Determining the maximum rent you should pay based on your salary is a crucial financial decision that ensures you maintain a healthy budget and avoid financial strain. A common rule of thumb is the 30% rule, which suggests that your rent should not exceed 30% of your gross monthly income. This guideline helps balance housing costs with other essential expenses like utilities, groceries, transportation, and savings. However, individual circumstances, such as high debt, living in an expensive city, or financial goals, may require adjusting this percentage downward. To find your max rent, calculate 30% of your monthly income and consider additional factors like local cost of living, personal priorities, and long-term financial stability.

| Characteristics | Values |

|---|---|

| General Rule (30% Rule) | Spend no more than 30% of your gross monthly income on rent. |

| 50/30/20 Budget Rule | Allocate 50% for needs (including rent), 30% for wants, and 20% for savings/debt repayment. |

| Net Income Consideration | Some experts suggest using net income (after taxes) instead of gross income for a more accurate budget. |

| Local Cost of Living | Adjust rent percentage based on local housing costs; higher in expensive cities, lower in affordable areas. |

| Debt and Financial Goals | Reduce rent percentage if you have significant debt or prioritize savings/investments. |

| Utilities and Additional Costs | Factor in utilities, parking, and other housing-related expenses when calculating affordability. |

| Emergency Fund | Ensure you have an emergency fund (3-6 months of expenses) before committing to higher rent. |

| Lifestyle and Priorities | Adjust rent based on personal priorities (e.g., living in a desirable neighborhood vs. saving more). |

| Roommates or Shared Housing | Consider roommates or shared housing to reduce rent burden if solo rent exceeds budget. |

| Negotiation | Negotiate rent or seek cheaper alternatives if your ideal rent exceeds the 30% threshold. |

Explore related products

What You'll Learn

![]()

50/30/20 Budget Rule Application

Determining your maximum rent based on salary is a critical step in financial planning, and the 50/30/20 budget rule offers a structured approach to this decision. This rule divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Housing, including rent, falls under the "needs" category, making it a cornerstone of this budgeting framework. By allocating no more than 50% of your income to essentials, you ensure that rent doesn’t overshadow other financial priorities like groceries, utilities, and transportation.

Applying the 50/30/20 rule to rent means calculating 50% of your after-tax income and ensuring your housing costs stay within that limit. For example, if your monthly take-home pay is $4,000, your total needs, including rent, should not exceed $2,000. This approach prevents overextending your budget and leaves room for discretionary spending and savings. However, it’s important to note that local cost of living and personal circumstances may require adjustments. In high-rent areas, you might need to reallocate funds from the "wants" category temporarily to cover housing costs.

A common pitfall when using this rule is underestimating the "needs" category. Rent often consumes a significant portion of this allocation, leaving less for other essentials. To avoid this, break down your needs further: list all fixed expenses like insurance, transportation, and utilities, then subtract these from the 50% allocation to determine your realistic rent limit. For instance, if your other needs total $800 monthly, your max rent should be $1,200 in the $4,000 take-home scenario.

Flexibility is key when applying the 50/30/20 rule to rent. If your ideal apartment exceeds your calculated limit, consider roommates, smaller spaces, or neighborhoods with lower rents. Alternatively, if your rent is well below the 50% threshold, redirect the surplus to savings or debt repayment, aligning with the 20% category. This rule isn’t rigid—it’s a guideline to balance housing costs with overall financial health.

Finally, the 50/30/20 rule encourages long-term financial stability by prioritizing savings and debt repayment alongside essential and discretionary spending. By capping rent at a reasonable percentage of your income, you create a sustainable budget that accommodates life’s unpredictability. Regularly review your allocations as your income or expenses change, ensuring your rent remains within the "needs" boundary while supporting your broader financial goals.

Worlds of Fun: ATV Adventures for All Abilities

You may want to see also

Explore related products

![]()

Income-Based Rent Calculators

Determining how much rent you can afford is a critical step in financial planning, and income-based rent calculators are invaluable tools for this purpose. These calculators use a simple yet effective formula, often recommending that you spend no more than 30% of your gross monthly income on rent. For example, if your monthly salary is $4,000, a calculator would suggest capping your rent at $1,200. This rule of thumb, known as the 30% rule, is widely accepted as a benchmark for financial stability, ensuring you have enough income left for other expenses like utilities, groceries, and savings.

While the 30% rule is a good starting point, income-based rent calculators often go beyond this by factoring in additional variables. Some tools consider your monthly debt obligations, such as student loans or car payments, to provide a more personalized recommendation. For instance, if you earn $5,000 monthly but have $800 in debt payments, a calculator might adjust your maximum rent downward to $1,700 instead of the standard $1,500. This tailored approach ensures that your rent doesn’t strain your overall budget, especially if you’re managing other financial commitments.

One of the most practical features of income-based rent calculators is their ability to account for regional cost-of-living differences. Rent affordability in a high-cost city like New York or San Francisco differs drastically from that in a more affordable area like Indianapolis or Memphis. Advanced calculators often prompt you to input your city or ZIP code, adjusting the 30% rule to reflect local housing market realities. For example, in a high-cost city, the calculator might suggest spending closer to 40% of your income on rent if that’s the norm, while in a low-cost area, it might recommend staying below 25%.

Using an income-based rent calculator isn’t just about finding a number—it’s about building a sustainable lifestyle. These tools often include additional features like expense trackers or savings goals to help you visualize how your rent fits into your broader financial picture. For instance, some calculators show how much you’ll have left for discretionary spending or emergencies after paying rent. This holistic view empowers you to make informed decisions, ensuring that your housing choice aligns with your long-term financial health.

Despite their utility, income-based rent calculators aren’t foolproof. They rely on the accuracy of the information you provide, so it’s essential to input your gross income, not net, and account for all recurring expenses. Additionally, these tools don’t consider unexpected costs like medical emergencies or job loss. As a practical tip, consider setting aside an emergency fund equivalent to 3–6 months of living expenses, including rent, to buffer against unforeseen circumstances. By combining the insights from these calculators with proactive financial planning, you can confidently determine your maximum rent while maintaining financial security.

Renting a PO Box Out-of-State: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Local Cost of Living Factors

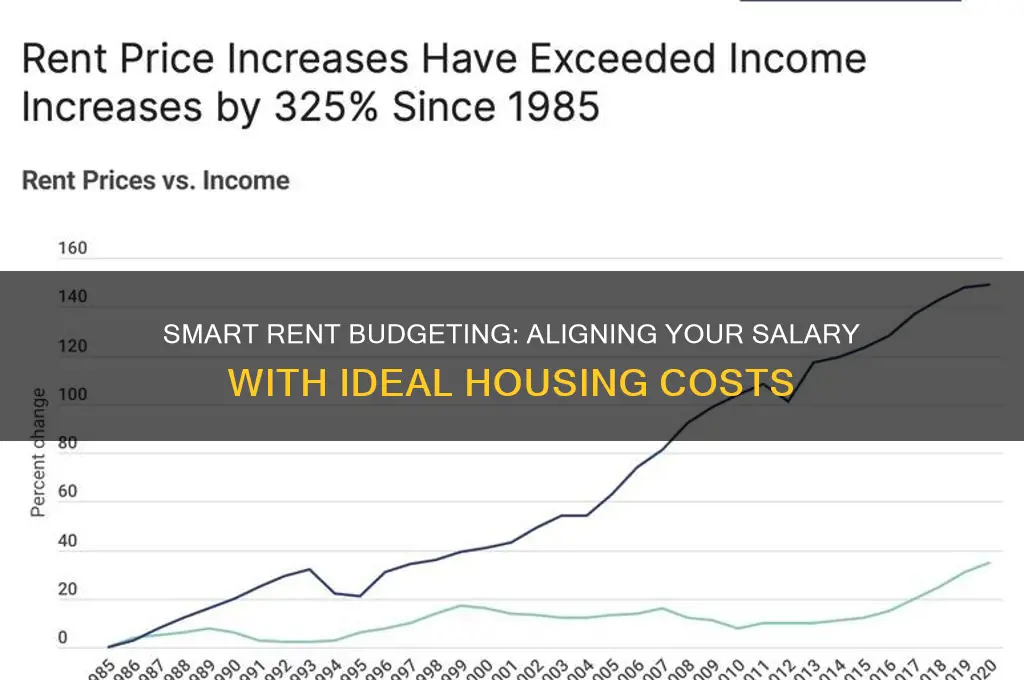

The cost of living varies dramatically by location, and this directly impacts how much of your salary you can reasonably allocate to rent. A one-bedroom apartment in San Francisco might devour 60% of your income, while the same percentage in Tulsa could secure you a spacious three-bedroom house. This disparity highlights the need to consider local factors beyond national averages when determining your max rent.

Simply put, a "one-size-fits-all" approach to rent budgeting doesn't exist.

Let's break down key local cost of living factors. Housing costs are the most obvious, but delve deeper than average rent prices. Research the availability of affordable housing options in your desired neighborhood. Are there rent control policies in place? Is there a high demand for rentals, driving prices up? Transportation costs are another major player. Do you need a car, or is public transportation reliable and affordable? Cities with robust public transit systems allow for lower car ownership costs, freeing up more of your budget for rent.

Food and utilities also vary significantly. Groceries in urban centers tend to be pricier than in suburban or rural areas. Similarly, utility costs can fluctuate based on climate and local energy prices.

To illustrate, consider two hypothetical scenarios. Imagine earning $60,000 annually. In a city with a moderate cost of living, where rent averages $1,200, transportation costs $200 monthly, and groceries are reasonably priced, you could comfortably allocate 30% of your income to rent ($1,500) while maintaining a balanced budget. However, in a high-cost city where rent averages $2,500, transportation costs $400 monthly, and groceries are expensive, that same 30% would leave you struggling to cover other essentials.

Actionable Tip: Utilize online cost of living calculators specific to your desired location. These tools factor in housing, transportation, food, and other expenses to provide a more accurate picture of affordability.

Remember, your max rent isn't just a number; it's a reflection of your lifestyle choices and the unique economic landscape of your chosen location. By carefully considering local cost of living factors, you can make an informed decision that ensures financial stability and a comfortable living situation.

Renting a Tux: Essential Checklist for a Perfect Formal Look

You may want to see also

Explore related products

![]()

Debt and Savings Considerations

High rent can shackle your financial future, especially if you're already managing debt or striving to save. Before committing to a lease, scrutinize your debt-to-income ratio (DTI), which should ideally stay below 36%. For instance, if your monthly income is $4,000, aim to keep all debt payments, including rent, under $1,440. Exceeding this threshold risks financial strain, making it harder to save or invest.

Consider your savings goals as a non-negotiable expense. Financial advisors recommend allocating at least 20% of your income to savings and investments. If your rent consumes 50% of your paycheck, you’re left with limited funds for emergencies, retirement, or other financial priorities. For example, a $3,000 monthly income with $1,500 rent leaves only $1,500 for all other expenses, including savings—a recipe for stagnation.

Student loans, credit card debt, or car payments compound the rent burden. Prioritize high-interest debt repayment while keeping rent manageable. For instance, if you owe $20,000 in student loans at 6% interest, allocate extra funds to reduce this debt rather than overspending on housing. A lower rent allows you to accelerate debt repayment, saving hundreds in interest over time.

Build an emergency fund equivalent to 3–6 months of living expenses before locking into a high rent. Unexpected costs like car repairs or medical bills can derail your finances if you’re already stretched thin. For a $3,000 monthly income, aim for $9,000–$18,000 in savings. If your rent is $1,200, you’ll have more flexibility to save than if it’s $1,800.

Finally, leverage budgeting tools like the 50/30/20 rule: 50% on needs (including rent), 30% on wants, and 20% on savings/debt. If rent exceeds 30% of your income, adjust by finding a cheaper place or increasing income. For a $4,000 salary, keep rent under $1,200 to maintain balance. Sacrificing short-term comfort for long-term financial health is a trade-off worth making.

Renting a Food Truck in NYC: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Emergency Fund Impact on Rent

A common rule of thumb suggests spending no more than 30% of your monthly income on rent. However, this guideline often overlooks the critical role of an emergency fund in shaping your financial resilience. Without a robust emergency fund, even a seemingly affordable rent can become a burden during unexpected crises. For instance, a sudden job loss, medical emergency, or car repair can force you to choose between paying rent and covering essential expenses, potentially leading to debt or eviction.

To integrate an emergency fund into your rent calculation, consider this two-step approach. First, determine your target emergency fund size, typically 3–6 months’ worth of living expenses. If you’re starting from scratch, allocate a fixed portion of your monthly income—say, 10–15%—to build this fund. Once established, subtract your monthly emergency fund contribution from your total income before calculating your rent budget. For example, if you earn $4,000 monthly and save $400 for emergencies, base your 30% rent limit on the remaining $3,600, capping rent at $1,080 instead of $1,200.

The psychological impact of an emergency fund on rent decisions is equally significant. Knowing you have a financial safety net reduces the pressure to compromise on rent affordability. It allows you to prioritize location, amenities, or housing quality without fearing financial instability. Conversely, lacking an emergency fund may tempt you to stretch your rent budget, assuming nothing will go wrong—a risky gamble that can backfire during unforeseen events.

For younger renters or those in volatile industries, a more conservative approach is advisable. Aim to keep rent below 25% of your income and accelerate emergency fund savings to 6 months’ coverage. Older renters with stable careers might opt for the 30% threshold but should ensure their emergency fund remains a non-negotiable priority. Regardless of age or income, regularly review your rent-to-income ratio and emergency fund balance to adjust for life changes, such as salary increases or rising living costs.

In practice, consider this scenario: A 28-year-old earning $50,000 annually ($4,167 monthly) decides to cap rent at 28% of their income after accounting for a $300 monthly emergency fund contribution. Their adjusted rent budget is $1,100 ($4,167 – $300 = $3,867; 28% of $3,867 = $1,083, rounded up). By prioritizing both rent affordability and emergency savings, they create a balanced financial plan that safeguards against unexpected shocks while maintaining housing stability.

Renting Without Claiming: Consequences and Risks You Need to Know

You may want to see also

Frequently asked questions

A common rule of thumb is the 30% rule, which suggests spending no more than 30% of your gross monthly income on rent. For example, if your monthly salary is $4,000, your max rent should be around $1,200.

Yes, consider your total monthly expenses, including utilities, groceries, transportation, and savings. If your other expenses are high, you may need to lower your max rent below 30% of your salary to maintain financial stability.

No, the 30% rule is a general guideline, but it may not be realistic in high-cost-of-living areas. In such cases, you may need to adjust your budget or consider roommates to keep housing costs manageable.

While a higher salary may allow for a higher rent, it’s important to reassess your budget and financial goals. Avoid increasing rent immediately; instead, prioritize saving, paying off debt, or investing before committing to a higher housing cost.