Determining the appropriate percentage of monthly income that should be allocated towards rent is a crucial aspect of financial planning and budgeting. This decision impacts not only one's immediate financial stability but also long-term savings and investment goals. Various factors influence this calculation, including individual income levels, cost of living, personal financial obligations, and housing market conditions. Financial experts often recommend the 30% rule, where rent should not exceed 30% of one's gross monthly income, to ensure a balanced budget that accommodates other essential expenses and savings. However, this guideline may need adjustment based on specific circumstances, such as high-income earners in expensive urban areas or individuals with significant debt. Understanding the nuances of this financial decision is key to making informed choices about housing affordability and overall economic well-being.

Explore related products

What You'll Learn

- General Rule of Thumb: Rent should be 30% of monthly income for financial stability

- Location Considerations: High-cost areas may require more than 30%, while lower-cost areas might be less

- Debt and Expenses: Consider other monthly obligations like debt payments and utilities when calculating affordable rent

- Savings Goals: Ensure enough income is left for savings and emergencies after paying rent

- Roommate Situations: Sharing a space can reduce individual rent costs, allowing for more flexibility in budget

![]()

General Rule of Thumb: Rent should be 30% of monthly income for financial stability

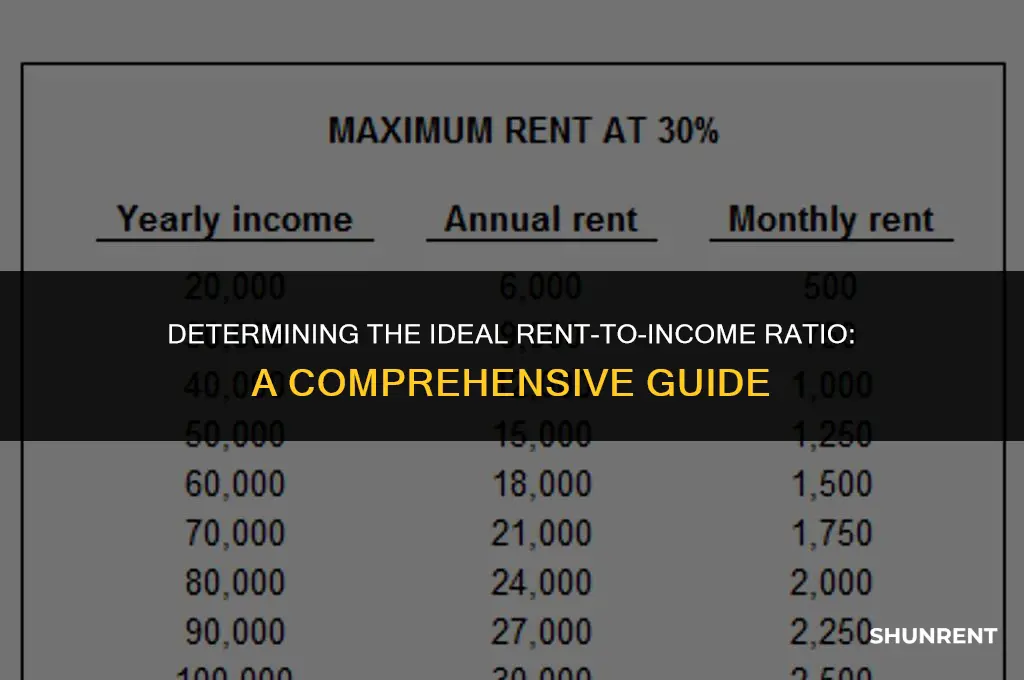

The 30% rule is a widely accepted guideline for determining how much of your monthly income should go towards rent. This rule of thumb suggests that for financial stability, your rent should not exceed 30% of your gross monthly income. This guideline helps ensure that you have enough money left over for other essential expenses, savings, and discretionary spending.

For example, if your monthly income is $5,000, applying the 30% rule would mean your rent should be no more than $1,500. This leaves you with $3,500 for other expenses such as utilities, groceries, transportation, and entertainment. It also allows for some flexibility in case of unexpected costs or changes in your financial situation.

However, it's important to note that the 30% rule is not a one-size-fits-all solution. Depending on your individual circumstances, such as your debt obligations, credit score, and financial goals, you may need to adjust this percentage. For instance, if you have significant student loan payments or credit card debt, you might want to allocate less than 30% of your income to rent to ensure you can meet your debt obligations and still have some savings.

Additionally, the cost of living in your area can greatly impact the feasibility of the 30% rule. In high-cost cities like New York or San Francisco, finding a rental that is only 30% of your income can be challenging. In such cases, you may need to consider alternative housing options, such as roommates or a longer commute, to keep your rent within a manageable range.

Ultimately, while the 30% rule provides a useful starting point, it's crucial to evaluate your unique financial situation and adjust your rent budget accordingly. By doing so, you can ensure that you maintain financial stability and avoid overextending yourself.

Setting Boundaries: How to Politely Decline Renting to a Friend

You may want to see also

Explore related products

![]()

Location Considerations: High-cost areas may require more than 30%, while lower-cost areas might be less

In high-cost urban areas, the 30% rule may not suffice to cover the exorbitant rental prices. For instance, in cities like New York or San Francisco, where the average rent for a one-bedroom apartment can exceed $3,000, allocating 30% of a $5,000 monthly income would still leave a significant shortfall. In such scenarios, renters may need to consider budgeting closer to 40% or even 50% of their income to secure a suitable living space. This highlights the importance of location-specific budgeting when it comes to rent.

Conversely, in lower-cost areas, the 30% guideline might be overly conservative. For example, in smaller towns or rural areas where the average rent is around $800, a 30% allocation from a $2,500 monthly income would result in a surplus. In these cases, renters could potentially allocate less than 30% of their income to rent, allowing for more flexibility in their budget for other expenses or savings.

The disparity in rental costs across different locations underscores the need for a nuanced approach to budgeting for rent. Rather than adhering strictly to a one-size-fits-all rule, individuals should consider the specific rental market conditions in their desired location. This might involve researching average rental prices, calculating the percentage of income required to cover rent in that area, and adjusting their budget accordingly.

For those moving to a new area, it can be helpful to use online rent calculators or consult with local real estate agents to get a better understanding of the rental landscape. Additionally, considering factors such as proximity to work, public transportation, and amenities can help renters make informed decisions about where to live and how much to budget for rent.

Ultimately, the key to successful rent budgeting is to be location-aware and flexible. By taking the time to understand the rental market in their desired area and adjusting their budget accordingly, renters can find a living space that meets their needs without breaking the bank.

Should You Claim Rent Payments on Your Taxes? A Guide

You may want to see also

Explore related products

![]()

Debt and Expenses: Consider other monthly obligations like debt payments and utilities when calculating affordable rent

When calculating affordable rent, it's crucial to consider other monthly obligations like debt payments and utilities. These expenses can significantly impact your ability to pay rent on time and in full. To ensure you're not overextending yourself financially, start by listing all your monthly debts and expenses. This includes credit card payments, student loans, car loans, and any other financial commitments you have.

Next, calculate the total amount of these obligations. This will give you a clear picture of how much money you have left over for rent. It's important to be honest with yourself about your financial situation and not to underestimate your expenses. If you're unsure about any of your obligations, take the time to review your bills and statements to get an accurate number.

Once you have a clear understanding of your monthly debts and expenses, you can start to determine how much rent you can afford. A general rule of thumb is that your rent should be no more than 30% of your gross income. However, this may not be realistic for everyone, especially if you have significant debt or expenses. In that case, you may need to adjust your budget or consider finding a roommate to help split the cost of rent.

It's also important to consider the cost of utilities when calculating affordable rent. These expenses can vary depending on the location and size of the apartment, as well as your personal usage habits. Be sure to ask the landlord about the average cost of utilities before signing a lease, and factor this amount into your budget.

Finally, remember to leave some room for savings and unexpected expenses. It's important to have a financial cushion in case of emergencies or unforeseen costs. By taking the time to carefully consider your monthly obligations and budget accordingly, you can find a rent that is both affordable and sustainable for your lifestyle.

How to Create a Rent Receipt: A Step-by-Step Guide

You may want to see also

Explore related products

$29.99

![]()

Savings Goals: Ensure enough income is left for savings and emergencies after paying rent

To ensure that enough income is left for savings and emergencies after paying rent, it's crucial to adopt a strategic approach to budgeting. One effective method is the 50/30/20 rule, where 50% of your income is allocated to necessities like rent and utilities, 30% to discretionary spending such as entertainment and dining out, and 20% to savings and debt repayment. By adhering to this guideline, you can create a balanced budget that prioritizes both immediate needs and long-term financial security.

Another key strategy is to automate your savings. Setting up automatic transfers from your checking account to a savings account can help you build an emergency fund without having to rely on willpower alone. Ideally, aim to save at least three to six months' worth of living expenses in an easily accessible, high-yield savings account. This cushion will provide financial peace of mind and protect you from unexpected expenses or income disruptions.

It's also important to regularly review and adjust your budget as needed. Life circumstances and financial goals can change over time, so it's essential to ensure that your budget remains aligned with your current priorities. Consider scheduling quarterly budget check-ins to assess your progress, identify areas for improvement, and make any necessary adjustments to your spending and saving habits.

In addition to these strategies, it's wise to explore ways to increase your income. This could involve pursuing a side hustle, asking for a raise at your current job, or developing new skills that could lead to higher-paying opportunities. By boosting your income, you'll have more flexibility to allocate funds towards savings and emergencies while still covering your rent and other essential expenses.

Finally, be mindful of common budgeting pitfalls, such as overspending on non-essential items or failing to account for irregular expenses. By staying vigilant and proactive in your financial management, you can create a stable financial foundation that supports both your immediate needs and your long-term savings goals.

Rent Charging: When Does it Apply?

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![]()

Roommate Situations: Sharing a space can reduce individual rent costs, allowing for more flexibility in budget

Sharing a living space with roommates can significantly reduce individual rent costs, providing more flexibility in one's budget. This arrangement allows individuals to allocate a smaller portion of their monthly income towards rent, potentially freeing up funds for other essential expenses or personal interests. For example, if a one-bedroom apartment costs $1,500 per month, sharing it with two roommates could reduce each person's rent to $500, assuming equal division of costs.

However, it's crucial to consider the potential downsides of sharing a space. Roommates may have different lifestyles, habits, and expectations regarding cleanliness, noise levels, and shared responsibilities. These differences can lead to conflicts and stress, which may outweigh the financial benefits. Additionally, sharing a space can limit privacy and personal freedom, as individuals must often compromise on decisions related to the shared living area.

To mitigate these challenges, it's essential to establish clear boundaries and expectations from the outset. This can be achieved through open communication and, if necessary, creating a roommate agreement that outlines responsibilities, rules, and consequences for not adhering to them. Furthermore, individuals should carefully consider potential roommates' backgrounds, personalities, and lifestyles to ensure compatibility.

In conclusion, while sharing a space with roommates can offer significant financial advantages, it's important to weigh these benefits against the potential drawbacks. By setting clear expectations, communicating openly, and choosing compatible roommates, individuals can maximize the benefits of shared living while minimizing the risks.

Where to Watch Rent Filmed Live on Broadway: Your Guide

You may want to see also

Frequently asked questions

A common guideline is that rent should be no more than 30% of your gross monthly income. This allows for other expenses such as utilities, food, transportation, and savings.

To calculate how much rent you can afford, multiply your gross monthly income by 0.30. For example, if your monthly income is $4,000, you can afford $1,200 in rent.

If your income varies, consider using an average of your monthly income over the past year to calculate your affordable rent. Alternatively, you can use the lowest monthly income you expect to receive as a conservative estimate.

Yes, in addition to your income, consider your other monthly expenses, debt obligations, and savings goals. You may need to adjust your rent budget accordingly to ensure you're not overextending yourself financially.