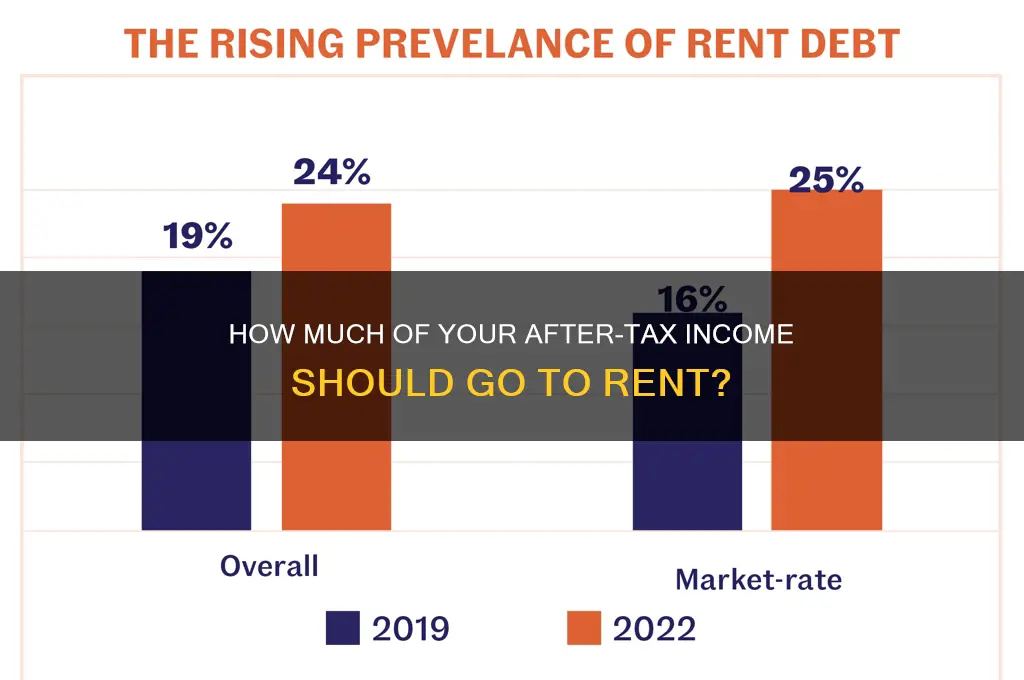

Determining what percentage of after-tax income should be allocated to rent is a critical financial consideration for individuals and families. Financial experts often recommend the 30% rule, which suggests that no more than 30% of one’s after-tax income should be spent on housing costs, including rent. This guideline helps ensure that individuals have enough funds left for other essential expenses, savings, and discretionary spending. However, this percentage can vary based on factors such as location, income level, and personal financial goals. In high-cost-of-living areas, for instance, individuals might need to allocate a higher percentage to rent, while those in more affordable regions may spend significantly less. Understanding this balance is key to maintaining financial stability and avoiding housing-related stress.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less of after-tax income |

| Average Rent Burden in the U.S. | ~30-40% of after-tax income (varies by city and income level) |

| Low-Income Households | Often spend 50% or more of after-tax income on rent |

| High-Cost Urban Areas | Rent can exceed 50% of after-tax income (e.g., San Francisco, NYC) |

| Global Comparison | U.S. average is higher than many European countries (e.g., Germany: 25%) |

| Affordable Housing Threshold | Rent should not exceed 30% of gross income (HUD standard) |

| Median Rent-to-Income Ratio (U.S.) | ~27% (as of 2023, varies by source) |

| Impact of Inflation | Rising rents outpace income growth, increasing rent burden |

| Regional Variations | Southern and Midwestern U.S. cities have lower ratios (~25%) |

| Policy Interventions | Rent control, housing subsidies, and zoning reforms aim to reduce burden |

Explore related products

What You'll Learn

- Affordable Rent Thresholds: Define income percentages ensuring renters avoid financial strain from housing costs

- Regional Cost Variations: Analyze how rent-to-income ratios differ across cities and rural areas

- Budgeting Strategies: Methods to allocate after-tax income efficiently while covering rent and essentials

- Policy Impacts: Examine government housing policies influencing rent affordability for various income groups

- Historical Trends: Track changes in rent-to-income ratios over decades to identify affordability shifts

![]()

Affordable Rent Thresholds: Define income percentages ensuring renters avoid financial strain from housing costs

A widely accepted rule of thumb suggests that renters should allocate no more than 30% of their after-tax income to housing costs. This benchmark, often referred to as the "30% rule," stems from federal affordability guidelines established in the 1960s. However, this one-size-fits-all approach fails to account for variations in income levels, cost of living, and individual financial obligations. For instance, a single earner making $30,000 annually would struggle to manage other expenses if paying $750 monthly rent, while a dual-income household earning $100,000 might find $2,500 rent manageable. This highlights the need for more nuanced thresholds tailored to specific financial contexts.

To refine affordability thresholds, consider a tiered approach based on income brackets. For low-income households (below $40,000 annually), capping rent at 25% of after-tax income provides a buffer for essentials like food, healthcare, and transportation. Middle-income earners ($40,000–$80,000) could reasonably allocate up to 30%, while higher-income households (above $80,000) might stretch to 35% without compromising financial stability. For example, a family earning $50,000 after taxes should aim for rent below $1,250 monthly, whereas someone earning $100,000 could afford up to $2,500. This tiered model acknowledges the disproportionate impact of housing costs on lower earners.

Beyond income, geographic cost of living disparities demand localized adjustments. In high-cost cities like San Francisco or New York, where median rents exceed $3,000, even the 30% rule may be unrealistic. Here, renters might need to prioritize shared housing or seek rent-controlled units. Conversely, in low-cost areas like the Midwest, renters could comfortably allocate closer to 20% of income to housing, freeing up funds for savings or debt repayment. Tools like the HUD Location Affordability Index can help renters assess regional affordability and adjust their thresholds accordingly.

Finally, renters must factor in non-housing expenses when determining their affordable rent threshold. A young professional with student loans might need to limit rent to 20% of income to accommodate debt payments, while a retiree with no debt could allocate more. Creating a detailed budget that accounts for fixed expenses (e.g., utilities, insurance) and variable costs (e.g., groceries, entertainment) ensures housing costs don’t crowd out other financial priorities. For instance, using a 50/30/20 budget (50% needs, 30% wants, 20% savings) can help renters identify a sustainable rent percentage within their overall financial plan.

In conclusion, defining affordable rent thresholds requires moving beyond the generic 30% rule to embrace income-based tiers, geographic adjustments, and individualized budgeting. By adopting these strategies, renters can avoid financial strain and build a stable foundation for long-term economic health.

Renting Office Space in Clonmel: A Comprehensive Guide for Businesses

You may want to see also

Explore related products

![]()

Regional Cost Variations: Analyze how rent-to-income ratios differ across cities and rural areas

Rent-to-income ratios are not one-size-fits-all; they fluctuate dramatically based on geographic location. In New York City, for instance, renters often allocate 40-50% of their after-tax income to housing, far exceeding the 30% threshold widely considered affordable. Conversely, in smaller cities like Tulsa, Oklahoma, this figure drops to around 20%, leaving residents with more disposable income for other expenses. This disparity underscores the importance of regional analysis when discussing housing affordability.

To understand these variations, consider the interplay of supply and demand. Urban centers with robust job markets and limited housing stock, such as San Francisco or Boston, drive rents upward, forcing residents to spend a larger share of their earnings on shelter. In contrast, rural areas and smaller towns often have surplus housing and lower demand, keeping rents relatively affordable. For example, in rural Iowa, renters typically spend only 15-20% of their after-tax income on housing, a stark contrast to metropolitan areas.

However, lower rent-to-income ratios in rural areas do not always equate to financial ease. Rural residents often face lower average incomes, meaning even a smaller percentage of income spent on rent can strain budgets. Additionally, limited access to high-paying jobs in these regions can exacerbate financial challenges. For instance, while a renter in rural Mississippi might spend only 18% of their income on housing, their overall earnings may be significantly lower than those in urban areas, making other expenses proportionally more burdensome.

When analyzing regional cost variations, it’s crucial to account for local economies and cost-of-living indices. In cities like Austin, Texas, where tech industry growth has driven up both incomes and rents, the rent-to-income ratio remains relatively stable at around 25-30%. Meanwhile, in declining industrial towns, such as those in the Rust Belt, stagnant wages and declining populations can lead to artificially low rent-to-income ratios, masking underlying economic distress.

For individuals and policymakers, understanding these regional nuances is essential for making informed decisions. Urban dwellers may need to prioritize high-income careers or consider suburban living to balance housing costs. Rural residents, on the other hand, might benefit from initiatives aimed at boosting local wages or diversifying economies. By examining rent-to-income ratios through a regional lens, we can better address the unique affordability challenges faced by different communities.

Discover LA's Most Affordable Rent: Cheapest Options in Los Angeles

You may want to see also

Explore related products

![]()

Budgeting Strategies: Methods to allocate after-tax income efficiently while covering rent and essentials

A common rule of thumb suggests allocating no more than 30% of after-tax income to rent, yet this benchmark often falls short in high-cost urban areas where housing consumes closer to 50%. Such disparities highlight the need for flexible budgeting strategies tailored to individual circumstances rather than rigid adherence to one-size-fits-all percentages. To navigate this, consider a tiered approach: prioritize rent as the largest fixed expense, then allocate funds to essentials like groceries, utilities, and transportation, leaving discretionary spending for last. This ensures stability in covering non-negotiable costs while maintaining adaptability for fluctuating expenses.

Analyzing your income and expenses reveals patterns that inform smarter allocation. Start by categorizing after-tax income into three buckets: fixed costs (rent, insurance), variable essentials (food, transportation), and discretionary spending (entertainment, dining out). Use budgeting apps or spreadsheets to track spending for at least three months, identifying areas where cuts are feasible without compromising quality of life. For instance, reducing dining out from $300 to $150 monthly frees up funds to offset higher rent in a safer neighborhood, aligning spending with long-term priorities.

Persuasive arguments for the 50/30/20 rule—allocating 50% to needs, 30% to wants, and 20% to savings—often overlook the rent-heavy reality of many households. Instead, adopt a dynamic 60/20/20 model for high-rent scenarios: 60% for essentials (including rent), 20% for savings, and 20% for discretionary spending. This adjustment ensures rent remains manageable while still prioritizing financial security through consistent savings. For example, a $4,000 monthly after-tax income would allocate $2,400 to essentials (with $1,200 for rent), $800 to savings, and $800 for leisure, balancing necessity with flexibility.

Comparing budgeting methods like zero-based budgeting (allocating every dollar to a category) versus the envelope system (using cash for specific expenses) reveals their strengths in rent-heavy scenarios. Zero-based budgeting ensures every dollar is accounted for, reducing overspending, while the envelope system provides tangible limits on discretionary spending. Combining these methods—allocating cash for groceries and entertainment while digitally tracking fixed expenses—can create a hybrid system that maximizes control over rent and essentials. For instance, a $600 grocery budget in cash prevents overspending, while automated rent payments ensure timely payments.

Descriptive examples illustrate the impact of strategic allocation. Imagine a 28-year-old earning $50,000 annually, with after-tax income of $3,500 monthly. Rent at $1,200 (34%) exceeds the 30% rule but is offset by reducing car ownership costs ($200/month) and cooking at home ($300/month savings). By reallocating $500 from discretionary spending to an emergency fund, they maintain financial stability while covering essentials. This tailored approach demonstrates how small adjustments can align spending with priorities, even when rent consumes a larger share of income.

Effective Strategies to Advertise Your Apartment for Rent Successfully

You may want to see also

Explore related products

$11.39 $22

![]()

Policy Impacts: Examine government housing policies influencing rent affordability for various income groups

Government housing policies significantly shape rent affordability, often determining whether households spend a manageable or burdensome portion of their after-tax income on housing. For instance, in the U.S., the widely accepted affordability threshold is 30% of income, yet nearly half of renters exceed this, particularly in low-income brackets. Policies like rent control, housing vouchers, and tax incentives for developers directly influence these outcomes, but their effectiveness varies by income group and market conditions.

Consider rent control, a policy intended to stabilize costs for existing tenants. While it benefits long-term renters in high-demand areas, it can reduce new housing supply as developers avoid regulated markets. This unintended consequence disproportionately harms lower-income households, who face fewer options and higher rents in unregulated units. For example, San Francisco’s rent-controlled market saw a 15% decrease in rental unit turnover, limiting accessibility for new entrants, particularly those earning below the median income.

Housing voucher programs, such as Section 8 in the U.S., offer a more targeted approach by subsidizing rent for eligible low-income families. However, their success hinges on landlord participation and local rent levels. In areas with tight housing markets, voucher holders often struggle to find units within program limits, effectively capping their housing options. A 2021 study found that only 40% of voucher recipients in New York City secured housing within the 120-day search period, highlighting the policy’s limitations in high-cost regions.

Tax incentives for affordable housing development provide another policy lever, encouraging private investment in low-income housing. Programs like the Low-Income Housing Tax Credit (LIHTC) have financed over 3 million units since 1986. Yet, these credits often prioritize developers’ returns over deep affordability, with many units targeting households at 60% of the area median income, leaving the poorest 20% underserved. This gap underscores the need for layered policies that address both supply and subsidy.

Ultimately, the impact of housing policies on rent affordability depends on their design, implementation, and alignment with local market dynamics. Rent control may stabilize costs for some but risks stifling supply; vouchers offer flexibility but require landlord cooperation; and tax incentives can expand inventory but may overlook the neediest. Policymakers must balance these trade-offs, combining measures like inclusionary zoning, expanded voucher funding, and deeper subsidies to ensure affordability across income groups. Without such integration, even well-intentioned policies risk falling short of their equity goals.

Discover the Average Rent in Wichita, Kansas: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Historical Trends: Track changes in rent-to-income ratios over decades to identify affordability shifts

Rent-to-income ratios have fluctuated dramatically over the past century, reflecting broader economic shifts and housing policies. In the mid-20th century, for instance, the average American household spent approximately 20-25% of after-tax income on rent. This era, marked by post-war prosperity and subsidized housing programs, saw relatively stable affordability. However, by the 1980s, deregulation and rising urban demand pushed this figure closer to 30%, a threshold often cited as the upper limit of affordability. Tracking these changes reveals how external factors—from inflation to zoning laws—reshape the financial burden of housing over time.

To analyze historical trends effectively, start by examining census data and housing surveys from the 1950s onward. Compare median rents to median incomes, adjusting for inflation to ensure consistency. For example, in 1960, the median rent was $70 per month, while the median household income was $5,000 annually. Fast forward to 2020, and median rent had soared to $1,097 monthly, with median income reaching $67,521. While raw numbers show growth, the rent-to-income ratio reveals a starker narrative: from 16.8% in 1960 to 19.5% in 2020, indicating a creeping affordability crisis.

A persuasive argument emerges when considering the impact of policy on these trends. The 1970s saw the decline of public housing initiatives, coinciding with a sharp rise in rent-to-income ratios. Conversely, regions with consistent rent control policies, such as certain European cities, have maintained ratios below 25% for decades. This comparison underscores the role of government intervention in stabilizing housing costs. Advocates for affordability should push for policies that cap rent increases relative to income growth, ensuring historical spikes aren’t repeated.

For a practical takeaway, consider this step-by-step approach to tracking local trends: First, gather historical rent and income data from sources like the U.S. Census Bureau or local housing authorities. Second, calculate annual rent-to-income ratios for your area, adjusting for inflation using the Consumer Price Index. Third, plot these ratios on a graph to visualize shifts. Finally, correlate spikes or dips with local events—such as new housing developments or economic recessions—to understand causality. This method empowers individuals and policymakers alike to address affordability proactively.

In conclusion, historical rent-to-income ratios serve as a critical barometer of housing affordability. By studying these trends, we uncover patterns that inform policy, investment, and personal financial decisions. Whether you’re a researcher, advocate, or renter, understanding this metric provides actionable insights into one of the most pressing issues of our time.

Renting Colocation for Mining: Is the Investment Truly Worth It?

You may want to see also

Frequently asked questions

A widely accepted rule of thumb is to spend no more than 30% of your after-tax income on rent. This helps ensure you have enough funds for other expenses and savings.

Divide your monthly rent by your monthly after-tax income, then multiply by 100. For example, if your rent is $1,000 and your after-tax income is $4,000, the calculation is ($1,000 / $4,000) * 100 = 25%.

In high-cost areas, exceeding 30% may be necessary, but it’s important to adjust other expenses accordingly. Aim to keep total housing costs (rent, utilities, etc.) within 30-35% of after-tax income to maintain financial stability.