When determining what portion of your income should be allocated towards rent, it's essential to consider several factors to ensure financial stability and avoid overburdening yourself. A general rule of thumb is the 30% rule, which suggests that no more than 30% of your gross income should go towards housing costs. This guideline helps maintain a balance between your housing expenses and other essential living costs, such as food, utilities, transportation, and savings. However, this percentage can vary based on individual circumstances, such as your location, income level, and personal financial goals. For instance, in high-cost-of-living areas, you might need to allocate a larger portion of your income to rent, while in more affordable regions, you may be able to get by with a smaller percentage. Ultimately, it's crucial to create a budget that works for you and allows you to live comfortably within your means.

Explore related products

What You'll Learn

- General guideline: 30% of income for rent is a common rule of thumb

- Location factors: Rent percentages vary by city; higher in urban areas

- Budgeting tips: Prioritize essential expenses, then allocate for rent

- Roommate considerations: Sharing a space can reduce individual rent costs

- Salary variations: Higher income may allow for a higher rent percentage

![]()

General guideline: 30% of income for rent is a common rule of thumb

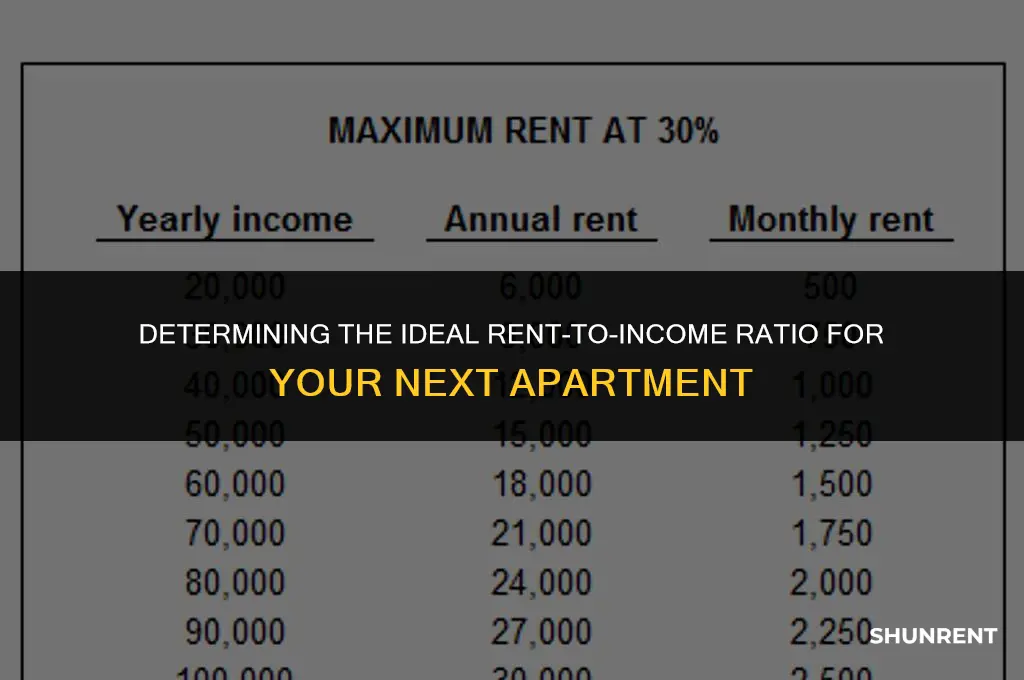

The 30% rule for rent allocation is a widely accepted guideline in personal finance. This principle suggests that a person should spend no more than 30% of their gross income on housing costs. The rationale behind this rule is to ensure that individuals have enough money left over for other essential expenses, savings, and discretionary spending. By capping rent at 30% of income, one can maintain a balanced budget and avoid the pitfalls of overspending on housing.

To apply the 30% rule effectively, it's crucial to calculate your gross income accurately. This includes all sources of income before taxes and deductions. Once you have your gross income figure, multiply it by 0.30 to determine the maximum amount you should spend on rent. For example, if your gross income is $5,000 per month, you should aim to spend no more than $1,500 on rent.

However, it's important to note that the 30% rule is a general guideline and may not be suitable for everyone. Factors such as location, lifestyle, and financial goals can influence how much one should allocate to housing. In high-cost-of-living areas, it may be necessary to spend more than 30% of income on rent to secure adequate housing. Conversely, in areas with lower living costs, one might be able to spend less than 30% and still maintain a comfortable lifestyle.

When deciding how much of your income to allocate to rent, it's also essential to consider your other financial obligations. This includes expenses such as utilities, groceries, transportation, healthcare, and debt payments. By taking a holistic approach to budgeting, you can ensure that you're not overextending yourself financially and that you have enough resources to cover all your needs.

In conclusion, while the 30% rule for rent allocation is a useful starting point, it's important to tailor this guideline to your individual circumstances. By considering factors such as location, lifestyle, and financial goals, you can determine a rent budget that is both affordable and sustainable. Remember to regularly review and adjust your budget as your financial situation changes to ensure that you're always on track with your financial goals.

Where to Rent 'Into the Spider-Verse': Your Ultimate Streaming Guide

You may want to see also

Explore related products

![]()

Location factors: Rent percentages vary by city; higher in urban areas

Rent percentages vary significantly by city, with urban areas typically commanding higher rates due to increased demand and limited space. For instance, in major metropolitan areas like New York City or San Francisco, rent can easily consume 30% or more of an individual's income. In contrast, smaller cities or rural areas may have much lower rent-to-income ratios, potentially falling below 10%.

Several factors contribute to these disparities. Urban centers often have higher costs of living overall, including expensive transportation, food, and entertainment options. Additionally, the concentration of jobs and educational institutions in these areas drives up demand for housing, allowing landlords to charge premium rates. On the other hand, smaller cities and rural areas may have lower demand and more available housing stock, leading to more affordable rent prices.

When determining how much of your income should go towards rent, it's essential to consider the specific location you're in. A general rule of thumb is to allocate no more than 30% of your gross income towards housing costs, but this may not be feasible in all areas. In high-rent cities, you may need to adjust your budget accordingly, potentially prioritizing housing over other expenses or considering alternative living arrangements such as roommates or subletting.

It's also important to factor in other location-specific costs when calculating your rent budget. For example, if you live in an area with high transportation costs, you may need to allocate more of your income towards rent to compensate for the increased expenses. Similarly, if you have access to affordable amenities such as grocery stores or healthcare facilities, you may be able to allocate less of your income towards rent.

Ultimately, the key to determining how much of your income should go towards rent is to carefully evaluate your individual circumstances and the specific location you're in. By considering factors such as local rent percentages, cost of living, and personal financial goals, you can make an informed decision that works best for you.

Understanding Minimum Lease Durations: A Tenant's Guide

You may want to see also

Explore related products

![]()

Budgeting tips: Prioritize essential expenses, then allocate for rent

To effectively manage your budget, it's crucial to prioritize essential expenses before allocating funds for rent. Essential expenses include necessities like food, utilities, healthcare, and transportation. By addressing these critical costs first, you ensure that you have a solid foundation for your financial stability. Once these essentials are covered, you can then determine how much of your income should be allocated towards rent.

A common rule of thumb is the 30% rule, which suggests that rent should not exceed 30% of your gross income. However, this may not always be feasible, especially in areas with high living costs. In such cases, it's important to strike a balance between rent and other essential expenses. Consider creating a detailed budget that lists all your monthly expenses, including rent, utilities, groceries, and other necessities. This will help you visualize where your money is going and identify areas where you can cut costs.

Another approach is to use the 50/30/20 rule, where 50% of your income goes towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment. By applying this rule, you can ensure that you're not only covering your necessities but also making progress towards your financial goals.

When allocating funds for rent, it's also important to consider additional costs such as utilities, maintenance fees, and potential increases in rent over time. Factor these expenses into your budget to avoid any surprises down the line. Additionally, be mindful of your lease terms and any penalties associated with breaking your lease early.

In conclusion, prioritizing essential expenses and then allocating funds for rent is a key aspect of effective budgeting. By following these tips and considering your unique financial situation, you can create a budget that works for you and ensures your financial stability.

Affordable U-Haul Rentals: Uncovering Cost-Effective Moving Solutions

You may want to see also

Explore related products

![]()

Roommate considerations: Sharing a space can reduce individual rent costs

Sharing a living space with roommates can significantly reduce the financial burden of rent, making it a practical solution for many individuals, especially in urban areas where housing costs can be exorbitant. By splitting the rent among multiple occupants, each person's share can be substantially lower than if they were to rent a place on their own. This arrangement can be particularly beneficial for young professionals, students, or anyone looking to save money while still enjoying the comforts of a well-furnished apartment.

However, finding the right roommates and managing the shared space effectively requires careful consideration and planning. Potential roommates should be vetted for their reliability, cleanliness, and compatibility with the existing occupants. Establishing clear rules and expectations from the outset can help prevent conflicts and ensure a harmonious living environment. Additionally, creating a shared budget for utilities and other common expenses can help distribute costs fairly and avoid misunderstandings.

One of the key advantages of sharing a space is the opportunity to build lasting friendships and create a sense of community. Living with others can foster personal growth and provide a support system, which can be invaluable, especially for those who are new to a city or country. Moreover, roommates can often share resources, such as furniture, appliances, and even food, further reducing individual expenses.

On the other hand, sharing a living space also comes with its challenges. Privacy can be limited, and personal space may be encroached upon if not properly managed. Noise levels, cleanliness standards, and differing lifestyles can all be sources of tension. It is essential for roommates to communicate openly and address any issues promptly to maintain a positive living situation.

In conclusion, while sharing a living space with roommates can be an effective way to reduce rent costs, it requires careful selection of roommates, clear communication, and a willingness to compromise. By navigating these considerations thoughtfully, individuals can enjoy the financial benefits of shared housing while also fostering meaningful connections and a supportive living environment.

Beyond the Security Deposit: Renter Responsibilities in Short-Term Leases

You may want to see also

Explore related products

![]()

Salary variations: Higher income may allow for a higher rent percentage

Individuals with higher incomes often have more flexibility when it comes to allocating a portion of their earnings towards rent. This is because a higher salary can accommodate a larger percentage dedicated to housing costs without compromising other essential expenses or financial goals. For instance, someone earning $100,000 per year may be able to comfortably allocate 30% of their income towards rent, which would amount to $3,000 per month. In contrast, an individual earning $50,000 per year might need to limit their rent expenditure to 25% of their income, equating to $1,250 per month, to ensure they have enough funds for other necessities.

The relationship between income and rent percentage can also be influenced by factors such as the cost of living in a particular area, the presence of dependents, and personal financial priorities. For example, in high-cost urban areas like New York City or San Francisco, even individuals with higher incomes may need to allocate a significant portion of their earnings towards rent to secure adequate housing. Conversely, in more affordable regions, a higher income may allow for a lower rent percentage while still maintaining a comfortable standard of living.

When determining the appropriate rent percentage based on income, it's essential to consider the 50-30-20 rule, a common budgeting guideline. This rule suggests that 50% of income should be allocated towards necessary expenses (such as rent, utilities, and groceries), 30% towards discretionary spending (like entertainment and dining out), and 20% towards savings and debt repayment. However, this is a general guideline and may need to be adjusted based on individual circumstances and financial goals.

In conclusion, salary variations play a significant role in determining the percentage of income that should be allocated towards rent. Higher incomes generally allow for a higher rent percentage, but this should be balanced against other financial obligations and priorities to ensure a sustainable and comfortable living situation.

Renting in Virginia: Does It Trigger Residency Tax Obligations?

You may want to see also

Frequently asked questions

A common rule of thumb is the 30% rule, which suggests that you should spend no more than 30% of your gross income on rent. This allows you to have enough money left over for other essential expenses, savings, and discretionary spending.

To determine if you're paying too much for rent, you can use the 30% rule as a guideline. If your rent exceeds 30% of your gross income, it may be considered too high. Additionally, you can compare your rent to the average rent in your area for similar properties to see if it's above market rate.

There are several strategies you can use to reduce your rent burden. These include:

- Negotiating with your landlord for a lower rent

- Looking for a roommate to share the rent

- Moving to a less expensive neighborhood or city

- Downsizing to a smaller apartment

- Increasing your income through a side job or salary raise