is $4,000, the rent-to-income ratio would be 1,200 / 4,000 = 0.3 or 30%.

A commonly accepted guideline is that a rent-to-income ratio of 30% or less is considered affordable. This means that an individual or household should spend no more than 30% of their gross income on rent and utilities.

The rent-to-income ratio is important because it helps individuals and households determine if they can afford a particular rental property. It also helps landlords and property managers assess the financial stability of potential tenants and reduce the risk of rental defaults.

Yes, the rent-to-income ratio can vary depending on location, cost of living, and individual circumstances. In high-cost urban areas, a higher rent-to-income ratio may be necessary, while in more affordable areas, a lower ratio may be achievable. Additionally, factors such as debt, credit score, and employment status can also influence the acceptable rent-to-income ratio.