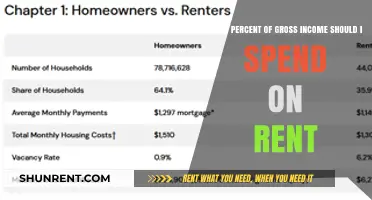

When considering the financial impact of renting, a common question arises: what percentage of pre-tax income should one allocate to rent? This is a crucial aspect of budgeting and financial planning, as it directly affects an individual's or household's overall financial health. Financial experts often recommend the 30% rule, which suggests that no more than 30% of one's pre-tax income should be spent on housing costs, including rent. This guideline aims to ensure that individuals have sufficient funds for other essential expenses, savings, and discretionary spending, promoting a balanced and sustainable lifestyle. However, this percentage can vary depending on factors such as location, income level, and personal financial goals, making it essential to assess individual circumstances when determining an appropriate rent-to-income ratio.

Explore related products

What You'll Learn

- Affordable Rent Thresholds: Define income percentages ensuring housing affordability without financial strain

- Regional Rent Variations: Analyze how location impacts pre-tax income allocation to rent

- Budgeting Strategies: Methods to balance rent expenses within pre-tax income limits

- Policy Influences: Government policies affecting rent-to-income ratios for households

- Income Fluctuations: Impact of variable income on sustainable rent percentage allocation

![]()

Affordable Rent Thresholds: Define income percentages ensuring housing affordability without financial strain

A widely accepted rule of thumb suggests that households should allocate no more than 30% of their pre-tax income to rent. This benchmark, established by the U.S. Department of Housing and Urban Development (HUD), aims to prevent financial strain while ensuring housing affordability. However, this one-size-fits-all approach overlooks critical factors such as geographic cost disparities, household size, and income variability. For instance, a family of four in San Francisco earning $80,000 annually would struggle to find housing within this threshold, while a single individual in rural Indiana might comfortably spend less than 20%. This highlights the need for a more nuanced definition of affordable rent thresholds.

To refine the 30% rule, consider a tiered approach based on income brackets and regional cost of living. For low-income households (below $30,000 annually), a 25% threshold is more realistic, as even small rent increases can lead to financial instability. Middle-income earners ($30,000–$70,000) might adhere to the traditional 30% guideline, while higher-income households (above $70,000) could allocate up to 35% without compromising other financial goals. Additionally, metropolitan areas with housing costs 50% above the national average should adjust thresholds downward by 5–10 percentage points to reflect local realities. This stratified model ensures affordability remains context-specific.

Implementing these thresholds requires practical tools for households and policymakers alike. Renters should calculate their pre-tax income monthly and multiply it by their applicable percentage to determine a sustainable rent limit. For example, a household earning $4,000 monthly should aim for rent below $1,200 (30% threshold). Policymakers can use these tiers to design housing subsidies or rent control measures, ensuring programs target those most at risk of housing insecurity. Pairing these thresholds with financial literacy programs can further empower individuals to make informed housing decisions.

Critics argue that income-based thresholds ignore other financial obligations, such as childcare, healthcare, and debt repayment. To address this, adopt a holistic budgeting framework where housing costs are one component of a balanced financial plan. For instance, the 50/30/20 rule allocates 50% of income to necessities (including rent), 30% to discretionary spending, and 20% to savings and debt repayment. Integrating affordable rent thresholds into such frameworks ensures housing remains affordable without sacrificing other essential expenses. This approach fosters long-term financial stability rather than merely addressing immediate housing needs.

Ultimately, defining affordable rent thresholds as a percentage of pre-tax income is a starting point, not a definitive solution. By tailoring thresholds to income levels, regional costs, and broader financial contexts, we can create a more equitable and sustainable housing landscape. Households and policymakers must collaborate to implement these guidelines, ensuring that housing affordability remains a cornerstone of economic well-being. After all, a home should be a foundation for prosperity, not a source of financial strain.

Rent-a-Wheel: 90-Day Interest-Free Financing Option

You may want to see also

Explore related products

![]()

Regional Rent Variations: Analyze how location impacts pre-tax income allocation to rent

The percentage of pre-tax income allocated to rent varies dramatically by region, with urban centers like New York City and San Francisco demanding upwards of 40–50% of earnings, compared to rural areas where renters might spend only 20–25%. This disparity isn’t just about city versus country; it’s a reflection of local economies, housing supply, and population density. For instance, in Manhattan, the median rent consumes nearly 60% of the average pre-tax income, while in Des Moines, Iowa, that figure drops to around 22%. Understanding these regional differences is crucial for budgeting, relocation decisions, and policy-making.

To analyze this further, consider the 30% rule, a common guideline suggesting that rent should not exceed 30% of pre-tax income. In high-cost regions, adhering to this rule often requires higher incomes or smaller living spaces. For example, a renter in Los Angeles earning $60,000 annually would need to find housing under $1,500 monthly to meet this threshold, a challenging feat in a market where the average rent exceeds $2,500. Conversely, in Tulsa, Oklahoma, where the average rent is $900, the same income allows for significantly more financial flexibility. This highlights how location dictates not just affordability but also lifestyle compromises.

Regional rent variations also reflect local job markets and wage levels. In tech hubs like Seattle or Austin, high-paying jobs inflate both incomes and housing costs, creating a skewed perception of affordability. A software engineer earning $120,000 might comfortably allocate 30% to rent in these cities, but a service worker earning $30,000 would struggle to find housing within the same threshold. This imbalance underscores the need for localized affordability metrics rather than one-size-fits-all guidelines.

For those considering relocation, a practical tip is to research price-to-income ratios for specific regions. This metric compares median housing costs to median incomes, offering a clearer picture of affordability. For instance, Miami has a ratio of 7.5, meaning residents spend 7.5 years of income to buy a home, while Pittsburgh’s ratio is 3.2. Renters can adapt this approach by comparing median rents to median incomes in their target area. Tools like Numbeo or the U.S. Census Bureau provide data to facilitate such comparisons.

In conclusion, regional rent variations are not just about geography—they’re a complex interplay of economics, demographics, and policy. By understanding these dynamics, individuals can make informed decisions about where to live, how much to save, and when to advocate for change. Whether you’re a renter in a high-cost city or considering a move, recognizing how location impacts pre-tax income allocation to rent is essential for financial stability and long-term planning.

QuickBooks Guide: Preparing 1099 Forms for Rental Income

You may want to see also

Explore related products

![]()

Budgeting Strategies: Methods to balance rent expenses within pre-tax income limits

A common rule of thumb suggests allocating no more than 30% of pre-tax income to rent, a guideline rooted in decades of financial planning. This benchmark, however, often clashes with the reality of skyrocketing housing costs in urban centers, where renters frequently exceed this limit. For instance, in cities like San Francisco or New York, residents may spend upwards of 50% of their income on rent, leaving little room for savings or emergencies. This disparity highlights the need for flexible budgeting strategies that adapt to individual circumstances rather than rigidly adhering to a one-size-fits-all rule.

To balance rent expenses within pre-tax income limits, start by reassessing your housing priorities. Consider downsizing to a smaller unit, moving to a less expensive neighborhood, or even exploring shared living arrangements. For example, a studio apartment in a suburban area might cost significantly less than a one-bedroom in the city center, freeing up funds for other financial goals. Pair this with a detailed budget that tracks all expenses, ensuring that rent doesn’t overshadow essentials like groceries, transportation, and healthcare. Tools like budgeting apps can automate this process, providing real-time insights into spending patterns.

Another effective strategy is to negotiate rent terms with your landlord. If you’ve been a reliable tenant, propose a longer lease in exchange for a reduced monthly rate or request a cap on annual rent increases. In some cases, offering to take on minor maintenance tasks, like landscaping or snow removal, can also lower your rent. For instance, a tenant in Chicago successfully negotiated a $100 monthly reduction by agreeing to handle seasonal yard work, saving $1,200 annually. This approach not only reduces housing costs but also fosters a positive landlord-tenant relationship.

For those with fluctuating incomes, such as freelancers or gig workers, creating a rent reserve fund is crucial. Set aside a portion of higher-earning months into a dedicated savings account to cover rent during slower periods. Aim to save at least one month’s rent as a buffer, gradually increasing this to three months’ worth for added security. Pair this with a dynamic budgeting approach that adjusts spending based on monthly earnings, ensuring rent remains manageable even during income dips.

Finally, consider increasing your pre-tax income to offset high rent costs. Explore side hustles, ask for a raise, or develop skills that qualify you for higher-paying roles. For example, a graphic designer earning $4,000 monthly might allocate $1,200 to rent, but by taking on freelance projects, they could boost their income to $5,000, reducing the rent-to-income ratio to 24%. This proactive approach not only eases financial strain but also empowers individuals to take control of their economic destiny. By combining strategic housing choices, negotiation, savings, and income growth, balancing rent within pre-tax limits becomes not just possible, but sustainable.

Renting Out Your LA Condo: A Step-by-Step Guide

You may want to see also

Explore related products

$11.39 $22

![]()

Policy Influences: Government policies affecting rent-to-income ratios for households

Government policies play a pivotal role in shaping the rent-to-income ratios that households face, often determining whether housing remains affordable or becomes a financial burden. One of the most direct interventions is rent control, a policy that caps the amount landlords can charge for rental units. While this measure can provide immediate relief for tenants, it often leads to unintended consequences. For instance, in cities like San Francisco, rent control has been linked to reduced housing supply as landlords opt to convert rental units into condos or Airbnb listings. This scarcity drives up rents for uncontrolled units, exacerbating affordability issues for those not covered by the policy. Policymakers must balance tenant protection with incentives for housing development to avoid such paradoxes.

Another critical policy tool is housing subsidies, which directly reduce the rent-to-income ratio for eligible households. Programs like the Housing Choice Voucher (HCV) program in the U.S. provide low-income families with vouchers to cover a portion of their rent, ensuring they spend no more than 30% of their income on housing. However, the effectiveness of these programs is often limited by funding constraints and administrative inefficiencies. For example, only one in four eligible households in the U.S. receives housing assistance due to insufficient federal funding. Expanding these programs and streamlining their administration could significantly reduce housing cost burdens for millions of families.

Tax incentives also influence rent-to-income ratios by encouraging the development of affordable housing. Governments can offer tax credits or deductions to developers who build units for low- and moderate-income households. The Low-Income Housing Tax Credit (LIHTC) program in the U.S. is a prime example, having financed over 3 million affordable units since its inception. However, these incentives often favor large-scale developers, leaving smaller builders and community-based initiatives at a disadvantage. Policymakers should consider tiered incentives that prioritize projects serving the lowest-income households and those in underserved areas.

Zoning laws and land-use regulations are another policy lever that indirectly affects rent-to-income ratios. Restrictive zoning, such as single-family-only zoning, limits housing density and drives up land costs, making it harder to build affordable units. Cities like Minneapolis have begun to address this by eliminating single-family zoning, allowing for more diverse and affordable housing types. Such reforms can increase housing supply and reduce rents over time, but they often face opposition from existing homeowners concerned about property values. Public education campaigns and phased implementation can help mitigate resistance and ensure equitable outcomes.

Finally, policies addressing income inequality are essential for tackling high rent-to-income ratios at their root. Minimum wage laws, earned income tax credits, and workforce development programs can increase household incomes, making housing more affordable without directly intervening in the rental market. For example, raising the minimum wage to $15 per hour could reduce the share of income spent on rent for millions of workers. However, these policies must be paired with housing supply measures to avoid inflationary pressures in the rental market. A holistic approach that combines income support with housing policy is key to achieving sustainable affordability.

Renting a Hospital Bed: Options, Costs, and What You Need to Know

You may want to see also

Explore related products

![]()

Income Fluctuations: Impact of variable income on sustainable rent percentage allocation

Variable income earners face a unique challenge when determining a sustainable rent percentage, as their earnings can fluctuate dramatically from month to month. Unlike salaried workers with predictable paychecks, freelancers, commission-based employees, and gig workers must navigate income volatility while maintaining housing stability. A commonly cited rule of thumb—allocating 30% of pre-tax income to rent—becomes precarious when income is inconsistent. For instance, a freelance graphic designer earning $6,000 one month and $2,000 the next would struggle to sustain a $1,500 rent payment during lean periods. This highlights the need for a more dynamic approach to rent budgeting for this demographic.

To mitigate the risk of overcommitting to rent, variable income earners should adopt a conservative baseline. Instead of targeting 30%, consider capping rent at 25% of average monthly pre-tax income over the past six months. For example, if earnings range from $3,000 to $7,000 monthly, calculate the average ($5,000) and allocate no more than $1,250 to rent. This buffer provides a safety net during low-income months. Additionally, maintaining an emergency fund equivalent to 3–6 months of essential expenses, including rent, is critical for financial resilience.

Another strategy involves prioritizing flexibility in housing arrangements. Variable income earners may benefit from shorter-term leases, roommate situations, or even co-living spaces that allow for adjustments in rent obligations. For instance, a commission-based salesperson might opt for a month-to-month lease or negotiate a rent cap with a landlord during slow seasons. This adaptability reduces the risk of defaulting on payments and aligns housing costs more closely with income fluctuations.

Finally, proactive income smoothing can help stabilize rent allocation. This involves setting aside a portion of high-earning months into a dedicated "rent reserve" account. For example, during a $7,000 income month, allocate $1,750 (30%) to rent and save the excess above the baseline ($1,250) in the reserve. This fund can then cover rent during lower-income months, ensuring consistent payments without strain. Pairing this strategy with detailed income tracking and forecasting tools, such as budgeting apps or spreadsheets, empowers variable income earners to make informed decisions about their housing commitments.

In summary, sustainable rent allocation for variable income earners requires a tailored approach that accounts for income unpredictability. By adopting conservative percentages, prioritizing housing flexibility, and implementing income smoothing techniques, individuals can achieve housing stability without compromising financial security. This proactive mindset transforms rent from a liability into a manageable expense, even in the face of fluctuating earnings.

Discover the Average Rental Prices in Herington, Kansas

You may want to see also

Frequently asked questions

This refers to the proportion of your income before taxes that you spend on rent. It's calculated by dividing your monthly rent by your monthly pre-tax income and multiplying by 100.

A common rule of thumb is the 30% rule, which suggests spending no more than 30% of your pre-tax income on rent. However, this may vary depending on individual circumstances, location, and personal financial goals.

To calculate this percentage, divide your monthly rent by your monthly pre-tax income, then multiply the result by 100. For example, if your monthly rent is $1,200 and your monthly pre-tax income is $4,000, the calculation would be: ($1,200 ÷ $4,000) x 100 = 30%.

If you're spending more than 30% of your pre-tax income on rent, consider exploring options to reduce housing costs, such as finding a more affordable rental, getting a roommate, or negotiating rent with your landlord. Additionally, review your budget to identify areas where you can cut expenses or increase income to better manage your finances.