Determining the ideal percentage of your paycheck that should go toward rent is a crucial financial decision that balances housing needs with overall budget stability. Financial experts commonly recommend the 30% rule, which suggests allocating no more than 30% of your gross income to rent, ensuring enough funds remain for other essentials like utilities, groceries, savings, and debt repayment. However, this guideline may vary based on individual circumstances, such as location, income level, and personal financial goals. High-cost-of-living areas might require a higher percentage, while those with lower expenses or higher incomes may comfortably allocate less. Ultimately, striking the right balance ensures financial security and avoids the risk of becoming rent-burdened, where housing costs strain your ability to meet other financial obligations.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less |

| Source of Recommendation | U.S. Department of Housing and Urban Development (HUD) |

| Purpose of 30% Rule | Ensures affordability and financial stability |

| Factors Influencing Percentage | Income level, location, debt, savings goals |

| High-Cost Areas Adjustment | May require 40-50% in cities like NYC or SF |

| Low-Income Households | May need to spend closer to 25% or less |

| Debt Considerations | Lower percentage if high student loans/debt |

| Savings Goals Impact | Lower percentage if prioritizing savings |

| Alternative Budgeting Methods | 50/30/20 rule (30% on housing) |

| Latest Data Year | 2023 |

Explore related products

What You'll Learn

- Affordable Rent Percentage: Ideal rent-to-income ratio for financial stability and budgeting effectively

- /30/20 Rule Application: How this rule allocates income for needs, wants, and savings

- Local Cost Variations: Adjusting rent percentage based on city or region living costs

- Emergency Fund Impact: Balancing rent with savings for unexpected expenses or job loss

- Debt and Rent Trade-off: Managing student loans, credit cards, and rent within paycheck limits

![]()

Affordable Rent Percentage: Ideal rent-to-income ratio for financial stability and budgeting effectively

Determining the ideal rent-to-income ratio is crucial for maintaining financial stability and effective budgeting. A widely accepted rule of thumb is the 30% rule, which suggests that no more than 30% of your gross monthly income should go toward rent. For example, if your monthly income is $4,000, your rent should ideally not exceed $1,200. This guideline helps ensure that you have enough funds left for other essential expenses, savings, and discretionary spending. However, this percentage isn’t one-size-fits-all; it depends on individual financial circumstances, such as debt obligations, lifestyle, and long-term financial goals.

Analyzing the 30% rule reveals its practicality but also its limitations. For instance, in high-cost-of-living areas like New York or San Francisco, adhering to this ratio can be nearly impossible for many residents. In such cases, a more realistic approach might be to aim for a higher percentage, such as 40%, while aggressively cutting costs in other areas. Conversely, in more affordable regions, keeping rent below 25% of income could allow for greater savings or investment opportunities. The key is to balance housing costs with other financial priorities, ensuring that rent doesn’t become a burden that compromises your overall financial health.

To effectively budget with rent as a significant expense, start by calculating your net income after taxes and deductions. Then, allocate funds for fixed expenses like utilities, insurance, and debt payments. Next, prioritize savings, aiming to set aside at least 10–15% of your income for emergencies and long-term goals. Finally, allocate the remaining funds for variable expenses like groceries, entertainment, and transportation. By structuring your budget this way, you can ensure that rent fits comfortably within your financial plan without overshadowing other critical areas.

A persuasive argument for sticking to a lower rent-to-income ratio is its impact on financial freedom. High rent payments can limit your ability to save for milestones like homeownership, retirement, or education. For young professionals or families, keeping rent below 30% of income can provide a safety net during unexpected financial setbacks. Additionally, it allows for flexibility in pursuing career changes, relocating, or investing in personal development without being tethered to a high housing cost. Prioritizing affordability in housing is not just about saving money—it’s about building a foundation for long-term financial resilience.

In conclusion, while the 30% rule serves as a helpful starting point, the ideal rent-to-income ratio should be tailored to your unique financial situation. Practical steps include assessing your income, expenses, and goals, and adjusting your housing budget accordingly. Whether you’re in an expensive city or a more affordable area, the goal is to strike a balance that supports both your current needs and future aspirations. By doing so, you can ensure that rent remains a manageable part of your budget, paving the way for greater financial stability and peace of mind.

Philadelphia: Renting Event Spaces and Halls

You may want to see also

Explore related products

![]()

50/30/20 Rule Application: How this rule allocates income for needs, wants, and savings

Rent, a cornerstone of living expenses, often consumes a significant portion of our income. The 50/30/20 rule offers a structured approach to budgeting, ensuring rent fits within a balanced financial plan. This rule divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Rent, as a fundamental need, falls squarely within the 50% allocation.

For individuals and families, this means rent should ideally not exceed half of your take-home pay. For example, if your monthly after-tax income is $4,000, rent should not surpass $2,000. This guideline promotes financial stability by preventing housing costs from overwhelming your budget.

However, the 50/30/20 rule isn't a rigid formula. It's a starting point for thoughtful budgeting. Consider factors like local cost of living, household size, and individual circumstances. In high-rent areas, adhering strictly to 50% might be unrealistic. In such cases, adjustments may be necessary, potentially reducing the percentage allocated to wants or increasing income through side hustles. Conversely, in more affordable regions, you might aim for a lower rent-to-income ratio, freeing up funds for savings or other needs.

Flexibility is key. The 50/30/20 rule provides a framework, but personalization is crucial for success.

To effectively apply this rule to rent, start by calculating your after-tax income. Then, determine your maximum rent budget based on the 50% allocation. Research rental options within this range, considering factors like location, amenities, and lease terms. Remember, rent isn't the only need within the 50% category. Utilities, groceries, transportation, and insurance also fall under this umbrella. Prioritize essential expenses and allocate funds accordingly.

By incorporating the 50/30/20 rule into your budgeting, you gain control over your finances. It encourages mindful spending, prioritizes savings, and helps prevent rent from becoming a financial burden. While adjustments may be needed based on individual circumstances, this rule provides a valuable roadmap for achieving financial stability and security.

Understanding NYC Commercial Rent Tax: A Step-by-Step Calculation Guide

You may want to see also

Explore related products

![]()

Local Cost Variations: Adjusting rent percentage based on city or region living costs

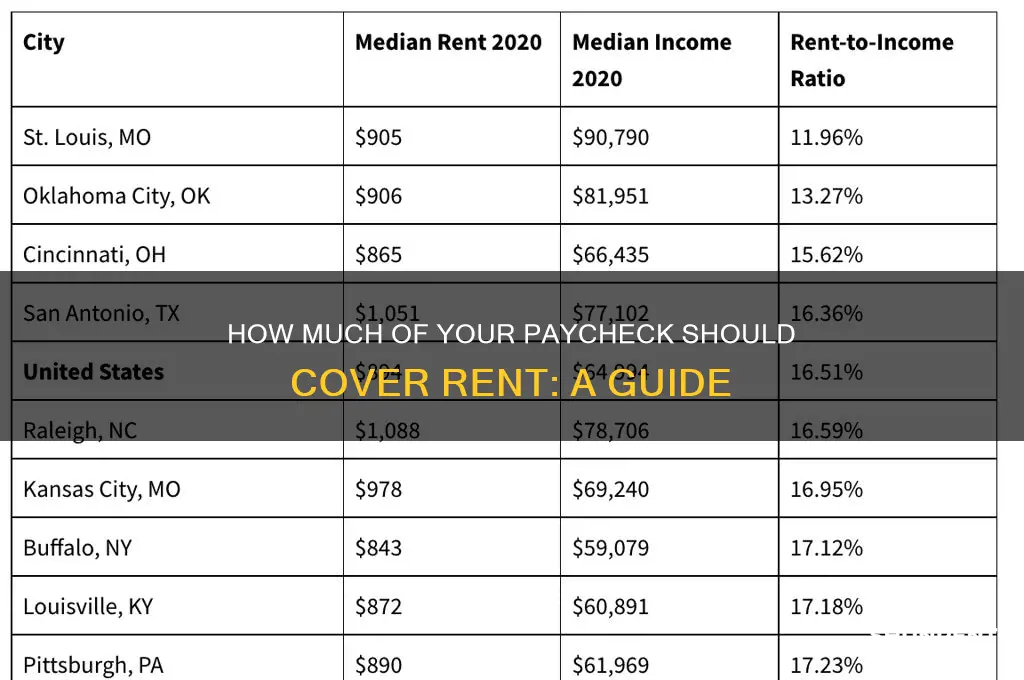

Rent should never be a one-size-fits-all calculation. The oft-cited "30% rule" – spending no more than 30% of your income on housing – crumbles under the weight of geographic reality. In San Francisco, where the median rent hovers around $3,700, even a household earning $100,000 annually would struggle to adhere to this guideline. Conversely, in Tulsa, Oklahoma, where median rent is a mere $850, that same 30% rule might leave you with a spacious apartment and a hefty surplus.

This disparity demands a localized approach. Consider a young professional earning $50,000 annually. In Austin, Texas, where rent averages $1,500, allocating 30% of their income ($1,250) would be feasible. However, in New York City, where the average rent surpasses $3,000, that same percentage would be unsustainable. A more realistic approach in NYC might involve aiming for 40-45% of income for rent, coupled with strategic budgeting in other areas.

Pro Tip: Utilize online cost-of-living calculators to compare housing expenses across cities. Websites like Numbeo and Expatistan provide detailed breakdowns, allowing you to adjust your rent percentage expectations accordingly.

The challenge lies in balancing affordability with lifestyle. While a lower rent percentage is ideal, it shouldn't come at the expense of other necessities or long-term financial goals. In high-cost cities, consider shared housing arrangements, exploring outlying neighborhoods with better affordability, or negotiating rent with landlords. Conversely, in lower-cost areas, prioritize saving or investing the surplus rather than simply upgrading to a more expensive apartment.

Caution: Don't fall into the trap of comparing your rent percentage to friends or family in different locations. Their financial circumstances and local costs are likely vastly different.

Ultimately, the ideal rent percentage is a dynamic figure, constantly shifting based on your location and individual circumstances. By acknowledging local cost variations and adopting a flexible approach, you can ensure that your housing expenses remain manageable and aligned with your overall financial well-being. Remember, the 30% rule is a starting point, not a rigid mandate. Tailor it to your reality, and you'll navigate the rental market with greater confidence and financial security.

Parkrose Hardware Chipper Rentals: Types and Availability Explained

You may want to see also

Explore related products

![]()

Emergency Fund Impact: Balancing rent with savings for unexpected expenses or job loss

Rent typically consumes 30% of take-home pay, a guideline echoed by financial experts and housing authorities. But this benchmark assumes stability—steady income, predictable expenses, and no major disruptions. Reality often diverges, particularly when emergencies strike. A sudden job loss, medical crisis, or car repair can upend this delicate balance, turning a manageable rent burden into a financial freefall. This is where the emergency fund enters as a critical counterweight, a buffer against the unexpected.

Consider the math: if 30% of your income goes to rent, allocating another 10–20% toward savings might feel like a stretch. Yet, this dual commitment is non-negotiable for long-term resilience. For instance, saving $200 monthly on a $4,000 income (5%) could take 20 months to build a $4,000 emergency fund—enough to cover three months of rent and essentials. Accelerating this timeline requires trade-offs: reducing discretionary spending, negotiating lower rent, or temporarily downsizing. The goal isn’t to eliminate rent’s share but to ensure it doesn’t dominate your financial landscape at the expense of preparedness.

The psychological impact of this balance cannot be overstated. Knowing you have a safety net reduces stress during emergencies, enabling clearer decision-making. For example, someone with a $5,000 emergency fund might confidently negotiate a severance package or take time to find a better job rather than rushing into a lower-paying role to cover rent. Conversely, without savings, a single missed paycheck can lead to eviction, debt, or reliance on high-interest loans, compounding financial strain.

Practical strategies include automating savings to make the process painless. Treat your emergency fund contribution like a fixed bill, transferring funds immediately after payday. If rent exceeds 30% of your income, explore housing alternatives—shared living, rent-controlled units, or relocating to a lower-cost area. Simultaneously, increase income through side gigs or skill-based freelancing to expand your savings capacity without sacrificing rent payments. The key is to view rent and emergency savings as interdependent priorities, not competing demands.

Ultimately, the 30% rent rule is a starting point, not a rigid mandate. Its effectiveness hinges on pairing it with a robust emergency fund. Aim to save 3–6 months’ worth of living expenses, adjusting based on job security, health, and family obligations. This dual focus transforms rent from a potential liability into a manageable expense, ensuring financial stability even when life takes an unexpected turn.

Land Contract vs. Rent-to-Own: Which Option Costs More?

You may want to see also

Explore related products

![]()

Debt and Rent Trade-off: Managing student loans, credit cards, and rent within paycheck limits

Balancing rent, student loans, and credit card payments on a limited paycheck requires strategic prioritization. The 30% rule—spending no more than 30% of your income on rent—is a widely cited guideline, but it falters when other debts consume a significant portion of your budget. For instance, if 20% of your paycheck goes to student loans and another 10% to credit card minimums, adhering strictly to the 30% rule might leave you struggling to cover essentials. Instead, consider a flexible approach: allocate up to 40% of your income to rent and debt combined, ensuring no single expense overwhelms your budget.

Analyzing the trade-off between rent and debt repayment reveals a critical tension. Lowering rent by moving to a cheaper area might free up funds to accelerate debt repayment, but it could also increase commuting costs or reduce access to job opportunities. Conversely, living in a more expensive area closer to work might allow you to save on transportation but leave less for debt payments. For example, if reducing rent from $1,200 to $900 frees up $300 monthly, allocating that to a credit card with a 20% interest rate could save hundreds in long-term interest. Weigh these factors based on your financial goals and lifestyle needs.

A persuasive argument for prioritizing high-interest debt over strict rent limits is the compounding cost of credit card interest. If your student loans carry a fixed 5% rate but your credit card charges 20%, paying the minimum on the former while aggressively tackling the latter is mathematically sound. For instance, a $5,000 credit card balance accrues $1,000 in interest annually at 20%, dwarfing the $250 interest on a $5,000 student loan. Redirecting even $100 from rent savings to this debt could shorten repayment timelines significantly.

Practical steps to manage this trade-off include creating a tiered budget. Start by allocating 50% of your income to needs (rent, utilities, groceries), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. Within the 20% category, prioritize debts by interest rate, focusing on credit cards first. If rent exceeds 30%, negotiate with landlords, consider roommates, or explore government housing assistance programs. For student loans, investigate income-driven repayment plans or refinancing options to lower monthly payments.

In conclusion, the rent-to-income ratio is not a one-size-fits-all rule, especially when juggling multiple debts. By adopting a holistic view of your financial obligations and making data-driven adjustments, you can strike a balance that minimizes interest costs while maintaining a livable rent. Remember, the goal is not to eliminate expenses but to optimize them for long-term financial health.

Can You Rent Highway Median Land for Business or Advertising?

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This helps ensure you have enough left for other expenses and savings.

While the 30% rule is a guideline, you may need to exceed it in high-cost areas. However, aim to keep rent as close to 30% as possible to avoid financial strain.

Multiply your gross monthly income by 0.30. For example, if you earn $4,000 per month, 30% would be $1,200.

It’s best to use your gross income (before taxes) for budgeting rent, as it provides a clearer picture of your overall earnings and helps you stay within the 30% guideline.

Consider finding a more affordable place, increasing your income, or cutting other expenses to balance your budget. Living beyond your means can lead to financial stress and debt.