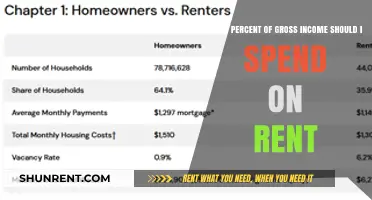

Determining what percent of income should go to rent in New York City is a critical financial consideration for residents, given the city’s notoriously high housing costs. While the general rule of thumb is to allocate no more than 30% of pre-tax income to rent, this guideline can be challenging to follow in NYC, where rental prices often exceed national averages. Factors such as neighborhood, apartment size, and personal financial goals further complicate this decision. For many New Yorkers, especially those with lower incomes, rent may consume a significantly larger portion of their earnings, leading to financial strain. Understanding this balance is essential for budgeting effectively and maintaining financial stability in one of the world’s most expensive cities.

Explore related products

What You'll Learn

![]()

NYC Rent Affordability Guidelines

In New York City, the 30% rule is often cited as the benchmark for rent affordability, but this guideline can feel disconnected from the city’s reality. For a single person earning the median income of $70,000 annually, 30% translates to $1,750 monthly—a figure that barely covers a studio in many neighborhoods. This disparity highlights the need for a more nuanced approach to NYC rent affordability guidelines, one that accounts for the city’s unique economic and housing landscape.

Consider the 50/30/20 budget rule, a framework that allocates 50% of income to necessities, 30% to discretionary spending, and 20% to savings. Applied to NYC, this suggests that rent could reasonably consume up to 40% of income if other necessities (like groceries and transportation) are factored in. For instance, a household earning $100,000 might allocate $4,000 monthly to housing, but this still falls short in areas like Manhattan or Brooklyn, where median rents exceed $3,500. The takeaway? The 30% rule may be aspirational rather than practical in NYC, necessitating adjustments based on individual circumstances.

For low-income households, NYC’s Housing Wage—the hourly wage needed to afford a two-bedroom rental without spending more than 30% of income—is $42.88, far above the city’s minimum wage of $15. This gap underscores the importance of supplemental programs like Section 8 vouchers or rent-stabilized units. For those relying on these resources, the affordability threshold shifts dramatically, with rent often capped at 30% of adjusted income rather than gross earnings. Practical tip: Use the NYC Housing Connect portal to explore affordable housing lotteries, which prioritize applicants based on income brackets.

Young professionals and recent graduates often face a different challenge: balancing rent with student loan payments and career-building expenses. In this demographic, a sliding scale approach may be more realistic. For example, someone earning $50,000 annually might allocate 45% of their income to rent in the short term, aiming to reduce this percentage as their earnings grow. Caution: Avoid committing more than 50% of your income to rent, as this leaves little room for emergencies or savings. Pair higher rent expenditures with strict budgeting in other areas, such as dining out or subscriptions.

Finally, consider the neighborhood factor. Rent affordability in NYC is deeply tied to location. In The Bronx, the median rent is around $1,600, while in Manhattan, it surpasses $4,000. A practical strategy is to prioritize neighborhoods where your target rent percentage aligns with local averages. For instance, if you’re aiming to spend 35% of a $60,000 income ($1,750 monthly), neighborhoods like Sunset Park or Astoria might be more feasible than Williamsburg or the Upper East Side. Tools like StreetEasy’s affordability calculator can help identify areas where your budget aligns with market rates. Conclusion: NYC’s rent affordability guidelines require flexibility, creativity, and a willingness to adapt to the city’s ever-evolving housing market.

Understanding Late Rent Payments: Average Rates and Key Insights

You may want to see also

Explore related products

![]()

Income-to-Rent Ratios Explained

In New York City, the 30% rule is often cited as a benchmark for income-to-rent ratios, suggesting that no more than 30% of your gross monthly income should go toward rent. This guideline, established by the U.S. Department of Housing and Urban Development (HUD), aims to ensure financial stability by leaving room for other expenses like utilities, groceries, and savings. However, in NYC’s hyper-competitive rental market, adhering to this rule can be challenging. For instance, the median rent for a one-bedroom apartment in Manhattan exceeds $3,500, while the median household income hovers around $70,000 annually. Simple math reveals that many renters far exceed the 30% threshold, often allocating closer to 50% or more of their income to housing.

To navigate this reality, it’s essential to reassess your budget and prioritize ruthlessly. Start by calculating your gross monthly income and multiplying it by 0.3 to determine your ideal rent limit. If NYC’s market pushes you beyond this, consider roommates, outer boroughs, or smaller units to reduce costs. For example, renting a studio in Brooklyn instead of a one-bedroom in Manhattan can save you upwards of $1,000 monthly. Additionally, factor in transportation costs if moving farther from the city center, as these can offset some savings. Tools like rent calculators and neighborhood guides can help you make informed decisions.

Critics argue that the 30% rule is outdated, particularly in high-cost cities like NYC, where housing consumes a larger share of income. A more realistic approach might be the 50/30/20 budget rule, which allocates 50% of income to necessities (including rent), 30% to discretionary spending, and 20% to savings and debt repayment. This framework acknowledges the financial pressures of urban living while still encouraging savings. For NYC renters, this might mean accepting a higher rent burden but ensuring other expenses are trimmed accordingly. For instance, cooking at home instead of dining out can free up funds to accommodate higher rent.

Ultimately, the income-to-rent ratio is a personal decision influenced by lifestyle, career stage, and financial goals. Young professionals starting their careers might prioritize living in trendier neighborhoods, even if it means spending 40% of their income on rent, while families may opt for lower ratios to prioritize savings and education funds. The key is to strike a balance that aligns with your long-term objectives. Regularly reviewing your budget and adjusting as your income grows or expenses change can help maintain financial health in NYC’s demanding rental landscape.

Renting Morgan County's City Park for Musikfest: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Budgeting for NYC Housing Costs

In New York City, the 30% rule is often cited as a benchmark for rent affordability, but this guideline can feel unrealistic in a market where median rents hover around $3,500 per month. For a household to comfortably afford this, they’d need an annual income of at least $140,000, placing them in the top quartile of earners. This disparity highlights why budgeting for NYC housing requires a tailored approach, not a one-size-fits-all rule.

To navigate this challenge, start by calculating your *net effective rent*, which accounts for concessions like free months or reduced fees. For instance, a $3,000/month apartment with one free month effectively costs $2,833 monthly. Next, assess your income stability. If you’re a freelancer or in a volatile industry, aim to keep housing costs below 25% of your income to build a buffer for lean months. Conversely, dual-income households with steady jobs might stretch to 35% if it means securing a desirable location or larger space.

A practical strategy is to prioritize *trade-offs* rather than sacrifices. For example, living in a further-out neighborhood like Astoria or Sunset Park can reduce rent by 20–30% compared to Manhattan or Williamsburg. Alternatively, consider a roommate situation, which can halve your rent burden. In 2023, 40% of NYC renters shared housing, making it a common and effective cost-saving measure.

Finally, factor in *hidden housing costs* like utilities, internet, and renters insurance, which can add $200–$400 monthly. Build these into your budget to avoid overspending. For instance, if your rent is $2,500, allocate $2,700–$2,900 for total housing expenses. This granular approach ensures you’re not just surviving in NYC but thriving within your means.

Do You Need a Deposit for Renting Storage Space?

You may want to see also

Explore related products

![]()

Impact of High Rent on Savings

High rent in NYC often consumes 40-50% of a tenant’s income, far exceeding the federally recommended 30% threshold. This disparity forces individuals to allocate a disproportionate share of their earnings to housing, leaving limited funds for other essentials, let alone savings. For example, a New Yorker earning $70,000 annually might spend $28,000 to $35,000 on rent, compared to the ideal $21,000. This $7,000 to $14,000 gap could otherwise fund emergency savings, retirement accounts, or debt repayment, but instead vanishes into the city’s rental market.

The impact of high rent on savings is not just financial but psychological. When a significant portion of income goes to rent, individuals experience heightened financial stress, often leading to short-term financial decisions that undermine long-term stability. For instance, a 2022 study found that NYC renters saving less than 10% of their income were twice as likely to rely on high-interest credit cards or payday loans during emergencies. This cycle of debt further erodes the ability to save, creating a vicious loop that perpetuates financial insecurity.

To mitigate the impact of high rent on savings, practical strategies are essential. First, consider roommates or smaller living spaces to reduce rent burden. For example, sharing a two-bedroom apartment in Brooklyn can save up to $500 monthly compared to living alone. Second, prioritize high-yield savings accounts or automated savings plans to maximize the limited funds available. Even saving 5% of income consistently can accumulate to $3,500 annually for someone earning $70,000. Lastly, explore NYC’s housing assistance programs, such as the Housing Choice Voucher Program, which can reduce rent to 30% of income for eligible households.

Comparatively, cities with lower rent burdens, like Austin or Phoenix, see residents saving 15-20% of their income on average. This highlights the systemic challenge in NYC, where the high cost of living stifles financial resilience. While moving may not be feasible for everyone, adopting a budget-first mindset can help. Allocate income using the 50/30/20 rule (50% needs, 30% wants, 20% savings), adjusting for NYC’s realities by capping rent at 40% and aggressively cutting discretionary spending to free up savings.

Ultimately, the impact of high rent on savings in NYC is a call to action for both individuals and policymakers. For tenants, it’s about making deliberate choices—like downsizing or leveraging shared living—to reclaim financial flexibility. For the city, it’s about addressing the root causes of housing affordability through rent control, increased supply, and tenant protections. Without intervention, the savings gap will widen, leaving New Yorkers vulnerable to economic shocks and delaying milestones like homeownership or retirement. The question isn’t just how much rent one can afford, but how much future one is willing to sacrifice.

Understanding Section 8 Monthly Rent Asking Rates: A Comprehensive Guide

You may want to see also

Explore related products

![The Allocation of Corporate Income for the Purpose of State Taxation [microform]](https://m.media-amazon.com/images/I/61zFmB76r6L._AC_UY218_.jpg)

![]()

Adjusting Lifestyle for NYC Rent

Living in New York City often means allocating a significant portion of your income to rent, with many experts suggesting that 30% is the ideal threshold. However, in a city where the median rent exceeds $3,000, this rule can feel unattainable for many. Adjusting your lifestyle to accommodate NYC rent requires strategic planning and a willingness to reprioritize your spending. Start by evaluating your current expenses and identifying areas where you can cut back. For instance, reducing dining out from five times a week to twice can save hundreds of dollars monthly, which can then be redirected toward rent.

One practical approach is to adopt a "needs vs. wants" mindset. Essentials like groceries, transportation, and utilities should take precedence over discretionary spending. Consider swapping expensive gym memberships for free workouts in parks or opting for public transit instead of ride-sharing. Additionally, explore shared housing options or rent-stabilized apartments, which can significantly lower your monthly burden. For example, living with roommates in a two-bedroom apartment in Brooklyn can reduce individual rent by up to 40% compared to living alone in a studio in Manhattan.

Another key adjustment is rethinking entertainment and leisure. NYC offers countless free or low-cost activities, from museum days to community events. Instead of spending $50 on a Broadway show, explore off-Broadway productions or free outdoor performances in the summer. Cooking at home instead of ordering takeout can also free up funds, with the average meal prep costing less than half of restaurant dining. Small, consistent changes like these can collectively make a substantial difference in your budget.

Finally, consider increasing your income to better align with NYC’s high cost of living. Side hustles, freelance work, or asking for a raise at your current job can provide the financial cushion needed to manage rent without sacrificing quality of life. For instance, a part-time gig earning $500 extra per month could cover the difference if your rent exceeds the 30% rule. Balancing lifestyle adjustments with income growth ensures that living in NYC remains feasible without feeling financially strained.

Rent-A-Center: Floor Models or New?

You may want to see also

Frequently asked questions

A widely accepted guideline is the 30% rule, which suggests that no more than 30% of your gross monthly income should be spent on rent. However, due to NYC's high cost of living, many residents end up spending closer to 40-50% of their income on rent.

Following the 30% rule in NYC can be challenging due to the city's high rental costs. Many residents, especially those with lower incomes, often exceed this threshold, sometimes spending up to 50% or more of their income on rent. It’s important to budget carefully and consider roommates or outer boroughs to manage costs.

Calculate your net monthly income (after taxes) and subtract essential expenses like groceries, transportation, and utilities. The remaining amount should cover rent while leaving room for savings and discretionary spending. If 30% of your gross income isn't feasible, aim for a ratio that allows you to meet your financial goals without feeling strained.