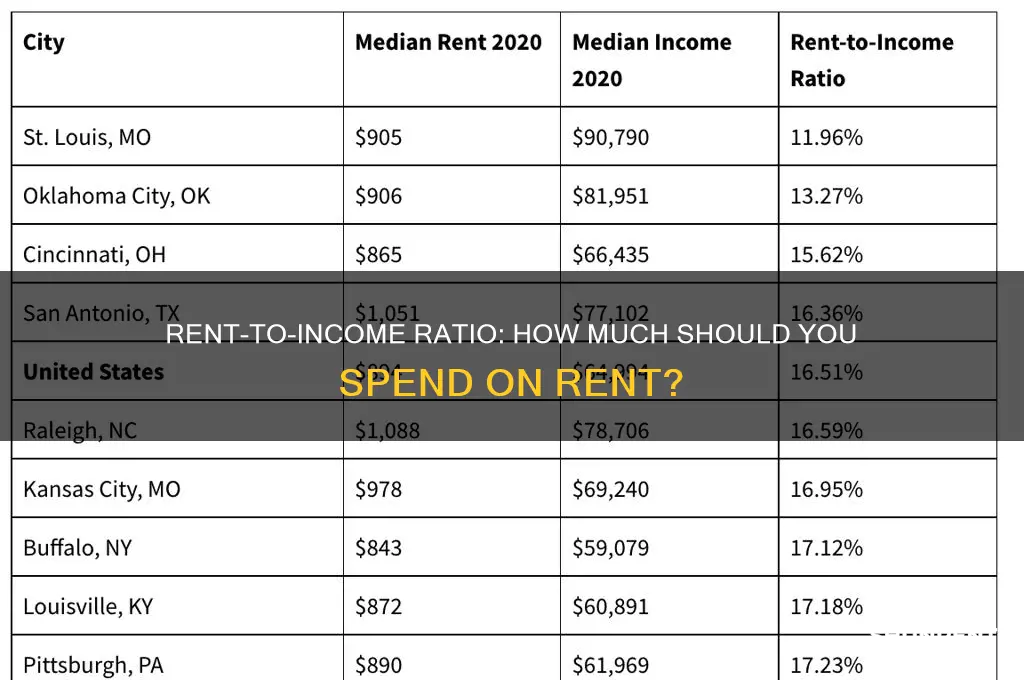

When considering renting a property, it’s crucial to evaluate the renting ratio in relation to your salary to ensure financial stability and avoid overextending your budget. A widely accepted guideline is the 30% rule, which suggests that your monthly rent should not exceed 30% of your gross monthly income. This ratio helps balance housing costs with other essential expenses, savings, and discretionary spending. However, this percentage may need adjustment based on factors such as your location, cost of living, and personal financial goals. For instance, in high-cost urban areas, renters might need to allocate a larger portion of their income to housing, while in more affordable regions, a lower ratio may be feasible. Understanding and adhering to a suitable renting ratio ensures that you maintain a healthy financial lifestyle while meeting your housing needs.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less of gross monthly income |

| Common Rule of Thumb | Spend no more than 1/3 of your monthly income on rent |

| Affordability Threshold | Rent should not exceed 30% of your pre-tax income |

| Median Rent-to-Income Ratio (US) | ~25-30% (varies by city and income level) |

| High-Cost Urban Areas | Ratios may exceed 30% due to higher rents |

| Low-Income Households | May spend >30% of income on rent, considered "rent-burdened" |

| Ideal Scenario | Aim for 25-28% to allow for savings and other expenses |

| Emergency Fund Consideration | Ensure rent doesn’t hinder building an emergency fund |

| Debt-to-Income Ratio | Rent should be factored into overall debt obligations (<36% recommended) |

| Regional Variations | Ratios differ by country/city; e.g., NYC avg. 40-50%, Midwest avg. 20-25% |

| Post-Tax Consideration | Some advisors suggest using post-tax income for a more accurate ratio |

| Housing Cost Burden | Spending >30% on rent is classified as cost-burdened by HUD (US) |

| Global Averages | Varies widely; e.g., UK avg. 35%, Germany avg. 25% |

| Minimum Wage Workers | Often spend 50-70% of income on rent in high-cost areas |

| Luxury Renting | High-income earners may allocate <20% for premium housing |

Explore related products

What You'll Learn

- Ideal Rent-to-Income Ratio: Aim for 30% or less of your monthly income on rent

- Budgeting for Rent: Allocate funds wisely to balance rent with other expenses effectively

- High Rent Impact: Exceeding 30% can strain finances, limiting savings and investments

- Location Influence: Urban areas often require higher rent ratios compared to rural regions

- Adjusting Lifestyle: Reduce non-essential spending if rent exceeds recommended salary percentage

![]()

Ideal Rent-to-Income Ratio: Aim for 30% or less of your monthly income on rent

Spending more than 30% of your monthly income on rent can quickly derail your financial stability. This widely accepted benchmark, often referred to as the 30% rule, stems from a 1981 amendment to the U.S. Housing and Urban Development (HUD) Act, which defined housing as "affordable" if it consumed no more than 30% of a household’s income. While this rule isn’t legally binding, it has become a standard for financial planners and renters alike. Exceeding this threshold leaves less room for savings, emergencies, and other essential expenses, increasing the risk of financial strain.

To apply the 30% rule, calculate your gross monthly income and multiply it by 0.3. For instance, if you earn $4,000 per month, your ideal rent should not exceed $1,200. However, this rule isn’t one-size-fits-all. High-cost-of-living areas like New York or San Francisco often force renters to spend closer to 50% of their income on housing. In such cases, prioritize cutting costs in other areas, like dining out or subscriptions, to maintain balance. Alternatively, consider roommates or relocating to a more affordable neighborhood.

Critics argue that the 30% rule fails to account for individual financial situations. For example, someone with significant student loans or medical debt may need to aim for an even lower rent-to-income ratio. Conversely, a high earner with minimal expenses might comfortably allocate more than 30% to rent without compromising financial goals. The key is to tailor the rule to your unique circumstances, ensuring it aligns with your overall budget and long-term objectives.

Practical tips for staying within the 30% threshold include negotiating rent, especially in competitive markets, and seeking out utilities-included rentals to reduce additional costs. If you’re consistently overspending on rent, reassess your housing priorities. Downsizing or moving further from city centers can significantly lower costs. Finally, track your spending using budgeting apps to ensure rent doesn’t overshadow other financial commitments. By adhering to the 30% rule—or a modified version suited to your needs—you can achieve a healthier balance between housing and overall financial well-being.

Renting Xfinity's 1000 Mbps Router: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Budgeting for Rent: Allocate funds wisely to balance rent with other expenses effectively

A common rule of thumb suggests that rent should not exceed 30% of your gross monthly income. This guideline, often referred to as the 30% rule, has been widely adopted as a benchmark for financial stability. However, this one-size-fits-all approach may not suit everyone's unique circumstances. For instance, a high-earning individual in an expensive city might comfortably allocate 40% of their salary to rent, while a low-income earner in a rural area could struggle with even 25%. The key is to assess your personal financial landscape and adjust this ratio accordingly.

Analyzing Your Financial Situation: Begin by calculating your monthly income after taxes and deductions. Then, list all essential expenses, including utilities, groceries, transportation, and insurance. Subtract these from your income to determine the remaining funds available for rent. For example, if your monthly take-home pay is $4,000, and essential expenses total $1,500, you have $2,500 left. Allocating 30% of your gross income ($1,200) to rent might be feasible, but consider if this leaves enough for savings, debt repayment, and leisure.

Prioritizing and Adjusting: Rent is a fixed expense, but it shouldn't dominate your budget. If the 30% rule seems unrealistic, consider these strategies: First, negotiate rent or explore cheaper accommodations. Second, increase your income through side hustles or salary negotiations. Third, reduce discretionary spending. For instance, cutting back on dining out or subscription services can free up funds. A 25-year-old professional might opt for a smaller apartment to save $200 monthly, allowing them to allocate more to student loan payments.

The Balancing Act: Effective budgeting is about trade-offs. If you're spending 35% of your income on rent, ensure other areas are optimized. Perhaps you cook at home, reducing grocery costs, or use public transport instead of owning a car. A family of four might choose a larger rental property, accepting a higher rent-to-income ratio, but saving on individual commuting costs. The goal is to create a sustainable budget where rent is a significant but not overwhelming expense.

Long-Term Financial Health: While managing rent is crucial, it's equally important to plan for the future. Ensure your budget includes savings for emergencies and retirement. Consider the 50/30/20 rule as an alternative: 50% for needs (including rent), 30% for wants, and 20% for savings and debt repayment. This approach provides a more comprehensive financial strategy. For instance, a young couple might allocate 35% to rent, 15% to entertainment, and 20% to savings, ensuring they build wealth while enjoying their current lifestyle.

Rent-to-Own Homes: Understanding the Timeline and Process

You may want to see also

Explore related products

![]()

High Rent Impact: Exceeding 30% can strain finances, limiting savings and investments

Spending more than 30% of your salary on rent pushes you into the "rent-burdened" category, a designation that carries significant financial consequences. This threshold, widely accepted by financial experts, isn't arbitrary. It's based on the understanding that housing is a necessity, but it shouldn't dominate your budget at the expense of other essential needs and long-term goals. Exceeding this ratio means less money for groceries, transportation, healthcare, and, crucially, savings and investments.

Imagine your monthly income as a pie chart. When rent slices off more than 30%, the remaining portions shrink dramatically. Savings for emergencies, retirement, or a down payment on a home become slivers, easily overlooked in the face of immediate expenses.

Let's illustrate with a scenario. Sarah, earning $4,000 monthly, spends $1,400 on rent (35% of her income). After taxes and other essentials, she's left with a mere $800 for discretionary spending and savings. This leaves little room for building an emergency fund, contributing to a 401(k), or even enjoying occasional leisure activities. Over time, this financial strain can lead to debt accumulation and a sense of financial insecurity.

In contrast, consider John, earning the same $4,000 but spending $1,000 on rent (25%). He has a more substantial $1,200 for savings and discretionary spending. This allows him to build a safety net, invest for the future, and enjoy a more balanced lifestyle.

The impact of exceeding the 30% threshold extends beyond immediate cash flow. It hinders long-term financial security. Without adequate savings, unexpected expenses become crises. Retirement planning gets pushed aside, potentially leading to reliance on limited social security benefits. The dream of homeownership fades as down payment savings remain stagnant.

To avoid this financial trap, prioritize finding housing that aligns with the 30% rule. Consider roommates, smaller spaces, or locations with lower rent. Negotiate rent whenever possible. Remember, sacrificing a bit of living space or convenience now can lead to greater financial freedom and security in the long run.

Claiming Renter's Income: A Step-by-Step Guide for Landlords

You may want to see also

Explore related products

![]()

Location Influence: Urban areas often require higher rent ratios compared to rural regions

Urban areas, with their bustling economies and vibrant cultures, often demand a larger slice of your paycheck for rent. This isn't just a hunch; it's a trend backed by data. A 2022 study by the Joint Center for Housing Studies at Harvard University found that renters in metropolitan areas spend, on average, 30% of their income on housing, compared to 25% in non-metropolitan areas. This disparity highlights a fundamental truth: location significantly influences the rent-to-income ratio.

Urban centers, with their concentrated job opportunities and amenities, attract a larger population, driving up demand for housing. This increased demand, coupled with limited land availability, leads to higher rents. Think of it as a bidding war for a limited resource – the more people vying for a scarce commodity, the higher the price climbs.

Consider the example of San Francisco, where the median rent for a one-bedroom apartment hovers around $3,700, according to Zumper's 2023 National Rent Report. This translates to a staggering 45% of the median household income being allocated to rent. In contrast, a similar apartment in a rural town like Springfield, Missouri, might rent for $800, consuming only 20% of the local median income. This stark contrast illustrates the direct correlation between urban density and rent burden.

However, it's not just about raw numbers. The "ideal" rent-to-income ratio is a moving target, influenced by individual circumstances and lifestyle choices. While the oft-cited 30% rule serves as a general guideline, it's crucial to factor in other expenses like transportation, childcare, and healthcare. A young professional in a high-paying job in New York City might comfortably manage a 40% rent ratio, while a family in a rural area with lower incomes might struggle with even 25%.

The key takeaway is this: when determining a sustainable rent ratio, location is paramount. Urban dwellers need to be prepared for a larger portion of their income going towards rent, while those in rural areas can generally expect a more favorable balance. Ultimately, the "right" ratio is the one that allows you to live comfortably within your means, factoring in both your income and the unique cost of living in your chosen location.

Top Money Transfer Apps for Seamless Rent Payments in 2023

You may want to see also

Explore related products

![]()

Adjusting Lifestyle: Reduce non-essential spending if rent exceeds recommended salary percentage

Rent should ideally consume no more than 30% of your gross monthly income, a guideline echoed by financial experts and housing authorities alike. When this threshold is breached, it’s a red flag signaling the need for immediate lifestyle adjustments. Non-essential spending becomes the first casualty in this recalibration, as discretionary expenses are the easiest to trim without compromising basic needs. Think of it as a financial diet: just as you’d cut empty calories to improve health, eliminating frivolous purchases can restore balance to your budget.

Start by categorizing your expenses into essentials (rent, utilities, groceries) and non-essentials (streaming subscriptions, dining out, impulse buys). A granular review of your bank statements over the past three months will reveal patterns of overspending. For instance, if you’re allocating $200 monthly to coffee shop visits or $50 to unused gym memberships, these are prime candidates for elimination. Tools like budgeting apps can automate this process, flagging recurring charges that don’t align with your revised financial priorities.

Next, adopt a mindset shift from ownership to access. Instead of buying books, borrow from libraries or use e-book subscriptions. Swap expensive gym memberships for free YouTube workouts or community fitness groups. Meal planning and cooking at home can slash grocery bills by 30–40%, while batch cooking ensures you’re not tempted by takeout on busy days. These changes aren’t about deprivation but about reallocating resources to where they matter most—your housing stability.

Finally, set clear, measurable goals to track progress. Aim to reduce non-essential spending by 20% in the first month, then reassess. If rent still exceeds the 30% mark, consider more drastic measures like downsizing or finding a roommate. Remember, adjusting your lifestyle isn’t a one-time fix but an ongoing practice. By prioritizing essentials and minimizing waste, you regain control over your finances and ensure rent doesn’t dictate your financial future.

Renting Out Your Duplex: A Guide to Listing One Unit Successfully

You may want to see also

Frequently asked questions

A healthy renting ratio is generally considered to be around 30% or less of your gross monthly income. This ensures you have enough left for other expenses and savings.

To calculate your renting ratio, divide your monthly rent by your gross monthly income and multiply by 100. For example, if your rent is $1,000 and your income is $4,000, your ratio is 25%.

While exceeding 30% is possible, it may strain your budget and limit your ability to save or cover unexpected expenses. Consider finding a more affordable rental or increasing your income if this is the case.

Yes, include all housing-related expenses like utilities, parking, and maintenance fees in your calculation to get a more accurate picture of your total housing costs relative to your salary.

A higher renting ratio leaves less room in your budget for savings, investments, or emergencies. Keeping your ratio below 30% helps ensure you can allocate funds to financial goals beyond just housing.