Determining what percentage of one's wage should go toward rent is a critical financial decision that balances housing affordability with overall financial stability. Financial experts commonly recommend the 30% rule, which suggests allocating no more than 30% of gross monthly income to rent, ensuring enough funds remain for other essentials like utilities, groceries, savings, and debt repayment. However, this guideline may not apply universally, as factors such as cost of living, personal financial goals, and regional housing market disparities can significantly influence affordability. For instance, in high-cost urban areas, renters might exceed this threshold, while in more affordable regions, they may allocate less. Ultimately, striking the right balance requires careful budgeting, prioritizing long-term financial health, and adjusting expenses to individual circumstances.

Explore related products

What You'll Learn

- Affordable Rent Thresholds: Define ideal rent-to-income ratios for financial stability and budgeting

- Regional Cost Variations: Explore how location impacts rent affordability across different cities/countries

- Budgeting Strategies: Tips for allocating wages to rent while covering other expenses

- Housing Market Trends: Analyze how market fluctuations affect rent affordability over time

- Government Assistance Programs: Overview of subsidies or policies aiding renters with high costs

![]()

Affordable Rent Thresholds: Define ideal rent-to-income ratios for financial stability and budgeting

A widely accepted rule of thumb suggests that no more than 30% of your gross monthly income should go toward rent. This guideline, often referred to as the 30% rule, stems from federal affordability standards and has become a benchmark for financial advisors and renters alike. However, this one-size-fits-all approach overlooks critical factors such as geographic cost of living, household size, and individual financial goals. For instance, in high-cost cities like San Francisco or New York, renters often exceed this threshold, while in more affordable areas, staying below 25% might be feasible. Understanding the nuances behind this ratio is essential for tailoring it to your unique circumstances.

To achieve financial stability, consider a tiered approach based on income level and lifestyle. For low-income households, capping rent at 25% of income ensures sufficient funds for essentials like groceries, utilities, and transportation. Middle-income earners might aim for the traditional 30% mark, provided they prioritize savings and debt repayment. High-income individuals could allocate up to 35% if their financial goals include aggressive investments or luxury expenditures. For example, a single earner making $4,000 monthly should ideally spend no more than $1,200 on rent, while a dual-income household earning $8,000 could afford $2,400 without compromising other financial priorities.

Budgeting for rent requires more than just adhering to a percentage; it demands a holistic view of your financial health. Start by calculating your net income after taxes and mandatory deductions. Subtract fixed expenses like insurance, loans, and childcare to determine your disposable income. Allocate rent within the recommended threshold, then prioritize savings (aim for 20% of income) and discretionary spending. For instance, if your net monthly income is $3,500, a $1,050 rent payment (30%) leaves $2,450 for other expenses. Automating savings and using budgeting apps can help maintain discipline and ensure rent doesn’t overshadow long-term financial goals.

Critics argue that rigid rent-to-income ratios fail to account for regional disparities and personal priorities. In cities where rent consumes 40-50% of income, residents often sacrifice savings or rely on roommates to stay afloat. Conversely, rural dwellers might spend as little as 20%, freeing up funds for travel or investments. To navigate these variations, consider the 50/30/20 rule: 50% for needs (including rent), 30% for wants, and 20% for savings and debt. Adjusting these categories based on local costs and personal values provides a more flexible framework than relying solely on rent percentages.

Ultimately, the ideal rent-to-income ratio is not a fixed number but a dynamic range informed by your financial situation and goals. For young professionals prioritizing career growth in expensive cities, exceeding 30% might be temporary and strategic. Families seeking stability may opt for lower ratios to accommodate education or retirement savings. Regularly reassess your budget as income, expenses, and priorities evolve. By balancing affordability with flexibility, you can ensure rent remains a stepping stone to financial stability rather than a barrier.

Understanding Rent-A-Center's Interest Rates: What You Need to Know

You may want to see also

Explore related products

![]()

Regional Cost Variations: Explore how location impacts rent affordability across different cities/countries

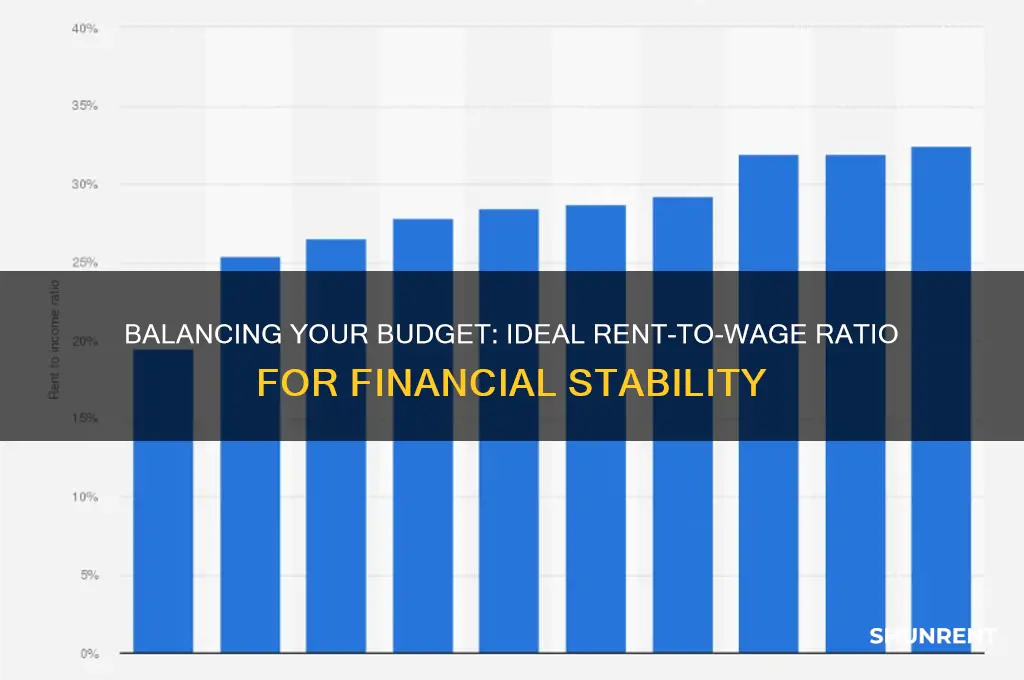

The 30% rule, a widely cited guideline suggesting that rent should consume no more than 30% of one's income, crumbles under the weight of regional cost variations. In San Francisco, where the median rent hovers around $3,700, a household would need to earn over $148,000 annually to adhere to this rule. Contrast this with Tulsa, Oklahoma, where median rent is roughly $850, allowing a household earning $34,000 to comfortably meet the 30% threshold. This stark disparity highlights how location dictates affordability, rendering blanket guidelines impractical.

Consider the global perspective. In Tokyo, Japan, despite its reputation for high living costs, efficient public transportation and compact living spaces allow many residents to allocate closer to 25% of their income to rent. Conversely, in Mumbai, India, where housing supply struggles to keep pace with demand, it's not uncommon for households to spend upwards of 50% of their income on rent. These examples underscore the interplay between local economies, housing policies, and cultural norms in shaping rent affordability.

To navigate these variations, adopt a location-specific approach. Start by researching the median rent-to-income ratio for your target city or country. For instance, in Berlin, Germany, where rent control measures are stringent, the ratio typically falls between 20-25%. Next, factor in ancillary costs unique to the region—utilities in Scandinavian countries, for example, are often included in rent, whereas in the U.S., tenants frequently bear these expenses separately. Finally, leverage local resources: in Singapore, the Housing and Development Board offers subsidized housing, while in New York City, rent stabilization laws cap annual increases.

A cautionary note: relying solely on global averages can lead to misinformed decisions. For instance, while the average rent-to-income ratio in the U.S. is around 28%, this figure masks extreme variations—from 18% in Wichita, Kansas, to 45% in Miami, Florida. Instead, drill down to neighborhood-level data. In London, rent in Zone 1 can easily consume 50% of a median income, whereas Zone 4 offers more affordable options at around 30%. Similarly, in Sydney, Australia, suburbs like Parramatta provide a more budget-friendly alternative to the central business district.

Ultimately, understanding regional cost variations empowers individuals to make informed decisions. For expatriates, this might mean negotiating a higher housing allowance in cities like Hong Kong, where rent can exceed 70% of income for some. For locals, it could involve relocating to adjacent areas with lower costs—a strategy increasingly adopted in cities like Austin, Texas, where urban sprawl has created pockets of affordability. By tailoring the rent-to-income ratio to local realities, individuals can achieve financial stability without sacrificing quality of life.

Evicting Tenants in Washington: A Step-by-Step Legal Guide for Landlords

You may want to see also

Explore related products

![]()

Budgeting Strategies: Tips for allocating wages to rent while covering other expenses

A common rule of thumb suggests allocating 30% of your gross income to rent, but this guideline often falls short in high-cost-of-living areas or for individuals with significant debt. For instance, in cities like San Francisco or New York, renters frequently spend closer to 50% of their income on housing, leaving little room for other essentials. This disparity highlights the need for a more flexible, personalized approach to budgeting. Instead of rigidly adhering to a one-size-fits-all percentage, consider your unique financial landscape, including income, debt, and lifestyle needs, to determine a sustainable rent allocation.

To effectively allocate wages to rent while covering other expenses, start by prioritizing needs over wants. Housing, food, and utilities are non-negotiable, while discretionary spending like dining out or entertainment should be adjusted based on your budget. For example, if your rent consumes 40% of your income, reduce non-essential expenses by cooking at home or canceling subscription services. Tools like the 50/30/20 rule—allocating 50% to needs, 30% to wants, and 20% to savings—can provide a framework, but adjust these ratios to fit your reality.

Another critical strategy is to build an emergency fund before committing to a high rent. Aim to save at least three to six months’ worth of living expenses in a liquid account. This buffer ensures that unexpected costs, such as car repairs or medical bills, don’t force you to sacrifice rent payments or accumulate debt. For instance, if your monthly expenses total $3,000, strive to save $9,000 to $18,000 before signing a lease that pushes your rent allocation above 30%.

For those struggling to balance rent with other expenses, consider alternative housing arrangements. Sharing a space with roommates, renting in a less expensive neighborhood, or negotiating rent with your landlord can significantly reduce housing costs. For example, moving from a studio in a downtown area to a shared apartment in a nearby suburb could cut rent by 20–30%, freeing up funds for savings or debt repayment. Similarly, offering to sign a longer lease or handle minor property maintenance might incentivize a landlord to lower your monthly payment.

Finally, leverage budgeting apps and spreadsheets to track spending and identify areas for adjustment. Apps like Mint or YNAB allow you to categorize expenses, set spending limits, and monitor progress toward financial goals. For instance, if you notice that 15% of your income goes to dining out, redirect half of that amount to savings or debt repayment. By visualizing your spending habits, you can make informed decisions about rent allocation and ensure it aligns with your broader financial priorities.

Ohio Boat Rental Age Requirements: What You Need to Know

You may want to see also

Explore related products

$61.95 $32

![]()

Housing Market Trends: Analyze how market fluctuations affect rent affordability over time

The 30% rule, a widely accepted guideline suggesting that individuals should allocate no more than 30% of their gross income to housing costs, has been a cornerstone of financial planning for decades. However, this rule is increasingly being challenged by volatile housing market trends that affect rent affordability. In cities like San Francisco and New York, where median rents exceed $3,000 per month, even dual-income households earning above the national median struggle to adhere to this benchmark. Market fluctuations, driven by factors like supply shortages, rising construction costs, and shifting migration patterns, have pushed rent-to-income ratios beyond sustainable levels for many. For instance, in 2022, renters in Miami saw a 25% year-over-year rent increase, forcing households to allocate closer to 40-50% of their income to housing, far surpassing the 30% threshold.

Analyzing historical data reveals a cyclical pattern in rent affordability, often tied to broader economic conditions. During the 2008 housing crisis, rents in many areas stabilized or even declined as homeowners turned to renting, increasing supply. Conversely, the post-pandemic recovery saw a surge in demand for rental units, coupled with a slowdown in new construction, driving rents upward. For example, in Austin, Texas, rents increased by 40% between 2020 and 2022, outpacing wage growth by a significant margin. This disparity highlights how market fluctuations can erode affordability, even in regions previously considered affordable. Policymakers and renters alike must monitor these trends to anticipate when rent burdens may become unsustainable.

To navigate these fluctuations, renters should adopt a dynamic approach to budgeting rather than rigidly adhering to the 30% rule. Start by tracking local rent trends using tools like Zillow or Apartment List to gauge whether your area is experiencing rapid growth. If rents are rising faster than wages, consider negotiating lease terms, such as longer-term contracts with capped annual increases, to stabilize costs. Additionally, explore secondary income streams or remote work opportunities that allow relocation to more affordable markets. For instance, a software engineer in Seattle might save $500 monthly by relocating to Phoenix, where rents are 30% lower but wages remain competitive.

A comparative analysis of global markets offers further insights into mitigating rent affordability challenges. In cities like Berlin, rent control policies have kept increases in check, ensuring that housing remains accessible to lower-income residents. Conversely, in Toronto, a lack of such regulations has led to rents consuming 50% or more of the average worker’s income. While policy changes are beyond individual control, renters can advocate for reforms like rent stabilization or increased housing supply. Simultaneously, building an emergency fund equivalent to 3-6 months of rent can provide a buffer during periods of rapid market shifts.

Ultimately, understanding how market fluctuations impact rent affordability requires a proactive and informed approach. Instead of relying solely on static guidelines, renters must adapt to local conditions, leveraging data and strategic planning to maintain financial stability. For young professionals or families in high-cost areas, this might mean prioritizing shared housing or suburban locations with lower rents. By staying ahead of trends and making data-driven decisions, individuals can ensure that their housing costs remain manageable, even in the face of unpredictable market dynamics.

Renting After Foreclosure: Overcoming Challenges and Securing Your Next Home

You may want to see also

Explore related products

![]()

Government Assistance Programs: Overview of subsidies or policies aiding renters with high costs

A common rule of thumb suggests that renters should allocate no more than 30% of their gross income to housing costs. However, skyrocketing rents in many urban areas have made this benchmark unattainable for millions. Government assistance programs step in to bridge this affordability gap, offering subsidies and policies designed to ease the burden on low- to moderate-income households. These initiatives vary widely in scope, eligibility, and impact, but they share a common goal: ensuring that housing remains accessible despite escalating costs.

One of the most well-known programs is the Housing Choice Voucher Program, colloquially known as Section 8. Administered by the U.S. Department of Housing and Urban Development (HUD), this initiative provides eligible families with vouchers to cover the difference between 30% of their income and the rent of a privately owned unit. For example, a family earning $30,000 annually would pay $750 per month (30% of $30,000), with the voucher covering the remainder of the rent up to a predetermined fair market value. While effective, long waitlists and limited funding often restrict access, leaving many in need without assistance.

Another critical tool is the Low-Income Housing Tax Credit (LIHTC) program, which incentivizes private developers to build affordable rental units. By offering tax credits to investors, the program reduces construction costs, allowing rents to be set at levels affordable to households earning 60% or less of the area median income. For instance, in a city with a median income of $60,000, a family of four earning $36,000 or less could qualify for reduced rent in a LIHTC property. This approach not only increases the supply of affordable housing but also fosters public-private partnerships to address the crisis.

State and local governments also play a pivotal role through initiatives like rent control and tenant-based rental assistance programs. Rent control policies, implemented in cities like New York and San Francisco, cap annual rent increases to prevent displacement. However, critics argue that such measures can reduce the availability of rental units over time. Meanwhile, tenant-based programs, such as California’s Housing Choice Voucher Program, provide direct financial aid to renters, often tailored to local cost-of-living indices. These localized efforts highlight the importance of context-specific solutions in addressing housing affordability.

Despite their benefits, government assistance programs face challenges such as underfunding, administrative inefficiencies, and eligibility gaps. For instance, HUD’s budget for rental assistance covers only a fraction of eligible households, leaving millions on waitlists. Policymakers must address these shortcomings by increasing funding, streamlining application processes, and expanding eligibility criteria to include more working-class families. Without such reforms, the goal of making housing affordable for all will remain elusive. By strengthening these programs, governments can ensure that the percentage of income spent on rent aligns with sustainable living standards, rather than forcing households into financial instability.

Filing Taxes as a Booth Renter: A Salon Professional's Guide

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent.

Not necessarily. The 30% rule is a general guideline, but individual circumstances, such as location, income, and other expenses, may require adjustments.

In high-cost areas, you may need to allocate more than 30% to rent. Consider budgeting carefully, finding roommates, or exploring more affordable neighborhoods.

The 30% rule typically uses gross income (before taxes), but it’s also important to ensure your rent fits comfortably within your net income after expenses.

If your rent exceeds 30%, consider reducing other expenses, increasing your income, or finding a more affordable living situation to avoid financial strain.