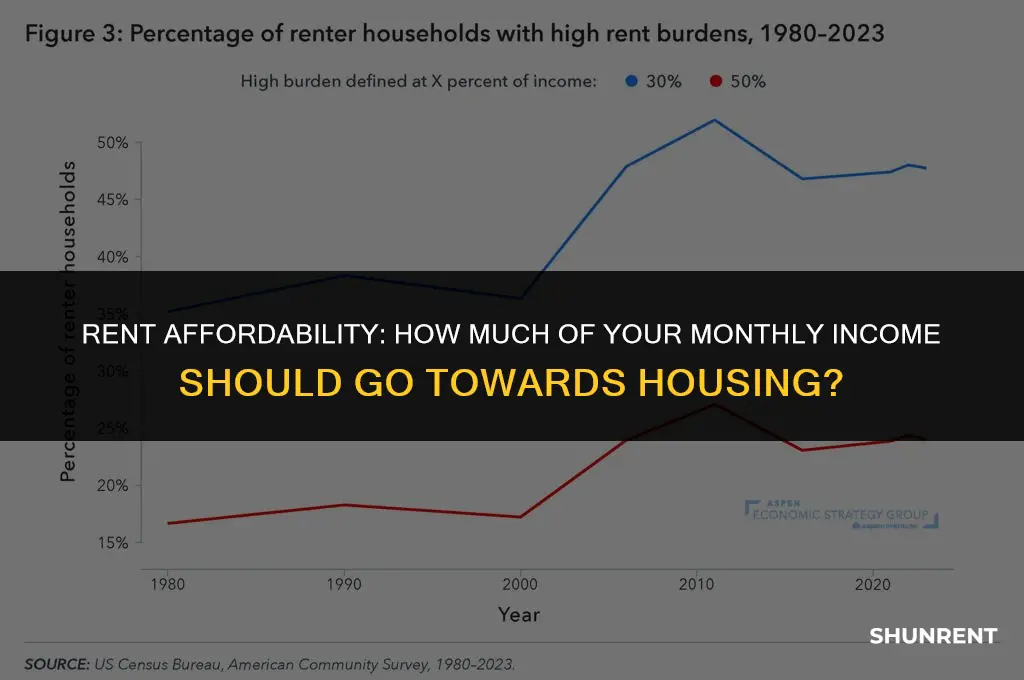

When determining what percentage of monthly income should be allocated for rent, it's essential to consider various factors that can influence this decision. Financial experts often recommend the 30% rule, which suggests that rent should not exceed 30% of your gross monthly income. This guideline helps ensure that you have enough money left over for other essential expenses, savings, and discretionary spending. However, this percentage can vary based on individual circumstances, such as the cost of living in your area, your debt obligations, and your personal financial goals. For instance, in high-cost urban areas, it might be necessary to allocate a higher percentage of income towards rent, while in more affordable regions, you may be able to get by with a lower percentage. Ultimately, the key is to strike a balance that allows you to maintain financial stability and achieve your long-term objectives.

Explore related products

What You'll Learn

- General Guidelines: Recommended percentages for rent based on income

- Financial Planning: Strategies for budgeting rent within monthly income

- Market Variations: How rent percentages differ by city or region

- Housing Assistance: Programs that help with rent affordability

- Rent Calculators: Tools to determine affordable rent based on income

![]()

General Guidelines: Recommended percentages for rent based on income

Determining the appropriate percentage of monthly income to allocate for rent is a crucial aspect of financial planning. General guidelines suggest that individuals should aim to spend between 25% to 30% of their gross monthly income on housing costs. This range allows for a balance between affordability and the ability to save for other financial goals. However, these percentages are not one-size-fits-all and can vary based on individual circumstances, such as debt obligations, savings goals, and lifestyle preferences.

For those with higher income levels, the 25% to 30% rule may result in excessive spending on rent. In such cases, it may be more prudent to allocate a smaller percentage of income towards housing and invest the remainder in other areas, such as retirement savings or wealth-building opportunities. Conversely, individuals with lower income levels may need to adjust their budget to accommodate higher rent costs, potentially seeking additional sources of income or reducing expenses in other areas.

When evaluating the recommended percentages for rent based on income, it is essential to consider the overall financial picture. This includes assessing current debt obligations, such as student loans or credit card debt, as well as savings goals, like building an emergency fund or saving for a down payment on a home. By taking a holistic approach to financial planning, individuals can make informed decisions about their housing costs and ensure they are aligning their spending with their long-term financial objectives.

In addition to income, other factors can influence the appropriate percentage of income to allocate for rent. For example, the cost of living in a particular area can significantly impact housing affordability. In high-cost-of-living cities, individuals may need to allocate a larger percentage of their income towards rent to secure adequate housing. Similarly, lifestyle preferences, such as the desire for a larger living space or proximity to certain amenities, can also affect the recommended rent percentage.

Ultimately, the key to determining the appropriate percentage of monthly income for rent is to conduct a thorough analysis of one's financial situation and housing needs. By considering factors such as income level, debt obligations, savings goals, and lifestyle preferences, individuals can make informed decisions about their housing costs and ensure they are on a path towards financial stability and security.

Exploring the Average Rent in Indiana: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Financial Planning: Strategies for budgeting rent within monthly income

Determining the appropriate percentage of monthly income to allocate for rent is a critical aspect of financial planning. A common rule of thumb is the 30% rule, which suggests that rent should not exceed 30% of your gross monthly income. However, this guideline may not be suitable for everyone, especially in high-cost-of-living areas or for individuals with significant debt or financial obligations.

To create a more personalized budget, start by calculating your net income after taxes and deductions. Then, list all your monthly expenses, including utilities, groceries, transportation, and debt payments. Subtract these expenses from your net income to determine how much you have left for rent. This approach will give you a clearer picture of what you can realistically afford.

Another strategy is to use the 50/30/20 rule, which allocates 50% of your income for necessities (including rent), 30% for discretionary spending, and 20% for savings and debt repayment. This rule can help ensure that you're not only covering your essential expenses but also making progress towards your financial goals.

When budgeting for rent, it's also important to consider the potential for unexpected expenses or changes in your financial situation. Building an emergency fund that covers 3-6 months of living expenses can provide a safety net in case of job loss or other financial setbacks. Additionally, regularly reviewing and adjusting your budget can help you stay on track and adapt to any changes in your income or expenses.

Ultimately, the key to successful financial planning is to find a balance between your rent and other expenses that allows you to live comfortably while also saving for the future. By carefully evaluating your income and expenses, and considering different budgeting strategies, you can create a plan that works best for your unique financial situation.

Renting a 4-Wheel Drive in Hawaii: Tips and Tricks

You may want to see also

Explore related products

![]()

Market Variations: How rent percentages differ by city or region

Rent percentages can vary significantly depending on the city or region you're in. For instance, in major metropolitan areas like New York City or San Francisco, it's not uncommon for rent to consume 30% or more of a person's monthly income. This is due to the high demand for housing in these areas, coupled with limited supply, which drives up prices. In contrast, in smaller cities or rural areas, rent may only account for 10-15% of monthly income, as the cost of living is generally lower and there is often more available housing.

Another factor that can influence rent percentages is the local economy. Cities with booming economies and high job growth rates tend to have higher rents, as more people are drawn to the area and compete for housing. On the other hand, cities with struggling economies may have lower rents, as fewer people are moving to the area and there is less demand for housing.

It's also important to consider the type of housing when looking at rent percentages. For example, a one-bedroom apartment in a city center may cost significantly more than a three-bedroom house in a suburban area. Additionally, amenities such as parking, utilities, and pet-friendliness can also impact rent prices.

To get a better understanding of rent percentages in different cities and regions, it can be helpful to look at rent reports or housing market analyses. These resources can provide valuable insights into the average rent prices in different areas, as well as trends over time. By doing your research, you can make a more informed decision about where to live and how much rent you can afford.

Own vs. Rent: Navigating Application Deployment Strategies for Your Business

You may want to see also

Explore related products

![]()

Housing Assistance: Programs that help with rent affordability

Housing assistance programs are designed to help individuals and families afford their rent, especially when it exceeds a certain percentage of their monthly income. These programs can be a lifeline for those struggling to make ends meet, providing financial support to ensure stable housing. One such program is the Housing Choice Voucher Program, commonly known as Section 8, which offers vouchers that cover a portion of the rent for eligible low-income families. Another option is the Low-Income Housing Tax Credit (LIHTC) program, which provides tax credits to developers who build or renovate affordable housing units, making them available at reduced rents.

Eligibility for these programs typically depends on factors such as income level, family size, and citizenship status. Applicants must meet specific criteria to qualify for assistance, and the amount of aid provided can vary based on individual circumstances. For instance, the Section 8 program generally requires that a family's income does not exceed 50% of the median income for the area, although this can vary by location. The LIHTC program, on the other hand, targets households earning between 20% and 60% of the area median income.

To apply for housing assistance, individuals must gather necessary documentation, such as proof of income, identification, and rental agreements. They can then submit their applications to the relevant housing authority or agency, which will review the information and determine eligibility. Once approved, recipients can use the assistance to help cover their rent, ensuring they have a safe and stable place to live.

It's important to note that housing assistance programs are not a one-size-fits-all solution. They are designed to address specific needs and circumstances, and the availability of funding can vary by location and program. As such, it's crucial for individuals seeking assistance to research the programs available in their area and understand the eligibility requirements and application process. By doing so, they can increase their chances of securing the help they need to afford their rent and maintain stable housing.

Understanding Rent-to-Own: A Guide to This Housing Option

You may want to see also

![]()

Rent Calculators: Tools to determine affordable rent based on income

Rent calculators are invaluable tools for both tenants and landlords, providing a straightforward method to determine affordable rent based on income. These calculators typically require users to input their monthly gross income and, in some cases, additional financial obligations such as debt payments or childcare expenses. The tool then applies a standard affordability rule—often the 30% rule, which suggests that rent should not exceed 30% of one's monthly income—to calculate an appropriate rent range.

For tenants, using a rent calculator can help avoid the common pitfall of overextending financially. By ensuring that rent payments are within a sustainable range, tenants can better manage their budgets, save for emergencies, and maintain financial stability. Landlords, on the other hand, benefit from these tools by being able to set rents that are both competitive and reasonable, thereby attracting and retaining responsible tenants.

One of the key advantages of rent calculators is their ability to provide a quick and objective assessment of affordability. This can be particularly useful in competitive rental markets where tenants may feel pressured to commit to a lease quickly. By using a rent calculator, tenants can make informed decisions and negotiate rents that align with their financial capabilities.

Moreover, rent calculators can also serve as educational resources. They often include additional features such as budget tracking, financial tips, and market analysis, which can help users better understand their financial situations and make more informed housing choices. For example, some calculators may highlight the importance of maintaining a certain debt-to-income ratio or saving for a security deposit.

In conclusion, rent calculators are essential tools for determining affordable rent based on income. They provide a simple yet effective way for tenants to manage their finances and for landlords to set fair and competitive rents. By promoting financial responsibility and informed decision-making, these tools contribute to a more stable and equitable rental market.

Is Renting a House in Cozumel Safe? A Comprehensive Guide

You may want to see also

Frequently asked questions

The general rule of thumb is that you should spend no more than 30% of your gross monthly income on rent.

The 30% rule is calculated by taking 30% of your gross monthly income. For example, if your monthly income is $5,000, 30% would be $1,500.

Some factors that might influence the percentage of income spent on rent include the cost of living in the area, the size and type of housing, the number of people living in the household, and the individual's financial goals and priorities.

No, the 30% rule is not a hard and fast rule. It is a general guideline that can be adjusted based on individual circumstances. Some people may need to spend more or less than 30% of their income on rent depending on their specific situation.

Spending too much on rent can lead to financial stress and difficulty in affording other necessary expenses such as food, utilities, and healthcare. It can also make it challenging to save for long-term goals such as retirement or buying a home.