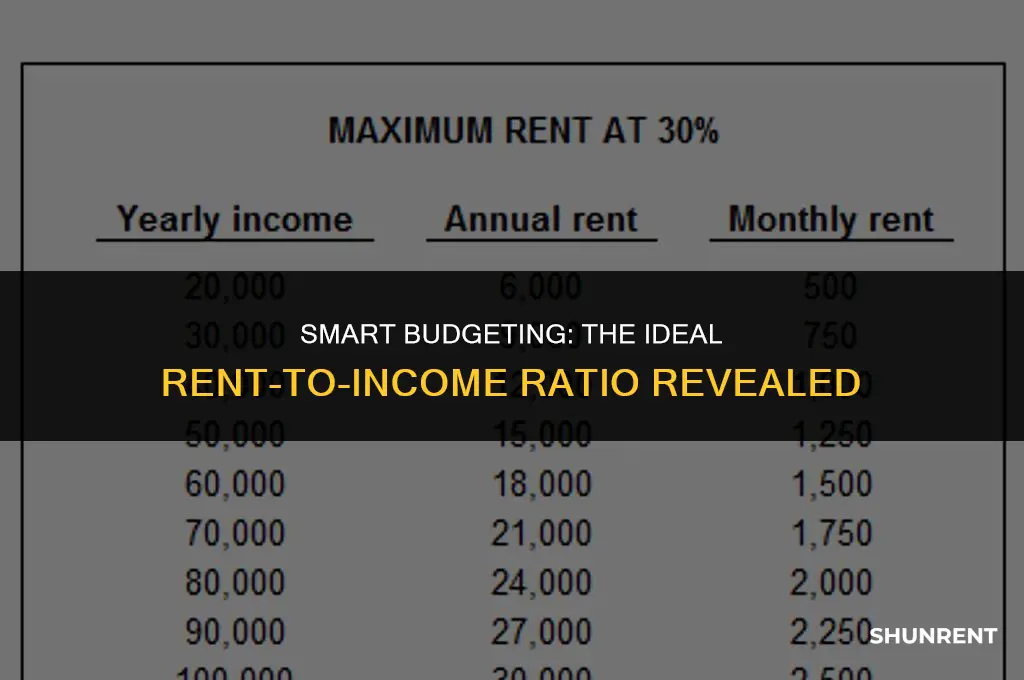

When it comes to budgeting for housing, understanding the ratio of rent to income is crucial. This ratio helps individuals and families determine how much they can afford to spend on rent each month based on their gross income. A general rule of thumb is the 30% rule, which suggests that rent should not exceed 30% of one's monthly income. However, this can vary depending on individual circumstances, such as debt obligations, savings goals, and other expenses. By calculating this ratio, one can ensure they are not overextending themselves financially and can maintain a balanced budget that accommodates all necessary expenditures.

Explore related products

What You'll Learn

- Ideal Rent-to-Income Ratio: Understanding the general guideline of 30% of income for rent

- Factors Affecting Rent Costs: Location, property type, and amenities influencing rental prices

- Calculating Rent Affordability: How to determine maximum affordable rent based on income and expenses

- Rent vs. Income Discrepancies: Strategies for managing when rent exceeds recommended income ratios

- Budgeting Tips for Renters: Effective ways to budget and save while renting, including utility costs

![]()

Ideal Rent-to-Income Ratio: Understanding the general guideline of 30% of income for rent

The 30% rent-to-income ratio is a widely accepted guideline that suggests renters should allocate no more than 30% of their gross income towards housing costs. This rule of thumb is designed to ensure that individuals have enough money left over for other essential expenses, savings, and discretionary spending. For example, if someone earns $5,000 per month, they should ideally spend no more than $1,500 on rent.

However, this guideline is not a one-size-fits-all solution. The ideal rent-to-income ratio can vary depending on individual circumstances, such as the cost of living in a particular area, the person's debt-to-income ratio, and their financial goals. In high-cost-of-living cities, it may be necessary to allocate a higher percentage of income towards rent in order to secure a suitable living space. Conversely, in areas with lower housing costs, renters may be able to get by with a lower rent-to-income ratio.

It's also important to consider the impact of other monthly expenses on the rent-to-income ratio. For instance, if someone has significant student loan payments or credit card debt, they may need to adjust their budget to accommodate these obligations. Additionally, renters should factor in the cost of utilities, internet, and other services when calculating their housing expenses.

To determine a personalized ideal rent-to-income ratio, individuals can use a budgeting tool or consult with a financial advisor. These resources can help renters assess their unique financial situation and create a budget that balances housing costs with other financial priorities. By taking a holistic approach to budgeting, renters can ensure that they are making informed decisions about their housing expenses and overall financial well-being.

Where to Post Irrigation Rent: Accounting Tips for Proper Allocation

You may want to see also

Explore related products

![]()

Factors Affecting Rent Costs: Location, property type, and amenities influencing rental prices

The cost of rent is a significant factor in determining the affordability of housing. Location is a primary driver of rental prices, with properties in urban centers and desirable neighborhoods commanding higher rents due to increased demand and limited supply. For instance, a one-bedroom apartment in a bustling city like New York or San Francisco can cost significantly more than a similar property in a smaller town or rural area. Proximity to public transportation, schools, and employment opportunities also plays a crucial role in influencing rental costs.

Property type is another key factor affecting rent prices. The size, layout, and condition of the property all contribute to its rental value. For example, a larger apartment with multiple bedrooms and bathrooms will typically cost more than a smaller studio or one-bedroom unit. Additionally, properties with modern amenities such as in-unit laundry, dishwashers, and air conditioning may command higher rents compared to those without such features. The age and maintenance status of the property can also impact rental costs, with newer or recently renovated buildings often being more expensive.

Amenities offered by the property or its surrounding area can further influence rental prices. Properties with access to swimming pools, gyms, and communal spaces may be more desirable and thus more expensive. Similarly, the presence of nearby parks, restaurants, and entertainment venues can increase the appeal of a property, leading to higher rents. On the other hand, properties located in areas with high crime rates or limited access to essential services may be less desirable and therefore less expensive.

When budgeting for rent, it is essential to consider these factors and how they impact the overall cost of living. A general rule of thumb is that rent should not exceed 30% of one's gross income, but this may vary depending on individual circumstances and the local housing market. By understanding the factors that influence rental prices, individuals can make informed decisions about their housing choices and ensure that they are allocating their budget effectively.

Ryder Beach Road Rental Inquiry: Is 45 Available for Lease?

You may want to see also

Explore related products

![]()

Calculating Rent Affordability: How to determine maximum affordable rent based on income and expenses

To calculate rent affordability, you need to determine the maximum amount of rent you can pay based on your income and expenses. A common rule of thumb is the 30% rule, which suggests that you should spend no more than 30% of your gross income on rent. However, this rule may not be suitable for everyone, especially if you have high expenses or debt.

First, calculate your gross income by adding up all your sources of income, including your salary, bonuses, and any other income you receive. Next, calculate your net income by subtracting taxes, social security, and any other deductions from your gross income. This will give you a more accurate picture of how much money you have available to pay rent.

Once you have your net income, calculate your total monthly expenses, including utilities, transportation, food, and any other bills you have. Subtract your total expenses from your net income to determine how much money you have left over for rent. This amount should be your maximum affordable rent.

For example, if your net income is $4,000 per month and your total expenses are $2,500, you would have $1,500 left over for rent. This would be your maximum affordable rent, assuming you want to maintain a comfortable living standard and avoid financial stress.

It's important to note that this calculation is just a starting point. You may need to adjust your budget based on your individual circumstances, such as if you have high debt or if you're saving for a down payment on a house. Additionally, you should consider other factors, such as the location and quality of the rental property, when determining how much rent you can afford.

Master Your Rented Server: A Guide to Gaining Admin Access

You may want to see also

Explore related products

![]()

Rent vs. Income Discrepancies: Strategies for managing when rent exceeds recommended income ratios

Navigating the challenge of rent exceeding income is a common financial hurdle. The general rule of thumb is that rent should not surpass 30% of one’s gross income to maintain financial stability. However, in many urban areas, this ratio can be significantly higher, leading to financial strain. To manage this discrepancy, it’s essential to adopt strategic budgeting practices.

Firstly, reassess your budget to identify areas where expenses can be reduced. This might include cutting back on non-essential spending such as dining out, entertainment, and subscription services. By allocating more funds towards rent, you can better manage the higher costs while still maintaining some level of financial flexibility.

Another strategy is to explore additional income streams. This could involve taking on a part-time job, freelancing, or renting out a spare room in your apartment. Increasing your income can help bridge the gap between your rent and the recommended income ratio, providing more financial breathing room.

Negotiating with your landlord can also be a viable option. If you have a good relationship with your landlord and a history of timely payments, you may be able to discuss a rent reduction or a payment plan that better aligns with your income. It’s important to approach this conversation professionally and be prepared to provide documentation of your financial situation.

Lastly, consider seeking assistance from local housing programs or non-profit organizations that offer financial counseling and support. These resources can provide valuable guidance on managing high rent costs and may offer additional strategies tailored to your specific circumstances.

In conclusion, managing rent that exceeds recommended income ratios requires a proactive and multifaceted approach. By reassessing your budget, exploring additional income sources, negotiating with your landlord, and seeking professional assistance, you can develop a comprehensive strategy to handle this financial challenge effectively.

Florida Airbnb Age Requirements: What You Need to Know

You may want to see also

Explore related products

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![]()

Budgeting Tips for Renters: Effective ways to budget and save while renting, including utility costs

To effectively budget as a renter, it's crucial to understand the ideal rent-to-income ratio. Financial experts generally recommend that your rent should not exceed 30% of your gross income. This guideline helps ensure that you have enough money left over for other essential expenses, savings, and discretionary spending. For instance, if your monthly gross income is $4,000, your rent should ideally be no more than $1,200.

However, this ratio can vary based on individual circumstances. If you have significant debt or other financial obligations, you may need to allocate less than 30% of your income to rent. Conversely, if you're in a high-cost area or have a particularly high income, you might be able to comfortably afford a higher rent percentage.

When budgeting for rent, it's also important to consider utility costs. These can vary widely depending on the property and location, so it's wise to ask the landlord about average utility expenses before signing a lease. You may also want to look into energy-efficient practices to help reduce these costs, such as using LED light bulbs, sealing drafts, and investing in a programmable thermostat.

Another effective budgeting tip for renters is to prioritize saving. Set aside a portion of your income each month for an emergency fund, which can help cover unexpected expenses like car repairs or medical bills. Additionally, consider setting up automatic transfers to a savings account to make saving a habit.

Finally, be mindful of your spending habits. Track your expenses to identify areas where you can cut back, and avoid unnecessary purchases. By being proactive with your budget and mindful of your spending, you can better manage your finances while renting.

Fair Rent Splitting Strategies for Roommates with Varying Incomes

You may want to see also

Frequently asked questions

The general guideline for the rent-to-income ratio is that your monthly rent should not exceed 30% of your gross monthly income. This rule helps ensure that you have enough money left over for other essential expenses and savings.

To calculate your rent-to-income ratio, divide your monthly rent by your gross monthly income. For example, if your rent is $1,000 and your income is $3,500, your ratio would be approximately 28.6%, which falls within the recommended 30% guideline.

If your rent-to-income ratio exceeds 30%, consider the following factors: your overall budget and expenses, the cost of living in your area, your savings goals, and whether you have any high-interest debt. You may need to adjust your budget, look for ways to reduce expenses, or consider finding a more affordable living situation to maintain financial stability.

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)