The issue of rent affordability and timely payments has become a pressing concern in the United States, with many Americans struggling to keep up with rising housing costs. As of recent data, a significant portion of renters are facing challenges in meeting their monthly obligations, leading to questions about what percentage of Americans are late on rent. Factors such as stagnant wages, increasing living expenses, and economic uncertainties have contributed to this growing trend, prompting a closer examination of the financial strain experienced by renters across the country. Understanding the scope of this problem is crucial for policymakers, landlords, and tenants alike, as it highlights the need for sustainable solutions to address housing affordability and financial stability.

Explore related products

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)

What You'll Learn

- Regional Variations: Rent delinquency rates differ significantly across states and cities in the U.S

- Economic Impact: High rent burdens correlate with increased late payments among American households

- Demographic Trends: Younger and lower-income renters are more likely to fall behind on rent

- Pandemic Effects: COVID-19 exacerbated late rent payments due to job losses and financial strain

- Policy Influence: Government assistance programs reduce late rent percentages during economic downturns

![]()

Regional Variations: Rent delinquency rates differ significantly across states and cities in the U.S

Rent delinquency rates in the U.S. are not uniform; they fluctuate dramatically based on regional economic conditions, housing markets, and local policies. For instance, states like New York and California, with high living costs and competitive rental markets, often report higher percentages of late rent payments compared to more affordable states like Indiana or Ohio. This disparity highlights the importance of analyzing regional data to understand the full picture of rental challenges across the country.

Consider the impact of local economies on rent delinquency. In cities heavily reliant on tourism, such as Las Vegas or Orlando, renters may face higher instability due to seasonal employment fluctuations. Conversely, tech hubs like Seattle or Austin, with robust job markets, tend to have lower delinquency rates. However, even within these cities, disparities exist—renters in gentrifying neighborhoods may struggle more than those in stable, suburban areas. To mitigate risk, landlords in volatile regions could offer flexible payment plans or rent stabilization programs tailored to local economic conditions.

A comparative analysis reveals that states with strong tenant protections, like Oregon and Washington, sometimes experience lower delinquency rates despite high rents. These protections, such as rent control or eviction moratoriums, provide renters with greater financial security. In contrast, states with fewer protections, like Texas or Georgia, may see higher delinquency rates, even with lower average rents. Policymakers can learn from these examples by implementing measures that balance landlord interests with tenant stability, such as emergency rental assistance programs or mandatory grace periods for late payments.

Descriptively, the Northeast and West Coast often dominate headlines for high rent burdens, but the South and Midwest present their own challenges. In Southern states, lower wages and limited public transportation can strain renters, even with cheaper housing. Midwestern cities, while more affordable, may lack job opportunities, leading to inconsistent income for renters. Addressing these regional nuances requires localized solutions, such as wage increases in the South or economic diversification in the Midwest, to reduce delinquency rates effectively.

Finally, a persuasive argument can be made for the need to invest in regional housing solutions. High delinquency rates in areas like Miami or Phoenix, where rapid population growth outpaces housing supply, underscore the urgency of increasing affordable housing stock. Similarly, rural areas with aging housing infrastructure and limited rental options need targeted investments to prevent delinquency. By allocating resources based on regional needs, policymakers and developers can create sustainable housing ecosystems that reduce late rent payments and improve financial stability for millions of Americans.

Sell or Rent Your Flat: Pros, Cons, and Smart Decisions

You may want to see also

Explore related products

![]()

Economic Impact: High rent burdens correlate with increased late payments among American households

A staggering 30-40% of American renters consistently face rent burdens, spending over 30% of their income on housing. This financial strain directly correlates with a concerning trend: late rent payments. As rent consumes a larger portion of household budgets, families are forced to make difficult choices, often prioritizing essentials like food and healthcare over timely rent payments.

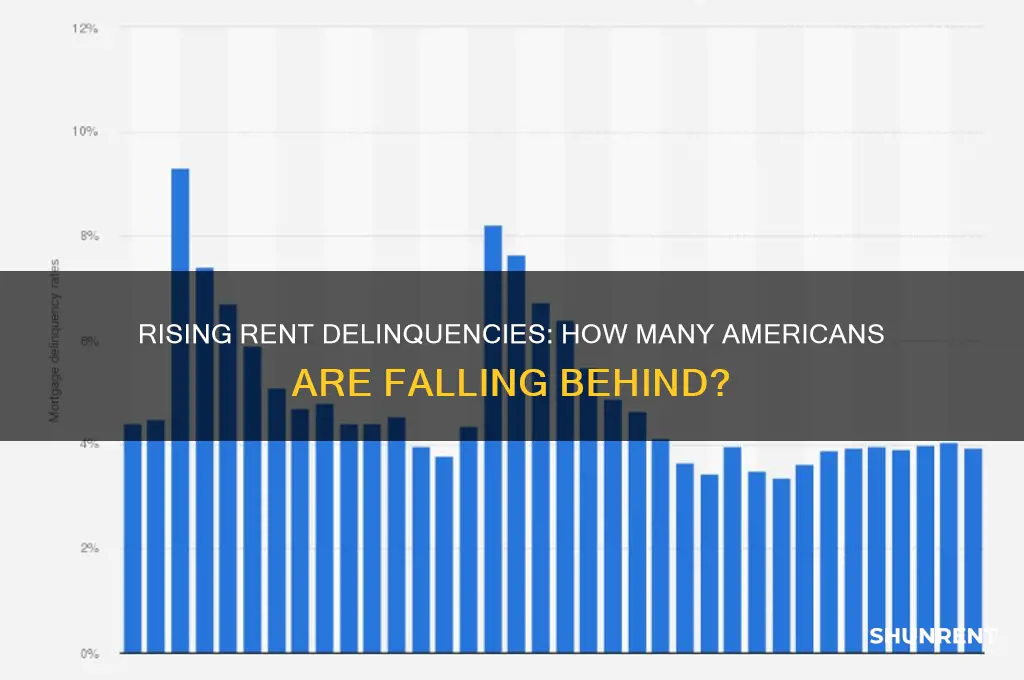

Data from the Census Bureau's Household Pulse Survey reveals a stark reality. In 2023, approximately 15% of renters reported being behind on rent, with low-income households disproportionately affected. This translates to millions of families living with the constant stress of potential eviction and the long-term consequences of damaged credit scores.

The economic impact of this crisis extends far beyond individual households. Landlords, reliant on consistent rent payments, face financial instability and may be forced to raise rents further, perpetuating the cycle. This ripple effect can lead to decreased consumer spending in local communities, impacting businesses and potentially leading to job losses.

Imagine a single mother working two jobs, earning just above minimum wage. With rent consuming 50% of her income, a single unexpected expense – a car repair, a medical bill – can easily push her into late payment territory. This scenario isn't hypothetical; it's the lived reality for countless Americans.

Breaking this cycle requires a multi-pronged approach. Increasing the availability of affordable housing units is crucial, coupled with rent control measures in high-cost areas. Expanding access to rental assistance programs and strengthening tenant protections can provide much-needed relief. Additionally, promoting financial literacy and budgeting skills can empower renters to manage their finances more effectively. Addressing the root causes of high rent burdens is essential for ensuring housing stability and mitigating the economic fallout of late rent payments.

Renting a Kayoko at Madison Memorial Terrace: A Simple Guide

You may want to see also

![]()

Demographic Trends: Younger and lower-income renters are more likely to fall behind on rent

Recent data reveals a stark disparity in rental payment punctuality across demographics, with younger and lower-income renters disproportionately struggling to keep up. According to a 2023 survey by the National Multifamily Housing Council, renters aged 18–34 are twice as likely to be late on rent compared to those over 55. Similarly, households earning below $30,000 annually report delinquency rates upwards of 20%, while those earning above $75,000 maintain rates below 5%. These figures underscore a systemic issue tied to age and income, demanding targeted solutions.

To address this trend, it’s critical to examine the root causes. Younger renters often face financial instability due to entry-level wages, student loan debt, and limited savings. For instance, the average monthly rent in the U.S. exceeds $1,500, while the median income for 22–29-year-olds hovers around $35,000 annually. This mismatch leaves little room for unexpected expenses, making timely rent payments a challenge. Lower-income households, meanwhile, are more vulnerable to economic shocks, such as job loss or medical emergencies, which can quickly derail financial stability.

Practical steps can mitigate these challenges. For younger renters, budgeting tools and financial literacy programs can help prioritize rent payments. Apps like Mint or YNAB offer real-time expense tracking, while workshops on debt management and savings strategies can empower this demographic. Lower-income renters may benefit from rental assistance programs, such as the Emergency Rental Assistance Program (ERAP), which provides up to 18 months of rent relief. Additionally, landlords can offer flexible payment plans or reduced late fees to ease the burden during temporary hardships.

A comparative analysis of successful interventions highlights the importance of collaboration. In cities like Minneapolis and Seattle, partnerships between local governments, nonprofits, and landlords have reduced eviction rates by 30%. These initiatives include rent subsidies, mediation services, and tenant protections. By replicating such models, communities can create a safety net for at-risk renters, ensuring housing stability while addressing the underlying economic disparities.

Ultimately, the demographic trend of younger and lower-income renters falling behind on rent is not just a statistic—it’s a call to action. Without intervention, this cycle perpetuates financial insecurity and widens the wealth gap. By implementing targeted support systems and fostering economic resilience, society can ensure that housing remains accessible to all, regardless of age or income. The solution lies in recognizing the unique challenges these groups face and crafting policies that meet them where they are.

Arnold Jackson's Age in 'Difficult Strokes': A Timeline Revealed

You may want to see also

![]()

Pandemic Effects: COVID-19 exacerbated late rent payments due to job losses and financial strain

The COVID-19 pandemic unleashed unprecedented financial strain on American households, with job losses and reduced income pushing many to the brink of eviction. According to a 2020 Census Bureau survey, nearly 14% of adult renters reported being behind on rent payments, a stark increase from pre-pandemic levels. This surge in late payments wasn’t merely a statistic—it was a reflection of millions of families grappling with sudden unemployment, reduced work hours, and the inability to meet basic financial obligations. The pandemic exposed the fragility of financial stability for a significant portion of the population, particularly those in low-wage industries like hospitality and retail, where layoffs were most severe.

Consider the mechanics of this crisis: When businesses shuttered due to lockdowns, millions lost their jobs overnight. For instance, the leisure and hospitality sector alone shed 8.2 million jobs in April 2020. Without a steady income, renters faced impossible choices—pay rent or cover essentials like food and medicine. Government stimulus checks and unemployment benefits provided temporary relief, but they were often insufficient to bridge the gap. A study by the Aspen Institute found that 30-40% of renters in major cities like New York and Los Angeles were at risk of eviction by the end of 2020, highlighting the depth of the crisis.

To mitigate this, policymakers implemented eviction moratoriums and rental assistance programs. However, these measures were often slow to reach those in need and were unevenly distributed across states. For example, while California allocated over $5 billion in rental assistance, many tenants faced bureaucratic hurdles and delays in receiving funds. This patchwork approach left countless renters vulnerable, with late payments accumulating and landlords facing their own financial pressures. The result? A cascading effect of economic instability that outlasted the immediate pandemic.

The long-term implications of this crisis are still unfolding. Even as the job market recovered, many renters struggled to clear arrears, with some owing thousands of dollars. A 2021 report by the National Low Income Housing Coalition revealed that 6.4 million renter households were behind on rent, totaling $34 billion in unpaid rent. This debt not only threatens individual financial health but also destabilizes the broader housing market. Landlords, particularly small property owners, faced mortgage defaults and maintenance challenges, further exacerbating the housing crisis.

Practical steps are needed to address this ongoing issue. Renters should explore local and federal rental assistance programs, such as the Emergency Rental Assistance Program (ERAP), which provides up to 18 months of rent and utility support. Tenants can also negotiate payment plans with landlords or seek legal aid to understand their rights under eviction moratoriums. For policymakers, the focus should be on streamlining assistance programs, increasing affordable housing investments, and creating long-term solutions to prevent future crises. The pandemic’s lesson is clear: financial resilience requires both individual action and systemic support.

Understanding Ontario's Rent-Geared-to-Income Calculation: A Comprehensive Guide

You may want to see also

![]()

Policy Influence: Government assistance programs reduce late rent percentages during economic downturns

Economic downturns often lead to a spike in late rent payments, as job losses and reduced income strain household budgets. However, data from the 2008 Great Recession and the COVID-19 pandemic reveal a critical trend: government assistance programs significantly mitigate this increase. For instance, during the pandemic, the Census Bureau’s Household Pulse Survey showed that late rent percentages dropped from 20% to 13% in households receiving stimulus checks or unemployment benefits. This underscores the direct correlation between targeted financial aid and housing stability during crises.

To understand the mechanism, consider the structure of programs like the Emergency Rental Assistance (ERA) program, which distributed over $46 billion to prevent evictions. By covering back rent and utilities, ERA not only reduced late payments but also alleviated the cascading financial pressures that often accompany rental delinquency. For example, a study by the Urban Institute found that households receiving ERA were 40% less likely to report being behind on rent compared to eligible non-recipients. This highlights the importance of timely, sufficient funding in policy design.

Critics often argue that such programs create dependency or misallocate resources, but evidence suggests otherwise. During the 2008 recession, the Temporary Assistance for Needy Families (TANF) program, when combined with state-level housing vouchers, reduced eviction rates by 25% in hard-hit areas like Detroit and Las Vegas. The key lies in pairing immediate relief with long-term support, such as job training or affordable housing initiatives. Without this dual approach, temporary aid risks becoming a band-aid solution rather than a bridge to stability.

Implementing effective assistance requires careful targeting and flexibility. For instance, the Pandemic Unemployment Assistance (PUA) program expanded eligibility to gig workers and freelancers, groups traditionally excluded from unemployment benefits. This inclusivity ensured that 8.5 million workers received aid, many of whom would have otherwise faced rent delinquency. Policymakers must prioritize such adaptive measures, especially as the gig economy grows and traditional safety nets fail to cover all workers.

In conclusion, government assistance programs are not just a moral imperative but a practical tool for reducing late rent percentages during economic downturns. By combining immediate financial relief with long-term support structures, these programs stabilize households and prevent the broader economic ripple effects of housing instability. As future crises loom, investing in such policies is not just a matter of compassion—it’s a strategic economic decision.

Affordable Bay Area Rentals: Smart Tips for Budget-Friendly Living

You may want to see also

Frequently asked questions

As of recent data, approximately 15-20% of American renters are late on rent payments, though this figure can fluctuate based on economic conditions and regional differences.

Common factors include job loss, unexpected expenses, rising housing costs, and economic downturns, with low-income households being disproportionately affected.

Late rent payments can lead to eviction, damage to credit scores, difficulty finding future housing, and increased financial stress for renters.